In a statement of cash flows prepared under International Financial Reporting

Standards, interest received is most often classified as an operating cash flow.

If a pension plan is underfunded, the company has a net loss-OCI.

Valuation allowances reduce deferred tax liabilities to the amount that is more likely

than not to be payable in the future.

Inventory costing methods are merely means by which costs are allocated between

ending inventory and cost of goods sold.

International Financial Reporting Standards allow the reversal of an inventory

write-down.

According to International Financial Reporting Standards (IFRS), an impairment loss

for property, plant, and equipment is required only when an asset’s book value exceeds

the undiscounted sum of the asset’s estimated future cash flows.

A change to the LIFO method of valuing inventory usually requires use of the

retrospective method.

Companies are not required to, but have the option to, value some or all of their

financial assets and liabilities at fair value.

A decrease in the receivables turnover ratio indicates a decrease in the time between

credit sales and cash collection.

An unrealized gain from marking an investment to fair value typically creates a

deferred tax asset.

Property, plant, and equipment and finite-life intangible assets must be tested for

impairment at least once a year.

Paid-in capital must consist solely of amounts invested by shareholders.

The periodicity assumption requires that present value calculations take into account the

number of compounding periods in each year.

When bonds and other debt are issued, costs such as legal costs, printing costs, and

underwriting fees are referred to as debt issuance costs (called transaction costs under

IFRS). If Brown Imports prepares its financial statements using IFRS:

a. The increase in the effective interest rate caused by the transaction costs is reflected

in the interest expense.

b. The decrease in the effective interest rate caused by the transaction costs is reflected

in the interest expense.

c. The transaction costs are recorded separately as an asset.

d. The recorded amount of the debt is increased by the transaction costs.

An investor purchases a 20-year, $1,000 par value bond that pays semiannual interest of

$40. If the semiannual market rate of interest is 5%, what is the current market value of

the bond?

a. $ 828.

b. $1,686.

c. $1,000.

d. $ 893.

LeAnn wishes to know how much she should invest now at 7% interest in order to

accumulate a sum of $5,000 in four years. She should use a table for the:

a. Present value of 1.

b. Future value of 1.

c. Present value of an ordinary annuity of 1.

d. Future value of an annuity due of 1.

The par value of common stock represents:

a. The arbitrary dollar amount assigned to a share of stock.

b. The liquidation value of a share.

c. The book value of a share of stock.

d. The amount received when the stock was issued.

Bonds were issued at a discount. In the bond amortization schedule:

a. The interest expense is less with each successive interest payment.

b. The total effective interest over the term to maturity is equal to the amount of the

discount plus the total cash interest paid.

c. The outstanding balance (book value) of the bonds declines eventually to face value.

d. The reduction in the discount is less with each successive interest payment.

The principal concern with accounting for related-party transactions is:

a. The size of the transactions.

b. Differences between economic substance and legal form.

c. The absence of legally binding contracts.

d. The lack of accurate data to record transactions.

A constraint on qualitative characteristics of accounting information is:

a. Timeliness.

b. Going concern.

c. Neutrality.

d. Cost-effectiveness.

In its 2016 income statement, WME reported $695,000 for service revenue earned from

membership fees. WME received $681,000 cash in advance from members during

2016. In its reconciliation schedule, WME should:

Each year, White Mountain Enterprises (WME) prepares a reconciliation schedule that

compares its income statement with its statement of cash flows on both the direct and

indirect method bases.

a. Show a $14,000 negative adjustment to net income under the indirect method for the

increase in unearned revenue.

b. Show a $14,000 negative adjustment to net income under the indirect method for the

decrease in unearned revenue.

c. Show a $14,000 positive adjustment to net income under the indirect method for the

increase in unearned revenue.

d. Show a $14,000 positive adjustment to net income under the indirect method for the

decrease in unearned revenue.

