Prepaid Insurance is an expense account which is used for recording expenses that have

been paid in advance.

In the partnership form of business, the owners of a business are called shareholders.

The Accounts Payable ledger has a controlling account in the General Ledger and a

separate subsidiary account for each creditor in the Accounts Payable ledger.

Notes receivable do not require a subsidiary ledger.

For a partnership, the equity section is called Shareholders Equity.

A balance sheet covers a period of time such as a month or year.

Because inventory errors are self-correcting in following accounting periods, managers

will be able to make correct decisions based on changes in net income and cost of

goods sold.

In a double-entry accounting system, total debits must always equal total credits.

The direct write-off method of accounting for bad debts records the loss from an

uncollectible account receivable at the time it is determined to be uncollectible.

When a single goods and services tax (GST) or Harmonized Sales Tax (HST) account is

used, a debit balance in the account means the government owes money to the business.

Incidental costs added to the value of inventory include import duties, transportation-in,

storage, and insurance.

The three methods of inventory valuation that are most often used in Canada are

specific identification, FIFO, and (moving) weighted average.

The person that borrows money and signs a promissory note is called the payee.

Toys “R” Us had cost of goods sold of $6,900 million. Its ending inventory was $2,000

million. Therefore its days’ sales in inventory was 90 days.

A general journal entry usually includes information about the date of a transaction,

titles of affected accounts, dollar amount of each debit and credit and an explanation of

the transaction.

The accounting equation can be expressed as liabilities = assets – equity.

The first section of the income statement reports cash from operating activities.

A wholesaler is a company that buys products from manufacturers and sells them to

consumers.

An error in valuing inventory will cause an error in the amount of cost of goods sold.

The accrual basis of accounting is a system of accounting in which the adjustment

process is used to assign revenues to the periods in which they are earned and to match

expenses with revenues.

The accounting cycle refers to the steps in preparing the work sheet for users.

A schedule of accounts receivable is a listing of all creditor accounts and account

balances.

A classified multiple-step income statement is a format that shows intermediate totals

between sales and net income and detailed calculations of net sales and cost of goods

sold.

The business entity principle requires that an owner keep accounting records separate

from personal records or records of any other businesses owned.

Depreciation expense is an example of accrued expense.

The Accounting Standards Board (AcSB), is the body that developed the International

Financial Reporting Standards.

Asset accounts normally have credit balances and expense accounts normally have

debit balances.

Earned but uncollected revenues that are recorded during the adjusting process, with a

credit to a revenue account and a debit to an expense account, are referred to as accrued

expenses.

A company’s cost of merchandise available for sale consists of beginning inventory plus

the net cost of purchases minus ending inventory.

The choice of an inventory cost flow assumption can have a dramatic impact on

amounts in financial statements.

Y-Mart had sales of $350,000. Its cost of goods sold was $200,000. Its gross profit was

$550,000.

An account is a detailed record of increases and decreases in a specific asset, liability or

equity item.

Because they decrease equity, withdrawals made by a business owner are credited to

his/her withdrawals account.

Augusto Diaz borrowed $1,000 and signed a 6-month promissory note at 11% interest.

The total amount of interest is $110.00.

An advantage of the moving weighted-average method is that it tends to smooth out

price changes.

