1) When the auditor suspects that fraud may be present, SAS No. 99 requires the

auditor to:

A) terminate the engagement with sufficient notice given to the client

B) issue an adverse opinion or a disclaimer of opinion

C) obtain additional evidence to determine whether material fraud has occurred

D) re-issue the engagement letter

2) The most commonly used method of statistical sampling for tests of details of

balances is:

A) attributes sampling

B) systematic sampling

C) discovery sampling

D) monetary-unit sampling

3) Quality controls are established for the entire CPA firm whereas GAAS are

applicable to the individual engagement.

A) True

B) False

4) The accounts payable department usually has responsibility for approving

acquisitions for payment by comparing the details on the:

A) vendor’s invoice and the receiving report

B) vendor’s invoice and the purchase requisition

C) purchase order, receiving report, and vendor’s invoice

D) purchase requisition, purchase order, and receiving report

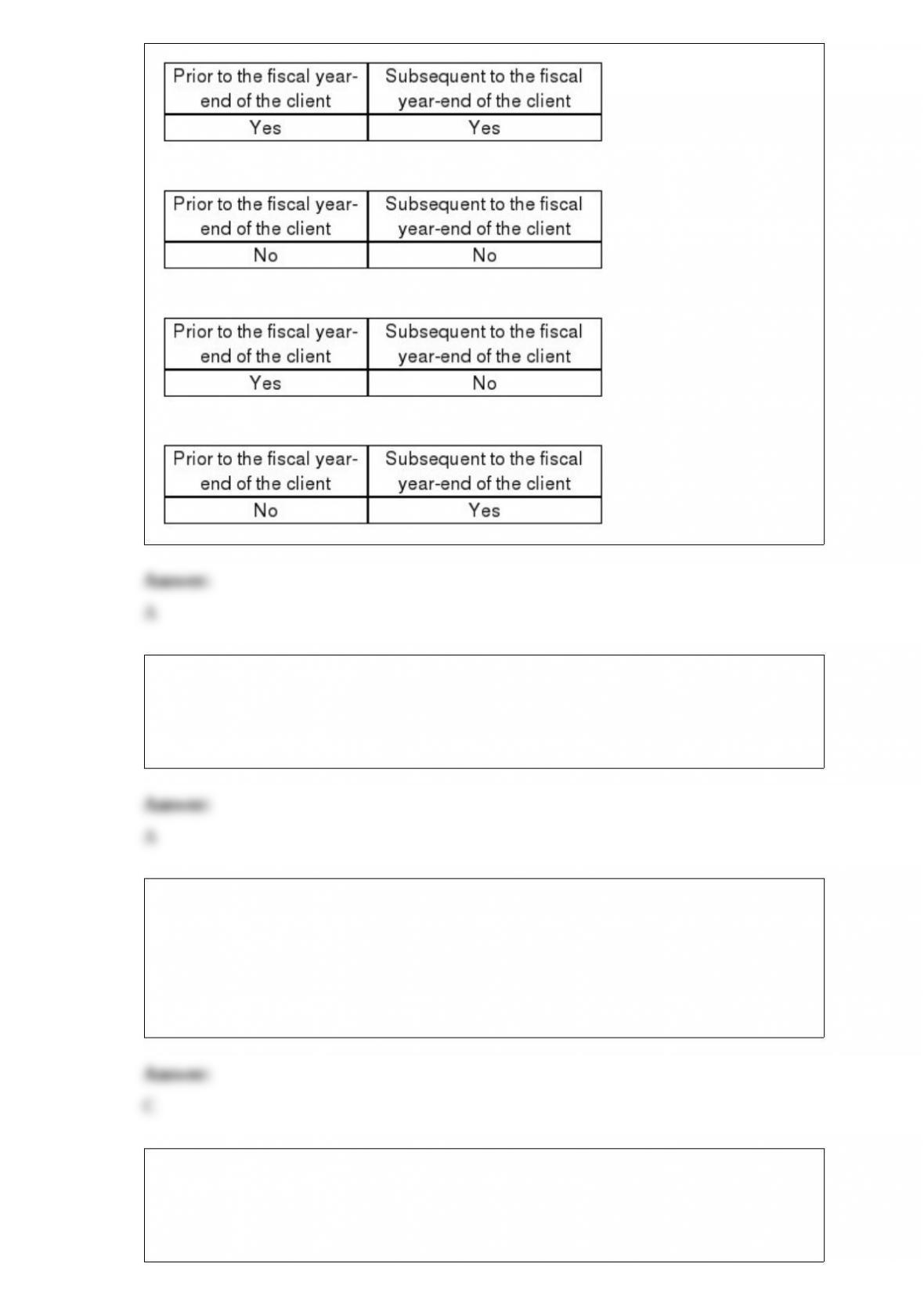

5) Audit procedures are concerned with the nature, extent, and timing in gathering audit

evidence. Which, of the following, is true as to the timing of audit procedures?

