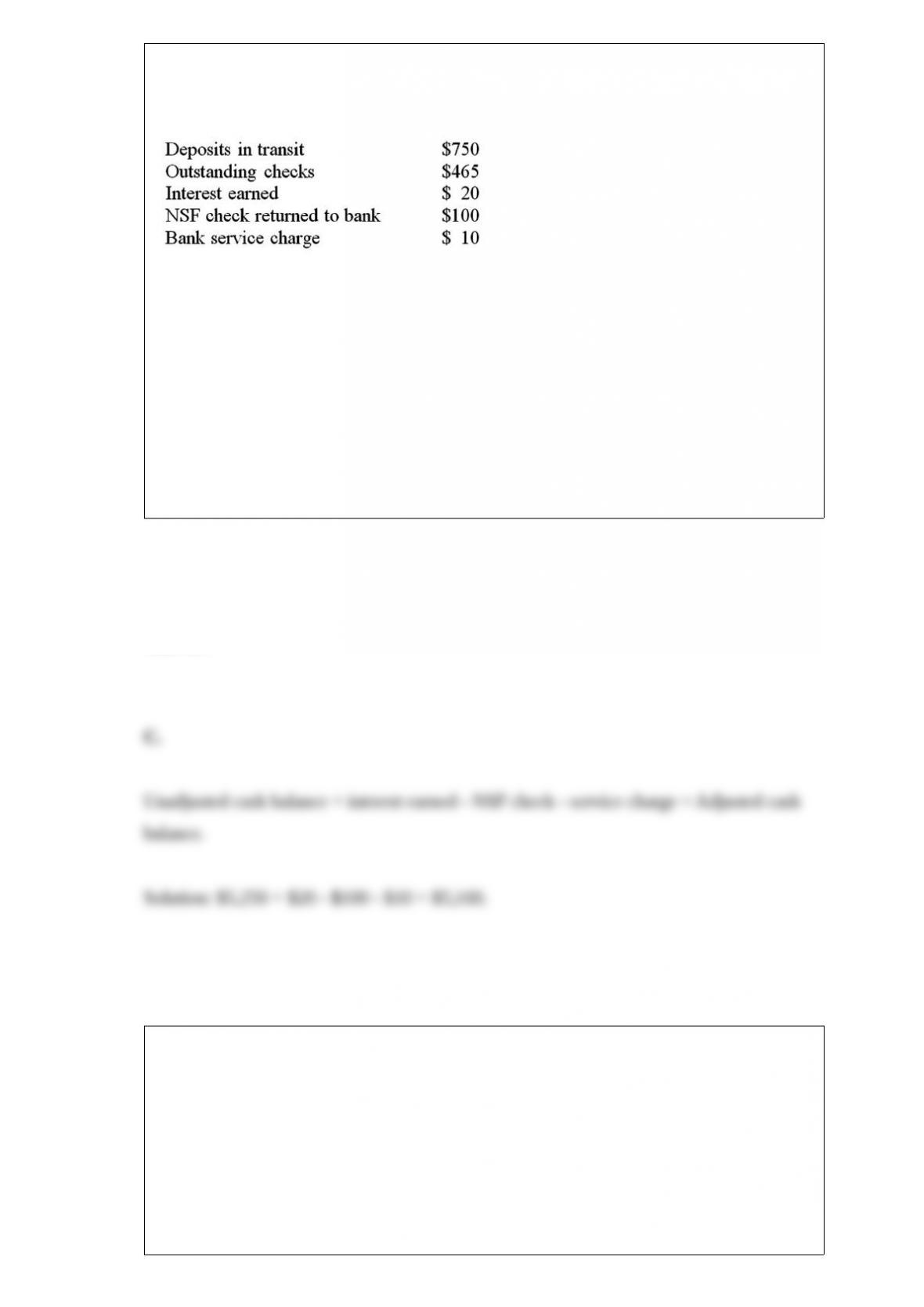

Before reconciling to its bank statement, Lauren Cosmetics Corporation’s general ledger

had a month-end balance in the cash account of $5,250. The bank reconciliation for the

month contained the following items:

Given the above information, what adjusted cash balance should Lauren report at

month-end?

A. $4,500.

B. $4,820.

C. $5,160.

D. $5,590.

Answer:

When a company uses the direct method to determine the cash flows from operating

activities, cash flows from operating activities will:

A. be identical to the amount reported using the indirect method.

B. be larger if there is a net cash inflow and smaller if there is a net cash outflow

compared to the amount reported using the indirect method.

C. always be larger than the amount reported using the indirect method.

D. be larger if there is a net cash outflow and smaller if there is a net cash inflow

compared to the amount reported using the indirect method.

Answer:

Which of the following statements regarding the trial balance is correct?

A. The adjusted trial balance is prepared after the financial statements to verify that the

numbers are accurate.

B. The primary purpose of the post-closing trial balance is to see whether revenues are

greater than expenses.

C. The adjusted trial balance is a check that the accounting records are still in balance

after posting all adjustments to the accounts.

D. The post-closing trial balance debit column total is the amount to be shown as Total

Assets on the Balance Sheet.

