Cash sales rung up by cashiers totaled $117,000. Cash in the drawer was counted and

found to be $119,000. The journal entry to record the day’s sales would include

A. a debit to cash for $117,000.

B. a credit to cash overage for $2,000.

C. a credit to sales for $119,000.

D. a debit to sales for $117,000.

Answer:

Which of the following is the correct sequence of steps in the accounting cycle?

A. Journal entries, T-accounts, financial statements, unadjusted trial balance.

B. T-account, journal entries, unadjusted trial balance, financial statements.

C. Journal entries, T-accounts, unadjusted trial balance, financial statements.

D. Financial statements, journal entries, T-accounts, unadjusted trial balance.

Answer:

A company makes a deferral adjustment that reduces a liability. This must mean:

A. an expense account is decreasing by the same amount.

B. an expense account is increasing by the same amount.

C. a revenue account is increasing by the same amount.

D. a revenue account is decreasing.

Answer:

Cash flow from investing activities includes

A. amounts received from a company’s stockholders for the sale of stock.

B. amounts received from the sale of the company’s office building.

C. amounts paid for dividends to the company’s stockholders.

D. amounts paid for salaries of employees.

Answer:

Some analysts compare companies by focusing on earnings before interest, taxes,

depreciation, and amortization (EBITDA), rather than net income.

Answer:

Choose the appropriate letter to match the term and the definition. Not all definitions

will be used.

Term:

_____ 1/ Treasury stock

_____ 2/ Cash dividend

_____ 3/ IPO

_____ 4/ Preferred stock

_____ 5/ Outstanding shares

_____ 6/ EPS

_____ 7/ Stock dividend

_____ 8/ Residual claim

_____ 9/ ROE

Definition:

A. When a company first starts selling stock to the public.

B. The additional shares of stock a company can issue beyond what are already issued.

C. Earnings per share that reflects treasury and preferred stock.

D. This payment raises stockholders’ equity.

E. Net income divided by average stockholders’ equity.

F. The shares of stock held by stockholders.

G. Stock shares that pay a fixed dividend rate but have no voting rights.

H. Net income divided by the average number of outstanding common shares.

I. Stock that allows owners to be listed among creditors.

J. This dividend does not reduce stockholders’ equity.

K. The shares of stock held by the issuing company.

L. Stockholders’ entitlement to remaining assets after creditors are repaid.

M. This payment decreases stockholders’ equity.

Answer:

Assume that, prior to preparing adjusting entries at the end of the year, Caterpillar

Corporation has a fixed asset turnover ratio of 3.4 based on average net fixed assets of

$500,000,000. Which of the following year-end adjustments would cause Caterpillar’s

fixed asset turnover ratio to increase?

A. Caterpillar accrues and capitalizes $50,000 for self-constructed assets.

B. Caterpillar accrues a liability for ordinary repair costs in the amount of $50,000.

C. Caterpillar writes down an impaired piece of equipment by $50,000.

D. Caterpillar increases the sales returns & allowances by $50,000.

Answer:

Typically, a profitable company that pays relatively high dividends:

A. is an attractive investment for those seeking a steady income, like retired people.

B. will reinvest more profit which can lead to smaller growth potential.

C. will experience more growth in stock price over time.

D. is a bad investment.

Answer:

If the market value of goods in inventory falls to $26,000 below its cost, the company

should:

A. do nothing, because assets are reported at their original purchase price.

B. credit inventory for $26,000.

C. debit inventory for $26,000.

D. use the weighted average cost method since that method provides a more accurate

indicator of current value.

Answer:

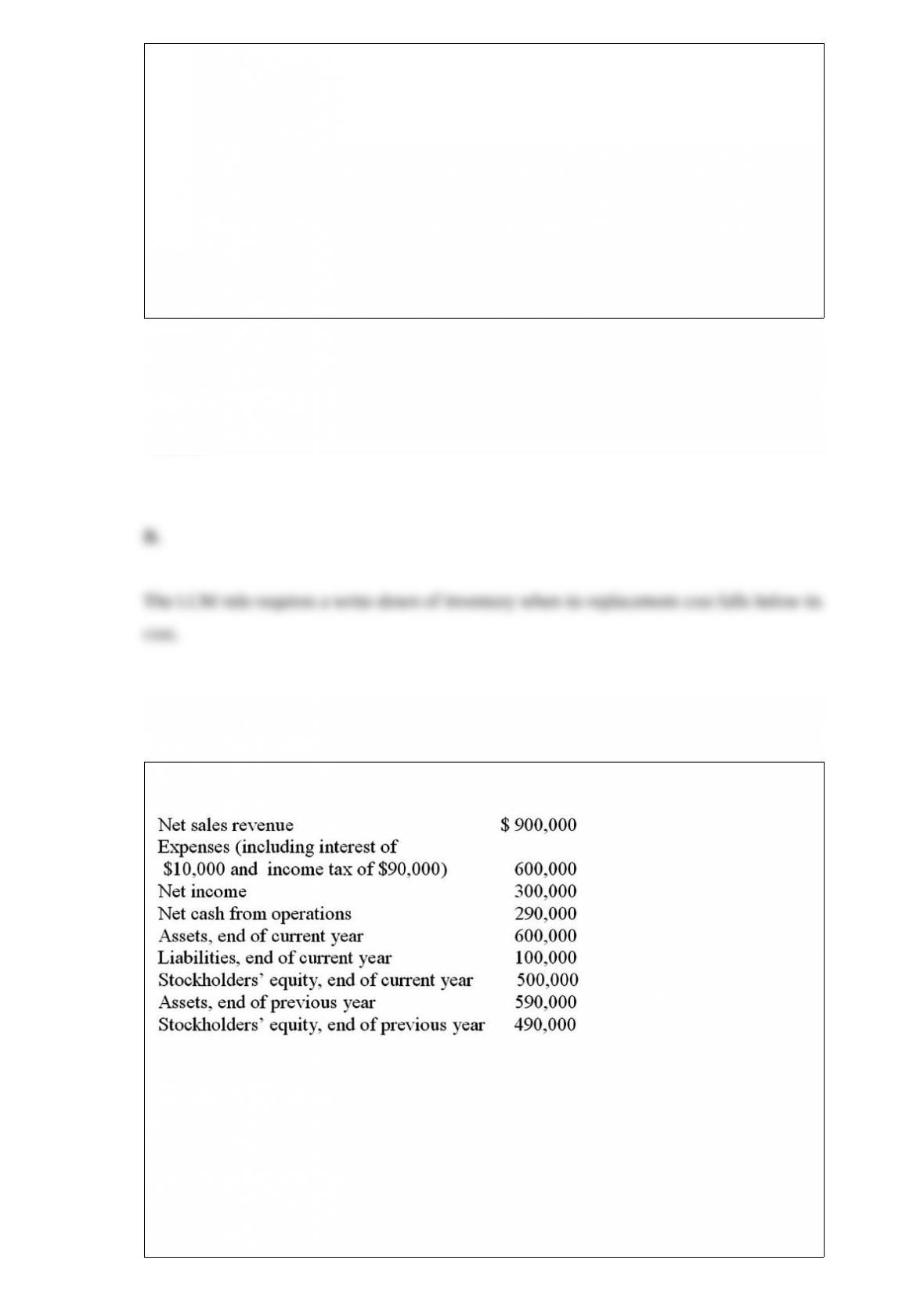

The following information is taken from the financial statements of B. Darin Company:

In addition, there was an average of 40,000 shares of common stock outstanding and

the current market price of the stock is $15 per share.

Use the information above to answer the following question. Which of the following is

closest to the company’s Times Interest Earned ratio for the current year?