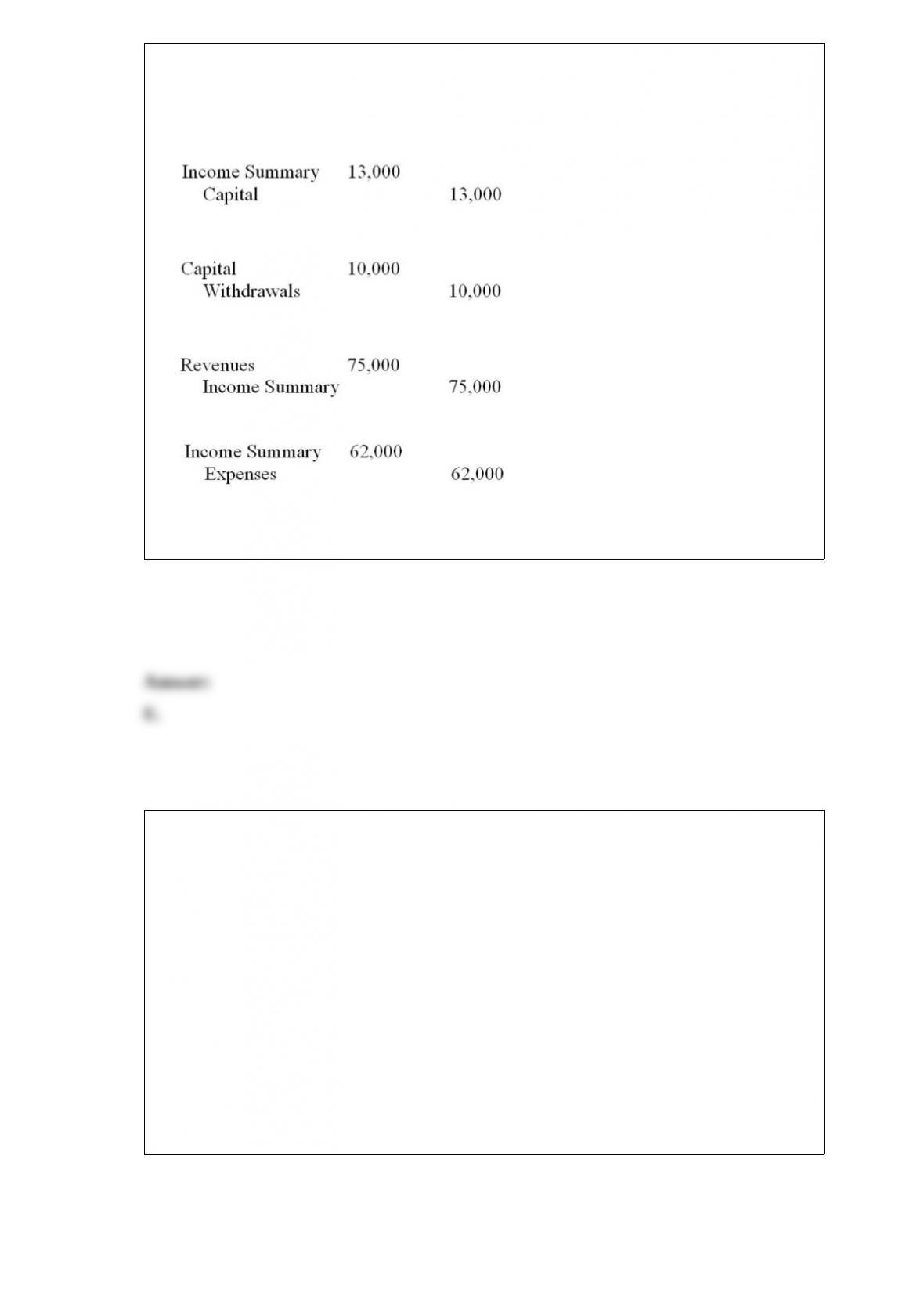

A company had revenues of $75,000, withdrawals of $10,000 and expenses of $62,000

during an accounting period. Which of the following entries should not be journalized

in the closing process?

A.

B.

C.

D.

E. All of these should be journalized in the closing process.

The rule that (1) requires revenue to be recognized at the time it is earned, (2) allows

the inflow of assets associated with revenue to be in a form other than cash, and (3)

measures the amount of revenue as the cash plus the cash equivalent value of any

noncash assets received from customers in exchange for goods or services is called the:

A. Going concern principle.

B. Cost principle.

C. Revenue recognition principle.

D. Monetary unit principle.

E. Business entity principle.

The current ratio:

A. Is used to measure a company’s profitability.

B. Is used to measure the relationship between assets and long-term debt.

C. Measures the effect of operating income on profit.

D. Is used to evaluate a company’s ability to pay its short-term obligations.

E. Only relates to long term liabilities.

According to generally accepted accounting principles, a company’s balance sheet

should show the company’s assets at:

A. The cash equivalent value of what was given up or the asset received, whichever is

more clearly evident.

