When a company pays its rent in advance, an asset is reported on the balance sheet.

Expenses are the costs of operating the business that are paid for in the period covered

by the income statement.

Depreciation is an allocation method, not a valuation method.

When a company issues bonds that include no periodic interest payments, the bonds are

referred to as “zero-coupon” bonds.

The daily activities involved in running a business, such as buying supplies and paying

salaries and wages, are classified as operating activities on the statement of cash flows.

When preparing the operating activities section of the statement of cash flows using the

indirect method, a decrease in accounts receivable is subtracted from net income.

A corporation’s charter establishes the number of shares of stock that will be issued in

an initial public offering (IPO).

When preparing the operating activities section of the statement of cash flows using the

direct method, a gain or loss from selling equipment is reported in the operating

activities section of the statement of cash flows.

Cary Inc. reported net credit sales of $300,000 for the current year. The unadjusted

credit balance in its Allowance for Doubtful Accounts is $500. The company has

experienced bad debt losses of 1% of credit sales in prior periods. Using the percentage

of credit sales method, what amount should the company record as an estimate of Bad

Debt Expense?

A) $2,500

B) $3,000

C) $2,980

D) $3,200

An Additional Paid-in Capital account could be used with all of the following

transactions except:

A) The issuance of par value stock at a price greater than the par value.

B) The reissuance of treasury stock at a price less than the price paid when the stock

was reacquired.

C) The reissuance of treasury stock at a price greater than the price paid when the stock

was reacquired.

D) The issuance of no-par stock.

Stockholders’ equity is:

A) a liability of the business.

B) an economic resource controlled by the business.

C) the owners’ claims on the business.

D) the profit generated by the business.

Which of the following statements is correct?

A) A current ratio of 1.60 means the company ‘s current assets are probably not

sufficient to pay its current liabilities.

B) The separate entity assumption requires that the financial activities of the owners of

a company be reported on the company ‘s balance sheet.

C) The cost principle states that recording activities at cost will result in the balance

sheet representing the true value of the company.

D) A transaction is recorded if it has a measurable financial effect on the assets,

liabilities or stockholders ‘ equity of a business.

Lansing Limited had a beginning balance in its Retained Earnings account of $385,600.

During the year, the company declared and paid a $4,700 dividend, and at the end of the

year, it reported Retained Earnings of $399,860. The company’s net income for the year

was:

A) $14,260.

B) $18,960.

C) $9,560.

D) $0.

Which of the following is an operating activity?

A) Repaying a bank loan

B) Paying a dividend to owners

C) Purchasing a new building

D) Purchasing goods to be offered for sale

For each of the following cash activities, choose the appropriate letter to match the

activity with the internal control principle to which it relates. Each internal control

principle may be used more than once.

Activity

1> ____ A password is required to open up the cash register

2> ____ The treasurer is the person who is approved to sign checks

3> ____ A list of checks received in the mail is prepared

4> ____ A bank reconciliation is prepared each month

5> ____ The treasurer is not permitted to make bank deposits

6> ____ Checks are pre-numbered.

7> ____ Cashiers cannot approve price changes.

8> ____ Unused checks are kept in the vault.

Internal Control Principle

A. Establish responsibility

B. Segregate duties

C. Restrict access

D. Document procedures

E. Independently verify

Some analysts compare companies by focusing on earnings before interest, taxes,

depreciation, and amortization (EBITDA), rather than net income.

Which of the following was passed by Congress in response to financial statement

frauds that occurred in the early 2000s?