A)

B)

C)

D)

6) The tolerable exception rate is the rate that the auditor will permit in the population

and still be willing to conclude a control is effective.

A) True

B) False

7) The auditor is responsible for communicating significant internal control deficiencies

to the audit committee, or those charged with governance. This communication:

A) may be oral or written

B) must be oral

C) must be written

D) must be oral via direct communication

8) In determining the level of audit efficiency, once the auditor has identified the key

internal controls and identified any deficiencies in order to determine the level of

control risk appropriate for a private company client, it is appropriate to decide

whether:

A) substantive tests can be reduced sufficiently to justify costs of performing tests of

controls

B) substantive tests can be increased sufficiently to justify costs of performing tests of

controls

C) tests of controls can be increased sufficiently to justify costs of performing

substantive tests

D) tests of controls can be reduced sufficiently to justify costs of performing

substantive tests

9) In a CPA firm operating as a limited liability partnership (LLP), the liability for one

partner’s actions does extend to the firm’s assets.

A) True

B) False

10) When performing audit tests of pricing and compilation for inventory, the client’s

perpetual inventory master file may be used in place of vendors’ invoices if controls

over the perpetual inventory master file are adequate.

A) True

B) False

11) Under which of the following circumstances would an auditor be most likely to

intensify an examination of a $500 imprest petty cash fund?

A) Reimbursement occurs twice each week

B) The custodian endorses reimbursement checks

C) Reimbursement vouchers are not prenumbered

D) The custodian occasionally uses the cash fund to cash employee checks

12) The same three defenses available to auditors in common lawsuits by third

parties-non-negligent performance, lack of duty, and absence of causal connectionare

also available for suits under the Securities Exchange Act of 1934 .

A) True

B) False

13) The United States Supreme Court has ruled that outside professionals such as

accountants who don’t help run corrupt businesses cannot be sued under the provisions

of the Foreign Corrupt Practices Act.

A) True

B) False

14) Before goods are shipped on account, a properly authorized person must:

A) prepare the sales invoice

B) approve the journal entry

C) approve the customer’s credit

D) verify that the unit price is accurate

15) Financial statement users often receive unreliable financial information from

companies. Which of the following is not a common reason for this?

A) Complex exchange transactions

B) Voluminous data

C) Remoteness of information

D) Each of these choices is a common reason for unreliable financial information

16) Match six of the terms (a-l) with the definitions provided below (1-6):

a.Acceptable risk of incorrect acceptance

b.Acceptable risk of incorrect rejection

c.Difference estimation

d.Misstatement bounds

e.Monetary-unit sampling

f.Mean-per-unit estimation

g.Point estimate

h.Probability proportional to size sample selection

i.Ratio estimation

j.Statistical inferences

k.Stratified sampling

l.Variable sampling

________ 1> Conclusions drawn from sample results based on knowledge of sampling

distributions.

________ 2> Sampling techniques for tests of details that use the statistical inference

processes.

________ 3> The risk that the auditor is willing to take of concluding a balance is

materially misstated when it is, in fact, fairly stated.

________ 4> A statistical sampling method that provides upper and lower misstatement

bounds expressed in monetary amounts.

________ 5> A method of variables sampling in which the auditor estimates the

population misstatement by multiplying the average misstatement in the sample by the

total number of population items and also calculates sampling risk.

________ 6> The risk that the auditor is willing to take of accepting a balance as

correct when the true misstatement in the balance is greater than tolerable misstatement.

17) The partnership of Booth & Haynes, CPAs, has been engaged to examine the

financial statements of Paul, Inc., in connection with the registration of Paul’s securities

with the Securities and Exchange Commission. Under these circumstances, which of

the following statements is true?

A) Booth & Haynes is assuming much greater third-party liability than it assumes on

engagements under common law

B) If its examination is not fraudulent, Booth & Haynes may issue an appropriate

disclaimer to the financial statements and thereby avoid liability

C) Booth & Haynes must incorporate if they wish to practice before the SEC

D) Booth & Haynes must be a large interstate firm if they wish to practice before the

SEC

18) Amounts involving fraud are usually considered ________ important than

unintentional errors of equal dollar amounts.