B. The market value of the asset received in all cases.

C. The cash outlay only, even if part of the consideration given was something other

than cash.

D. The best estimate of a certified internal auditor.

E. Current replacement cost.

An income statement account used to record cash overages and cash shortages arising

from omitted petty cash receipts and from errors in making change is the:

A. Cash Lost account.

B. Bank Reconciliation account.

C. Petty Cash account.

D. Cash Over and Short account.

E. Cash Receivable account.

A method of estimating bad debts expense that involves a detailed examination of

outstanding accounts and that is usually the most reliable is the:

A. Direct write-off method.

B. Income statement method.

C. Aging of accounts receivable method.

D. Simplified balance sheet method.

E. Accounts receivable method.

Merchandise inventory is:

A. Reported on the balance sheet under plant and equipment.

B. Products a company owns for resale to customers.

C. Reported on the income statement as an expense.

D. Includes supplies.

E. Included on a service company’s balance sheet.

Indicate beside each of the following accounts whether the account is a temporary or

permanent account.

(a) Cash

(b) Prepaid insurance

(c) Unearned fees

(d) Accounts receivable

(e) Insurance expense

(f) Smith, capital

(g) Smith, withdrawals

(h) Rent expense

(i) Fees earned

(j) Supplies

(k) Supplies expense

(l) Depreciation expense, building

(m) Accumulated depreciation, building

Interim statements:

A. Are required by CRA.

B. Are necessary to achieve full disclosure about a business’s operations.

C. Are usually monthly or quarterly statements prepared in between the traditional,

annual statements.

D. Are required by CRA and are necessary to achieve full disclosure about a business’s

operations.

E. All of these answers are correct.

Sole proprietorships and partnerships are not subject to income tax in Canada.

The information on a work sheet can be used to prepare:

A. Year end financial statements.

B. Adjusting entries.

C. Closing entries.

D. Interim financial statements.

E. All of these answers are correct.

If a business is not being sold or closed, the amounts reported in the accounts for assets

used in operations are based on costs. This practice is justified by the:

A. Cost principle.

B. Going concern principle.

C. Revenue recognition principle.

D. Business entity principle.

E. Monetary unit principle.

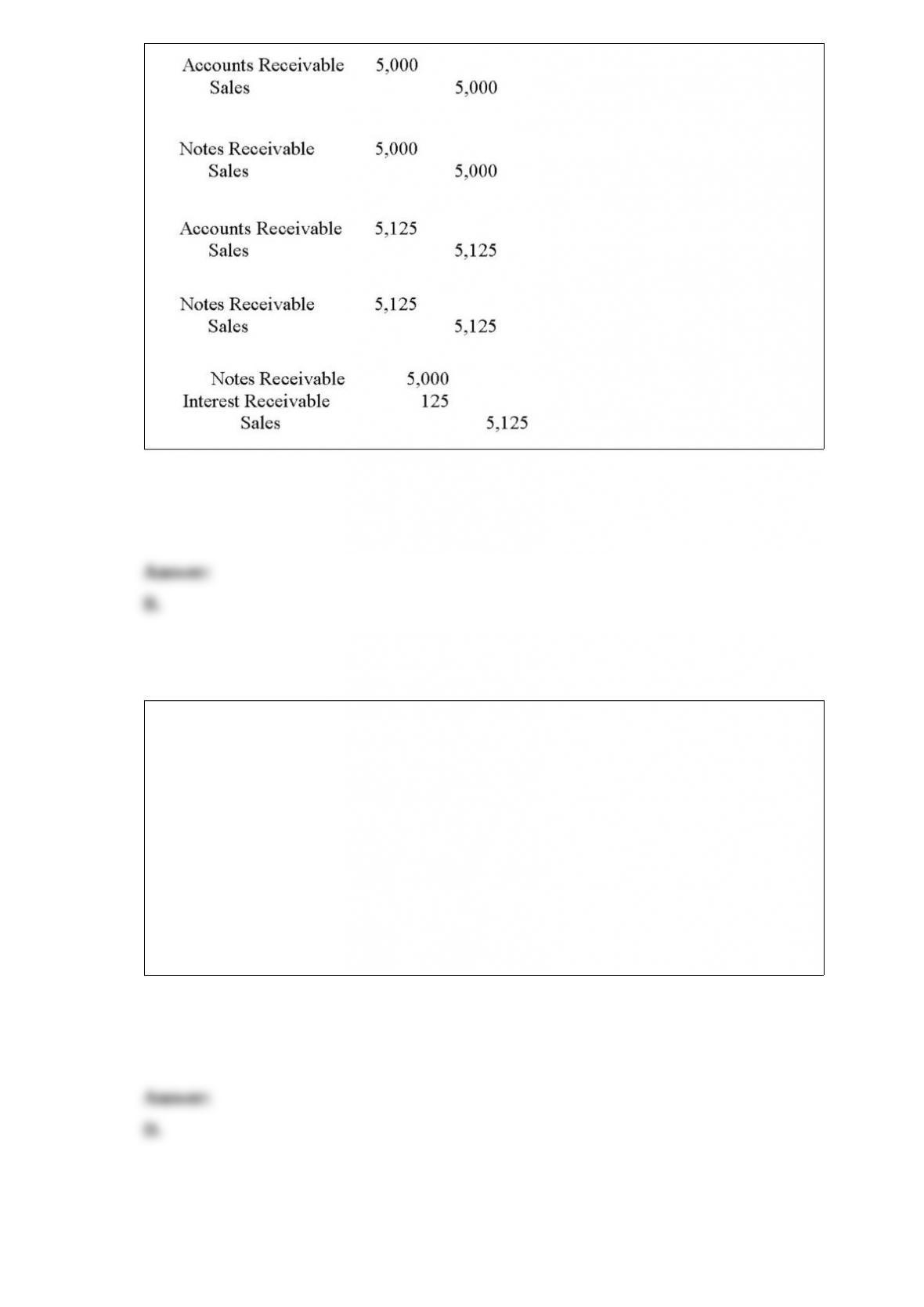

The Liccorish Pizza bought $5,000 worth of merchandise from TechCom and signed a

90-day, 10% promissory note for the $5,000. TechCom’s journal entry to record the

transaction is:

A.

B.

C.

D.

E.

A periodic inventory system:

A. Requires updating the inventory account every month.

B. Records the cost of new merchandise purchased in a permanent account.

C. Does not require a physical count of inventory.

D. Records the cost of new merchandise purchased in a temporary account.

E. All of these answers are correct.

An error is indicated if the following account has a balance appearing on the

post-closing trial balance:

A. Office Equipment.

B. Accumulated Depreciation, Office Equipment.

C. Depreciation expense, Office Equipment.

D. Ted Nash, Capital.

E. Salaries Payable.

The amount of bad debt expense can be estimated by:

A. The percent of sales approach.

B. The percent of accounts receivable approach.

C. The aging of accounts receivable approach.

D. Both the percent of sales approach and the percent of accounts receivable approach.

E. All of these answers are correct.

The Accounts Payable account in the General Ledger is:

A. The account that controls the subsidiary accounts payable ledger.

B. The account that controls the purchases journal.

C. The subsidiary account to the purchases journal.

D. Part of a special journal.

E. Part of a subsidiary ledger.

Which of the following statements is

TRUE?

