Which of the following usually results in an increase in a deferred tax asset?

a. Accelerated depreciation for tax reporting and straight-line depreciation for financial

reporting.

b. Prepaid insurance.

c. Subscriptions delivered for which customers had paid in advance.

d. None of these answer choices are correct.

The FASB’s standard-setting process includes, in the correct order:

a. Exposure draft, research, discussion paper, Accounting Standards Update.

b. Research, exposure draft, discussion paper, Accounting Standards Update.

c. Research, discussion paper, exposure draft, Accounting Standards Update.

d. Discussion paper, research, exposure draft, Accounting Standards Update.

On January 1, 2016, Princess Corporation leased equipment to King Company. The

lease term is eight years. The first payment of $675,000 was made on January 1, 2016.

The equipment cost Princess Corporation $3,600,000. The present value of the

minimum lease payments is $3,960,000. The lease is appropriately classified as a

sales-type lease. Assuming the interest rate for this lease is 10%, how much interest

revenue will Princess record in 2017 on this lease?

a. $261,000.

b. $328,500.

c. $325,350.

d. $293,850.

Which of the following is a contingency that would most likely require accrual?

a. Potential claims on extended warranties.

b. Customer premium offers.

c. Potential liability on a product where none have yet been sold.

d. Sales tax payable.

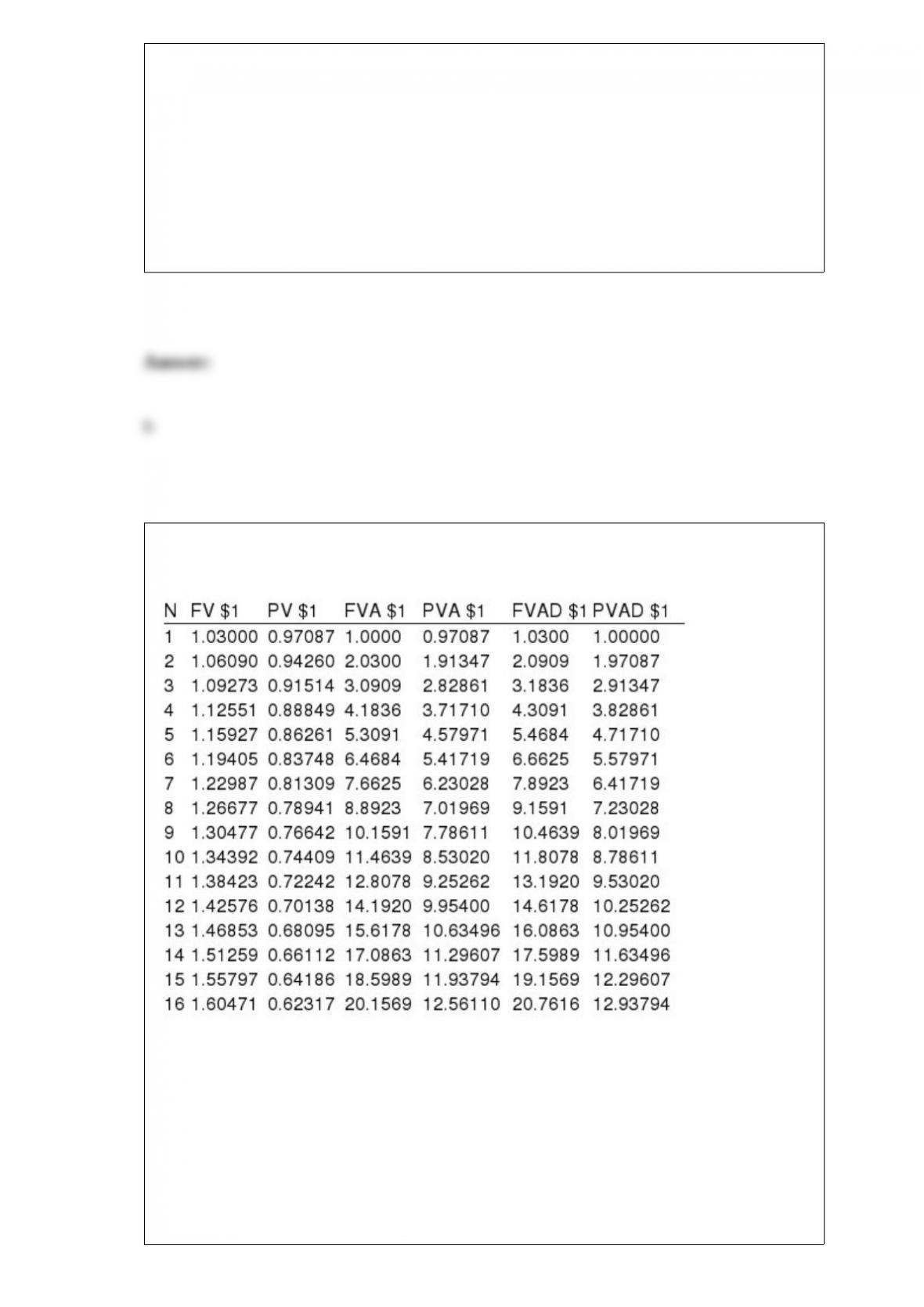

Present and future value tables of $1 at 3% are presented below:

Sondra deposits $2,000 in an IRA account on April 15, 2016. Assume the account will

earn 3% annually. If she repeats this for the next nine years, how much will she have on

deposit on April 14, 2023?

a. $20,600.

b. $20,928.

c. $23,616.

d. $24,715.

