When auditing capital stock accounts, the cutoff assertion is the most important to

consider.

An approved purchase requisition form authorizes shipment of goods to customers.

Materiality is based only on a quantitative analysis of the financial statements.

The components of the audit risk model include inherent risk, control risk, and

detection risk.

The repurchase of stock includes the reacquisition of stock (treasury stock), but not the

retirement of stock.

Auditing standards permit both statistical and nonstatistical methods of audit sampling.

Obsolete inventory should be written down to its current market value.

Professionalism refers to the conduct, aims, or qualities that characterize a given

profession.

The auditor’s use of analytical procedures for auditing cash is limited.

Independence standards are required for audits of public companies, but not for audits

of private companies.

In a public company, management’s report on internal control must be signed by the

members of the audit committee.

Attribute sampling is used to estimate the proportion of a population that possesses a

specified characteristic.

Based on PCAOB guidelines, the audit of ICFR and financial statements audit should

be conducted as an “integrated audit.”

The audit committee is directly responsible for the appointment, compensation, and

oversight of the work of any accounting firm employed by a public company.

The PCAOB makes it clear that the CEO and CFO are responsible for the internal

control over financial reporting and the preparation of the statements.

In a public company, management must assess and report on internal control over

financial reporting.

If a periodic physical inventory of property, plant, and equipment is taken, the

individual responsible for the inventory should be independent of the custodial and

record-keeping functions.

The rules contained in Section 1.100 cover issues relating to independence, integrity,

and auditing standards.

Internal control includes monitoring of controls.

The principal business objectives of the purchasing process are acquiring goods and

services and paying for those goods and services.

An example of a Type I event or condition is the settlement of a lawsuit after the

balance sheet date for an amount different from the amount recorded in the year-end

financial statements.

An auditor must disclaim an opinion when the auditor lacks independence.

An imprest cash account is used for specific purposes and generally maintains a very

small balance.

A Type I error is the risk of incorrect acceptance.

One major issue associated with long-term debt is the classification of the short-term

portion of long-term debt that is due in the next year.

Rules of Conduct are enforceable.

Inherent risk is typically assessed at a low to moderate level for inventory due to the

nature of the asset.

Channel stuffing is an improper practice used to boost sales by inducing distributors to

buy more inventory than they can promptly resell.

The cash account is affected by all of the entity’s business processes.

Conflicts of interest often occur between absentee owners and managers.

A practitioner is allowed to perform either of two types of attestation engagements for

reporting on internal control: (1) examination or (2) review.

A scope limitation results from an inability to obtain sufficient appropriate evidence

about some component of the financial statements.

Analytical procedures can be used to examine the reasonableness of accounts payable

and accrued expenses.

Independence is one of the general standards for attestation engagements.

An opinion based in part on the report of another auditor requires an

explanatory/emphasis-of-matter paragraph be added to the standard unqualified audit

report.

A reliance strategy is used when control risk has been set at high.

A tort is a breach of contract for which civil action may be taken.

Within the context of quality control, the primary purpose of continuing professional

education and training activities is to enable a CPA firm to provide personnel within the

firm with

A. technical training that ensures proficiency as an auditor.

B. opportunities for career advancement outside the accounting firm.

C. knowledge required to fulfill assigned responsibilities.

D. knowledge required to perform a peer review.

The report in a review engagement provides

A. limited assurance.

B. positive assurance.

C. an opinion.

D. a summary of findings.

The purpose of segregating the duties of distributing payroll checks and hiring

personnel is to separate the

A. duties within the accounting function.

B. custody of assets from the accounting for those assets.

C. authorization of transactions from the custody of related assets.

D. operational responsibility from record keeping responsibility.

An auditor is performing substantive procedures of pricing and extension of perpetual

inventory balances consisting of a large number of items. Past experience indicates

numerous pricing and extension errors. Which of the following statistical sampling

approaches is most appropriate?