A. The trial balance is never used to prepare financial statements.

B. The trial balance is a list of all the accounts in the journal.

C. Another name for the trial balance is the “chart of accounts”.

D. The trial balance is a list of the accounts in the general ledger.

E. A trial balance is only prepared at year end.

A debit is used to record:

A. An increase in a liability account.

B. A decrease in an asset account.

C. A decrease in the withdrawals account.

D. An increase in an asset account.

E. An increase in a revenue account.

Current liabilities become due:

A. Within one year.

B. Within the operating cycle of a business.

C. When bills have to be paid.

D. A or B, whichever is longer.

E. All of these answers are correct.

Real accounts are:

A. Another name for temporary accounts.

B. Another name for permanent accounts.

C. Closed at the end of the accounting period.

D. Income statement accounts.

E. Not shown on the balance sheet.

Salaries paid with cash appear on which of the following statement(s)?

A. Balance sheet.

B. Income statement.

C. Statement of changes in equity.

D. Statement of cash flows.

E. Both an income statement and statement of cash flows.

HCF, a finance company, lends Able Business $12,000 at 5% on December 1, 2015.

HCF’s adjusting entry on December 31, 2015, should include:

A. A debit to Interest Earned for $50.

B. A credit to Interest Receivable for $50.

C. A credit to Interest Earned for $50.

D. A debit to Cash for $600.

E. A debit to Interest Expense for $600.

Which of the following statements is correct?

A. Prepaid expenses, depreciation, and unearned revenues involve previously recorded

assets and liabilities.

B. Accrued expenses and accrued revenues involve assets and liabilities that have not

yet been recorded.

C. Adjusting entries are used to record both accrued expenses and accrued revenues

D. Prepaid expenses, depreciation, and unearned revenues require adjusting entries to

record the effects of the passage of time.

E. All of these answers are correct.

For the current month, Brixell Company had net sales of $12,000. Brixell typically

achieves a gross profit of 15%. Cost of goods sold under the gross profit method would

be:

A. $6,000.

B. $7,000.

C. $8,000.

D. $10,200.

E. $16,000.

Identify each of the following items as either (a) cash or (b) cash equivalent.

_____ 1. Coins

_____ 2. Petty cash

_____ 3. Three-month certificate of deposit

_____ 4. Currency

_____ 5. Certified cheque

_____ 6. Cashier’s cheque

_____ 7. Loose change in a coffee tin

_____ 8. Money orders

If, on a trial balance, the total of the debits is $7,500 and the total of the credits is

$7,419, the difference could have been caused by:

A. An error in copying an account balance from the ledger to the trial balance.

B. A transposition error.

C. A sliding error.

D. Posting only one side of an entry.

E. All of these answers are correct.

A promissory note:

A. Is an account receivable.

B. Is a written promise to pay a specified amount of money at a certain date.

C. Is a liability to the payee.

D. Is a written promise to pay a specified amount of money at a certain date and is a

liability to the payee.