A. 30

B. 40

C. 3

D. 0.025

Answer:

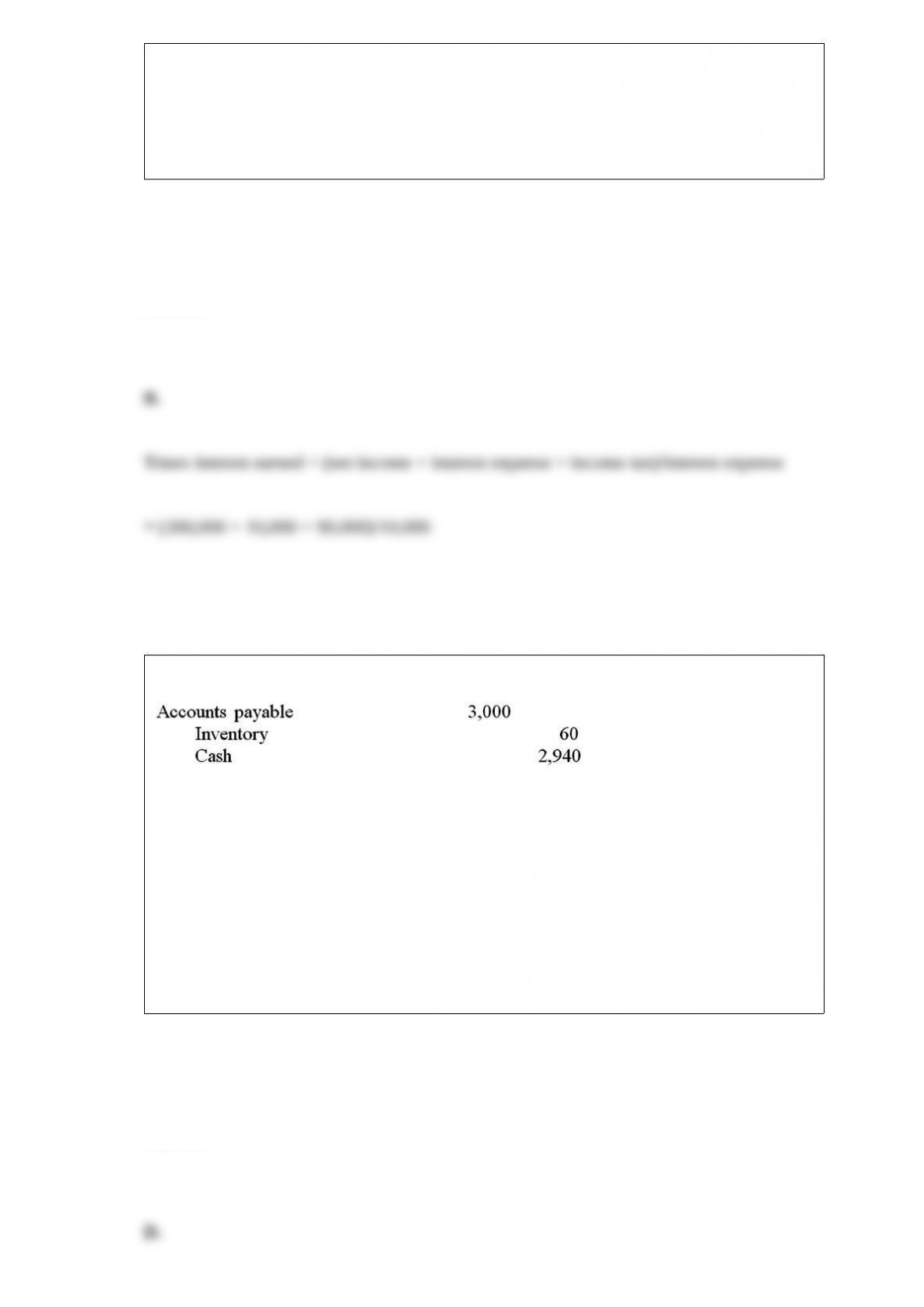

A company using a perpetual inventory system made the following entry:

What does this entry reflect?