A. Unstratified mean-per-unit.

B. Monetary-unit sampling.

C. Stop or go.

D. Difference projection.

Which of the following tends to be most predictable for purposes of analytical

procedures applied as substantive procedures?

A. Relationships involving balance sheet accounts.

B. Transactions subject to management discretion.

C. Relationships involving income statement accounts.

D. Data subject to audit testing in the prior year.

Which of the following is generally requested in a legal letter?

A. A request that the attorney comment on unasserted claims where his or her views

differ from management’s evaluation.

B. A list of all attorneys that performed any work for the entity during the year.

C. A statement indicating that the attorney is responsible for the fair presentation of

unasserted claims in the entity’s financial statements.

D. A request that the attorney provide a copy of all invoices given to the entity during

the year.

An auditor compares information on canceled checks with information contained in the

cash disbursements journal. The objective of this test is to determine that

A. recorded cash disbursement transactions are properly authorized.

B. proper cash purchase discounts have been recorded.

C. cash disbursements are for goods and services actually received.

D. no discrepancies exist between the data on the checks and the data in the journal.

The auditor is least likely to learn of retirement of equipment through which of the

following?

A. Reviewing the purchase return and allowance account.

B. Reviewing depreciation.

C. Analyzing debits to the accumulated depreciation account.

D. Reviewing insurance policy riders.

An auditor’s purpose in reviewing credit ratings of customers with delinquent accounts

receivable most likely is to obtain evidence concerning management’s assertions about

A. valuation and allocation.

B. completeness.

C. existence.

D. rights and obligations.

Jones Retailing, a nonpublic entity, has asked Winters, CPA, to compile financial

statements that omit substantially all disclosures required by generally accepted

accounting principles. Winters may compile such financial statements, provided the

A. reason for omitting the disclosures is explained in the engagement letter and

acknowledged in the management representation letter.

B. financial statements are prepared on a comprehensive basis of accounting other than

generally accepted accounting principles.

C. distribution of the financial statements is restricted to internal use only.

D. omission is not undertaken to mislead the users of the financial statements and is

properly disclosed in the accountant’s report.

In nonstatistical sampling for tests of controls, increasing the desired confidence level

results in a

A. higher tolerable deviation rate.

B. lower expected deviation rate.

C. larger sample size.

D. smaller sample size.

The element of the audit planning process most likely to be agreed upon with the entity

before implementation of the audit strategy is the determination of the

A. evidence to be gathered to provide a sufficient basis for the auditor’s opinion.

B. procedures to be undertaken to discover litigation, claims, and assessments.

C. pending legal matters to be included in the inquiry of the entity’s attorney.

D. timing of inventory observation procedures to be performed.

Match the test of controls described below to the appropriate assertion it is used to test.

1)Review entity’s competitive bidding procedures

2)Review the cash disbursements journal for reasonableness of account distribution

3)Trace a sample of receiving reports to their respective vendor invoices and vouchers

4)Review monthly bank reconciliations

5)Test a sample of vouchers for the presence of authorized purchase order and receiving

report

6)Compare the dates on the receiving reports with the dates of the relevant vouchers

a) Authorization

b) Classification

c) Occurrence

d) Completeness

e) Cutoff

f) Accuracy

The main difference between SAS and AU is

A. They are the same except that SAS are organized chronologically and the AU are

organized by topical area.

B. SAS are issued by the ASB and AU are issued by the PCAOB.

C. SAS are issued by the PCAOB and AU are issued by the ASB.

D. SAS define minimum standards of performance for auditors while AU define

financial accounting principles that must be followed according to GAAP.

The Sarbanes-Oxley Act of 2002 is considered the most sweeping securities law since

the 1933 and 1934 Acts. Which item in the list below was not part of the

Sarbanes-Oxley Act of 2002?

