Monitoring of the revenue cycle may be accomplished partially through the use of

exception reporting.

Various types of ways that fraud could be perpetrated should be hypothesized by the

auditor prior to conducting audit testing.

The Rules of Conduct govern the performance of CPAs in carrying out their public

responsibilities.

A number of studies of bankruptcies have shown that certain combinations of ratios,

like the Altman Z-score, have good predictive power in indicating the likelihood of

bankruptcy.

When business risk is low, the auditor does not have a high concern that about the

ability of the organization to operate efficiently.

Statistical sampling assists auditors in determining the sufficiency of evidence gathered.

The SEC requires publicly owned corporations to have their quarterly financial

information reviewed by their independent auditors before it is issued, but does not

require that the auditor’s review report be included with the quarterly information,

although many companies do include the auditor’s report.

If an audit firm accepts or continues to provide audits to a client firm with ineffective

internal controls over financial reporting, the management representation letter will note

that an adverse opinion will likely be issued.

Utilitarian theory is an approach for addressing ethical problems by identifying a

hierarchy of rights that should be considered in solving ethical dilemmas.

The auditor should be aware of material asset additions that are in remote locations and

physically inspect such assets.

When evaluating identified misstatements, the auditor only needs to consider

misstatements in the current year, and not misstatements from the prior year.

Touring a company’s plant offers much insight into potential audit issues.

The AICPA Auditing Standards Board (ASB) requires a 5-year mandatory cooling off

period for partner rotation.

The substantial doubt about an entity’s ability to continue as a going concern is a phrase

that is used in an unqualified opinion with a certain type of explanatory language.

Physical controls are necessary to protect and safeguard assets from accidental or

intentional destruction and theft.

The scope paragraph of an unqualified opinion primarily provides information relating

to the division of responsibilities.

Ineffective internal controls result in higher risk of material misstatement in the

financial statements than effective internal controls.

The purpose of the auditor’s consideration of the effectiveness of internal controls is to

determine the nature, extent and timing of substantive testing.

In assessing the fair value of Level 1 assets, the auditor can perform an analysis of the

volume of trading activity as part of obtaining audit evidence.

If unusual or unexpected relationships related to long-lived assets are identified during

preliminary analytical procedures, the planned audit procedures (tests of controls,

substantive procedures) would be adjusted to address the risk of material misstatement.

Brown, Inc. obtained a patent for its product five years ago and should expense the

entire amount of the unamortized balance if the product is no longer sold.

When there is an uncertainty surrounding the financial statements, the auditor may still

be able to give an unqualified opinion.

An auditor can issue a disclaimer of opinion because of an inability to obtain sufficient

appropriate evidence.

Sample size in a MUS sample is a function of risk of incorrect acceptance, tolerable

misstatement, and expected misstatement.

Legal expenses are reviewed by auditors for possible litigation and related FAS 5

treatment.

Monetary unit sampling (MUS) results in an efficient sample size and concentrates on

the dollar value of the account balances.

Current FMV of assets and liabilities of non-goodwill assets is one of the factors

affecting goodwill impairment valuations.

In a quality audit, the auditor will review management’s processes for certification to

provide reasonable assurance that those processes are adequate and that they can be

relied upon.

Rights theory focuses on evaluating actions in terms of the fundamental rights of the

parties involved.

Kiting is an example of a technique used to intentionally and materially overstate cash.

All of the following are required by the auditor before allowing the client to take

inventory before year-end except which one?

A.Absence of “red flags”.

B.Internal control is weak.

C.The auditor can effectively test the year-end balance through a combination of

analytical procedures and selective testing of transactions between the physical count

and the year-end.

D.The auditor reviews the intervening transactions for evidence of any manipulation or

unusual activity.

The PCAOB’s AS No. 5 states that internal controls may be preventive or detective.

Which of the following controls is preventive?

A.Requiring two persons to open mail containing payments.

B.Reconciling the accounts receivable subsidiary file with the control account.

C.Using batch totals.

D.Preparing bank reconciliations.

Which of the following accounts is NOT a major account in the acquisition and

payment cycle?

A.Inventory.

B.Cost of goods sold.

C.Accounts payable.

D.All of the above are major accounts.

Which of the following is not a potential indicator of going concern problems for a

client?

A.Negative trends in key financial ratios.

B.Loss of key personnel.

C.Plan to sell nonessential assets.

D.Default on a loan.

Which of the following is not a purpose of the management representation letter?

A.It reminds management of its responsibility for the financial statements.

B.It confirms oral responses obtained by the auditor earlier in the audit and the

continuing appropriateness of those responses.

C.It decreases the possibility of misunderstanding concerning the matters that are the

subject of the representations.

D.It implies that the auditor is responsible for the design of the internal controls.

In attribute sampling, which of the following does the risk of incorrect acceptance deal

with?

A.Effectiveness.

B.Efficiency.

C.Reliability.

D.Both A and B.

An audit committee must be comprised of outside directors and at least one outside

financial expert. An individual with which of the following characteristics is considered

an outside director?

A.A director who is not a member of management and has no other relationship to the

organization.

B.A consultant to the organization who works as an honorary member of the board.

C.A director who is also a member of management and has no other relationship to the

company.

D.A director who is a CPA and CIO of an affiliated organization.

Completeness of revenues may be tested by the auditor through the selection of a

sample of which of the following?

A.Shipping documents and tracing them to the sales journal.

B.Accounts receivable and tracing them to cash receipts.

C.Recorded sales transactions and tracing them to the general ledger.

D.Inventory records and tracing them to the shipping documents.

The risk of material misstatement refers to which of the following?

A.Inherent risk.

B.Control risk and acceptable audit risk.

C.The combination of inherent risk and control risk.

D.Inherent risk and audit risk.

When requiring a letter of audit inquiry from the client’s attorney, which of the

following information will be requested?

A.A statement regarding conflicts of interest that the attorney may have with the client.

B.The attorney’s expert opinion of proper GAAP treatment related to client

contingencies.

C.An evaluation of the likelihood of unfavorable outcome of, and estimated losses from

contingencies.

D.Possible auditor defenses for third-party litigation related to ordinary negligence

claims.

When confirming receivables in testing for overstatements, assume that there are few or

no misstatements expected and the selection will be based on the dollar value of

individual items. Which of the following is the auditor most likely to use?

A.MUS sampling.

B.Stratified mean-per-unit sampling.

C.Ratio estimation sampling.

D.Attribute sampling.

Which of the following is the international body that sets standards for the practice of

internal auditing across the world?

A.The Internal Audit Reporting Standards Board.

B.The Institute of Internal Auditors.

C.The International Accounting Standards Board.

D.The Charter of Certified Internal Auditors.

The auditor may discover that the recorded cost of inventory exceeds the designated

market price when testing which assertion?

A.Existence.

B.Cutoff.

C.Valuation.

D.Rights.

To conduct an audit, what must an auditor do?

A.Comply with relevant ethical standards.

B.Exercise perfect judgment.

C.Obtain sufficient appropriate evidence to provide absolute assurance.

D.All of the above.

Which of the following is not a step the auditor needs to determine in designing

sampling for substantive testing?

A.The audit objective.

B.The method of selecting a sample.

C.Expected misstatement conditions.

D.Control failure risk.

Assessing disclosures does not require reasonable assurance of which of the following?

A.The disclosures are understandable to users.

B.Disclosed events and transactions have occurred and pertain to the entity.

C.All material and immaterial disclosures have been reported.

D.The information is disclosed accurately and at appropriate amounts.

Which method focuses on the materiality of current year misstatements and the

reversing effect of prior-year misstatements on the income statement?

A.Rollover method.

B.Iron curtain method.

C.Percentage approach.

D.Judgmental method.

Which of the following types of audit evidence is the most reliable?

A.Evidence from the client’s organization.

B.Evidence from a poorly controlled system.

C.Directly observable evidence.

D.Facsimiles of documents.

Which of the following is not part of the control environment of an organization?

A.Management’s philosophy and operating style.

B.Organizational structure.

C.Human resources.

D.Both A and B.

E.All of the above are part of the control environment.

The quality of an organization’s internal controls affect which of the following?

A.The reliability of financial data.

B.The ability of management to make good decisions.

C.The ability to remain in business.

D.All of the above.

Which of the following expense accounts is associated with natural resources? ?

A.Depreciation expense.

B.Amortization expense.

C.Depletion expense.

D.Capitalization expense.

As cash processing systems become more automated and integrated, which of the

following is true about the general concept of segregation of duties?

A.Segregation of duties becomes less important.

B.Segregation of duties becomes more important.

C.The importance of segregation of duties does not change.

D.Segregation of duties becomes completely computerized without human

involvement.

Which of the following applications are incorporated into statistical sampling?

A.Binomial and confidence intervals.

B.Random and haphazard selection.

C.Hypergeometric distribution with audit risk.

D.Probability and statistical inference with audit judgment.

A client company has a history of negative cash flow trends and continuing losses.

Which type of opinion will the auditor most likely issue?

A.Adverse.

B.Unqualified with explanatory language.

C.Qualified.

D.Disclaimer of opinion.

Which of the following best describes year-to-year comparisons of account balances?

A.Time analyses.

B.Reasonableness tests.

C.Ratio analyses.

D.Trend analyses.

Which is the primary assertion tested in conjunction with obtaining evidence regarding

impairment?

A.Valuation.

B.Cutoff.

C.Existence.

D.Rights.

Other comprehensive bases of accounting do not include which of the following?

A.Cash basis.

B.Tax basis.

C.Regulatory basis.

D.Intended basis.

Material misstatements in the financial statements, including those requiring

restatements strongly imply a material weakness in which of the following?

A.Income statement.

B.Balance sheet.

C.Internal control over financial reporting.

D.Cash flow statements.

Who is responsible for internal controls within an organization?

A.The internal auditor.

B.The external auditor.

C.Management.

D.The PCAOB.

Which one of the following is a reporting standard requirement?

A.The auditor will state explicitly whether the financial statements are fairly presented

in accordance with the applicable financial reporting framework.

B.The auditor will identify in the auditor’s report, those circumstances in which auditing

principles have not been consistently observed in the current period in comparison to

the preceding period.

C.The auditor will review adjusting journal entries for accuracy, and if the auditor

concludes those entries are not reasonable accurate, the auditor must so state in the

auditor’s report.

D.The auditor will express an unqualified opinion on the financial statements, or will

conduct additional audit procedures until such an opinion can be expressed.

Which of the following procedures is not a procedure used by an auditor in searching

for unrecorded disposals of long-lived assets?

A.Inquire clients about disposals.

B.Examine cash receipts journal.

C.Observe inventory count.

D.Examine scrap sales accounts.

The fraud triangle has three components. Which of the components must be present for

a fraud to occur?

A.All factors must be present for fraud to occur.

B.All factors need not be present.

C.Fraud can occur if any one of the factors is present.

D.None of the above

A review report provides the user with which one of the following types of assurance?

A.Reasonable assurance.

B.Basic assurance.

C.Absolute assurance.

D.Limited assurance.

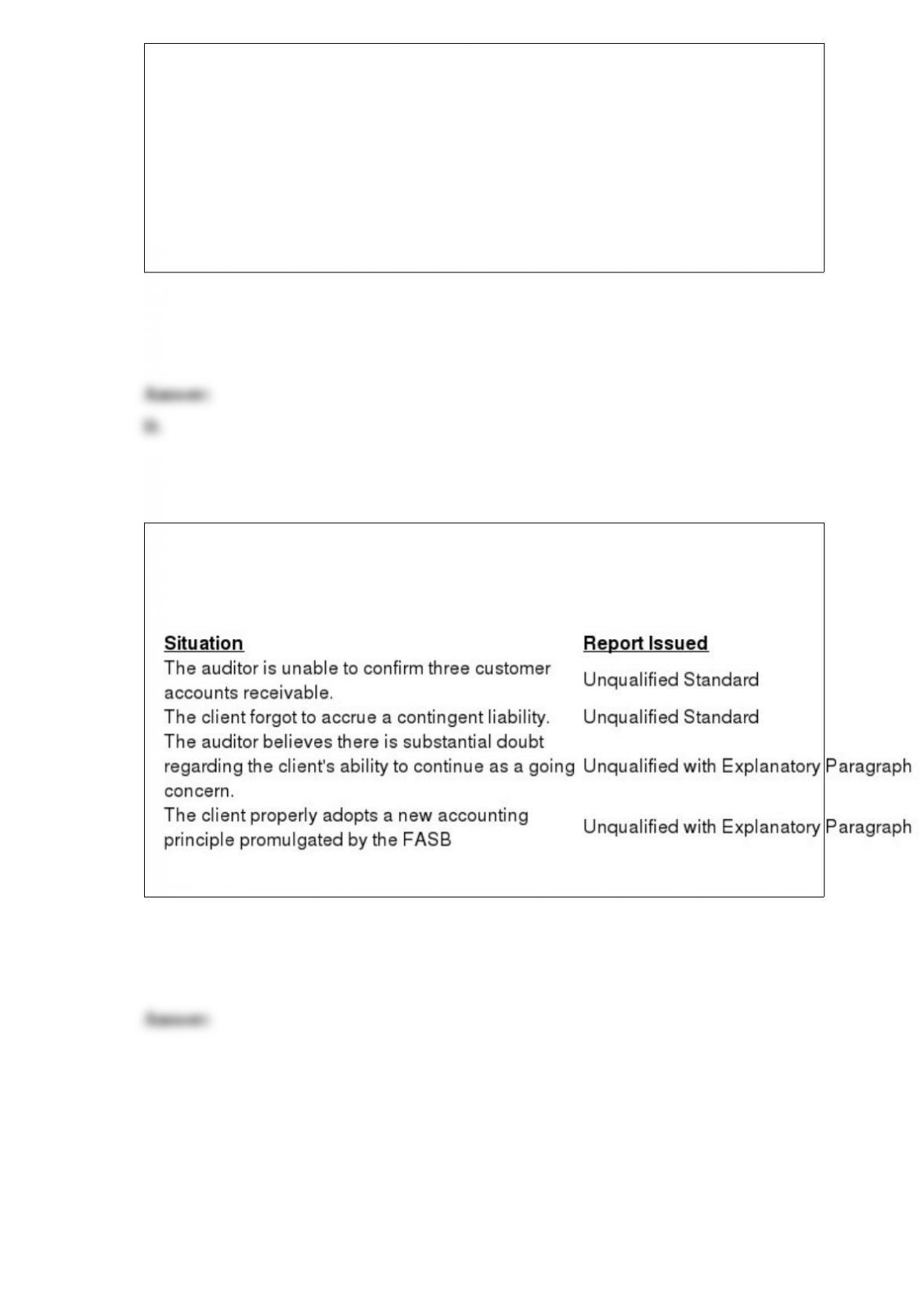

For each of the following situations, define the type of problem encountered and

provide an explanation as to the type of report which was issued.

Discuss the differences between a traditional receiving system and an automated

integrated receiving system.

Under the clarified auditing standards, what is the structure of each auditing standard

issued by the ASB? What is the purpose of each section?

Describe what is meant by asset impairment and explain where inherent risks related to

asset impairment stems from.

Discuss the three or more attributes that an auditors possess in order to maintain

credibility. Explain the importance of these attributes to the audit.

The auditor for Knowles, Inc. is attempting to determine whether the recorded sales and

accounts receivable are supported by valid transactions. Identify the assertions being

tested and develop the substantive procedures to be used to satisfy the auditor’s

objectives.

What are the procedures available to auditors in auditing accounts payable and what

level of assurance is obtained by each? Describe at least three. Which primary assertion

is tested through these approaches?

Audit documentation serves as the primary support of an audit. Give at least six

examples of the components of proper working paper documentation.

What control procedures should be implemented to ensure the completeness objective is

met with respect to sales?

Recent landscape changes in accounting and auditing developed from corporate fraud

and, arguably, auditor failure. In order to continually lead and adapt to the dynamics of

regulation, principles based accounting practices and auditing standards, what types of

skills and traits are auditors required to possess?

Define auditing and discuss how its components fit into an overview of a financial

statement audit.

Subsequent to the date of the financial statements, as part of post-balance sheet date

audit procedures, a CPA learned that a recent fire caused significant damage to one of

the client’s two manufacturing facilities. However, the loss will not be reimbursed by

insurance. Newspapers in the area describe the event in detail and the event is widely

known. The financial statements and related notes as prepared by the client did not

disclose the fire loss.

REQUIRED:

Which type of audit report would you suggest be issued this year and why?

Identify and describe at least four procedures the audit team may perform in order to

determine potential obsolescence of items in the inventory balances.