A. A purchase of inventory at a discount.

B. A return of inventory for credit.

C. A sale of inventory on account.

D. A payment within the discount period for inventory previously purchased on credit.

Answer:

Benchmarks are not

A. points of comparison to use in evaluating financial statement amounts.

B. prior period results of a company which provide trend information.

C. competitor financial information to be used to evaluate a company’s performance.

D. evaluations of a single business in a single period.

Answer:

A company has gross profit of $58,300 and a gross profit percentage of 25%. What is

the company’s net sales?

A. $233,200.

B. $14,575.

C. $72,825.

D. $711,260.

Answer:

The first financial statement prepared after the adjusted trial balance is:

A. the balance sheet.

B. the income statement.

C. the statement of cash flows.

D. the statement of retained earnings.

Answer:

When originally purchased, a vehicle had an estimated useful life of 8 years. The

vehicle cost $25,000 and its estimated residual value is $3,000. After 3 years of

straight-line depreciation, the asset’s total estimated useful life was revised from 8 years

to 5 years and there was no change in the estimated residual value. The depreciation

expense in year 4 is

A. $6,875.

B. $4,400.

C. $4,125

D. $1,650.

Answer:

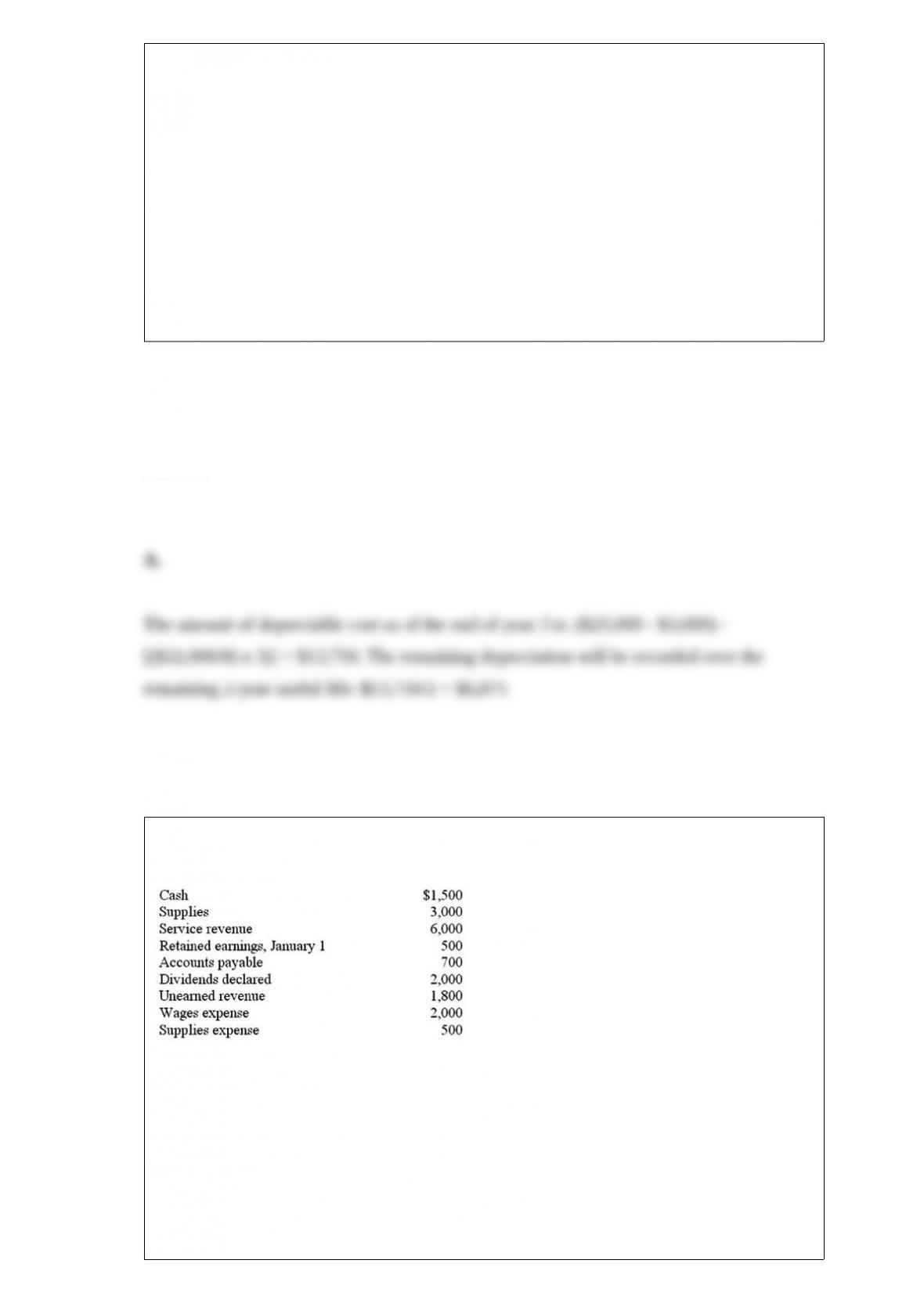

The December 31, 2013, adjusted trial balance of a company, where all accounts have

normal balances is:

Given this information, after all closing entries are made, the balance in the retained

earnings account is:

A. $2,000.

B. $4,000.

C. $0.

D. $1,500.

Answer:

Choose the appropriate letter to match the term and the definition. Not all definitions

will be used.

Term:

_____ 1/ Convertible

_____ 2/ Carrying value

_____ 3/ Discount

_____ 4/ Callable

_____ 5/ Maturity

_____ 6/ Market interest rate

_____ 7/ Stated interest rate

_____ 8/ Premium

Definition:

A. A bond feature that changes the interest rate on the bond with market conditions.

B. When a bond is issued for a price less than its face value.

C. Also known as the face value or par value of a bond.

D. A bond with the feature that allows creditors to exchange the bond for company

stock.

E. The interest rate printed on the bond certificate.