The distinction between operating and nonoperating income relates to:

a. Continuity of income.

b. Primary activities of the reporting entity.

c. Consistency of income stream.

d. Reliability of measurements.

A direct financing lease is classified in the lessor’s balance sheet as:

a. An asset.

b. A liability.

c. Interest revenue.

d. A contra account to lease liability.

In the Norwalk Agreement, the FASB and IASB pledged to:

a. Combine their organizations to form the BUSYB.

b. Make progress on specific MOU projects.

c. Achieve convergence by the year 2015.

d. Remove existing differences between their standards.

Lance Chips granted restricted stock units (RSUs) representing 40 million of its $1 par

common shares to executives, subject to forfeiture if employment is terminated within

four years. After the recipients of the RSUs satisfy the vesting requirement, the

company will distribute the shares. The common shares had a market price of $5 per

share on the grant date. The total compensation cost pertaining to the restricted stock

units is:

A. $ 5 million.

B. $ 40 million.

C. $ 50 million.

D. $200 million.

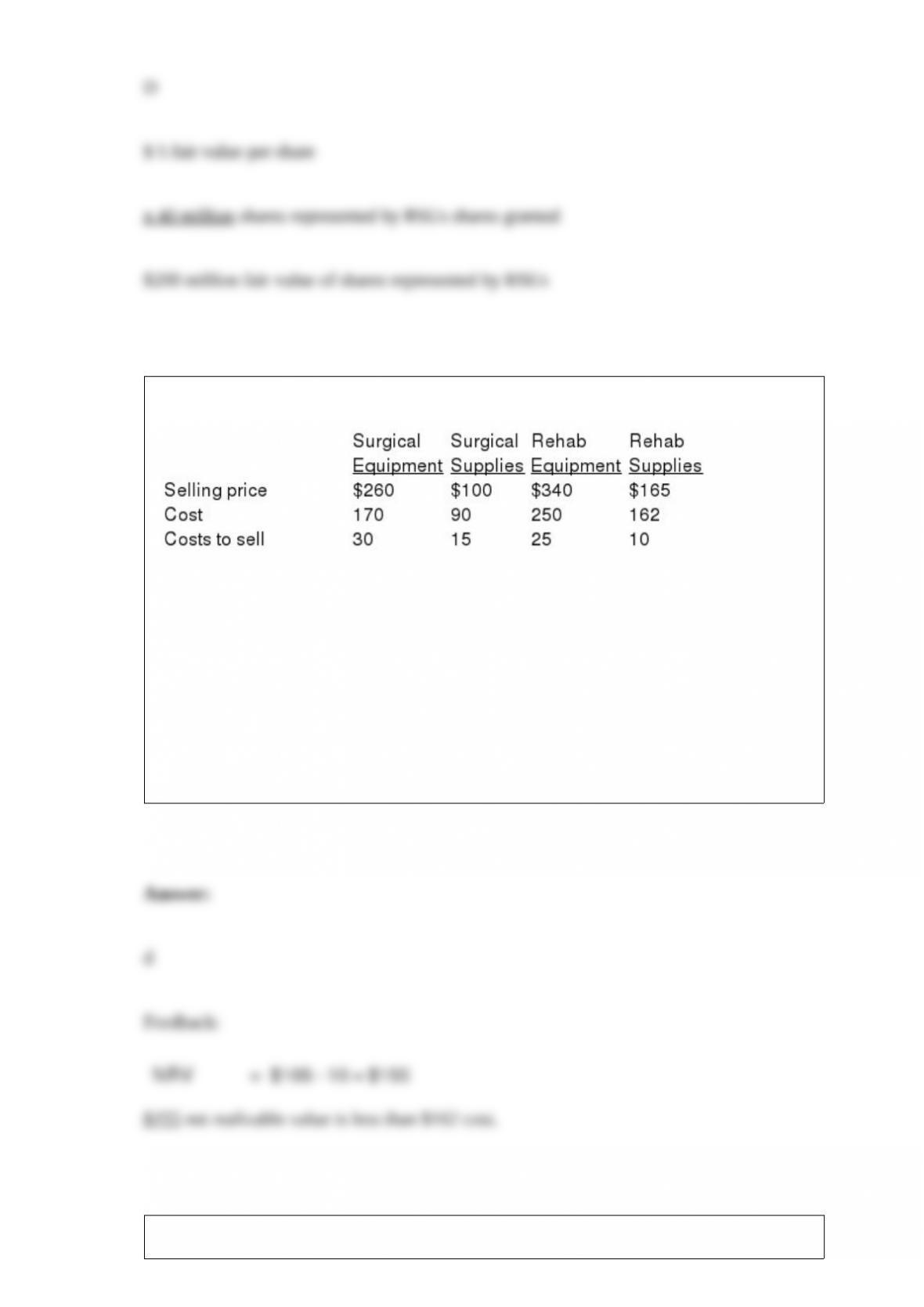

Data related to the inventories of Costco Medical Supply are presented below:

In applying the lower of cost and net realizable value rule, the inventory of rehab

supplies would be valued at:

a. $165.

b. $152.

c. $162.

d. $155.