Answer:

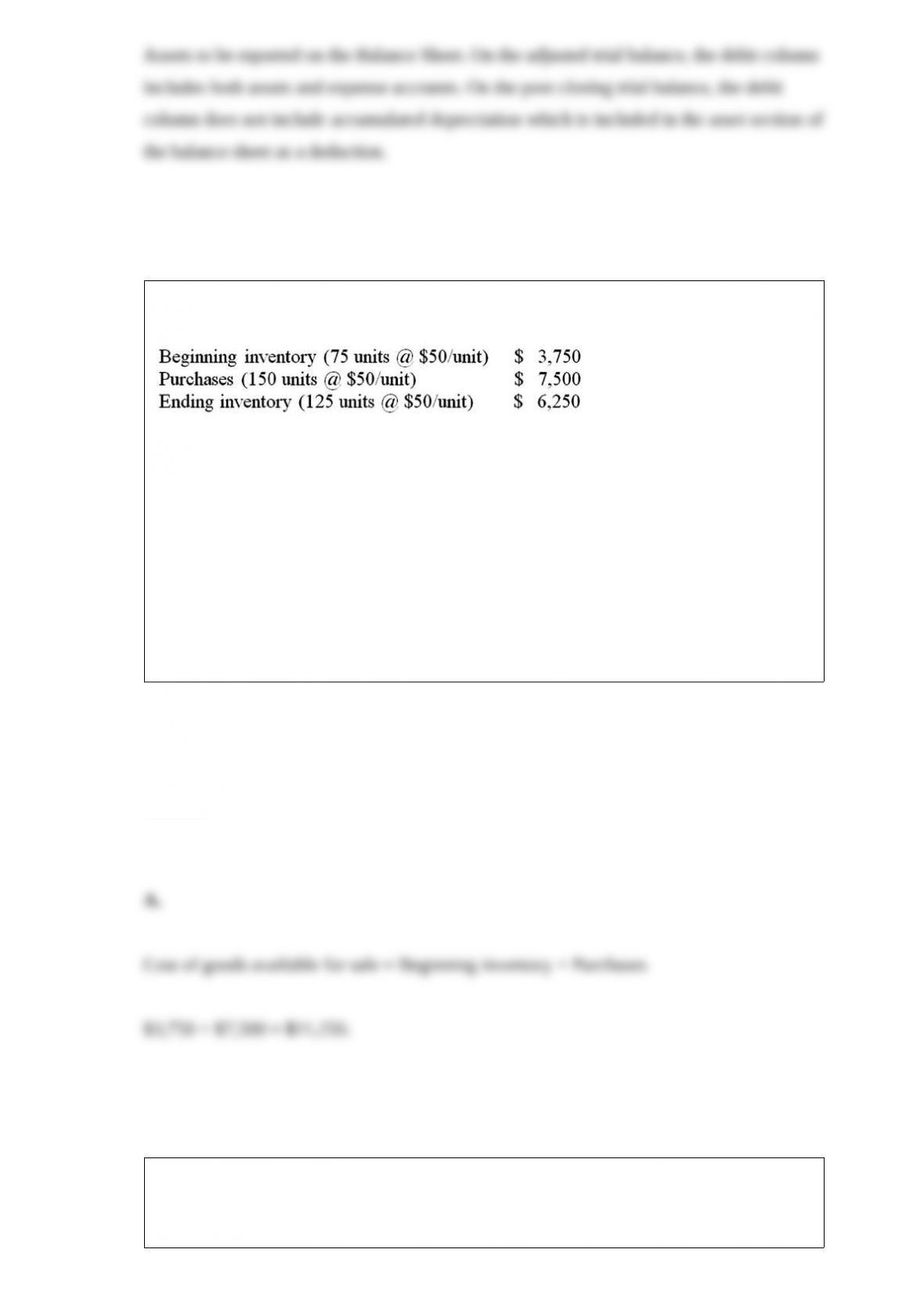

FAD Company uses a periodic inventory system and its inventory records for the period

contain the following information:

Use the information above to answer the following question. What is the amount of cost

of goods available for sale?

A. $11,250

B. $17,500

C. $5,000

D. $13,750

Answer:

Which of the following activities would not affect the inventory account for a company

that uses the perpetual inventory system?

A. Purchases

B. Purchase returns

C. Advertising

D. Freight-in

Answer:

Match the characteristic of the company with the description of the type of company.

A. Partnership.

B. Publicly traded corporation.

C. Privately traded corporation.

D. Sole Proprietorship.

_____ 1/ Issues shares of stock that are traded on a stock exchange such as the NYSE.

_____ 2/ The owners of the business are personally liable for the debts of the company.

_____ 3/ Shares of stock must be purchased directly from current owners.

_____ 4/ Can raise more financial capital by selling stock to the greatest number of

investors.

_____ 5/ The easiest form of business to start.

_____ 6/ The business ceases to exist upon the departure of one of the owners.

_____ 7/ The owners pay taxes on the profits of the business.

Answer:

Which of the following is calculated by dividing net sales by average total assets?

