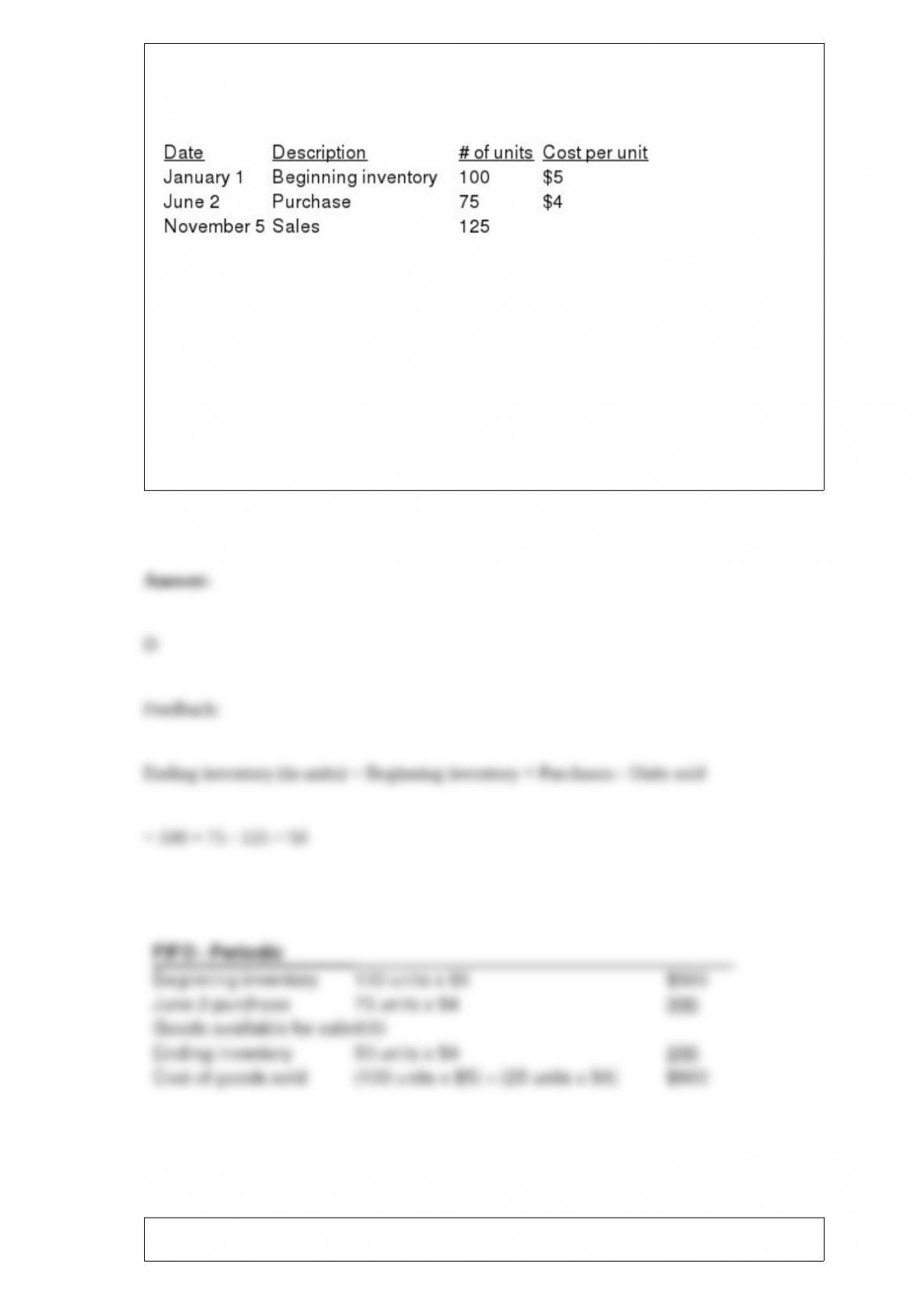

Maxell Company uses the FIFO method to assign costs to inventory and cost of goods

sold. The company uses a periodic inventory system. Consider the following

information:

What amounts would be reported as the cost of goods sold and ending inventory

balances for the year?

A) Cost of goods sold $625; Ending inventory $175

B) Cost of goods sold $755; Ending inventory $225

C) Cost of goods sold $550; Ending inventory $250

D) Cost of goods sold $600; Ending inventory $200

Lucia Inc. uses a perpetual inventory system. The company has a beginning inventory

of 400 units at $70 per unit. The company purchases 1,000 units in August at $72 each

and 600 units in November at $75 each. The company sells 1,000 units in September

and 900 units in December.

Required:

Calculate the company’s ending inventory and cost of goods sold using the each of

following inventory costing methods. (Round the per unit cost to two decimal places

and then round your answer to the nearest whole dollar.)

Part a. FIFO

Part b. LIFO

Part c. Weighted Average

Sales tax collected by a company is normally reported as:

A) a current liability.

B) income tax expense.

C) an asset.

D) an operating expense.

Which of the following statements about adjustments is not correct?

A) Adjusting entries affect the cash account.

B) Adjustments to prepaid expenses and unearned revenues are deferral adjustments.

C) Adjustments for wages and income taxes are normally accrual adjustments. .

D) Adjusting entries involve one income statement account and one balance sheet

account.

Which of the following statements correctly describes an imprest system?

A) An imprest system is an internal control procedure relating to cash receipts.

B) There is no difference between a petty cash fund and an imprest bank account.

C) If the transfers from the payroll account to the employees ‘ checking accounts occur

without error, the imprest payroll bank account will equal zero after all employees have

been paid.

D) The use of an imprest system eliminates the need for bank reconciliations.

On December 16, 2015, B. Darin Company received $3,600 from S. Dee Company for

rent of an office owned by B. Darin Company. The payment covers the period from

December 16, 2015 through February 15, 2016. B. Darin Company recorded this as

Unearned Rent when it was received on December 16. The adjusting entry on

December 31 would include a:

A) credit to Rent Revenue of $900.

B) credit to Unearned Rent Revenue of $900.

C) debit to Rent Revenue of $1,800.

D) debit to Unearned Rent Revenue of $1,800.

A retailer using a periodic inventory system returned $3,000 of defective inventory

which was purchased on account from one of its wholesale suppliers. The entry to

record this transaction on the retailer’s books would include a debit to:

A) Accounts Receivable.

B) Cost of Goods Sold.

C) Accounts Payable.

D) Inventory.

The perpetual inventory method of tracking inventory is considered superior to the

periodic method because the perpetual method:

A) makes calculations easier and less technology can be deployed.

B) tells what inventory a company should have at any point in time.

C) saves a company from ever having to count the goods in inventory.

D) is more consistent with how companies calculated inventory in the past.

Flynn Company ‘s monthly bank statement showed the ending balance of cash of

$18,500. The bank reconciliation for the period showed an adjustment for a deposit in

transit of $1,500, outstanding checks of $2,000, a NSF check of $700, bank service

charges of $30 and the EFT from a customer in payment of the customer ‘s account of

$1,500.

Use the information above to answer the following question. What journal entry should

be recorded by Flynn Company for the NSF check returned?

A). Debit Accounts Receivable and credit Cash for $700

B). Debit Cash and credit Accounts Receivable for $700

C) Debit Cash and credit Accounts Payable for $700

D) No journal entry is necessary for this item.

Which number is potentially the largest?

A) The number of shares authorized.

B) The number of shares issued.

C) The number of shares outstanding.

D) The number of shares certified.

Cash equivalents would include:

A) a 30-day bank certificate of deposit.

B) the amount in the petty cash fund.

C) a 6-month U.S. treasury bill.

D) the balance in the company ‘s savings account.