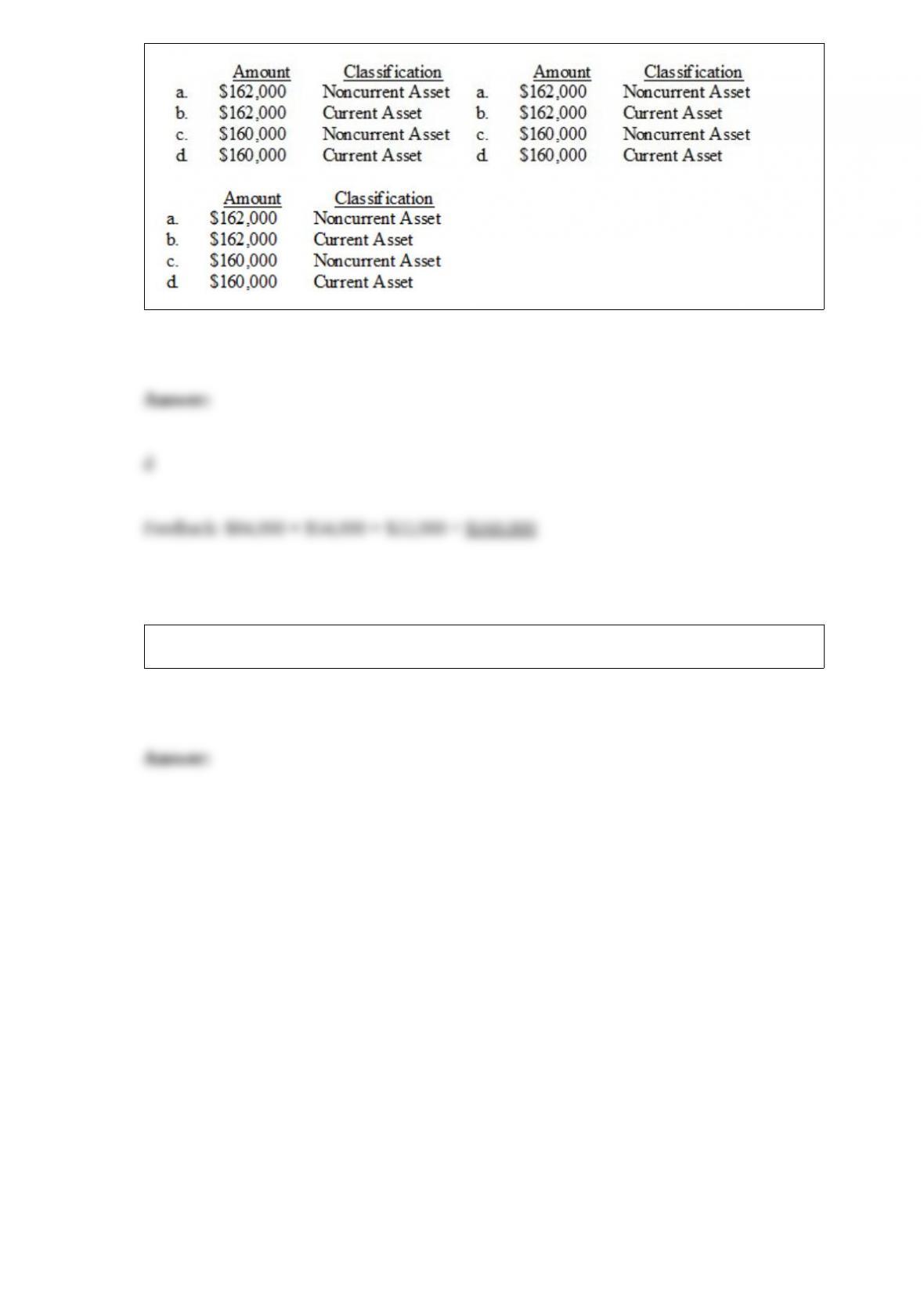

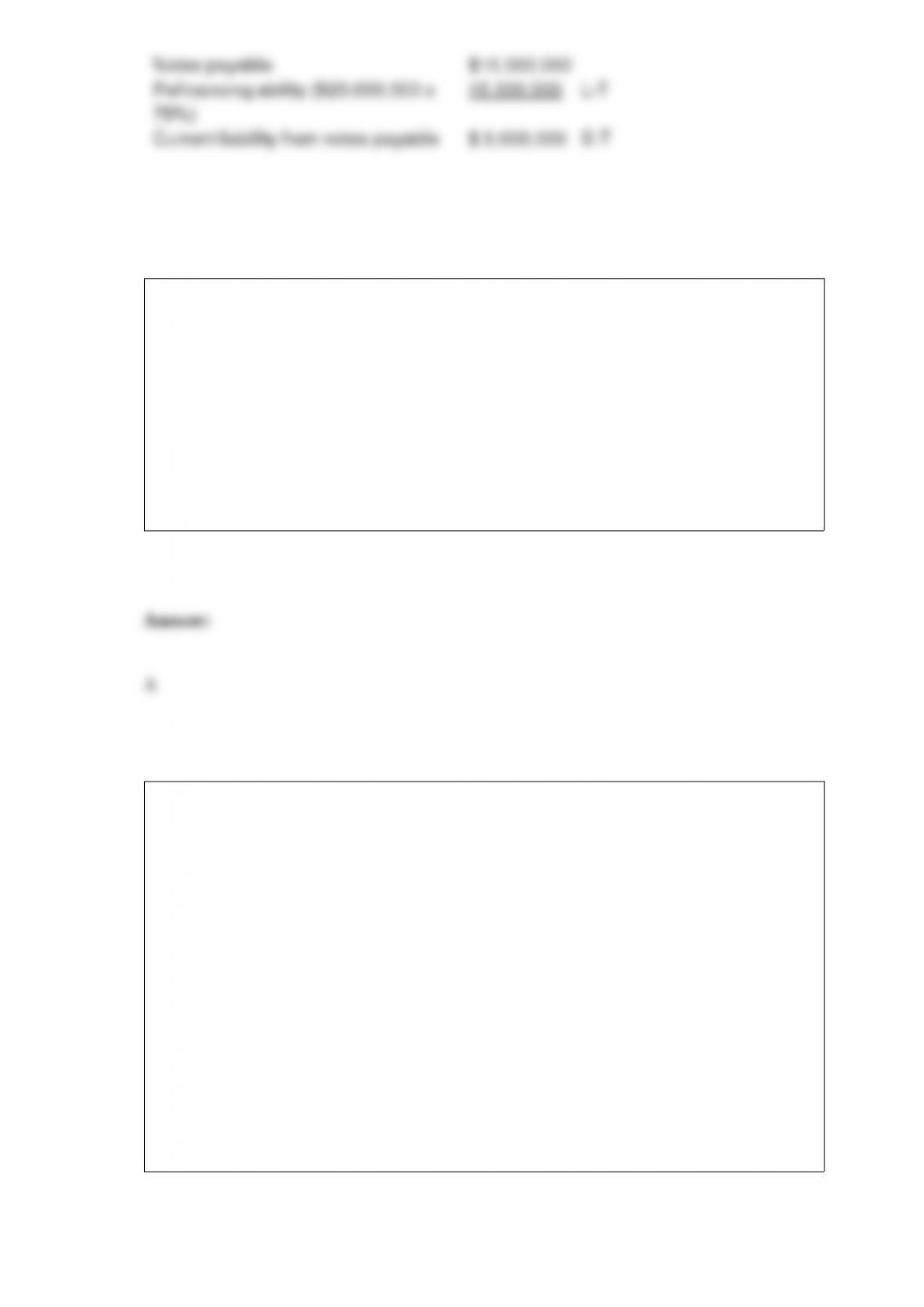

Branch Company, a building materials supplier, has $18,000,000 of notes payable due

April 12, 2017. At December 31, 2016, Branch signed an agreement with First Bank to

borrow up to $18,000,000 to refinance the notes on a long-term basis. The agreement

specified that borrowings would not exceed 75% of the value of the collateral that

Branch provided. At the date of issue of the December 31, 2016, financial statements,

the value of Branch’s collateral was $20,000,000. On its December 31, 2016, balance

sheet, Branch should classify the notes as follows:

a. $15,000,000 long-term and $3,000,000 current liabilities.

b. $4,500,000 short-term and $13,500,000 current liabilities.

c. $18,000,000 of current liabilities.

d. $18,000,000 of long-term liabilities.

Restricted stock units (RSUs):

A. are a grant valued in terms of a set number of shares of company stock.

B. are reported as a liability if payable in shares rather than cash.

C. are recorded based on a value estimated by a restricted stock valuation model.

D. represent shares issued at the date of grant that must be returned if the recipient fails

to satisfy the vesting requirement.

Listed below are 5 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the correct term. 1> Subsequent events a.

Management’s views on its operations, liquidity, and capital resources.

2> Proxy statement

3> MD&A b. Includes disclosures of executive compensation.

4> Auditors’ report c. Independent and professional opinion about the fairness of the

financial statements.

5> Summary of significant accounting policiesd. Occurs after the fiscal year-end, but

before the statements are issued.

e. Information about the company’s choices from among various alternative accounting

methods.