For 2016, Rahal’s Auto Parts estimates bad debt expense at 1% of credit sales. The

company reported accounts receivable and an allowance for uncollectible accounts of

$86,500 and $2,100, respectively, at December 31, 2015. During 2016, Rahal’s credit

sales and collections were $404,000 and $408,000, respectively, and $2,340 in accounts

receivable were written off.

Rahal’s adjusted allowance for uncollectible accounts at December 31, 2016, is:

a. $4,340.

b. $4,100.

c. $3,800.

d. $4,040.

On January 1, 2016, Zebra Corporation issued 1,000 of its 8%, $1,000 bonds at 98.

Interest is payable semiannually on January 1 and July 1. The bonds mature on January

1, 2026. Zebra paid $50,000 in bond issue costs. Zebra uses the straight-line

amortization method. What is the bond book value reported in the December 31, 2016,

balance sheet?

a. $1,045,000.

b. $1,040,000.

c. $987,000.

d. $982,000.

From the perspective of the lessee, leases may be classified as either:

a. Direct financing or sales-type.

b. Capital or direct financing.

c. Capital or operating.

d. Direct financing or operating.

The rate of return on assets indicates:

a. The margin of safety provided to creditors.

b. The extent of “trading on the equity” or financial leverage.

c. Profitability without regard to how resources are financed .

d. The effectiveness of employing resources provided by owners.

Canliss Mining uses the retirement method to determine depreciation on its office

equipment. During 2014, its first year of operations, office equipment was purchased at

a cost of $14,000. Useful life of the equipment averages four years and no salvage value

is anticipated. In 2016, equipment costing $5,000 was sold for $600 and replaced with

new equipment costing $6,000. Canliss would record 2016 depreciation of:

a. $3,500.

b. $4,400.

c. $5,400.

d. None of these answer choices are correct.

•

Interest is eligible to be capitalized as part of an asset’s cost, rather than being expensed

immediately, when:

a. The interest is incurred during the construction period of the asset.

b. The asset is a discrete construction project for sale or lease.

c. The asset is self-constructed, rather than acquired.

d. All of these answer choices are correct.

If a company uses LIFO, a LIFO liquidation causes a company’s income taxes to

increase:

a. When inventory purchase costs are rising.

b. When inventory purchase costs are declining.

c. Whether inventory purchase costs are declining or rising.

d. LIFO liquidations have no effect on a company’s income taxes.

Which of the terms or phrases listed below is more associated with financial statements

prepared in accordance with U.S. GAAP than with International Financial Reporting

Standards?

a. Accumulated other comprehensive income.

b. Investment revaluation reserve.

c. Share premium.

d. Preference shares.

In terms of business volume, the dominant form of business organization is the:

a. Partnership.

b. Corporation.

c. Limited liability company.

d. Proprietorship.