A. Net profit margin.

B. Fixed asset turnover.

C. Asset turnover ratio.

D. Current ratio.

Answer:

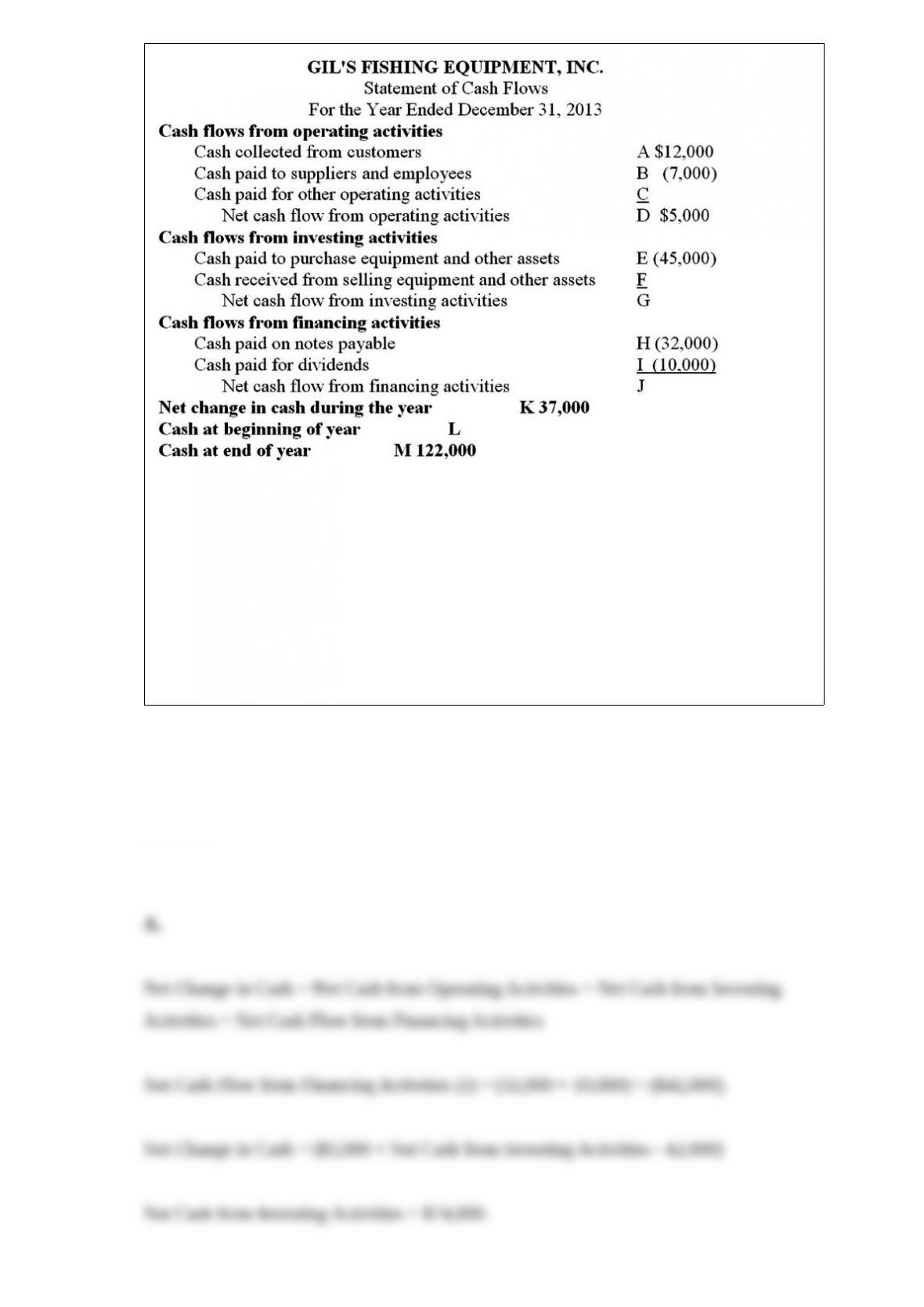

In the above statement of cash flows, what amount is represented by letter J?

A. ($42,000)

B. $42,000

C. ($22,000)

D. $22,000

Answer:

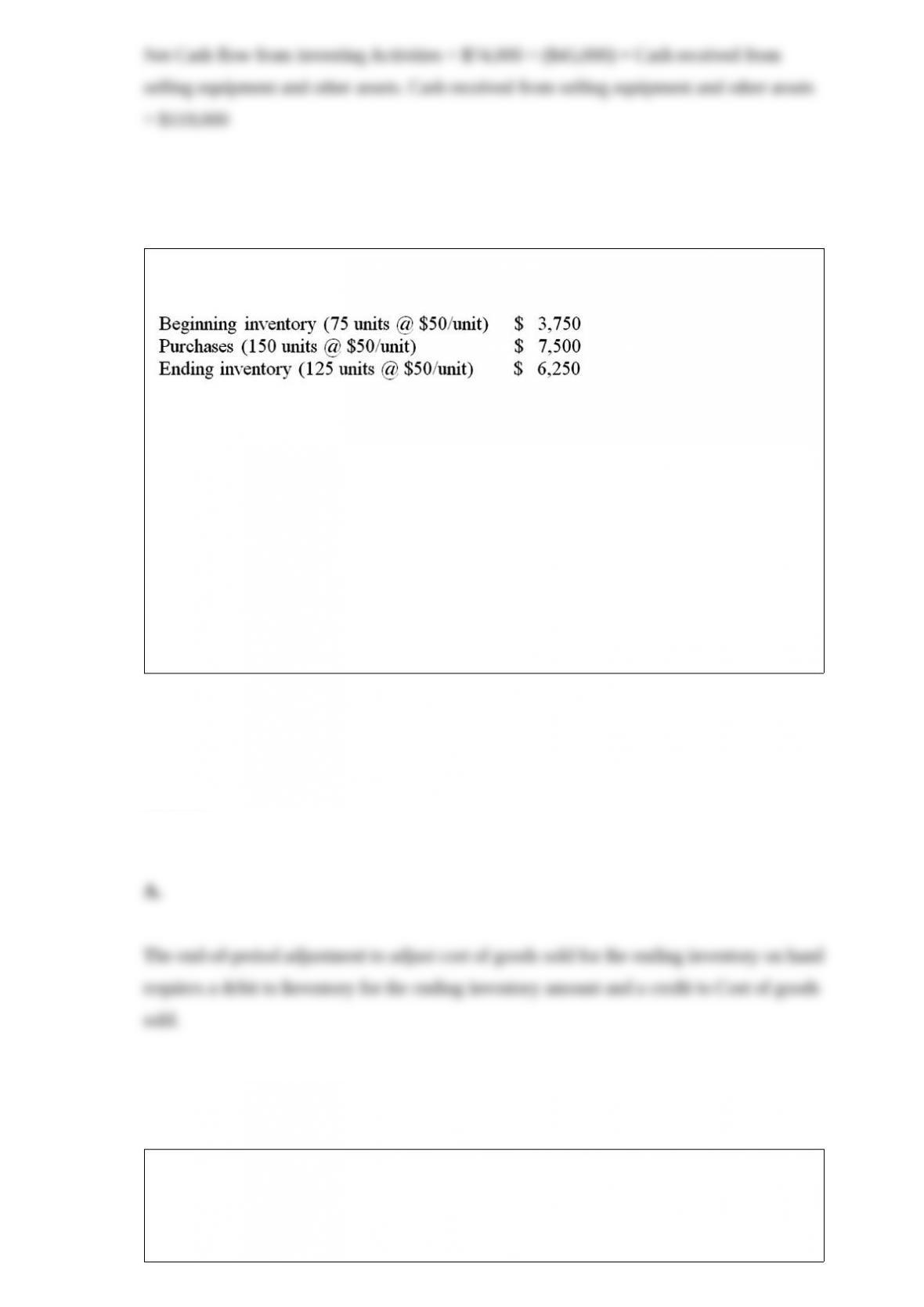

FAD Company uses a periodic inventory system and its inventory records for the period

contain the following information:

Use the information above to answer the following question. The journal entry

necessary at the end of the period to adjust cost of goods sold for the ending inventory

still on hand will include which of the following?

A. Debit Inventory, $6,250.

B. Credit Cost of goods sold, $11,250.

C. Credit Purchases, $10,200.

D. Credit Inventory, $5,000.

Answer:

An example of an accrued revenue is

A. accumulated interest on a note receivable.

B. accumulated interest on a note payable.

C. unearned revenue.

D. accounts receivable.

Answer:

The costs assigned to the individual assets acquired in a basket purchase is based on

their relative

A. historical costs.

B. market values.

C. book values.

D. depreciable costs.

Answer:

Which of the following sequences indicates the correct order of steps in the accounting

cycle?

A. T-accounts, journal entries, trial balance, financial statements.

B. T-accounts, journal entries, financial statements, trial balance.

C. Journal entries, T-accounts, trial balance, financial statements.

D. Journal entries, T-accounts, financial statements, trial balance.

Answer:

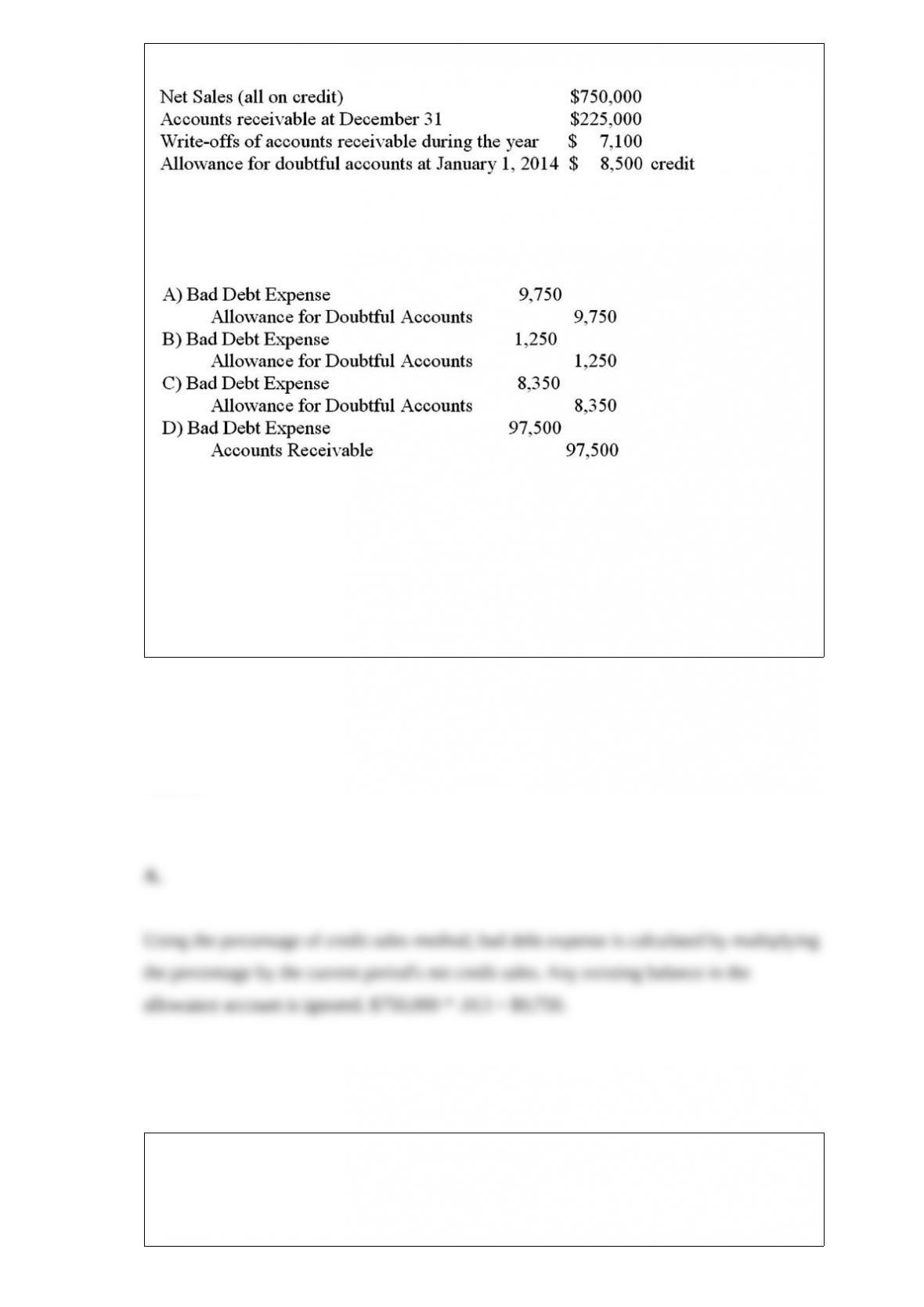

Geisel, Inc had credit sales for 2014 of $510,000. and sales returns of $10,000. Credit

sales for 2013 were $610,000 and sales returns were $10,000. Accounts receivable on

December 31, 2014 were $148,000. The allowance for doubtful accounts at December

31, 2014 before adjustment had a debit balance of $1,000. Bad debt expense of $6,000

was recorded for 2014.

a. Calculate the accounts receivable turnover ratio and the days to collect for 2013 and

2014 (round each calculation to one decimal place).

The net receivables balance reported on the company’s 12/31/12 financial statements

was $120,000. The net receivables balance reported on the 12/31/13 financial

statements was $130,000.

b. Discuss the implications of the receivables turnover ratio and days to collect as

calculated in part (a). Discuss possible reasons for any changes in the values for these

ratios, and implications for the provision for uncollectible accounts.

Answer:

Your company has 500 units in inventory that had been purchased for $12 each and that

would currently cost $15 to replace. Your supplier has just announced the cost of these

goods is rising to $16.50.

A. Your company should make no adjustments to the inventory account.

B. Your company should adjust the inventory account using the lower of the recent

market values, which is $15.

C. Your company should adjust the inventory account using the cost, which is $12.00.

D. Your company should adjust the inventory account using the average of the recent

market values, which is $14.50.

Answer:

The debt-to-assets ratio is the:

A. ratio of current liabilities to current assets.

B. ratio of long term liabilities to fixed assets.

C. ratio of total liabilities to total assets.

D. proportion of short-term liabilities to total liabilities.

Answer:

On the 15th of the month, a company receives $8,000 in payments from customers.

$1,000 is for services performed on that day and the remaining is payment for services

performed in the previous month. The $8,000 cash receipt would be recorded as a:

A. debit of $7,000 to Accounts Receivable, debit of $1,000 to Service Revenue, and a

credit of $8,000 to Cash.

B. debit of $8,000 to Cash, a credit of $7,000 to Accounts Receivable, and a credit of

$1,000 to Service Revenue.

C. debit of $7,000 to Accounts Receivable, a debit of $1,000 to Unearned Revenue, and

a credit of $8,000 to Cash.

D. debit of $8,000 to Cash, debit of $1,000 to Service Revenue, and a credit of $7,000

to Accounts Receivable.

Answer:

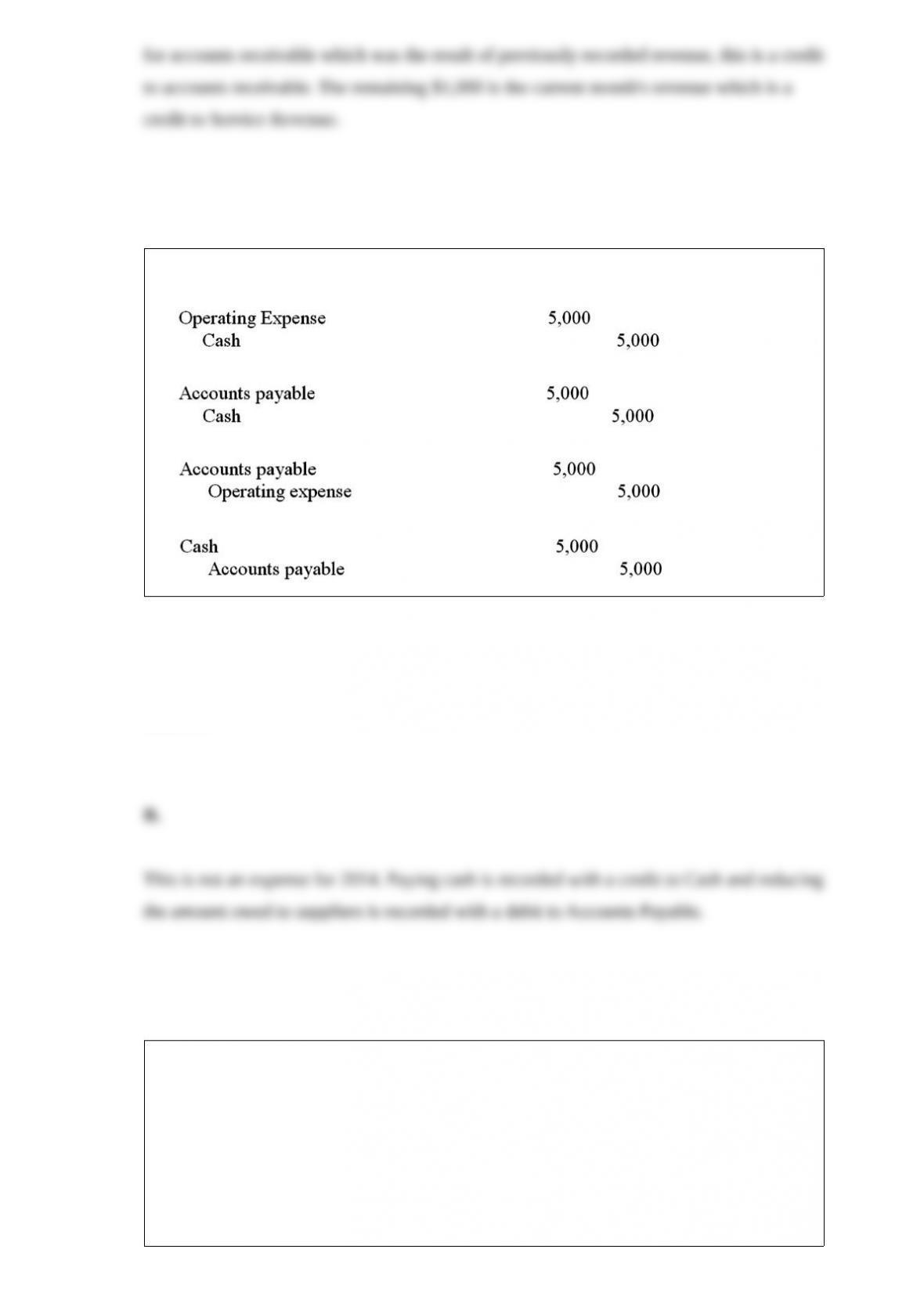

Which of the following is the journal entry to record activity #4?

A.

B.

C.

D.

Answer:

Companies using a perpetual inventory system:

A. never physically count their inventory.

B. must count their inventory at least once a week.

C. still need to count the inventory at the end of the period.

D. always know the actual amount in inventory from their accounting records.

Answer:

The direct write-off method for uncollectible accounts:

A. ignores the matching principle.

B. is an acceptable alternative method of recognizing bad debt expense under GAAP.

C. results in higher bad debt expense for most companies.

D. may only be used by companies that do not extend credit to their customers.

Answer:

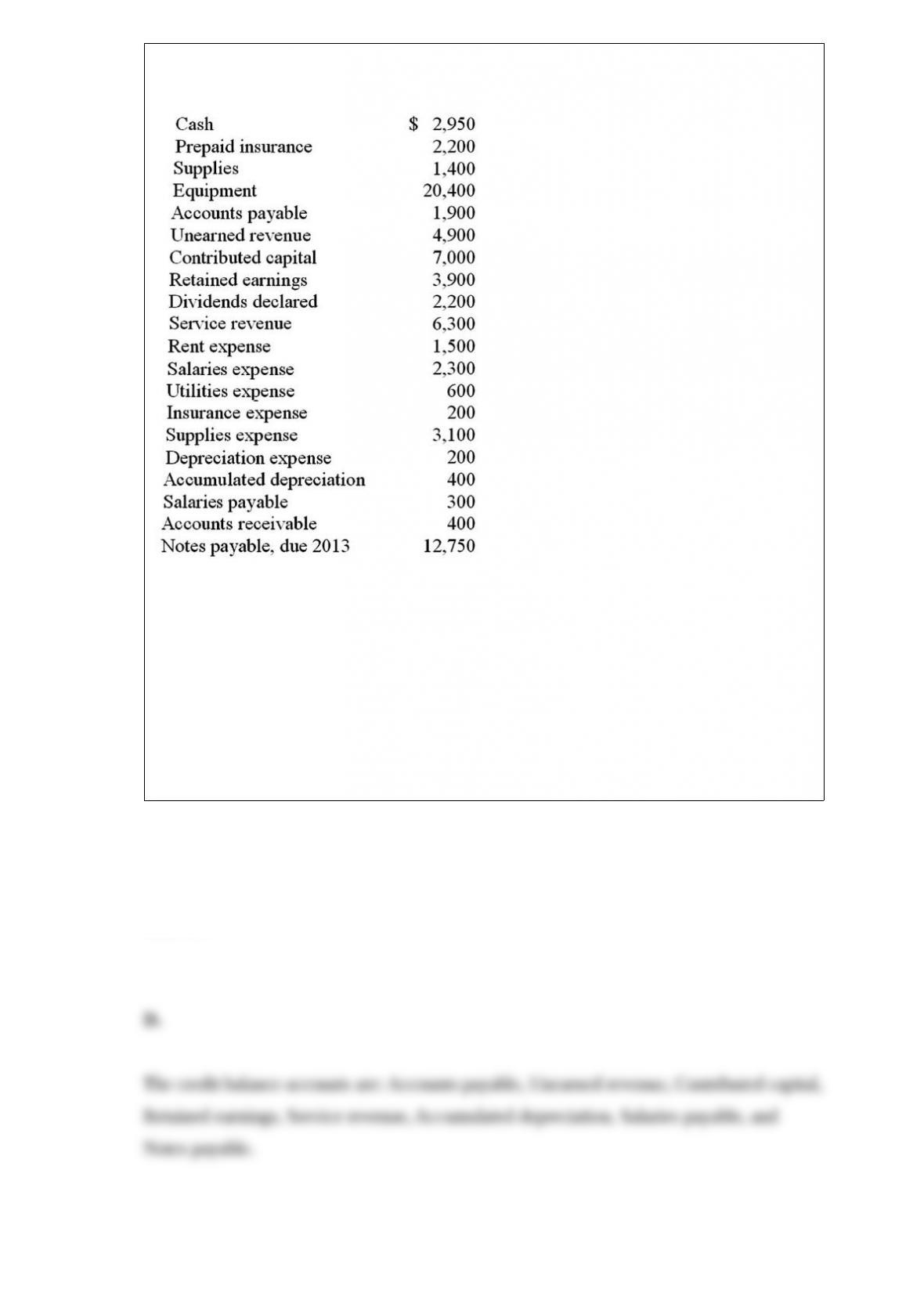

The following items are taken from the adjusted trial balance prepared as of December

31, 2013. All accounts have normal balances.

What is the total of the credit column of the adjusted trial balance?

A. $24,700

B. $37,050

C. $74,900

D. $37,450

Answer:

A current dividend preference means that:

A. preferred stockholders are paid current dividends before common stockholders are

paid dividends.

B. unpaid dividends to preferred stockholders accumulate and must be paid before

common stockholders receive dividends.

C. preferred stockholders are paid their full fixed dividend rate each period as long as

the company is in operation.

D. unpaid cash dividends to preferred stockholders must be replaced with stock

dividends during the current period.

Answer:

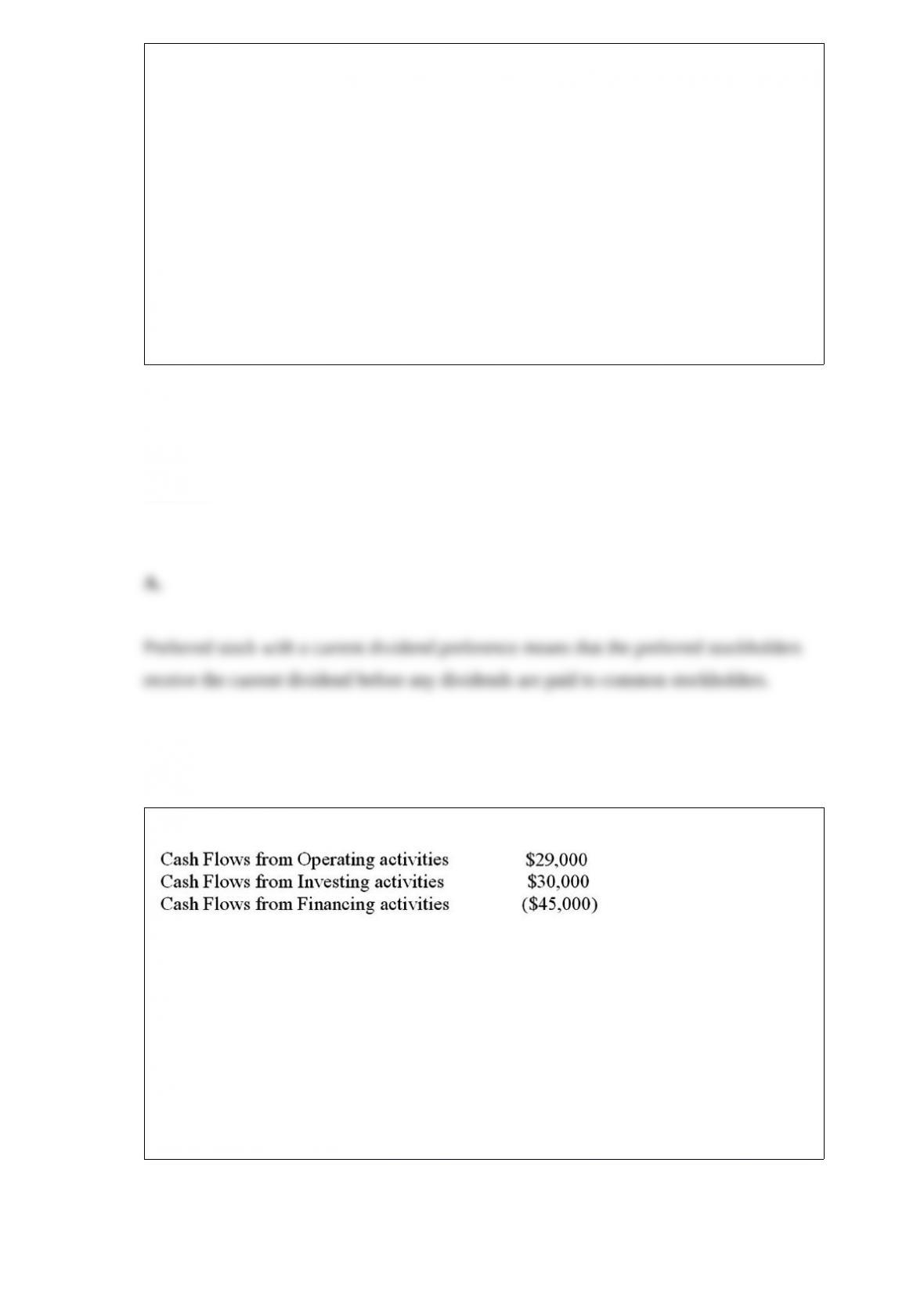

The statement of cash flows for a company contained the following:

What was the change in cash for the period?

A. $14,000 increase

B. $15,000 increase

C. $14,000 decrease

D. $15,000 decrease

Answer:

Use the information above to answer the following question. What is the inventory

turnover for 2014?

A. 3.87

B. 4

C. 4.14

D. 2

Answer:

At December 31, 2014, a company’s records include the following:

Use the information above to answer the following question. Assuming the company

estimates bad debts as 1.3% of credit sales, what is the required adjusting entry to

record bad debt expense for the year?

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

The inventory turnover ratio is calculated as:

A. Cost of goods sold divided by Sales.

B. Cost of goods sold divided by Average inventory.

C. Ending inventory divided by Cost of goods sold.

D. Average inventory divided by Cost of goods sold.

Answer:

On July 1, 2014, Icespresso Inc. signed a two-year $8,000 note receivable with 9

percent interest. At its due date, July 1, 2016, the principal and interest will be received

in full. Interest revenue should be reported on Icepresso’s income statement for the year

ended December 31, 2014, in the amount of:

A. $1,440.

B. $720.

C. $420.

D. $360.

Answer:

A legal document called a stock certificate is used to indicate ownership in a

A. Corporation

B. Sole proprietorship

C. Partnership

D. Both sole proprietorship and partnership

Answer:

A company issued $300,000, 10-year, 10 percent bonds at 105.

Use the information above to answer the following question. What is the total amount

of interest expense that will be recorded over the life of these bonds?

A. $300,000

B. $285,000

C. $315,000

D. $330,000

Answer:

Which of the following ratios is calculated by dividing liquid assets by current

liabilities?

A. Current ratio.

B. Quick ratio.

C. Turnover ratio.

D. Working capital ratio.

Answer:

A company was recently formed with $60,000 cash contributed to the company by its

owners. The company then borrowed $30,000 from a bank and bought $10,000 of

inventory and paid cash for it. The company also purchased $70,000 of equipment by

paying $10,000 in cash and issuing a note for the remainder.

What is the amount of the total liabilities to be reported on the balance sheet?

A. $60,000

B. $0

C. $90,000

D. $80,000

Answer:

Which of the following ratios is calculated by dividing current assets by current

liabilities?

A. Quick ratio.

B. Solvency ratio.

C. Debt ratio.

D. Current ratio.

Answer:

Choose the appropriate letter to match the term and the definition. Not all definitions

will be used.

Term:

_____ 1/ Date of declaration

_____ 2/ Issued shares

_____ 3/ Seasoned new issues

_____ 4/ Pro rata basis

_____ 5/ Date of record

_____ 6/ Additional paid-in capital

_____ 7/ Outstanding shares

_____ 8/ Stock options

_____ 9/ Payment date

Definition:

A. The date on which a company authorizes a dividend payment.

B. The total number of shares currently owned by stockholders.

C. When cash or stock dividends are issued according to the proportion of stock owned.

D. Dividends that have not had income tax withheld from them.

E. The date on which a company determines who receives a dividend.

F. When employees of a company have the opportunity to buy a company’s stock in the

future at a fixed price.

G. The accumulation of all the past dividends the company has not paid.

H. When a company sells issues of stock after its IPO.

I. The date on which a company debits dividends payable and credits cash.

J. When cash or stock dividends are issued in an equal dollar or share amount per

stockholder.

K. The date on which a liability is recorded for a dividend.

L. The total number of shares the company has sold, whether held by stockholders or by

the company.

M. When owners of the company contribute additional capital beyond what they paid

for their stock.

N. The amount owners paid the issuer for the stock above the par value of the stock.

Answer:

Limited liability companies (LLCs) are like general partnerships in that:

A. income tax is not paid by the company itself.

B. the business exists separate from its owners.

C. liability is limited.

D. amounts paid to the owners are recorded as salaries expense.

Answer: