A distinguishing characteristic of intangible assets is the degree of uncertainty about

when or if they will provide future benefits.

Material restructuring costs are reported as an element of income from continuing

operations.

Depending on the circumstances, the classification of a compensating balance may be

either current or noncurrent, and the arrangement should be disclosed in the notes.

A contract between a seller and a buyer need not be in writing to be enforceable.

Unrealized gains and losses are included in other comprehensive income for securities

that are classified as available for sale.

Changes in enacted tax rates that do not become effective in the current period affect

deferred tax accounts only after the new rates take effect.

Compound interest includes interest earned on interest.

Shipping charges on outgoing goods are included in either cost of goods sold or selling

expenses.

The concept of substance over form influences the classification of obligations expected

to be refinanced.

For a purchase commitment contained within a single fiscal year, if the market price is

less than the contract price, the purchase is recorded at the contract price.

Which of the following changes should be accounted for using the retrospective

approach?

a. A change in the estimated life of a depreciable asset.

b. A change from straight-line to declining balance depreciation.

c. A change to the LIFO method of costing inventories.

d. A change from the completed-contract method of accounting for long-term

construction contracts.

How many types of potential common shares must a corporation have in order to be

said to have a complex capital structure?

a. Three.

b. Two.

c. One.

d. Zero.

The APBO increases each year by the:

a. Interest accrued on the APBO and the portion of the EPBO attributed to that year.

b. Interest accrued on the EPBO and the portion of the EPBO attributed to that year.

c. Interest accrued on the APBO and the portion of the APBO attributed to that year

d. Interest accrued on the EPBO and the portion of the APBO attributed to that year.

If the residual value of a leased asset turns out to be more than the amount guaranteed

by the lessee, the:

a. Lessor must compensate the lessee for the excess.

b. Lessee must pay the lessor the amount of the excess.

c. Lessee will reduce the last year’s depreciation.

d. Lessor is not obligated to compensate the lessee for the excess.

A net operating loss (NOL) carryforward cannot result in the balance sheet at the end of

the NOL year showing:

a. A receivable under current assets for an income tax refund.

b. A current deferred tax asset.

c. A noncurrent deferred tax asset.

d. Both a current and a noncurrent deferred tax asset.

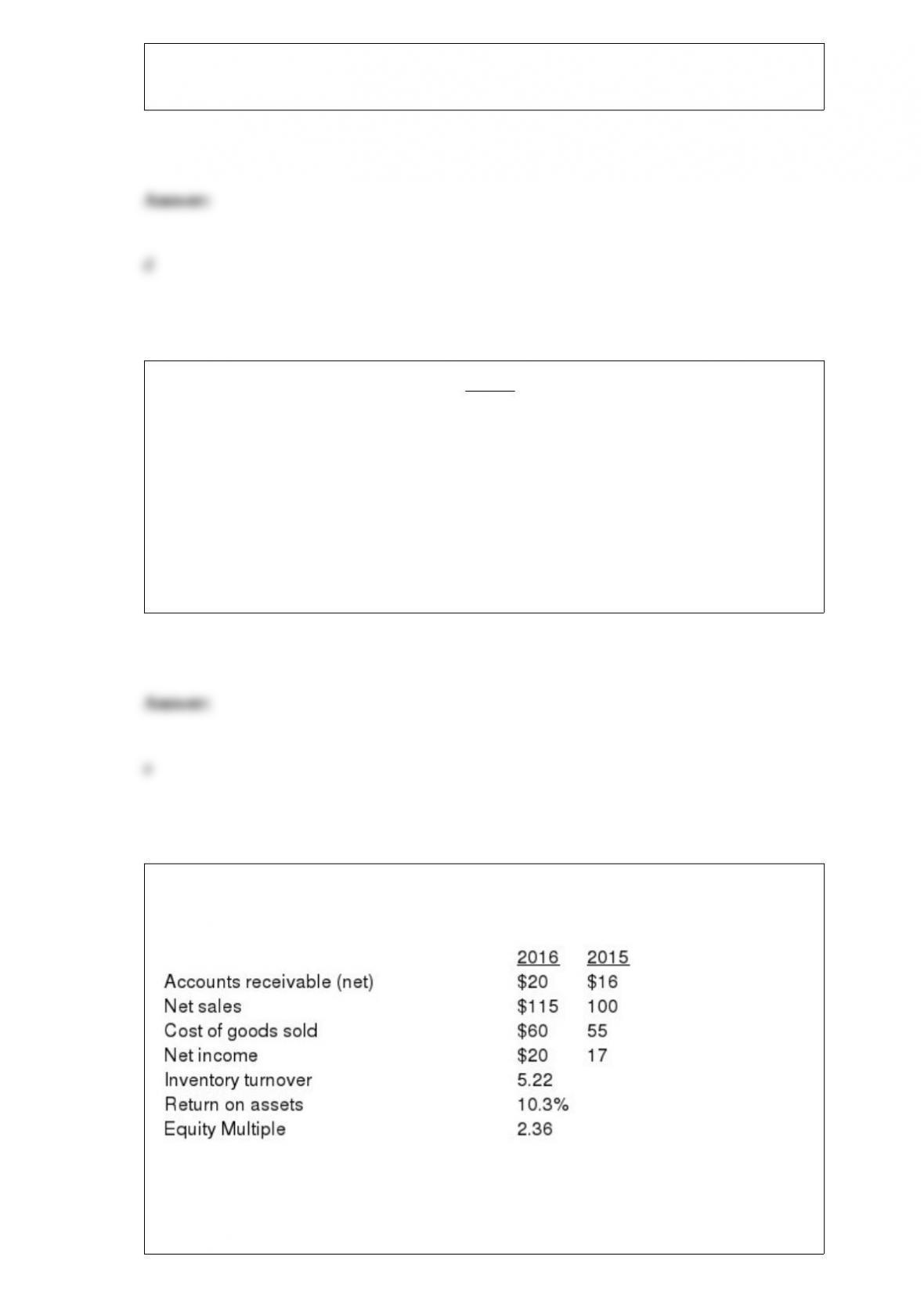

Excerpts from Dowling Company’s December 31, 2016 and 2015, financial statements

and key ratios are presented below (all numbers are in millions):

Dowling’s 2016 profit margin is (rounded):

a. 17.4%.

b. 18.5%.

c. 18.0%.

d. 16.5%.

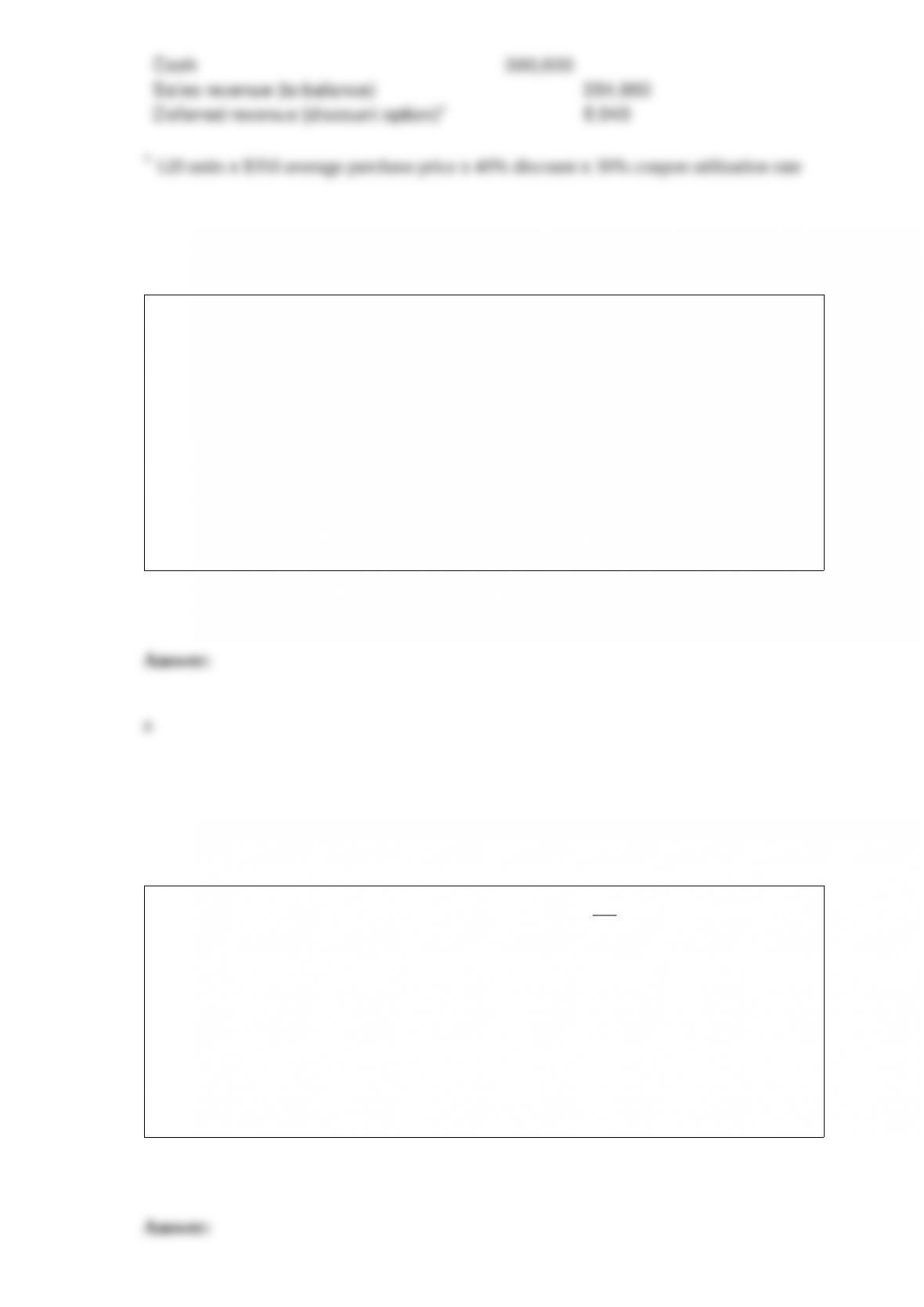

DGA Associates, Inc. sells computer workstations designed for architects. In 2016, it

sold 120 workstations for $360,000. For each workstation sold, DGA distributed a 40%

discount coupon for any additional future purchases made in the next 12 months. Based

on historical experience, DGA expects that approximately 30% of the coupons will be

utilized, and the goods purchased with the coupons would normally sell for $350.

Required:

(a) How many performance obligations are in a contract to purchase a computer

workstation? Explain the reasons for your answer.

(b) Prepare a journal entry to record revenue for the sale of 120 computer workstations,

assuming that DGA uses the residual method to estimate the stand-alone selling price of

the workstations sold without the discount coupon.

Share issue costs refer to the costs of obtaining the legal, promotional, and accounting

services necessary to effect the sale of shares. The costs reduce the net cash proceeds

from selling the shares and thus paid-in capital’”-excess of par, and are:

a. Not recorded separately.

b. Recorded as an asset.

c. Recorded as a liability.

d. Amortized over time.

The acquisition costs of property, plant, and equipment do not include:

a. The ordinary and necessary costs to bring the asset to its desired condition and

location for use.

b. The net invoice price.

c. Legal fees, delivery charges, installation, and any applicable sales tax.

d. Maintenance costs during the first 30 days of use.

Mary signed up and paid $1200 for a 6 month ceramics course on June 1st with Choplet

Ceramics. As of August 1st, Choplet’s accounting records would indicate:

a. $400 of revenue, $800 of accounts receivable

b. $400 of revenue, $800 of deferred revenue

c. $1,200 of revenue, $1,200 of cash

d. $800 of revenue, $400 of accounts receivable

Blue Cab Company had 50,000 shares of common stock outstanding on January 1,

2016. On April 1, 2016, the company issued 20,000 shares of common stock. The

company had outstanding fully vested incentive stock options for 5,000 shares

exercisable at $10 that had not been exercised by its executives. The end-of-year market

price of common stock was $13 while the average price for the year was $12. The

company reported net income in the amount of $269,915 for 2016. What is the diluted

earnings per share (rounded)?

a. $3.60.

b. $4.10.

c. $4.50.

d. $3.81.

Long-term notes receivable issued for noncash assets at an unrealistically low interest

rate will be:

a. Discounted at an imputed interest rate.

b. Recorded at the contract amount.

c. Recorded at an amount equal to the future cash flows.

d. Accounted for on the installment basis.

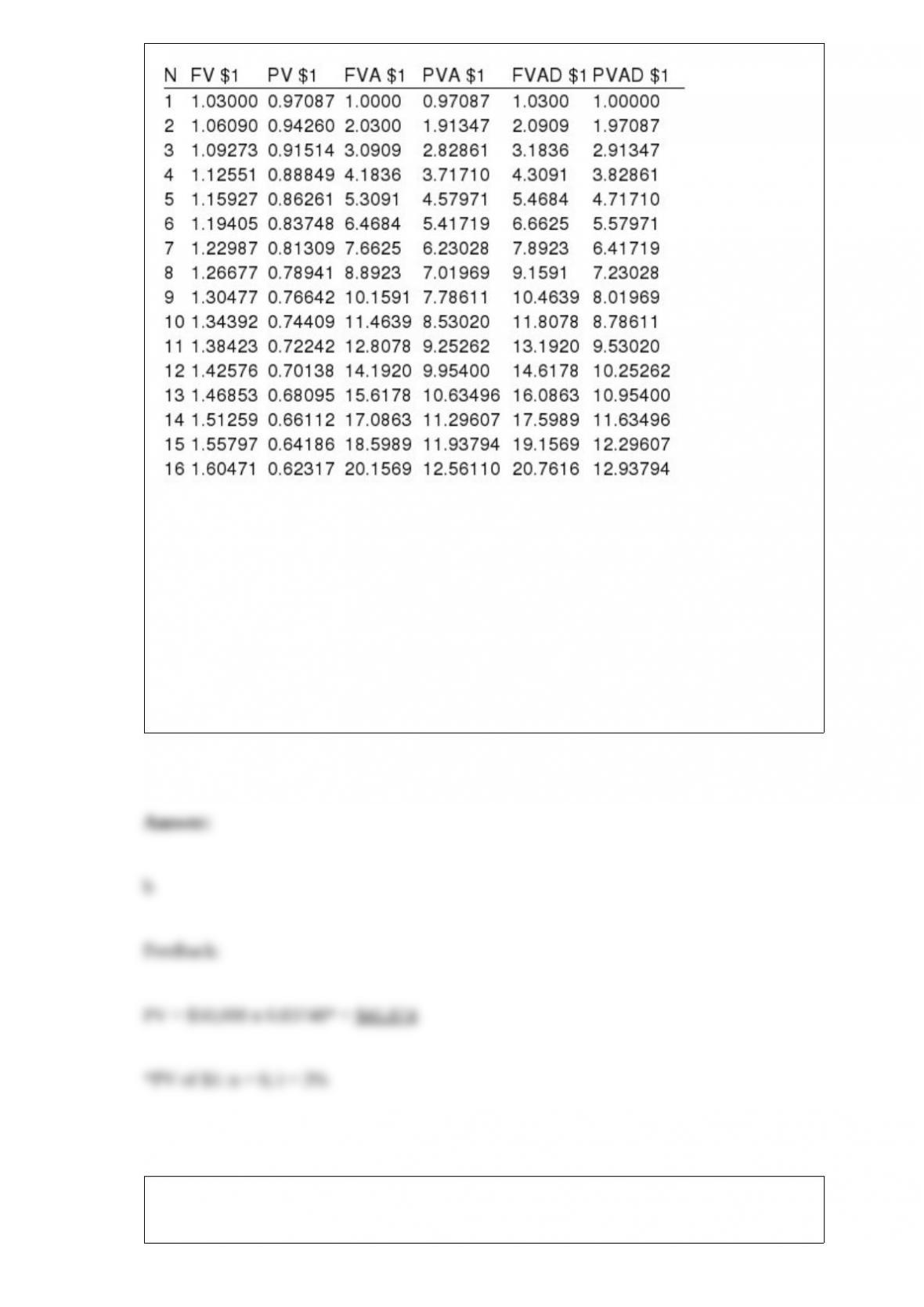

Present and future value tables of $1 at 3% are presented below:

Monica wants to sell her share of an investment to Barney for $50,000 in three years. If

money is worth 6% compounded semiannually, what would Monica accept today?

a. $ 8,375.

b. $41,874.

c. $11,941.

d. $41,000.

The calculation of diluted earnings per share assumes that stock options were exercised

and that the proceeds were used to:

a. Buy common stock as an investment.

b. Retire preferred stock.

c. Buy treasury stock.

d. Increase net income.

Baker Inc. acquired equipment from the manufacturer on 10/1/2016 and gave a

noninterest-bearing note in exchange. Baker is obligated to pay $918,000 on 4/1/2017

to satisfy the obligation in full. If Baker accrued interest of $9,000 on the note in its

2016 year-end financial statements, what is its imputed annual interest rate?

a. 2%.

b. 4%.

c. 6%.

d. None of these answer choices are correct.

Recording pension expense would usually:

a. Increase the PBO.

b. Increase current assets.

c. Increase the prior service cost-AOCI.

d. Increase the net loss-AOCI.

The December 31, 2015, balance sheet of Ming Inc. included 12% bonds with a face

amount of $100 million. The bonds were issued in 2005 and had a remaining discount

of $3,400,000 at December 31, 2015. On January 1, 2016, Ming called the bonds at a

price of 102.

Required: Prepare the journal entry by Ming to record the retirement of the bonds on

January 1, 2016.

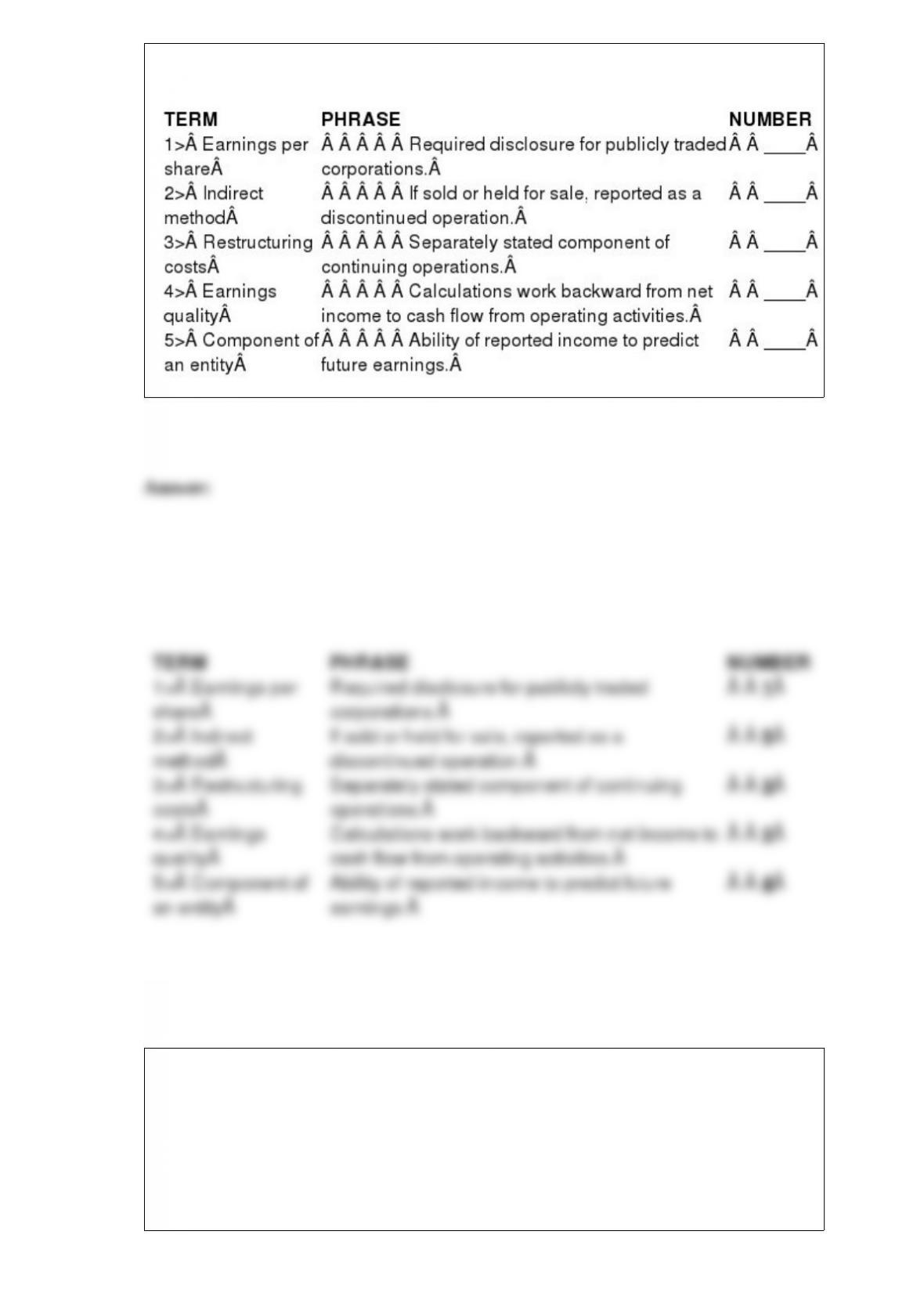

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

On January 1, 2016, Hobart Mfg. Co. purchased a drill press at a cost of $36,000. The

drill press is expected to last 10 years and has a residual value of $6,000. During its

10-year life, the equipment is expected to produce 500,000 units of product. In 2016

and 2017, 25,000 and 84,000 units, respectively, were produced. Required:

Compute depreciation for 2016 and 2017 and the book value of the drill press at

December 31, 2016 and 2017, assuming the straight-line method is used.

Beaumont Company enters into a contract to provide a high quality diving-certification

preparation package, including goggles, snorkels, air tanks, fins, a wetsuit, and 5 private

lessons to get ready for diving certifications. The entire package sells for $2,500.

Typically, Beaumont incurs $375 on compensation and other costs to provide the

private lessons, and earns an average of 40% profit over cost on service offerings.

Required: Assuming that the diving equipment and the certification lessons are

separate performance obligations, estimate the stand-alone selling price of the certified

lessons based on the expected cost plus margin approach.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct number code for the term.