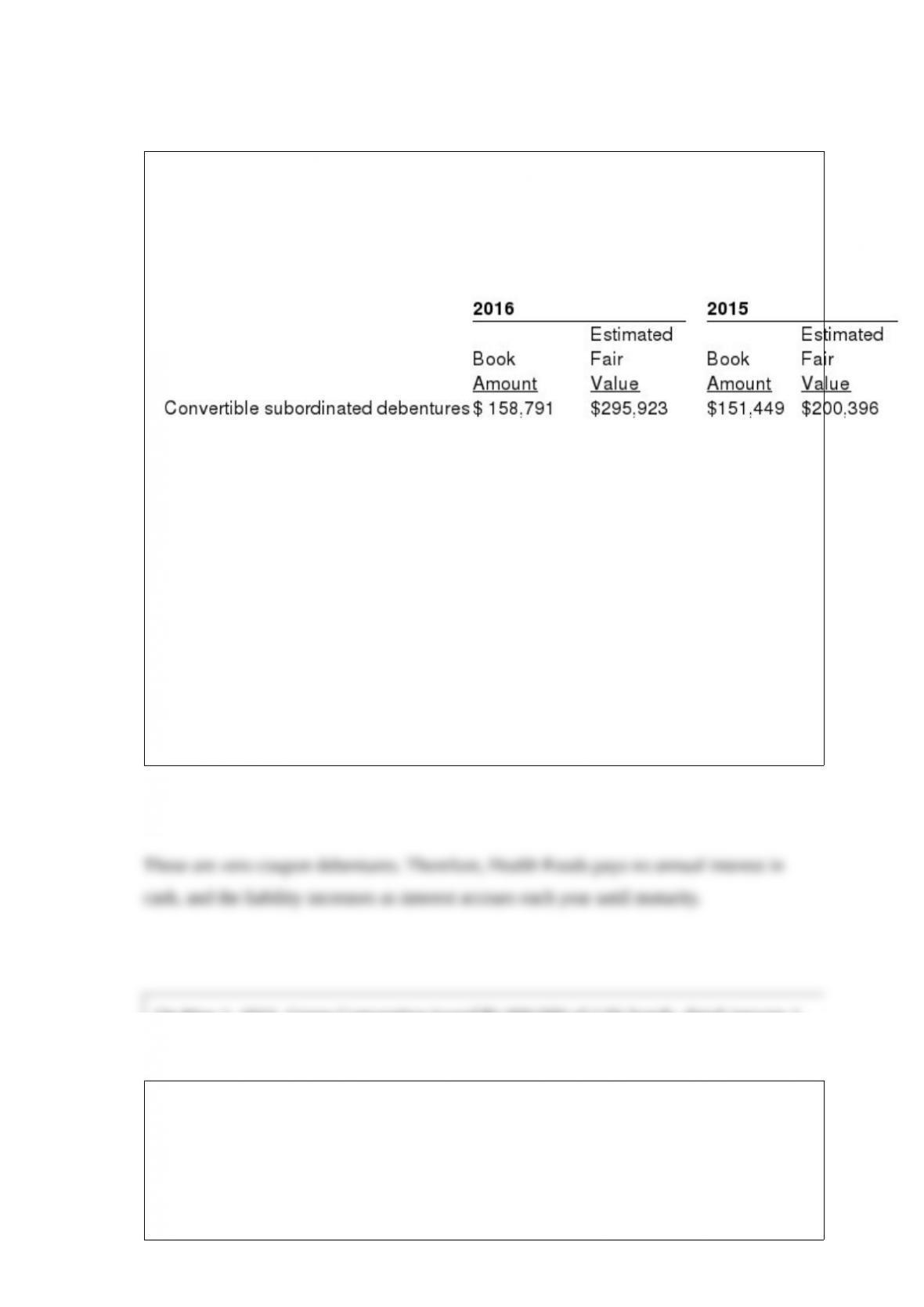

In its 2016 annual report to shareholders, Health Foods, Inc., disclosed the following

information about some of its indebtedness: The fair value of convertible subordinated

debentures is estimated using quoted market prices. Book amounts and estimated fair

values of our financial instruments other than those for which book amounts

approximate fair values as noted above are as follows (in thousands)

In addition, the company disclosed the following: We have outstanding zero coupon

convertible subordinated debentures which had a book amount of approximately $158.8

million and $151.4 million at September 26, 2016, and September 28, 2015,

respectively. The debentures have an effective yield to maturity of 5 percent and a

principal amount at maturity on March 2, 2030, of approximately $308.8 million. The

debentures are convertible at the option of the holder, at any time on or prior to

maturity, unless previously redeemed or otherwise purchased. The debentures have a

conversion rate of 10.64 shares per $1,000 principal amount at maturity, representing

3,285,632 shares. The debentures may be redeemed at the option of the holder on

March 2, 2020, or March 2, 2025, at the issue price plus accrued original discount

totaling approximately $188 million and $241 million, respectively.

Required: Why did the book amount of the debentures increase during fiscal year

2016?

On May 1, 2016, Green Corporation issued $1,000,000 of 12% bonds, dated January 1,

2016, for $975,000 plus accrued interest. The bonds mature on December 31, 2030, and

pay interest semiannually on June 30 and December 31. Green’s fiscal year ends on

December 31 each year.

Required:

1> Determine the amount of accrued interest that was included in the proceeds received

from the bond sale. Show calculations.

2> Prepare the journal entry for the issuance of the bonds.

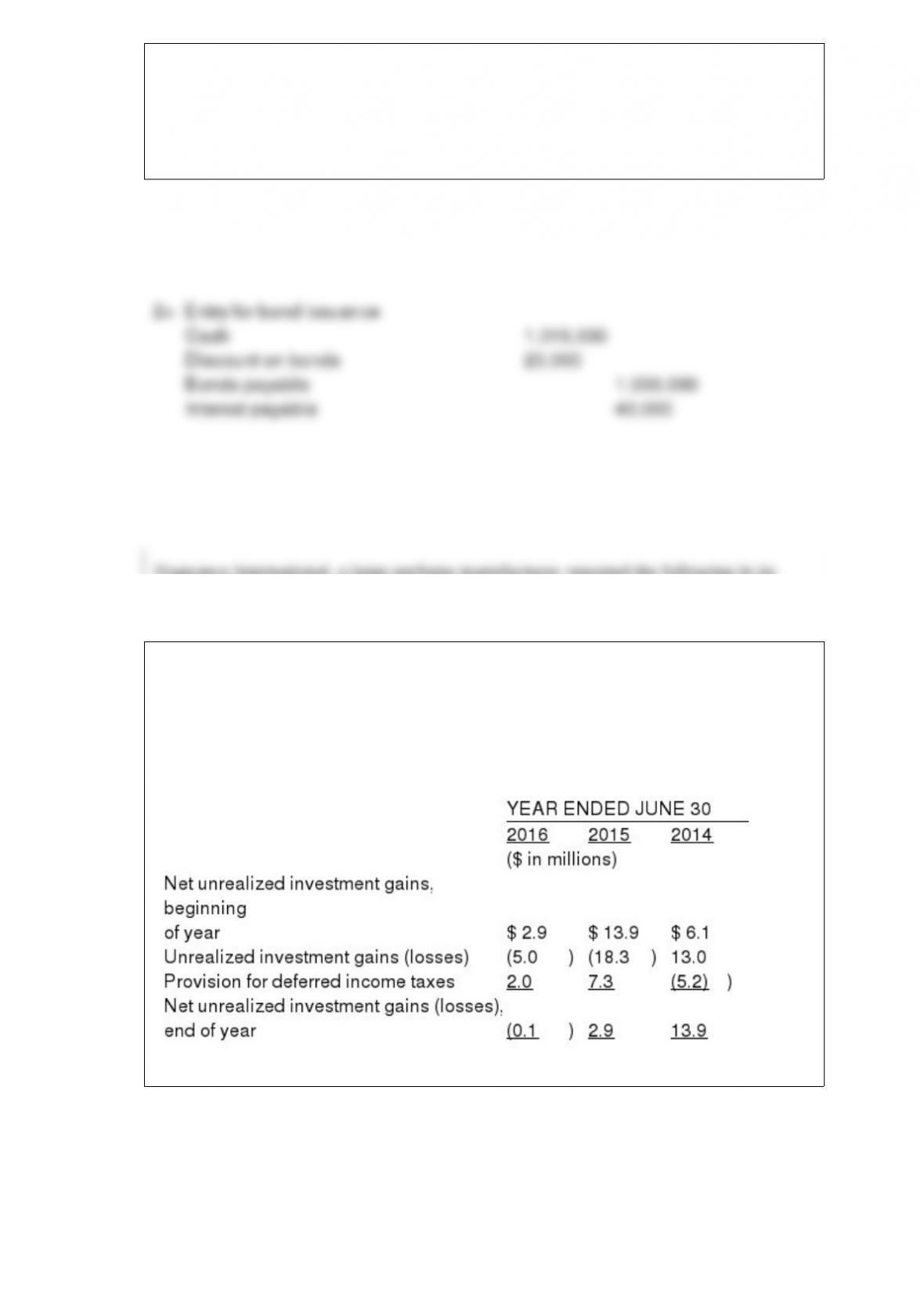

Fragrance International, a large perfume manufacturer, reported the following in its

2016 annual report to shareholders: ACCUMULATED OTHER COMPREHENSIVE

INCOME The components of accumulated other comprehensive income (loss)

(“AOCI”) included in the accompanying consolidated balance sheets consist of the

following:

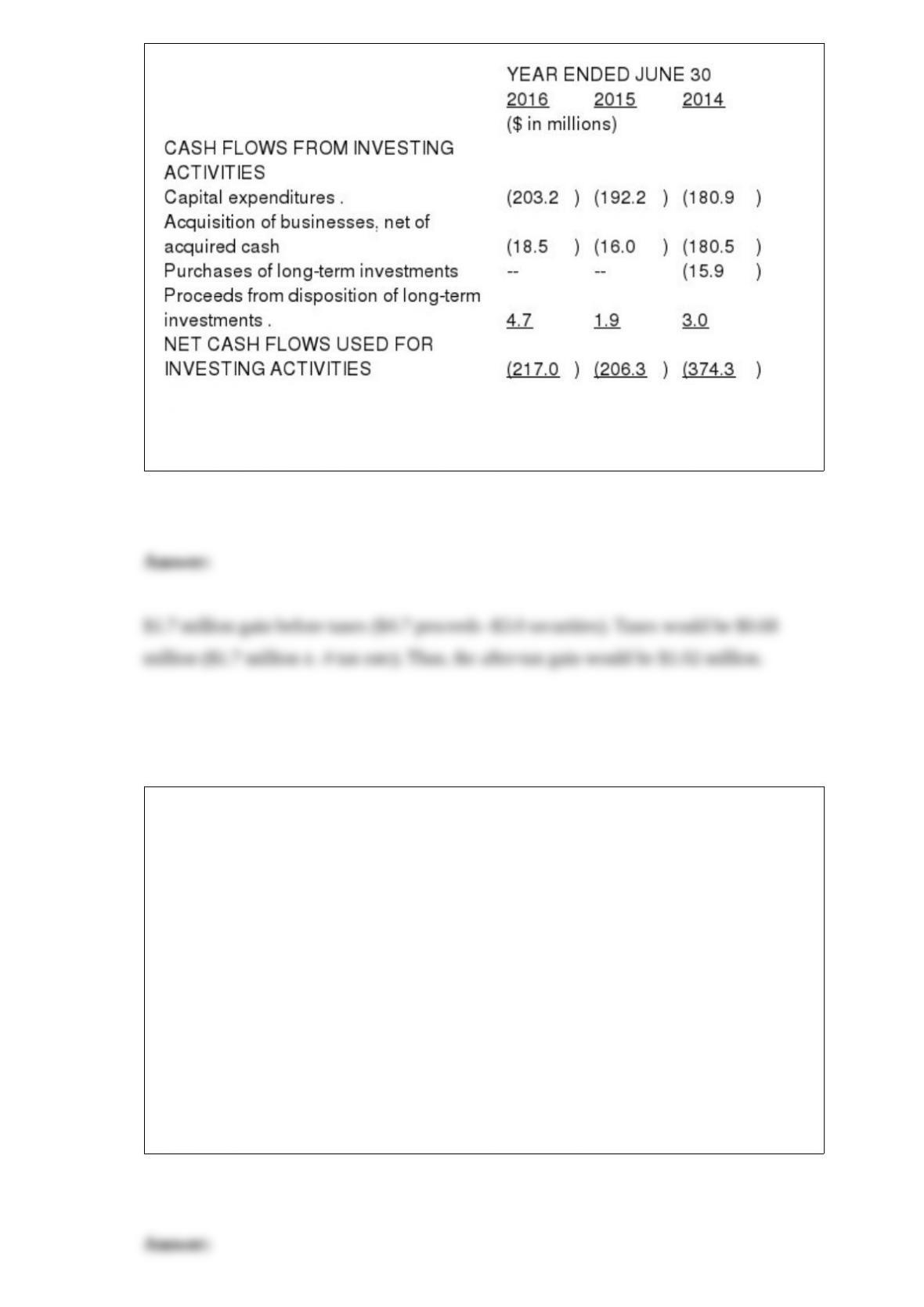

CONSOLIDATED STATEMENTS OF CASH FLOWS

Investments sold during 2016 originally cost $3.0 million. What was the after-tax

realized gain or loss on the sale of available-for-sale securities in 2016? Assume a 40%

tax rate.

In 2016, Southwestern Corporation completed the treasury stock transactions listed

below.

February 2: Reacquired 70,000 shares at $12.

March 17: Sold 20,000 shares at $14.

May 17: Sold 25,000 shares at $8.

Southwestern had issued 100,000 shares of its $1 par common stock for $10 several

months ago.

Required:

Prepare the journal entries to record the above transactions using the cost method.

Atlas Trucking incurred the following costs during 2016:

1> Spent $15,000 on a major overhaul for a tractor-trailer rig. The overhaul is expected

to increase the service life of the rig by three years.

2> Repaired the air-conditioning system for $3,000.

3> Rearranged and reconfigured the maintenance, loading, and unloading facilities at a

cost of $75,000. The rearrangement is expected to result in substantial cost savings and

increased efficiency over the next several years.

Required:

Prepare journal entries to record the above costs.

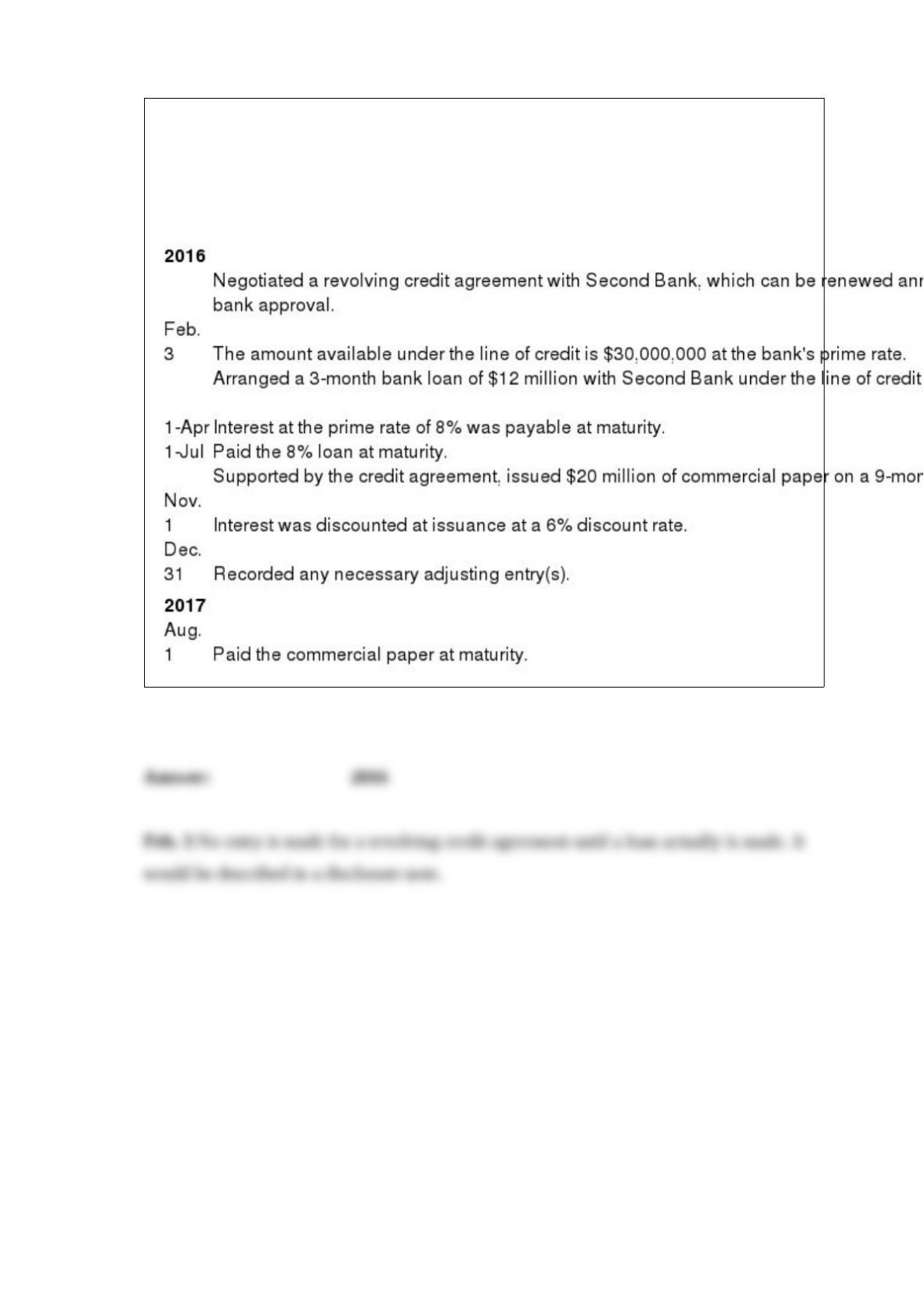

The following selected transactions relate to liabilities of Rose Dish Corporation. Rose’s

fiscal year ends on December 31. Required:

Prepare the appropriate journal entries through the maturity of each liability.

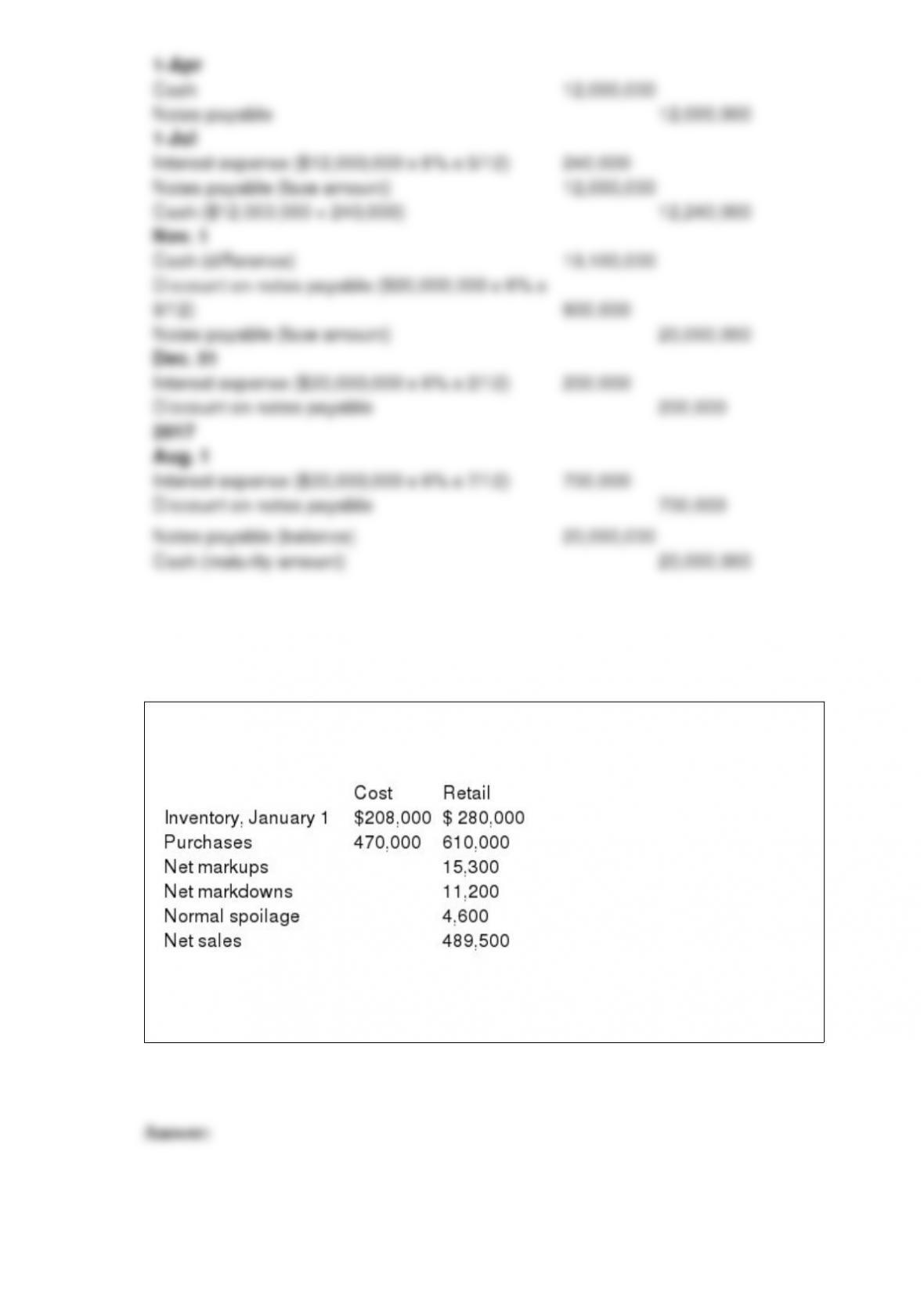

Harley Inc. uses the conventional retail method to estimate its ending inventories. The

following data has been summarized for December 31, 2016:

Required:

Estimate the cost of ending inventory applying the conventional retail method.

Explain how the loss is reported in the financial statements (other than the balance

sheet).

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.

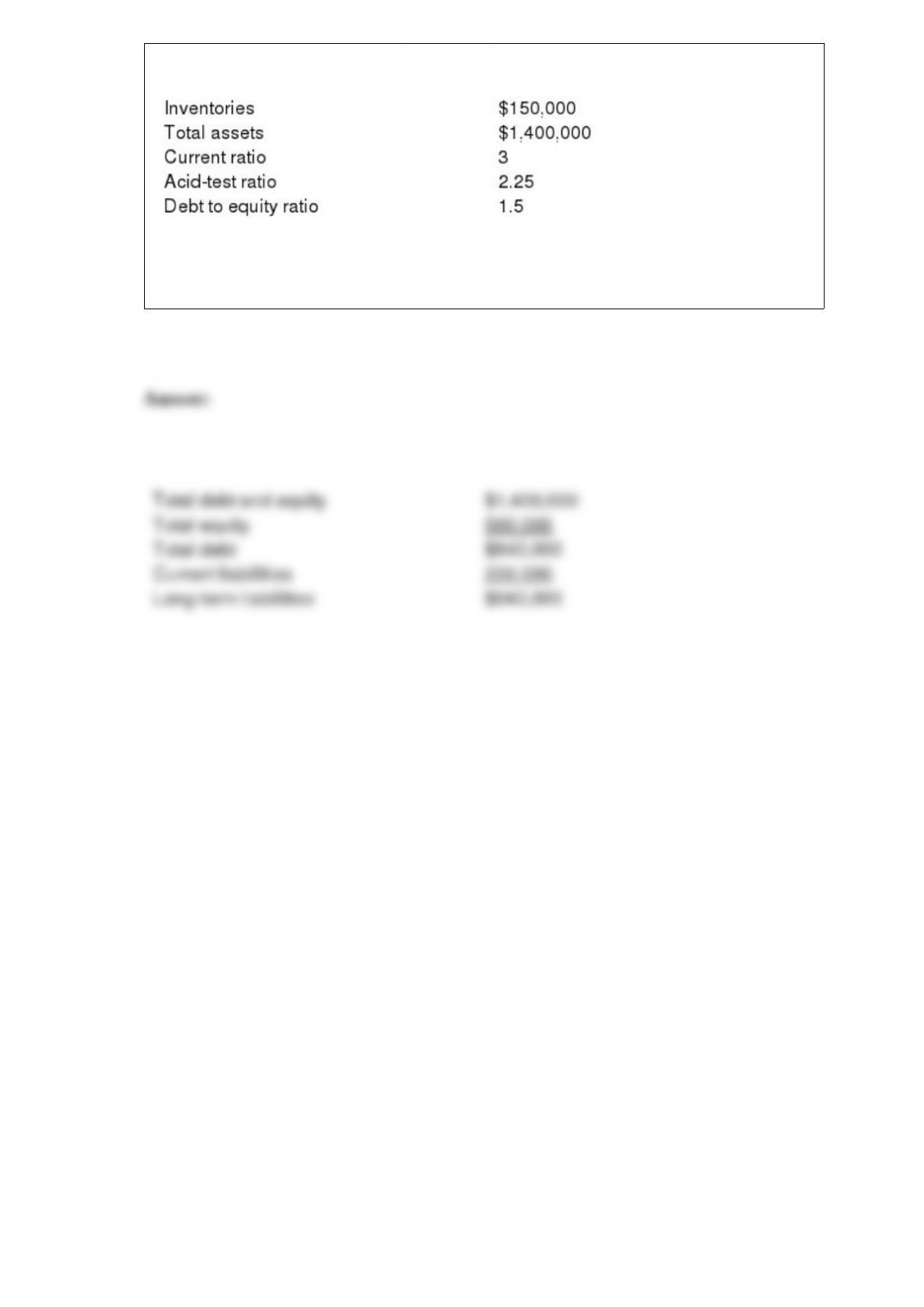

Bronco Electronics’ current assets consist of cash, marketable securities, accounts

receivable, and inventories. The following data were abstracted from a recent financial

statement:

Required: Compute the following for Bronco:

Long-term liabilities