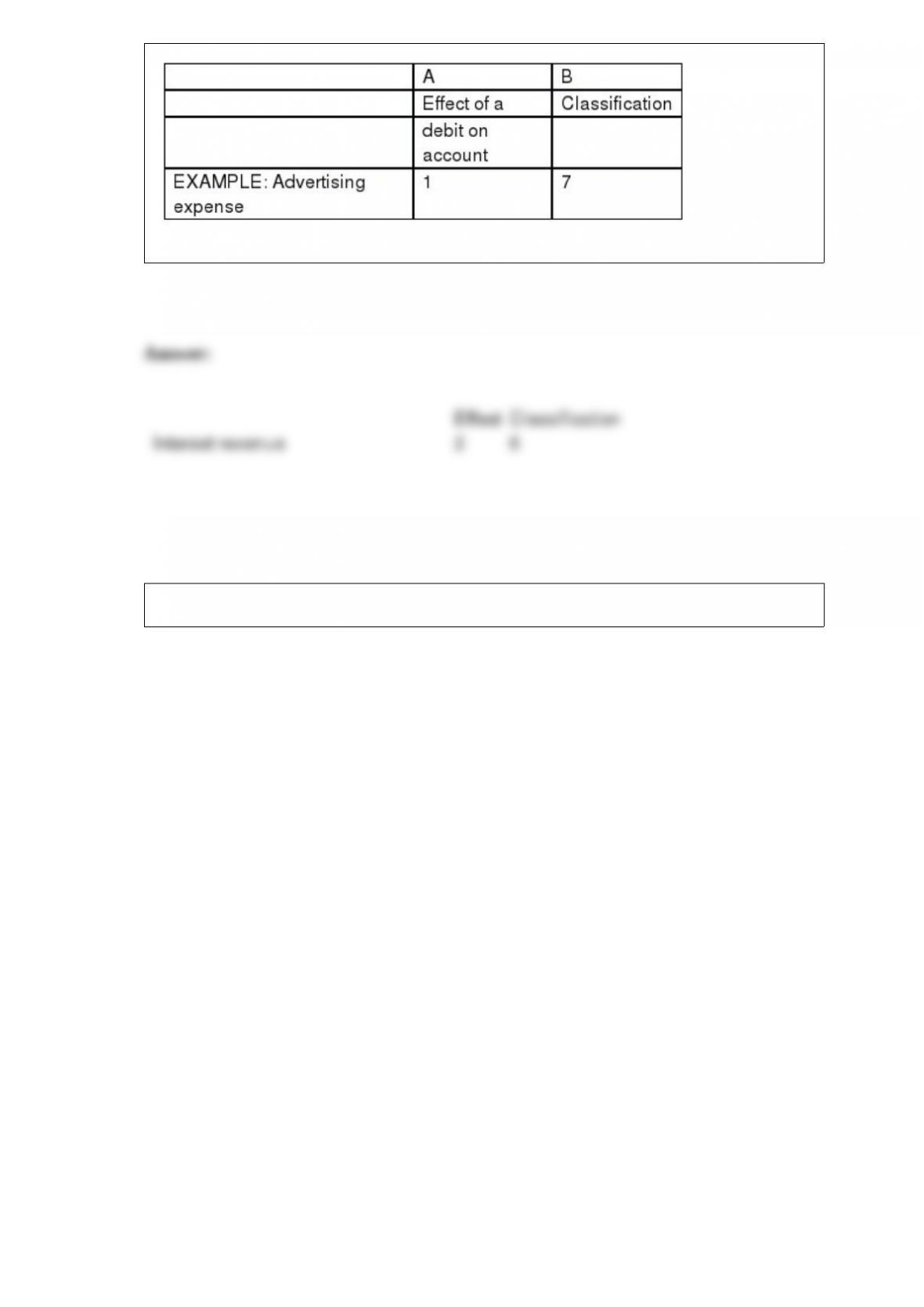

Below is a list of accounts in no particular order. Assume that all accounts have normal

balances. Required: In column A, indicate whether a debit will:

1> Increase the account balance, or

2> Decrease the account balance. In column B, classify each account according to the

following scheme. For contra accounts, indicate the classification of the account to

which it relates.

1>A current asset in the balance sheet.

2>A noncurrent asset in the balance sheet.

3>A current liability in the balance sheet.

4>A long-term liability in the balance sheet.

5>A permanent equity account in the balance sheet.

6>A revenue account in the income statement.

7>An expense account shown in the income statement.

8> Account does not appear in either the balance sheet or the income statement.

Interest revenue

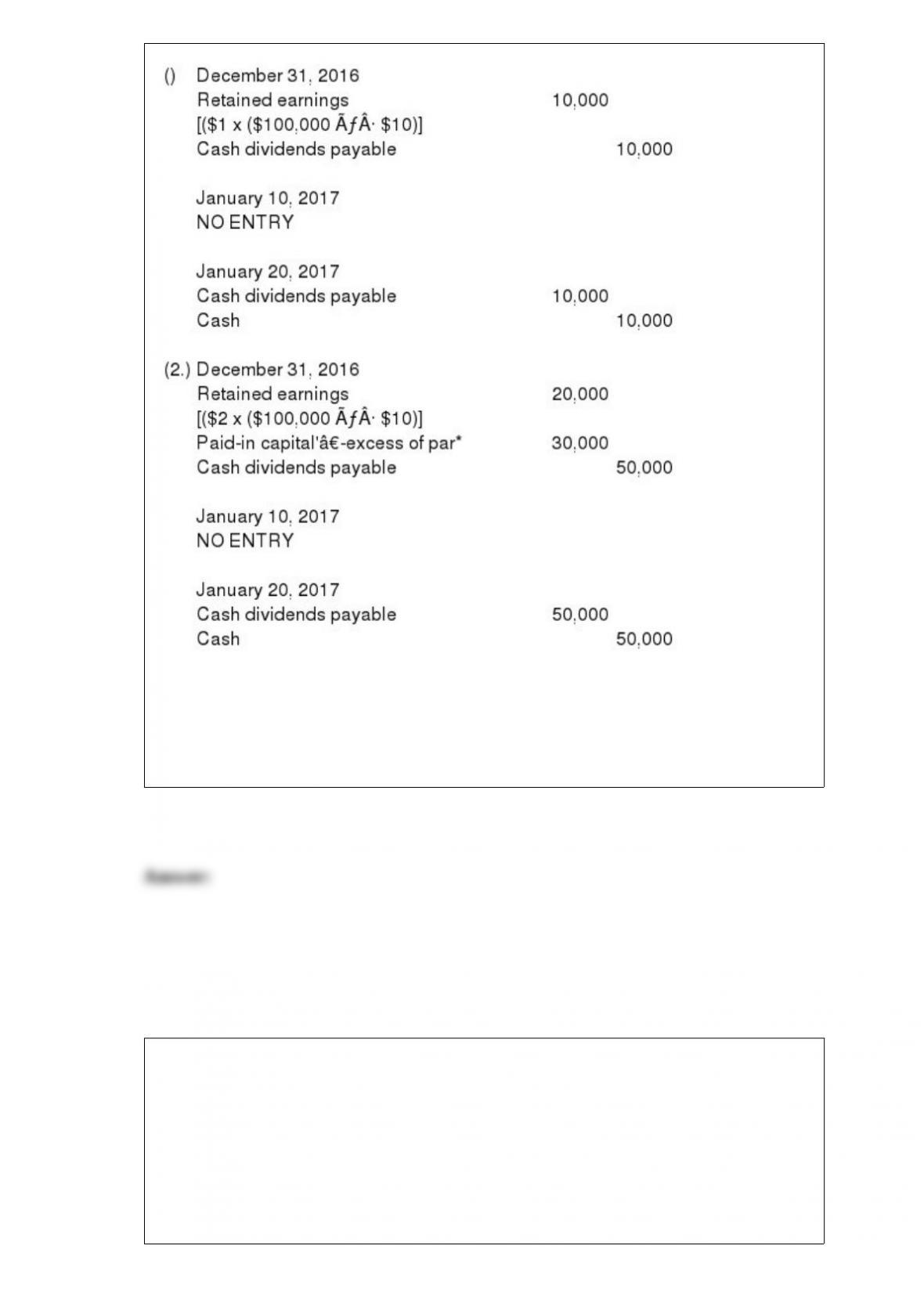

*Since the dividend exceeds the retained earnings balance, the excess is a liquidating

dividend.

Topic Area:

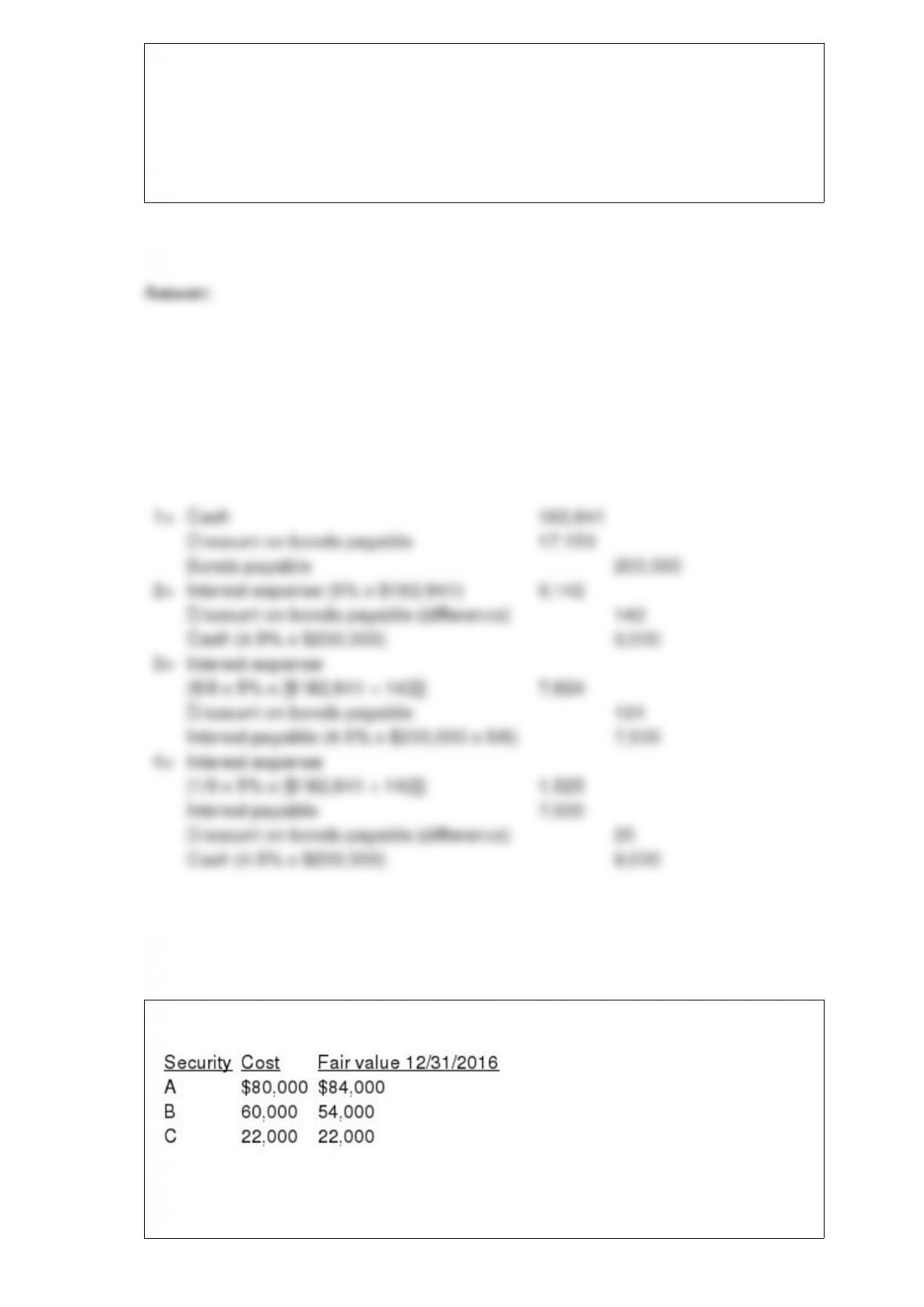

On February 1, 2016, Lagune & Sons issued 9% bonds dated February 1, 2016, with a

face amount of $200,000. The bonds sold for $182,841 and mature in 20 years. The

effective interest rate for these bonds was 10%. Interest is paid semiannually on July 31

and January 31. Lagune’s fiscal year is the calendar year.

Required:

1> Prepare the journal entry to record the bond issuance on February 1, 2016.

2> Prepare the entry to record interest on July 31, 2016, using the effective interest

method.

3> Prepare the necessary journal entry on December 31, 2016.

4> Prepare the necessary journal entry on January 31, 2017.

Anthers Inc. bought the following portfolio of trading securities near the end of 2016.

What amount will be reported in the balance sheet for this portfolio at December 31,

2016, and how will it be classified?