A) less

B) no less

C) no more

D) more

19) Which of the following audit tests form the basis for an auditor’s report on internal

control over financial reporting?

A) Analytical procedures

B) Tests of transactions

C) Tests of controls

D) Tests of details of balances

20) The auditor must extend the audit procedures in the audit of year-end cash when

there are inadequate internal controls.

A) True

B) False

21) Auditors must maintain control of confirmations until they are returned from the

customer.

A) True

B) False

22) The record of the issuance and repurchase of capital stock for the life of the

corporation is maintained in the:

A) shareholders’ capital stock master file

B) capital stock certificate record

C) schedule of stock owners

D) corporate directory

23) In comparing management fraud with employee fraud, the auditor’s risk of failing to

discover the fraud is:

A) greater for management fraud because managers are inherently more deceptive than

employees

B) greater for management fraud because of management’s ability to override existing

internal controls

C) greater for employee fraud because of the higher crime rate among blue collar

workers

D) greater for employee fraud because of the larger number of employees in the

organization

24) The most important consideration in evaluating the fairness of the amounts accrued

for vacation pay, sick pay, and other benefits is the:

A) consistent accrual of these liabilities relative to those of preceding periods

B) actual expense incurred for the prior period

C) amount expended to date in the current period

D) profitability of the client which will enable these liabilities to be met

25) The Sarbanes-Oxley Act applies to which of the following companies?

A) All companies

B) Privately held companies

C) Public companies

D) All public companies and privately held companies with assets greater than $500

million

26) An auditor performs a test to determine whether all merchandise for which the

client was billed was received. The population for this test consists of all:

A) merchandise received

B) vendors’ invoices

C) canceled checks

D) receiving reports

27) Analytical procedures must be performed in:

A) the planning and test of control stages

B) conjunction with tests of transactions and tests of details of balances

C) the planning and completion stages

D) the planning, test of control, and completion stages

28) The permanent files included as part of audit documentation do not normally

include:

A) a copy of the current and prior years’ audit programs

B) copies of articles of incorporation, bylaws and contracts

C) information related to the understanding of internal control

D) results of analytical procedures from prior years

29) CPAs may provide bookkeeping services to their non-public audit clients, but there

are a number of conditions that must be met if the auditor is to maintain independence.

Which of the following conditions is not necessary?

A) The CPA must not assume a management role or function

B) The client must hire an external CPA to approve all of the journal entries prepared by

the auditor

C) The auditor must comply with GAAS when auditing work prepared by his/her firm

D) The client must accept responsibility for the financial statements

30) A substantive test of transactions commonly used to test the completeness objective

for acquisitions is “Trace from a file of receiving reports to the acquisitions journal.”

A) True

B) False

31) An effective procedure to test the existence objective for sales is to vouch sales

journal entries to copies of sales orders, shipping documents, and sales invoices.

A) True

B) False

32) Confirmation of accounts receivable balances normally provides evidence

concerning the:

A) valuation of the balances

B) rights of the balances

C) existence of the balances

D) completeness of the balances

33) To prevent fraud, management should deny cash access to anyone responsible for:

A)

B)

C)

D)

34) Items that materially affect the comparability of financial statements generally

require disclosure in the footnotes. If the client refuses to properly disclose the item, the

auditor will most likely issue:

A) a disclaimer

B) an unqualified opinion

C) a qualified opinion

D) an adverse opinion

35) Which is the following is most correct regarding the distinction(s) between the

auditor’s responsibilities for searching for errors and fraud.

A) little

B) a significant

C) no

D) various

36) Sarbanes-Oxley and the Securities Exchange Commission restrict auditors from

providing many consulting services to their publically traded audit clients.

A) True

B) False

37) When expressing an unqualified opinion, the auditor who evaluates the audit

findings should be satisfied that the:

A) amount of known misstatement is documented in the management representation

letter

B) estimate of the total known and likely misstatements is less than a material amount

C) estimate of the total likely misstatement includes sample error

D) amount of known misstatement is acknowledged and recorded by the client

38) When using the cycle approach to segmenting the audit, the reason for treating

capital acquisition and repayment separately from the acquisition of goods and services

is that:

A) the transactions are related to financing a company rather than to its operations

B) most capital acquisition and repayment cycle accounts involve few transactions, but

each is often highly material and therefore should be audited extensively

C) both A and B are correct

D) neither A nor B is correct