A. Enhances prosecutorial tool available in fraud cases.

B. Legislates new guidelines for ethics and integrity for public accounting firms.

C. Expands statutory prohibitions against fraud and obstruction of justice.

D. Increases authorized penalties for securities and financial fraud.

E. Strengthens the legal protections accorded whistleblowers.

Auditing standards define special purpose financial statements as including those

prepared under the following base(s)

A. regulatory basis.

B. tax basis.

C. contractual basis.

D. regulatory basis, tax basis, and contractual basis.

A high detection risk strategy includes all of the following except:

A. Interim testing.

B. Reduced testing of transactions.

C. Heavy reliance on analytical procedures as substantive procedures.

D. Audit work only completed at year-end.

A surprise observation by an auditor of an entity’s regular distribution of paychecks is

primarily designed to satisfy the auditor that

A. all unclaimed payroll checks are properly returned to the cashier.

B. the paymaster is not involved in the distribution of payroll checks.

C. all employees have in their possession proper employee identification.

D. names on the company payroll are those of bona fide employees presently on the

job.

The auditor should ordinarily mail confirmation requests to all banks with which the

entity has conducted any business during the year, regardless of the year-end balance,

since

A. the confirmation form also seeks information about indebtedness to the bank.

B. this procedure will detect kiting activities that would otherwise not be detected.

C. the mailing of confirmation forms to all such banks is required by generally accepted

auditing standards.

D. this procedure relieves the auditor of any responsibility with respect to non-detection

of forged checks.

Governmental auditing often extends beyond examinations leading to the expression of

an opinion on the fairness of financial presentation and includes audits of efficiency,

effectiveness, and

A. Monetary stimulus.

B. Evaluation.

C. Accuracy.

D. Compliance.

In which of the following circumstances would a CPA who audits XM Corporation lack

independence?

A. The CPA and XM’s president are both on the board of directors of COD Corporation.

B. The CPA and XM’s president each owns 25 percent of FOB Corporation, a

closely-held company.

C. The CPA has an automobile loan from XM, which is a savings and loan organization

and the loan is collateralized by the automobile.

D. The CPA reduced XM’s usual audit fee by 40 percent because XM’s financial

condition was unfavorable.

Smith is engaged in the audit of a cable TV firm that services a rural community. All

receivable balances are small, customers are billed monthly, and internal control is

effective. To determine the existence of the accounts receivable balances at the balance

sheet date, Smith would most likely

A. send positive confirmation requests.

B. send negative confirmation requests.

C. examine evidence of subsequent cash receipts instead of sending confirmation

requests.

D. use statistical sampling instead of sending confirmation requests.

The audit working papers belong to

A. The company under audit.

B. The government.

C. The audit firm.

D. They are public record documents.

Responding to a question such as “What would happen if…” is an attribute of which of

the following types of engagements?

A. Financial projection.

B. Financial forecast.

C. Financial forecast and financial projection.

D. Review.

The program flowcharting symbol representing a decision is a

A. Triangle.

B. Circle.

C. Rectangle.

D. Diamond.

Your audit client is under intense pressure to meet an earnings target. Which transaction

assertion for transactions within the purchasing process are you most concerned with?

A. Existence or occurrence.

B. Completeness.

C. Rights and obligations.

D. Presentation and disclosure.

The occurrence assertion for accounts payable includes

A. determining whether all accounts payable are recorded.

B. determining whether all accounts payable actually are liabilities.

C. determining whether all accounts payable are recorded in the proper period.

D. determining whether all accounts payable are properly classified in the financial

statements.

When an auditor increases the planned assessed level of control risk because certain

control activities were determined to be ineffective, the auditor would most likely

increase the

A. Extent of tests of details.

B. Level of inherent risk.

C. Extent of tests of controls.

D. Level of detection risk.

The achieved (actual) level of audit risk

A. Can always be accurately assessed by the auditor.

B. Should be greater than or equal to acceptable audit risk.

C. Can never be known with certainty.

D. Is the same for all audit engagements.

The auditor is concerned with establishing that dividends are paid to stockholders of the

entity owning stock as of the

A. issue date.

B. declaration date.

C. record date.

D. payment date.

Harvey Jones, CPA, uses statistical sampling to test control procedures. What is a

benefit of using statistical sampling?