A) Federal Accounting Standards Board Act

B) Securities and Exchange Act

C) Sarbanes-Oxley Act

D) Clayton Act

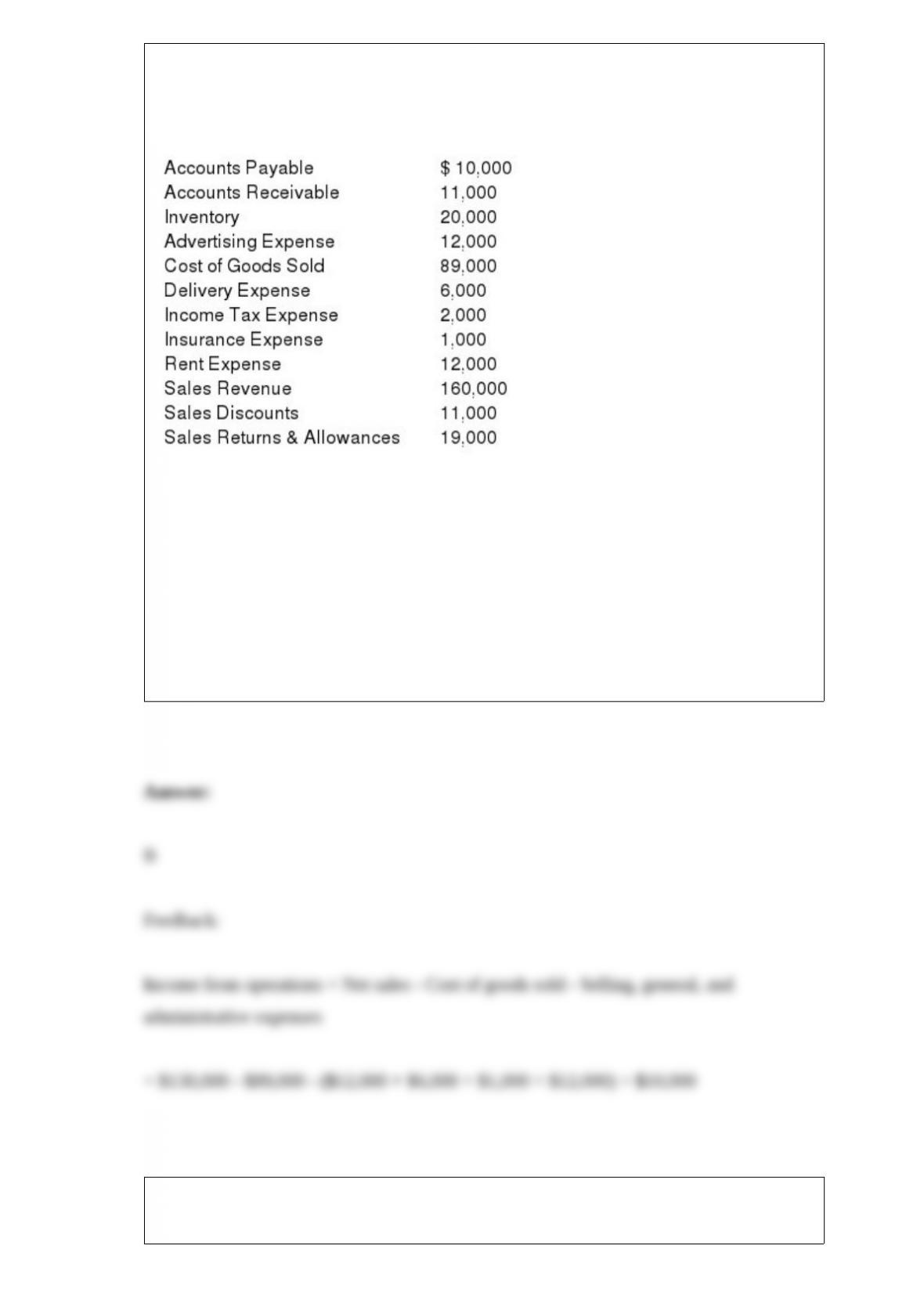

The following is a listing of some of the balance sheet accounts and all of the income

statement accounts for Aldine Inc. as they appear on the company’s adjusted trial

balance.

Use the information above to answer the following question. Income from operations

would be:

A) $6,000.

B) $10,000.

C) $11,000.

D) $12,000.

When the amount of a contingent liability can be reasonably estimated and its

likelihood is possible but not probable, the company should:

A) include a description in the notes to the financial statements.

B) record the amount of the liability times the probability of its occurrence.

C) accrue the amount of the liability as a long-term liability.

D) exclude any information about the contingent liability from its financial statements

and notes.

The book value of equipment is equal to which of the following?

A) Cost of equipment plus the related accumulated depreciation

B) Accumulated depreciation less the related depreciation expense

C) Cost of equipment less the related accumulated depreciation

D) Its accumulated depreciation plus the related depreciation expense

Adventure Company uses the aging of accounts receivable method to estimate Bad

Debt Expense. The balance of each account receivable is aged on the basis of three

categories as follows: (1) 1-30 days old, (2) 30-90 days old, and (3) more than 90 days

old. Based on experience, management has estimated what portion of receivables of a

specific age will not be paid as follows: (1) 1%, (2) 15%, and (3) 40%, respectively.

At December 31, 2016, the unadjusted credit balance in the Allowance for Doubtful

Accounts was $100. The total Accounts Receivable in each age category were: (1) 1-30

days old, $65,000, (2) 30-90 days old, $10,000, and (3) more than 90 days old, $4,000.

Required:

Part a. Calculate the estimate of uncollectible accounts at December 31, 2016.

Part b. Prepare the appropriate adjusting entry dated December 31, 2016.

On April 6, Lopez Co. purchased $5,000 of inventory, terms 1/15, n/30. Lopez Co. uses

a perpetual inventory system. The company paid for the purchase on April 26. The entry

to record the payment on April 26 includes which of the following?

A) A credit to Inventory for $50

B) A debit to Accounts Payable for $4,900

C) A credit to Accounts Payable for $5,000

D) A credit to Cash for $5,000

A company receives $95 for merchandise sold to a consumer of which $5 is for sales

tax. The $5 of sales tax:

A) increases sales revenue.

B) increases current liabilities.

C) increases selling expenses.

D) is not recorded until it is forwarded to the state government.

On January 1, 2016, Effron Inc. sells $2 million of 8% bonds at face value with interest

to be paid at the end of each year. Effron accrues interest at the end of each quarter

during the year.

Steve’s Skateboards uses the periodic inventory system and had the following sales

transactions during April:

April 2 – Sold inventory to Happy Hobby Shop on credit for $4,800, terms 1/15, n/60.

The items sold had a cost of $2,700.

April 4 – Happy Hobby Shop returned inventory that had a selling price of $200. The

cost of the inventory returned was $110.

April 13 – Happy Hobby Shop paid for the inventory sold on April 2, taking any

appropriate discount earned

Required:

Prepare the journal entries to record these transactions on the books of Steven’s

Skateboards.

Match each transaction with the type of entry that will be required at April 30, the

company’s year-end.

Transaction

____ 1> The company has $8,300 in Prepaid Rent at the beginning of April and uses

$3,600 of that for its April rent.

____ 2> The company provides lawn care in April for customers who will be billed and

make payment in May.

____ 3> The company owes interest on loans for the month of April and will not pay

this interest until May.

____ 4> The company uses $1,600 worth of fertilizer from its stock of supplies.

____ 5> The company provides lawn care in April for customers who paid in March.

____ 6> The company transfers revenues of $50,000 and expenses of $32,000 to

Retained Earnings.

____ 7> The company makes an entry to allocate the use of equipment during the

current account period.

____ 8> The company transfers the balance in the Dividends account of $1,200 to

Retained Earnings.

____ 9> The company records income taxes.

____ 10> The weekly payroll of $5,000 to be paid next week is recorded.

Type of Entry

A – Accrual adjusting entry

D – Deferral adjusting entry

C – Closing entry

Friedman Company made the following purchases during the year:

On December 31, there were 28 units in ending inventory. These 28 units consisted of 1

from the January 10 purchase, 2 from the March 15 purchase, 5 from the April 25

purchase, 15 from the July 30 purchase, and 5 from the October 10 purchase. Using

specific identification, calculate the cost of the ending inventory.

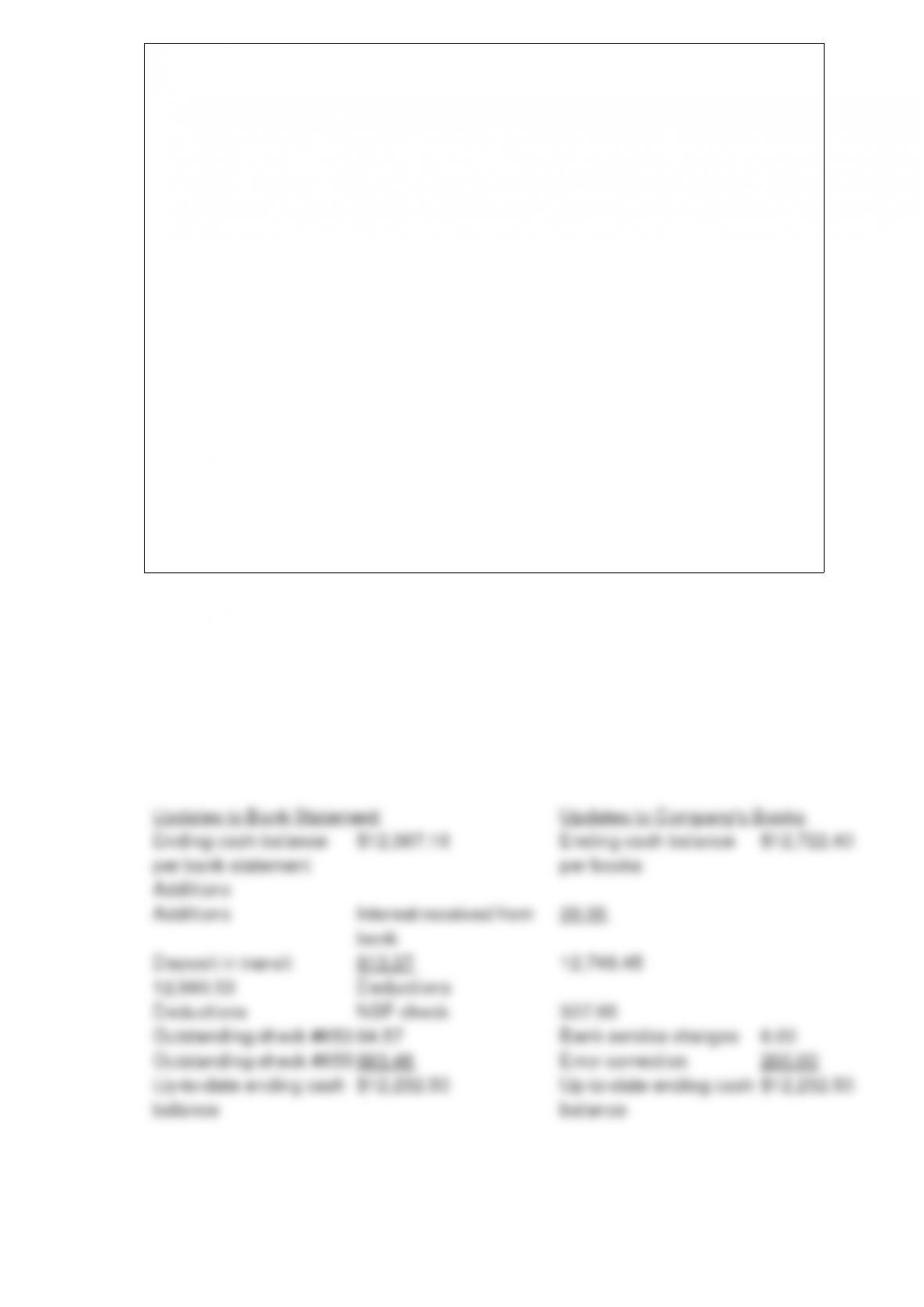

You have received the bank statement for your company’s account and need to reconcile

it with your general ledger cash account. Your records show an ending balance for the

month of $12,722.40 while the bank’s records show an ending balance of $12,367.16.

The bank charged $8 in service fees and paid $26.05 in interest.

All but three checks written during the month were processed by the bank without

incident during the month. The three exceptions were:

Check #841 was correctly processed by the bank as $981.27 but was mistakenly

recorded by you as $781.27.

Check #853 for $64.57 had not yet been processed by the bank.

Check #855 for $683.46 had not yet been processed by the bank.

All but two of the deposits made during the month were processed by the bank without

incident. The two exceptions were:

A customer check for $307.95, which had been deposited during the month, was

returned NSF.

A deposit totaling $613.37 had not yet been processed by the bank.

Required:

Using the information provided above, prepare a bank reconciliation.

Choose the appropriate letter to match the account balance change with the type of

adjustment made to net income when using the indirect method to determine net cash

flow provided by operating activities.

Account Balance Change

1> _____ Decrease in Property, Plant, and Equipment

2> _____ Increase in Accounts Receivable

3> _____ Decrease in Inventory

4> _____ Decrease in Prepaid Expenses

5> _____ Increase in Accounts Payable

6> _____ Decrease in Accrued Liabilities

7> _____ Decrease in Income Tax Payable

8> _____ Increase in Dividends Payable

9> _____ Gain on Sales of Property, Plant and Equipment

10> _____ Depreciation

Type of Adjustment

A – Add item to net income

S – Subtract item from net income

N – No adjustment necessary

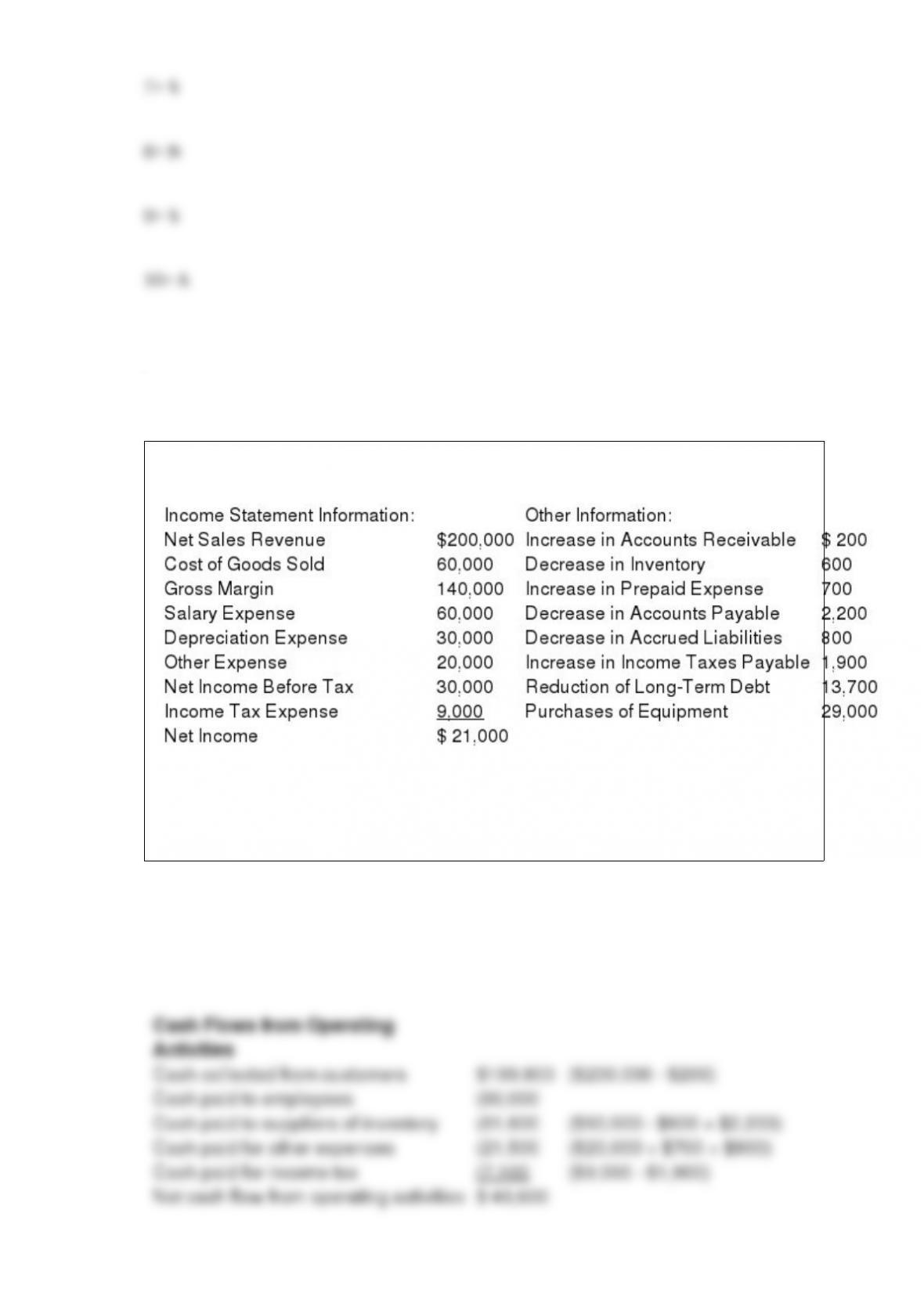

Consider the following information:

Required:

Use the direct method to compute the amount of net cash flows provided by (used in)

operating activities.