When a machine having a net book value of $15,000 is sold for $12,000:

A. current assets decrease, equipment (net) increases, and net income increases.

B. current assets increase, equipment (net) decreases, and net income increases.

C. current assets increase, equipment (net) decreases, and net income decreases.

D. current assets increase, equipment (net) increases, and net income decreases.

When a cost formula is used to describe a mixed (semi-variable) cost behavior pattern,

total costs are expected to increase and per unit variable costs are expected to:

A. increase as the level of activity increases.

B. decrease as the level of activity decreases.

C. decrease as the level of activity increases.

D. remain constant as the level of activity increases.

For performance reports to be most effective for management by exception, they

should:

A. be issued at the same time for all responsibility centers.

B. be held until the financial statements for the month have been issued.

C. be issued as soon as possible after the activity or period covered.

D. show all of the costs associated with the responsibility center being reported about.

A principal difference between operational budgeting and capital budgeting is the time

frame of the budget. Because of this difference, capital budgeting:

A. is an activity that involves only the financial staff.

B. is done on a rolling budget period basis.

C. focuses on the present value of cash flows from investments.

D. is concerned with a long-term net income forecast.

Which of the following requires an explanatory paragraph in the independent auditors’

report?

A. Basing the opinion on the work of another auditor.

B. Uncertainties about the outcome of a significant event that would have affected the

presentation of the financial statements.

C. Substantial doubt about the entity’s viability to continue as a going concern.

D. None of the above.

E. Items A, B and C are correct.

At December 31, 2016, the end of the first year of operations at Xavion Inc., the firm’s

accountant neglected to accrue payroll taxes of $55,400 that were applicable to payrolls

for the year then ended.

(a.) Write the journal entry or use the horizontal model to show the effect of the accrual

that should have been made as of December 31, 2016.

(b.) Determine the income statement and balance sheet effects of not accruing 2016

payroll taxes at December 31, 2016 (assuming that the payroll taxes were not accrued,

as originally stated).

(c.) Assume that when the payroll taxes were paid in January 2017, the payroll tax

expense account was charged. Assume that at December 31, 2017, the accountant again

neglected to accrue the payroll tax liability, which was $40,800 at that date. Determine

the income statement and balance sheet effects of not accruing 2017 payroll taxes at

December 31, 2017.

Erca, Inc. produces automobile bumpers. Overhead is applied on the basis of machine

hours required for cutting and fabricating. A predetermined overhead application rate of

$15.00 per machine hour was established for 2016.

(a.) If 9,000 machine hours were expected to be used during 2016, how much overhead

was expected to be incurred?

(b.) Actual overhead incurred during 2016 totaled $135,000, and 9,200 machine hours

were used during 2016. Calculate the amount of over- or underapplied overhead for

2016.

(c.) Explain the accounting necessary for the over- or underapplied overhead for the

year.

Expenditures capitalized as long-lived assets generally include those expenditures that:

A. are made for normal repairs to maintain the usefulness of the asset over a number of

years.

B. are for items that have a physical life of more than a year, regardless of their cost.

C. are material in amount and that have an economic benefit to the entity only in the

current year.

D. are material in amount and that have an economic benefit to the entity that extends

beyond the current year.

When a company splits its common stock 3 for 1:

A. total paid-in capital increases by a factor of 3.

B. retained earnings is decreased by the market value of the shares issued.

C. the market value of the company’s stock normally falls by two-thirds.

D. the stockholders are assured of receiving larger cash dividends.

The impact of changing price levels on amounts reported in financial statements is:

A. reported as a separate item on the balance sheet.

B. accomplished by reporting assets at their replacement cost.

C. required to be described in the notes to the financial statements.

D. encouraged, but not required to be described in the notes to the financial statements.

The predetermined overhead application rate based on direct labor hours is computed

as:

A. actual total overhead costs divided by actual direct labor hours.

B. estimated total overhead costs divided by estimated direct labor hours.

C. actual total overhead costs divided by estimated direct labor hours.

D. estimated total overhead costs divided by actual direct labor hours.

Balance sheet disclosures for preferred stock include all of the following except:

A. The number of shares issued.

B. The number of shares outstanding.

C. The liquidating or redemption value.

D. The credit or market value.

E. The number of shares authorized.

For which of the following reconciling items would an adjusting entry be necessary on

the company’s book?

A. A deposit in transit.

B. An error by the bank.

C. Outstanding checks.

D. A bank service charge.

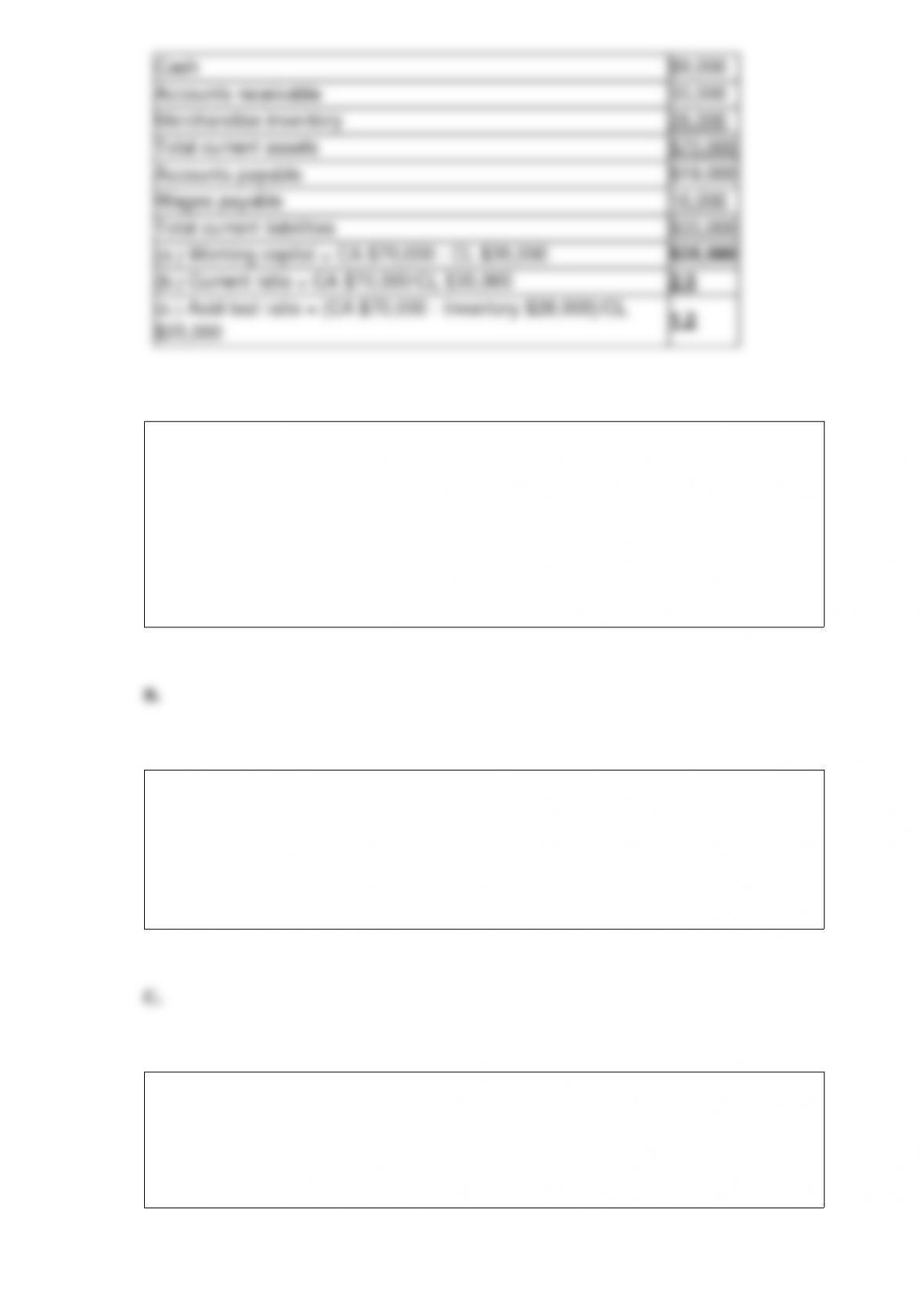

The following amounts were reported on the December 31, 2016, balance sheet:

Required:

(a.) Calculate working capital at December 31, 2016.

(b.) Calculate the current ratio at December 31, 2016.

(c.) Calculate the acid-test ratio at December 31, 2016.

The term, “realization,” in revenue recognition refers to which of the following?

A. The entity has completed, or substantially completed, the activities it must perform

to be entitled to the revenue benefits.

B. The product or service has been exchanged for cash, claims to cash, or an asset that

is readily convertible to a known amount of cash or claims to cash.

C. The entity has received an irrevocable order for goods or services.

D. Cash has been received with an irrevocable order for goods or services.

E. None of the above.

Capital expenditure analysis, which leads to the capital budget, attempts to determine

the impact of a proposed capital expenditure on the organization’s:

A. segment margin.

B. contribution margin.

C. ROI.

D. cost of capital.

The time frame associated with an income statement is:

A. a point in time in the past.

B. a past period of time.

C. a future period of time.

D. a function of the information included in it.

The potential rental value of space used in the manufacturing process:

A. is a variable production cost.

B. is an unavoidable production cost.

C. is a sunk production cost.

D. is an opportunity cost if production is not outsourced.

On January 1, 2017, the balance in Great Lakes Co.’s Allowance for Bad Debts account

was $15,600. During the year, a total of $10,500 of delinquent accounts receivable were

written off as bad debts. The balance in the Allowance for Bad Debts account at

December 31, 2017, was $21,900.

(a.) What was the total amount of bad debts expense recognized during the year?

b.) As a result of a comprehensive analysis, it is determined that the December 31,

2017, balance of Allowance for Bad Debts should be $18,900. Show, in general journal

format the adjustment required.

A performance report for direct labor shows a variance between the budget and actual

amounts. This difference is a:

A. budget variance.

B. direct labor efficiency variance.

C. direct labor spending variance.

D. direct labor rate variance.

A working capital loan will generally:

A. not have an interest rate.

B. require that interest (if any) be paid monthly.

C. not affect working capital.

D. be classified as a noncurrent liability.

Which of the following formula elements is not used in calculating the accounting rate

of return?

A. operating income.

B. a present value factor.

C. depreciation expense.

D. average investment.

An item that cost $120 is to be sold for a price that will yield a gross profit ratio of

20%. The selling price should be:

A. $96

B. $144

C. $150

D. $600 Selling Price = Cost of product/(1 – Desired gross profit ratio)

The part of the variable overhead budget variance due to the difference between actual

variable overhead cost and the standard cost allowed for the actual inputs used is called

the:

A. variable overhead spending variance.

B. variable overhead budget variance.

C. variable overhead efficiency variance.

D. variable overhead volume variance.

The term preemptive right pertains to which of the following?

A. The Board of Directors rights in liquidation.

B. Present shareholders’ right to purchase shares from any additional share issuances.

C. Present shareholders’ right to purchase treasury shares when reissued.

D. Preferred stockholders’ right to dividends.

The going concern concept refers to a presumption that:

A. the entity will be profitable in the coming year.

B. the entity will not be involved in a merger within a year.

C. the entity will continue to operate in the foreseeable future.

D. top management of the entity will not change in the coming year.

The primary difference between absorption costing and direct costing is the treatment

of:

A. direct material costs.

B. variable manufacturing overhead.

C. fixed manufacturing overhead.

D. direct labor costs.

Springfield Manufacturing Co. is considering the investment of $60,000 in a new

machine. The machine will generate cash flow of $7,500 per year for each year of its 15

year life and will have a salvage value of $4,000 at the end of its life. Springfield’s cost

of capital is 10%.

(a.) Calculate the net present value of the proposed investment. Ignore income taxes,

and round all answers to the nearest $1.

(b.) Calculate the present value ratio of the investment.

(c.) What will the internal rate of return on this investment be relative to the cost of

capital? Explain your answer.

(d.) Calculate the payback period of the investment.

For the fiscal year ended March 31, 2017, a company reported earnings per share of

$1.95 and cash dividends per share of $0.30. During fiscal 2018, the company had a

3-for-2 stock split. In the annual report for the fiscal year ended March 31, 2018,

earnings per share and cash dividends for fiscal 2017 would be reported, respectively,

as:

A. $1.95 and $0.30

B. $2.91 and $0.45

C. $1.30 and $0.20

D. $0.65 and $0.10

The accounting concept/principle being applied when an adjustment is made is usually:

A. matching revenue and expense.

B. consistency.

C. original cost.

D. materiality.

A favorable materials quantity variance would occur if:

A. more material is purchased than is used.

B. actual pounds of materials used were less than the standard pounds allowed.

C. actual labor hours used was greater than the standard labor hours allowed.

D. actual pounds of materials used was greater than the standard pounds allowed.

Zero-based budgeting forces managers to:

A. identify and prioritize the activities that are carried out in their departments.

B. justify all of their expenditures for each budget period.

C. both A and B.

D. none of the above.

Most entities satisfy the accounting criteria for recognizing an expense when:

A. a commitment is made to purchase a product or service.

B. cash is paid to a supplier.

C. a cost is incurred in the revenue generating process.

D. a dividend is paid to stockholders.

Prepare a bank reconciliation for Show Me, Inc., as of June 30 from the following

information:

(a.) The June 30 balance shown on the bank statement is $5,796.

(b.) Outstanding checks at June 30 totaled $330.

(c.) A deposit of $424 made on June 30 was not included in the balance shown on the

bank statement.

(d.) The bank statement contained an adjustment of $410 for a note receivable

collected by the bank on behalf of Show Me, Inc. ($382 principal and $28 interest).

(e.) A bank charge of $34 was made to the account during June. Although the company

was expecting a charge, the amount was not known until the bank statement arrived.

(f.) The bank erroneously charged a $340 check of Shirt, Inc., against the Show Me,

Inc., bank account.

(g.) The June 30 balance in the general ledger Cash account, before reconciliation, is

$6,026.

(h.) The bank statement included a notice that a customer’s check for $172 that had

been deposited on June 14 had been returned NSF.