A. It provides a means of mathematically measuring the sampling risk that result from

examining only a part of the data.

B. It eliminates the use of judgment required of Jones because the AICPA has

established numerical criteria for this type of testing.

C. It increases Jones’ knowledge of the entity’s prescribed procedures and their

limitations.

D. It is required by generally accepted auditing standards.

Which of the following policies constitutes a control weakness related to the acquisition

of factory equipment?

A. Acquisitions are to be made through and approved by the department in need of the

equipment.

B. Advance executive approvals are required for equipment acquisitions.

C. Variances between authorized equipment expenditures and actual costs are to be

immediately reported to management.

D. Depreciation policies are reviewed only once a year.

In designing written audit programs, an auditor should plan specific audit procedures to

test

A. Timing of audit procedures.

B. Cost-benefit of gathering evidence.

C. Selected audit techniques.

D. Management assertions.

Describe the limitations of internal control. Why do limitations on internal control

exist?

Information Nation has two hundred locations spread across the fifty states. Twenty of

the locations are considered to be individually important, but fifty of the locations are

not important even when aggregated from the others. Five locations deal with foreign

exchange trading. These locations are not considered important, but they are important

when aggregated with the other locations. As an auditor, discuss the considerations

involved in testing multiple locations and group the locations accordingly (provide how

many locations are included in each group). Include the treatment that each group

should receive from the auditor.

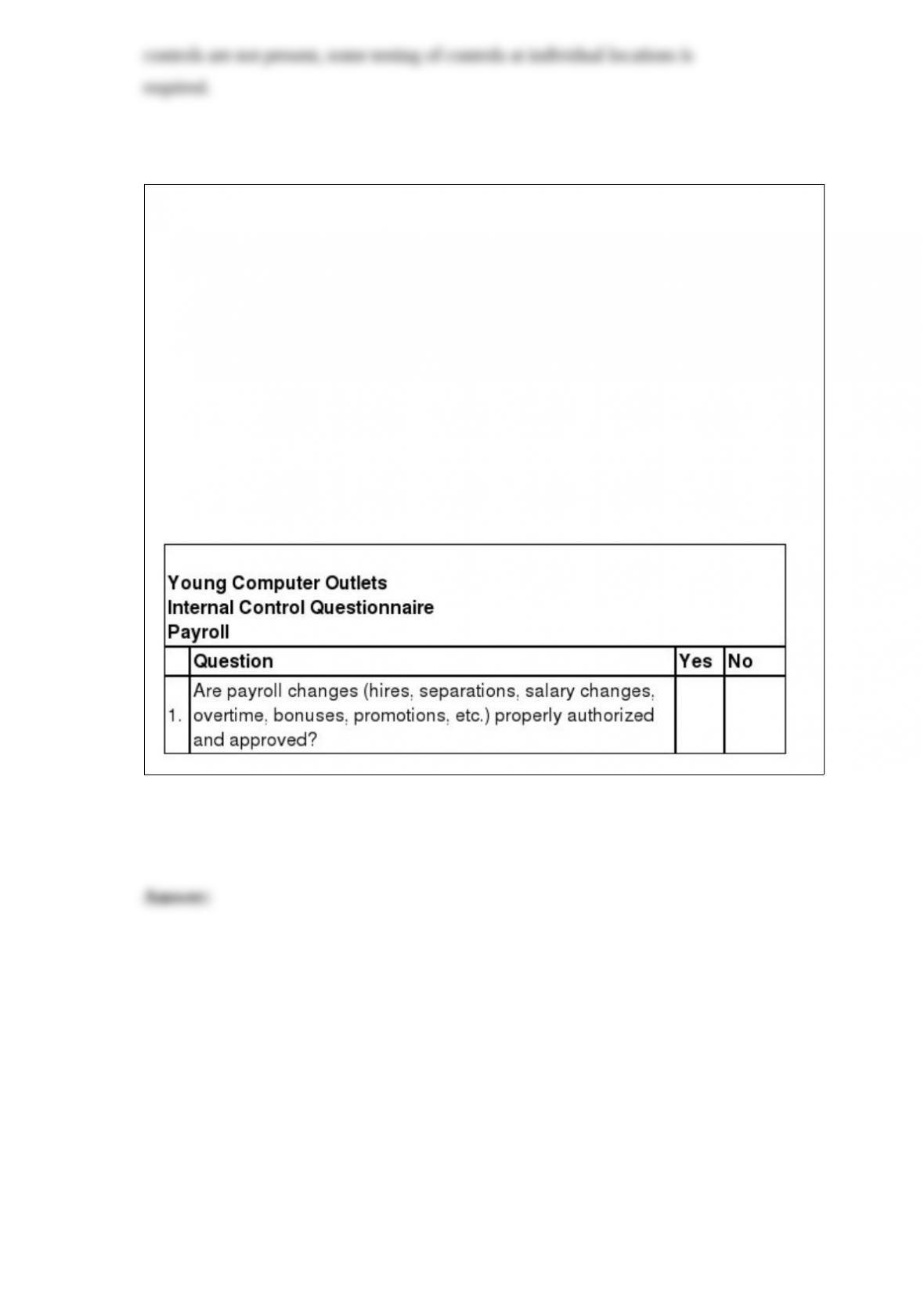

Brownstein, CPA, has been engaged to audit the financial statements of Young

Computer Outlets, Inc., a new client. Young is a privately owned chain of retail stores

that sells a variety of computer software and video products. Young uses an in-house

payroll department at its corporate headquarters to compute payroll data and to prepare

and distribute payroll checks to its 300 salaried employees. Brownstein is preparing an

internal control questionnaire to assist in obtaining an understanding of Young’s internal

control and in setting control risk.

Prepare a “Payroll” segment of Brownstein’s internal control questionnaire that would

assist in obtaining an understanding of Young’s internal control and for setting the

control risk. Do not prepare questions relating to cash payroll, IT applications, or

payments based on hourly rates, piecework, commissions, employee benefits (pensions,

health care, vacations, and so on), or payroll tax accruals other than withholdings. Use

the following format:

We know from cost accounting that there are three components that make up the

standard costs for inventory. Explain how an auditor could test each of these

components for a company that manufactures pillows.

Stan is auditing First Financial Services and would like to use financial ratios to test the

ability of First Financial Services to meet its current obligations. Identify two ratios that

would help Stan in this task. Indicate how each ratio is calculated and what a high ratio

would signify to Stan.

Data capture occurs through source documentation, direct data entry, or a combination

of the two. List three purposes of data capture controls.

Give an example of a test of controls that could be used by an auditor to test for the

following assertions: Occurrence, Accuracy, and Cutoff.

Before performing sampling procedures in an audit of controls, Sue set the tolerable

deviation rate at 4.0%. After the procedures, she computes a computed upper deviation

rate of 5.4%. What can Sue conclude about the entity’s controls?

What is one advantage and one disadvantage of classical variables sampling?

Why do professions establish codes of conduct that define ethical behaviors for

members of the profession?

What auditing standards are used to conduct an audit for a privately-held corporation?

What auditing standards are used to conduct an audit for a publicly-traded corporation?

What organization is responsible for setting each of these sets of standards?

You are the owner of a small grocery store, Corner Marketplace. Explain the five

process categories and how they apply to your business.

Which type of confirmation is used more frequently by auditors”accounts receivable

confirmations or accounts payable confirmations? Why?

Section 11 under the Securities Act of 1933 treats claims against auditors more

favorably than common law. What two things does a plaintiff need to prove to have a

case against the auditor of a company in which she purchased new investments? What

does the auditor have to do to have the case dismissed?

According to the text, what are the two functions of working papers?