F. A bond with the feature that lets creditors examine financial data and demand new

loan conditions.

G. The amount a company receives when it sells a bond; also known as issue price.

H. When a bond is issued for a price greater than its face value.

I. A bond with the feature that allows the borrowing company to pay off a bond

whenever it wishes.

J. Rate of interest that investors demand from a bond.

K. The time at which the face value of a bond must be paid to the lender.

L. Is multiplied by the market interest rate to calculate the (effective) interest expense

on a bond.

Answer:

Which of the following factors would lead a company to prefer equity financing?

A. Interest rates are high.

B. The company’s stock price is low.

C. The company is in a high tax bracket.

D. The company currently has a low debt ratio.

Answer:

An increasing balance in the inventory account and a declining inventory turnover ratio

implies that the inventory build up is occurring because:

A. goods are not selling as fast as they were in the past.

B. the company is expecting to sell more in the future.

C. goods are selling, but it is taking longer to collect payment.

D. goods cannot be shipped fast enough.

Answer:

A company has net sales of $612,850 and cost of goods sold of $441,252. The

company’s gross profit percentage is:

A. 72%.

B. 0.28%.

C. 38.9%.

D. 28%.

Answer:

On October 31, 2013, the bank’s records say that your company has $12,973 in its

checking account. You are aware of three outstanding checks for a total of $2,112.19.

During October, 2013, the bank rejected two deposited checks from customers totaling

$654.19 because of insufficient funds and charged you $12.00 in service fees. You had

not yet received notice about the bad checks, but you were aware of and have recorded

the $12.00 of service fees. Prior to adjustment on October 31, 2013, your Cash account

would have a balance of:

A. $14,402.73.

B. $15,711.11.

C. $11,498.73.

D. $10,202.35.

Answer:

The best interpretation of the word “credit” is the

A. left side of an account.

B. increase side of an account.

C. right side of an account.

D. decrease side of an account.

Answer:

Which of the following accounts would normally have a credit balance?