E. All of these answers are correct.

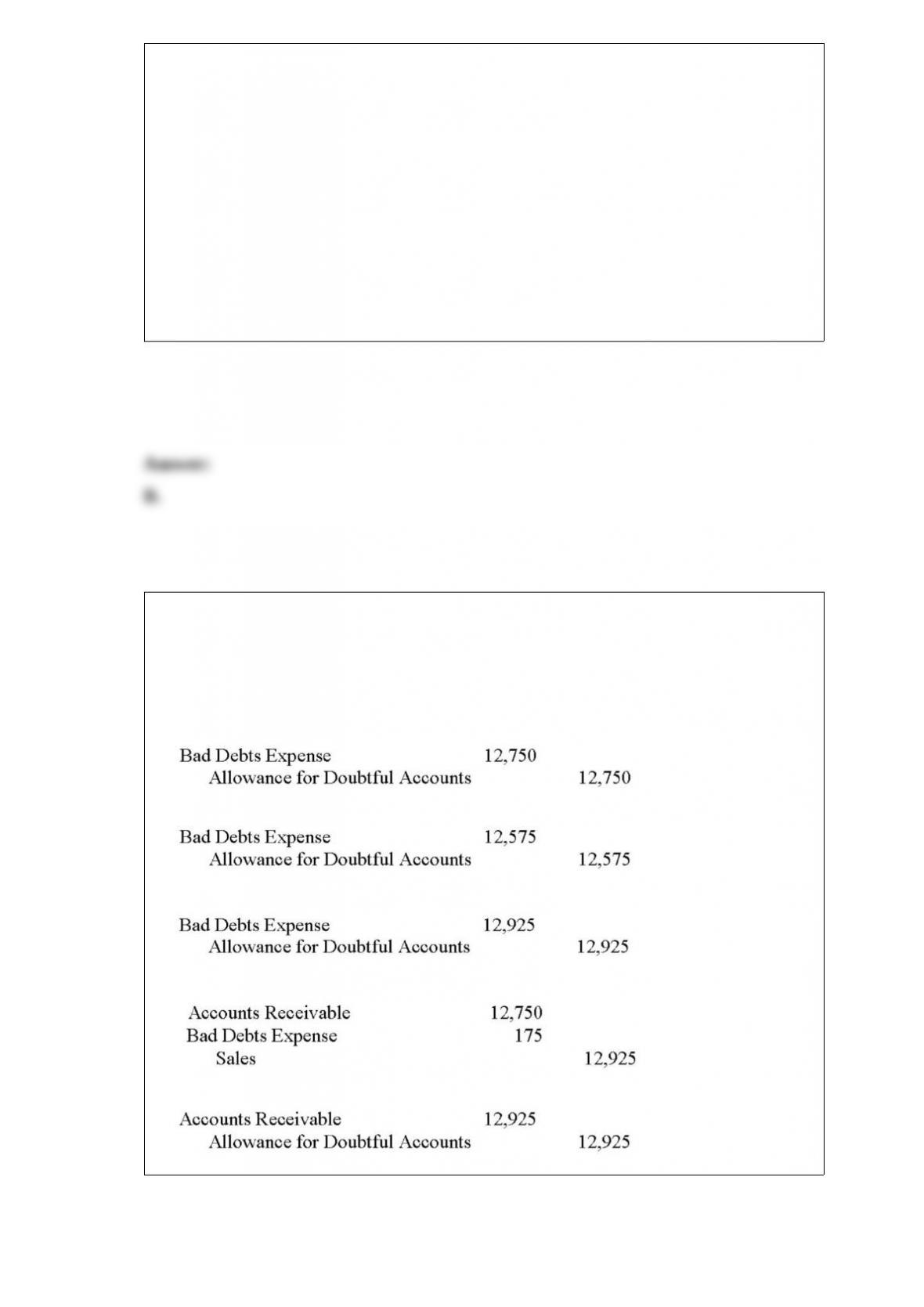

TechCom ages its accounts receivables to determine the end of the period adjustment

for bad debts. At the end of the year, management estimated that $12,750 of the

accounts receivable balances would be uncollectible. The Allowance for Doubtful

Accounts had a debit balance of $175. What entry should TechCom make at the end of

the year, for the estimated bad debts expense?

A.

B.

C.

D.

E.

The business entity principle:

A. Requires that sole proprietors have unlimited liability.

B. Requires that partnership income be taxed at the partnership level.

C. Means that business records should be kept separate from the owner’s personal

records.

D. Requires that partnerships have written agreements.

E. Requires that corporations have shareholders.

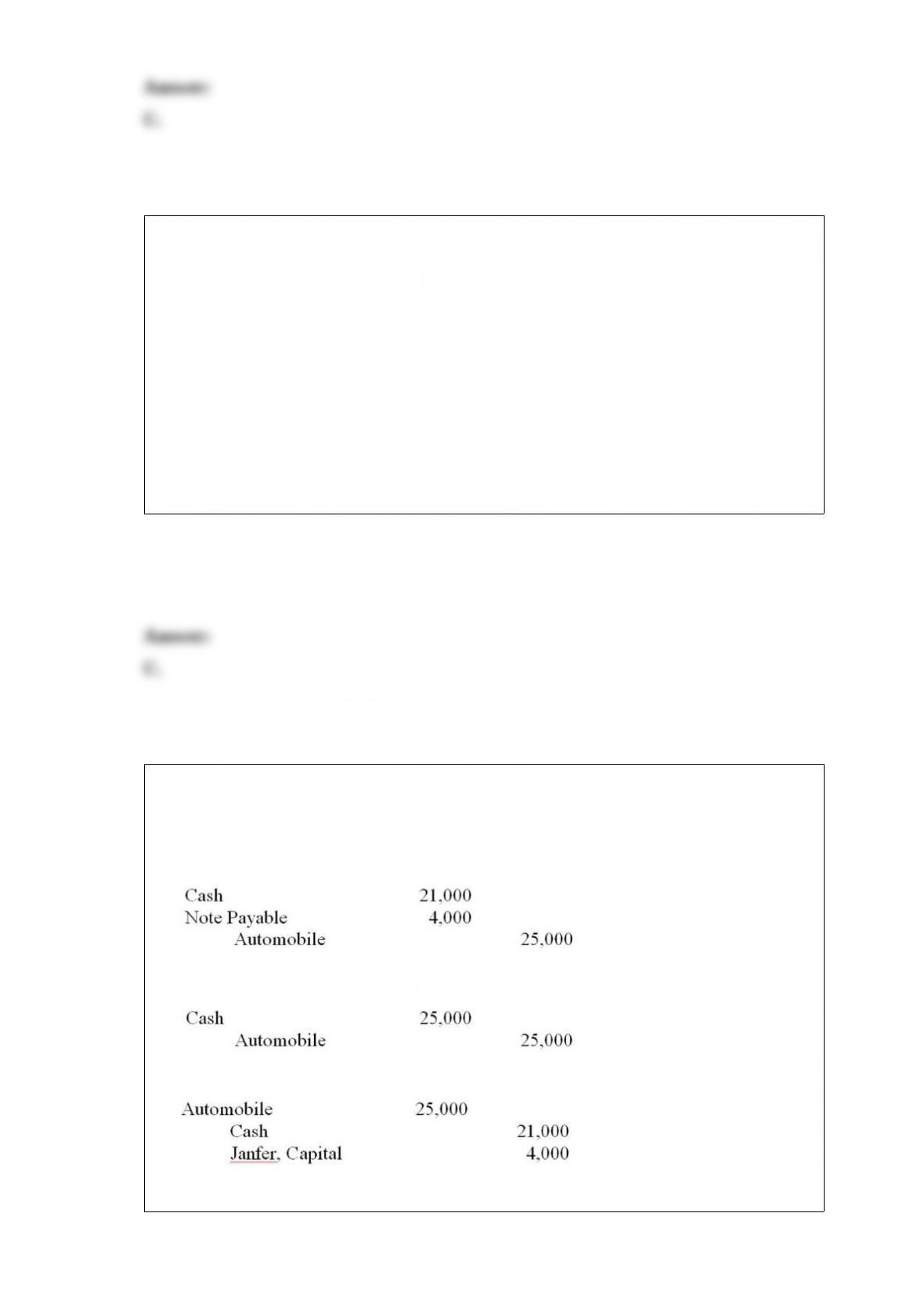

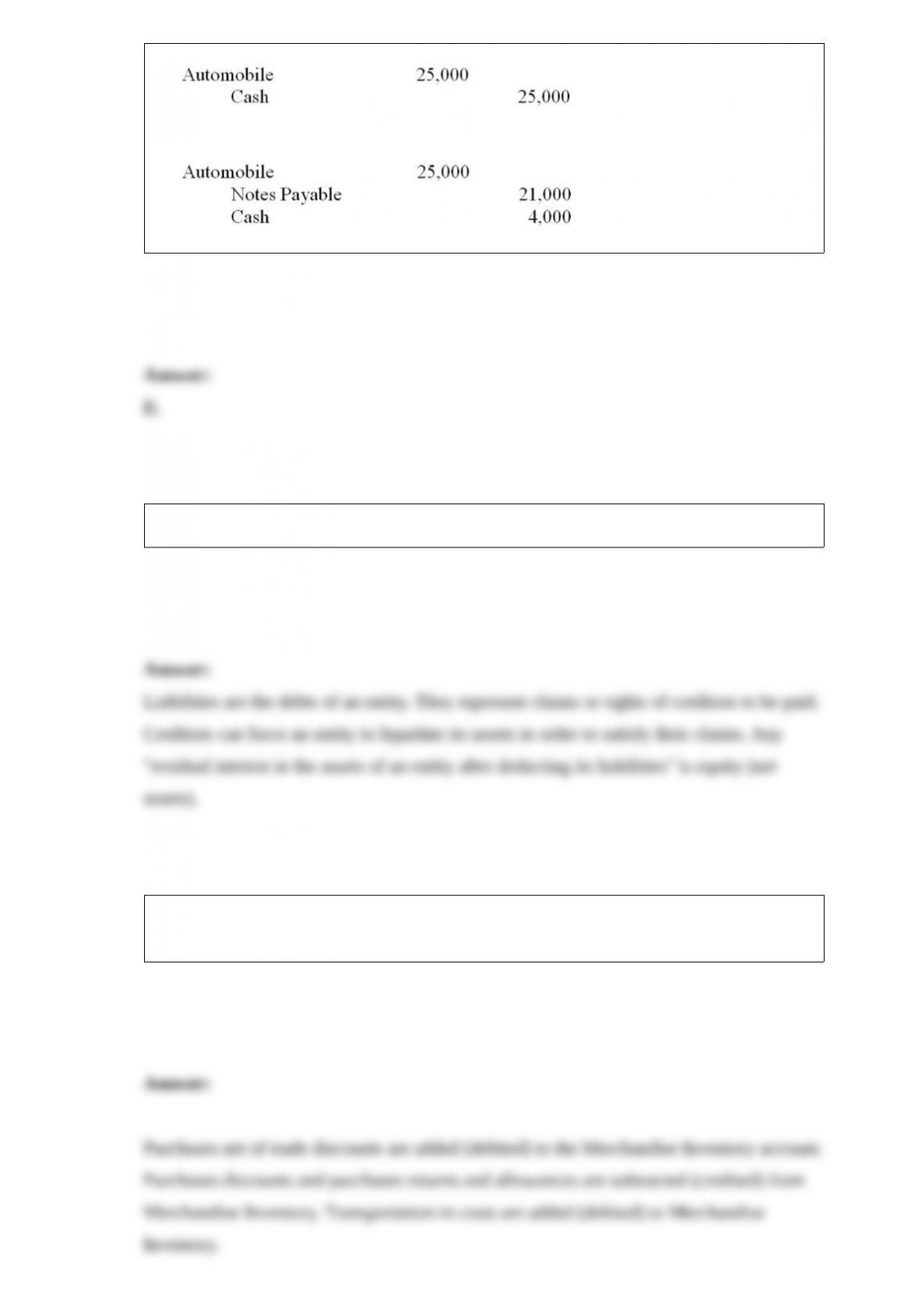

Green’s Book Store purchased a new automobile that cost $25,000, made a down

payment of $4,000, and signed a note payable for the balance. The entry to record this

transaction is:

A.

B.

C.

D.

E.

What distinguishes liabilities from equity?

Describe the recording process for purchases of merchandise inventory using a

perpetual inventory system.

The acid-test ratio measures the _______________ of a firm.

______________________ are liabilities requiring delivery of products and services at

a later date.

Describe the types of entries required in later periods that result from accruals.

Describe the attributes of inventory as an asset of a merchandising company.

Explain the purpose of preparing adjusting entries at the end of a period.