A. Inventory

B. Cost of goods sold

C. Sales

D. Sales returns & allowances

Answer:

The net amount shown on a balance sheet for an intangible asset with an unlimited life

should be:

A. the price for which it could be sold.

B. its book value or impaired fair value, whichever is lower.

C. its purchase price minus accumulated amortization.

D. its purchase price adjusted for inflation.

Answer:

During one pay period, your company distributes $130,500 to employees as net pay.

The income tax withholdings were $19,000 and the FICA withholdings were $5,000.

The total wages and payroll tax expense to the company for this pay period, excluding

any unemployment taxes, was:

A. $149,500.

B. $130,500.

C. $154,500.

D. $159,500.

Answer:

How does an asset impairment loss impact a company’s financial statements?

A. Raises expenses and lowers both revenue and net income.

B. Lowers assets, stockholders’ equity, and net income.

C. Raises expenses and lowers net income with no effect on any other items.

D. Raises liabilities and lowers stockholders’ equity.

Answer:

GE buys back 300,000 shares of its stock from investors at $45 a share. Two years later

it reissues this stock for $65 a share. The stock reissue would be recorded as:

A. a debit to Cash of $19.5 million and a credit to Treasury Stock of $19.5 million.

B. a debit to Cash of $13.5 million, a debit to Additional Paid-in Capital of $6 million, a

credit to Treasury Stock of $13.5 million, and a credit to Stockholders’ Equity of $6

million.

C. a debit to Cash of $19.5 million, a credit to Treasury Stock of $13.5 million, and a

credit to Additional Paid-in Capital of $6 million.

D. a debit to Cash of $19.5 million, a credit to Treasury Stock of $13.5 million, and a

credit to Gain on Sale of Treasury Stock of $6 million.

Answer:

Payroll taxes paid by employees include which of the following?

A. Federal income tax, federal unemployment tax, and Medicare.

B. Social security tax, federal unemployment tax, and state unemployment tax.

C. FICA taxes, federal unemployment tax, and state unemployment tax.

D. Federal income tax, state income tax, and Medicare.

Answer:

One major difference between deferral and accrual adjustments is:

A. accrual adjustments affect income statement accounts and deferral adjustments affect

balance sheet accounts.

B. deferral adjustments increase net income and accrual adjustments decrease net

income.

C. deferral adjustments are made under the cash basis of accounting and accrual

adjustments are made under the accrual basis of accounting.

D. accounts affected by an accrual adjustment always go in the same direction (i.e.,

both accounts are increased or both accounts are decreased) and accounts affected by a

deferral adjustment always go in opposite directions.

Answer:

In a period of rising prices, the inventory costing method that will tend to smooth out

erratic changes in costs is

A. FIFO.

B. LIFO.

C. Weighted average.

D. Specific identification.

Answer:

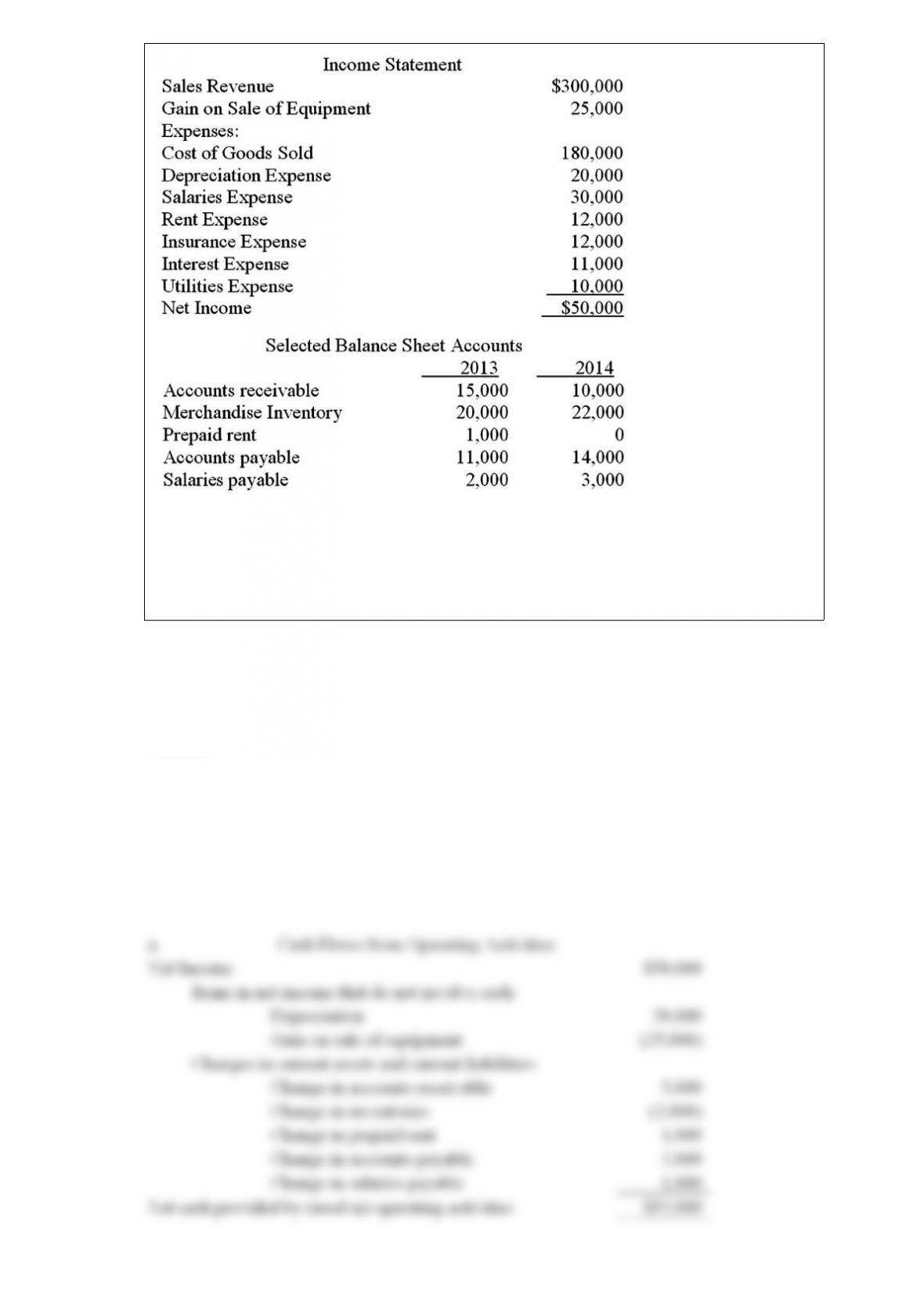

The income statement and selected balance sheet information for Fudnuddler

Corporation for the year ended December 31, 2014 is presented below.

a. Prepare the cash flows from operating activities section of the 2014 statement of cash

flows using the indirect method.

b. Comment on the reasons for the net cash flow from operating activities.

Answer:

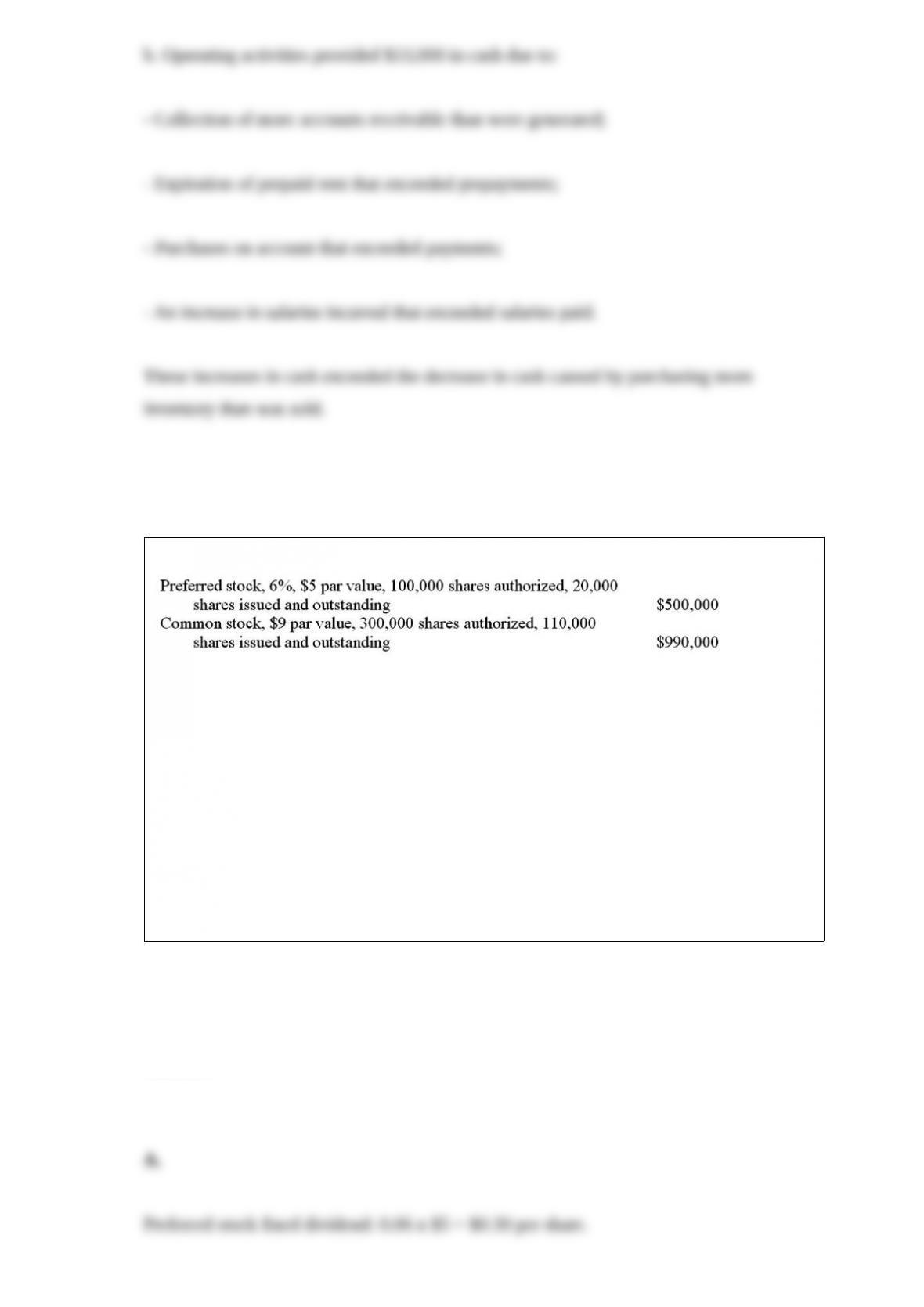

A company has the following paid-in capital:

Use the information above to answer the following question. If the company pays a

$35,000 dividend, and the preferred stock is cumulative and two years’ dividends are in

arrears, what is the amount the common stockholders will receive?

A. $17,000

B. $23,000

C. $29,000

D. $35,000

Answer:

The days-to-collect measure is calculated as:

A. the number of days an average selling and collecting cycle takes.

B. the average number of times the firm completes the selling and collecting cycle

during the year.

C. the average number of days for a customer’s payment to clear the banking system.

D. the average number of days before the company receives a customer’s payment and

uses the cash to re-order merchandise.

Answer:

The three key pieces of information that are stated on a bond certificate are:

A. the interest payment, the face value of the bond, and the credit rating of the

company.

B. the market interest rate, the price of the bond, and the maturity date.

C. the stated interest rate, the face value of the bond, and the maturity date.

D. the interest payment, the issue price of the bond, and the credit rating of the

company.

Answer: