A corporation does not have a legal obligation to pay dividends.

Sales discounts are discounts that consumers get from buying clearance items at a

reduced price.

Every transaction increases at least one account and decreases at least one account.

A merchandising company’s operating cycle begins with the sale of inventory and ends

with the cash collection from sales.

Stockholders’ equity is the difference between a company’s assets and its liabilities.

If cost of goods sold remains unchanged, an increase in the inventory turnover ratio is

indicative of a(n):

A) reduction in the cost of goods sold.

B) decrease in inventory.

C) increase in inventory.

D) increase in sales revenue.

To calculate the company’s income tax expense for the current period, it is necessary to

know the company’s:

A) operating revenue and tax bill from prior periods.

B) adjusted income (before income taxes) and the company’s tax rate.

C) operating expenses and revenue.

D) revenues, expenses, and dividends.

A system used to reimburse employees for expenditures they have made on behalf of

the organization is referred to as a:

A) electronic funds transfer.

B) voucher system.

C) petty cash system.

D) internal control system.

A company has earnings per share of $1.20, it paid a dividend of $.50 per share, and the

market price of the company’s stock is $45 per share. The price/earnings ratio is closest

to:

A) 37.50.

B) 64.29.

C) 2.40.

D) 2.0.

Which of the following would generally be considered an operating revenue or

expense?

A) Income from renting out extra warehouse space

B) Interest on a note payable

C) Dividends earned on an investment is another company’s stock

D) Depreciation

During April, the Grass is Greener Company buys and pays for a six-month supply of

fertilizer in order to receive a bulk discount. The company uses accrual basis

accounting. The cost of fertilizer recorded:

A) immediately as an expense.

B) as a liability, which will later be reduced as the fertilizer used.

C) partially as an expense and partially as a liability.

D) as an asset, which will later be reduced as the fertilizer is used.

Which of the following statements regarding sales returns and allowances is correct?

A) Recording sales returns and allowances in a separate account is an important internal

control that allows management to evaluate the volume of returns and allowances as a

potential indicator of the quality of their products.

B) The Sales Returns & Allowances account balance should be added to the Sales

account balance when computing net sales.

C) The Sales Returns & Allowances account is an example of a contra-asset account.

D) Recording a sales allowance requires two entries.

A company that uses the allowance method to account for its bad debts had credit sales

of $740,000 in 2015, including a $720 sale to Arbor Corporation. On December 31,

2015, the company estimated its bad debts at 1.5% of its credit sales. On June 1, 2016,

the company wrote off as uncollectible the $720 account of Arbor Corporation; and on

December 21, 2016, Arbor Corporation unexpectedly paid her account in full.

Required:

Prepare the necessary journal entries dated: (a) on December 31, 2015, to reflect the

estimate of Bad Debt Expense; (b) on June 1, 2016, to write off the bad debt; and (c) on

December 21, 2016, to record the unexpected collection.

Friedman Company uses the aging of accounts receivable method. Its estimate of

uncollectible receivables resulting from the aging analysis equals $25,000. The

unadjusted credit balance in the Allowance for Doubtful Accounts account is $8,000.

What is the estimated Bad Debt Expense for the period?

A) $8,000

B) $17,000

C) $25,000

D) $33,000

Consider the formula used to calculate each of the following financial performance

ratios. From the list of financial statement items below, match its letter with the ratio it

is used to calculate. Some financial statement items will be used more than once. Some

ratios will use one letter from the list and some ratios will use two letters from the list.

Ratio

1> ___ Net Profit Margin

2> ___ Debt-to-assets ratio

3> ___ EPS

4> ___ ROE

5> ___ Days to collect

6> ___ Days to sell

7> ___ Price earnings ratio

8> ___ Current ratio

9> ___ Fixed asset turnover

10> ___ Gross profit percentage

11> ___ Quick ratio

Financial Statement Item

A) Net income

B) Interest paid

C) Cost of goods sold

D) Net sales revenue

E) Total liabilities

F) Total assets at year end

G) Average stockholders’ equity

H) Current liabilities

The Don’t Tread on Me Tire Company had Retained Earnings at December 31, 2015 of

$200,000. During 2016, the company had revenues of $400,000 and expenses of

$350,000, and the company declared and paid dividends of $11,000. Retained earnings

on the balance sheet as of December 31, 2016 will be:

A) $39,000.

B) $239,000.

C) $250,000.

D) $289,000.

On October 10, a company paid $12,000 to a supplier. Of that amount, $2,000 was for

supplies received on October 10 and $10,000 was for supplies that were purchased on

account during September. The journal entry to record the $12,000 payment would

include a debit to:

A) Supplies for $10,000, a debit to Accounts Payable for $2,000, and a credit to Cash

for $12,000.

B) Supplies and a credit to Cash for $12,000.

C) Supplies Expense and a credit to Cash for $12,000.

D) Supplies for $2,000, a debit to Accounts Payable for $10,000, and a credit to Cash

for $12,000.

The following activities took place during the month of November at a corporation that

operates a shoe repair shop.

1> Salaries and wages in the amount of $33,000 are paid to employees.

2> On the last day of November, the company acquires equipment on account of

$55,000.

3> Payment of $375 made on account to a consulting firm for services received from

that firm during October.

4> Payment of $12,000 made at the beginning of November for six months of rent; the

period covered by the payment begins in November.

5> Utility bills in the amount of $125 arrive in the mail; the bills will not be paid until

December.

Required:

Indicate what accounts would be used to record the initial transaction arising from each

activity.

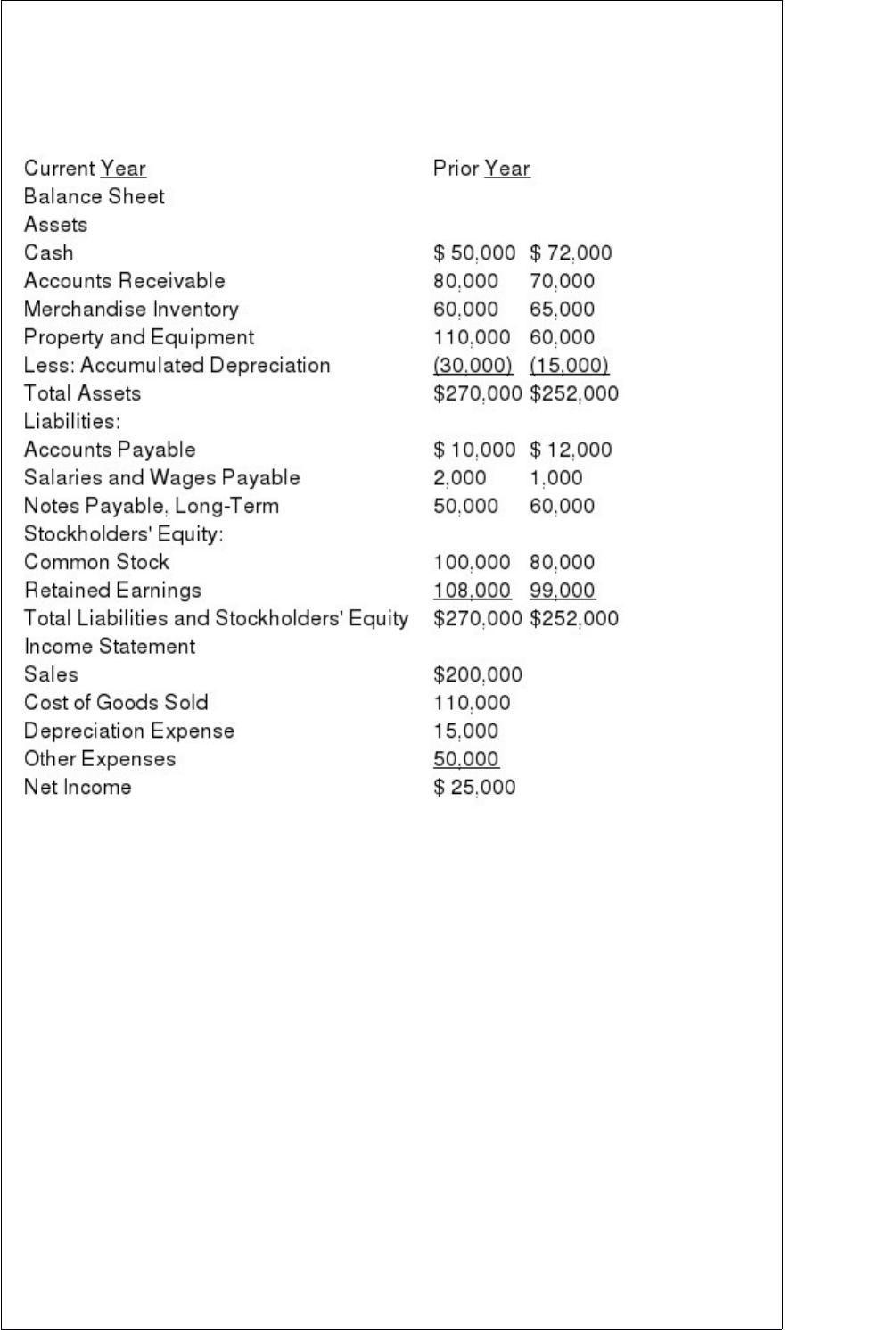

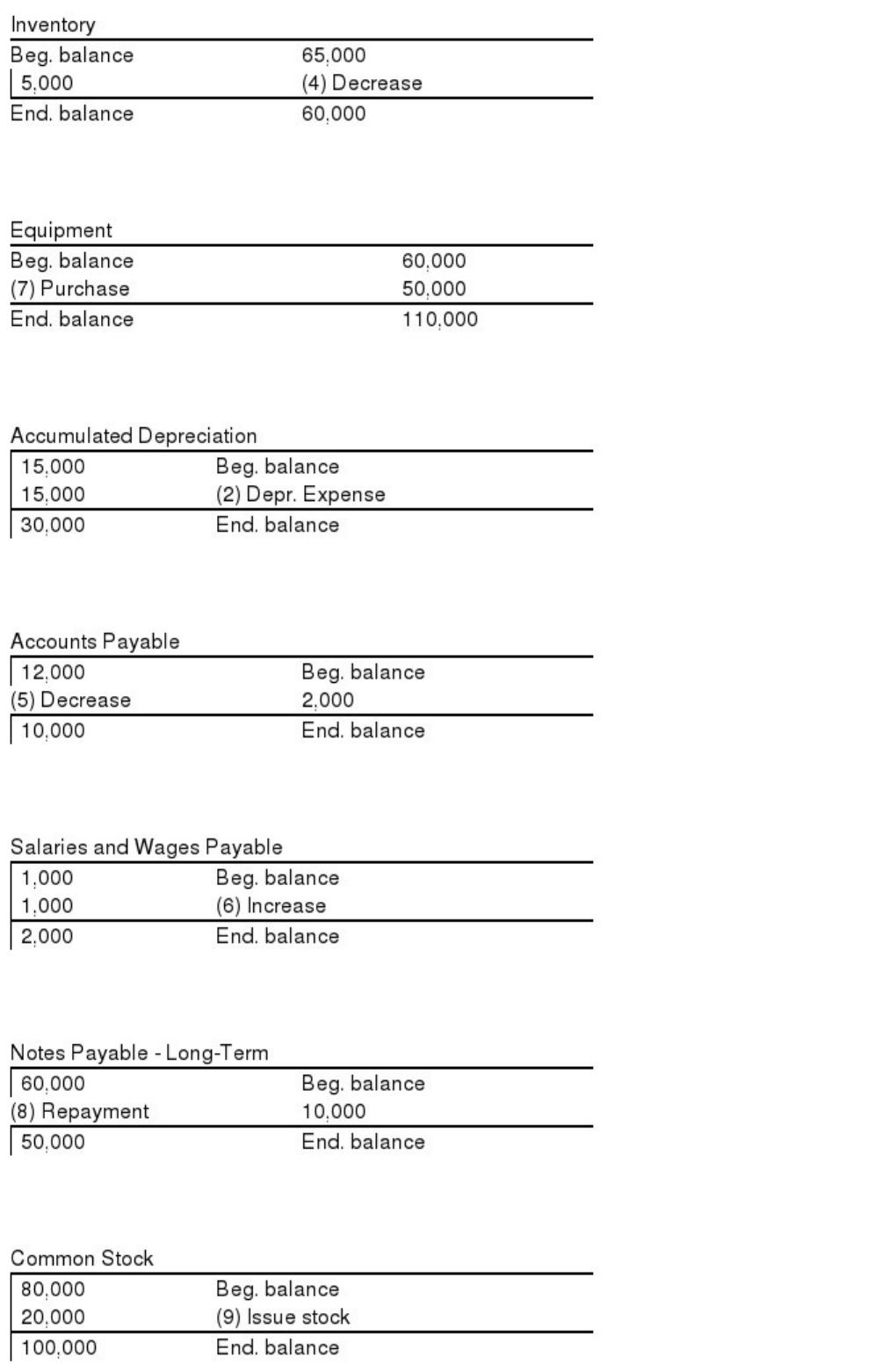

The management team of Wickersham Brothers Inc. is preparing its annual financial

statements. The statements are complete except for the statement of cash flows. The

completed comparative balance sheets and income statements are summarized.

Other information from the company’s records includes the following:

Bought equipment for cash, $50,000.

Paid $10,000 on long-term note payable.

Issued new shares of common stock for $20,000 cash.

Cash dividends of $16,000 were declared and paid to stockholders.

Accounts Payable arose from inventory purchases on credit.

Income Tax Expense ($4,000) and Interest Expense ($3,000) were paid in full at the end

of both years and are included in Other Expenses.

Required:

Prepare a schedule summarizing operating, investing, and financing cash flows using

the T-account approach

Listed below are components of several transactions. In the blank to the left indicate

whether a debit (dr) or credit (cr) would be required to record the component of the

transaction.

_____ (1) Increase in Cash.

_____ (2) Increase in Accounts Payable.

_____ (3) Decrease in Notes Payable.

_____ (4) Increase in Inventory.

_____ (5) Increase in Common Stock.

_____ (6) Decrease in Equipment.

A company had calculated net income to be $77,550 based on the unadjusted trial

balance. The following adjusting entries were then made for:

Salaries and wages owed but not yet paid of $790

Interest earned but not received from investments of $750

Prepaid insurance premiums amounting to $550 have expired

Unearned revenue in the amount of $750 has now been earned.

Required:

Determine the amount of net income (loss) that will be reported after the adjustments

are recorded.

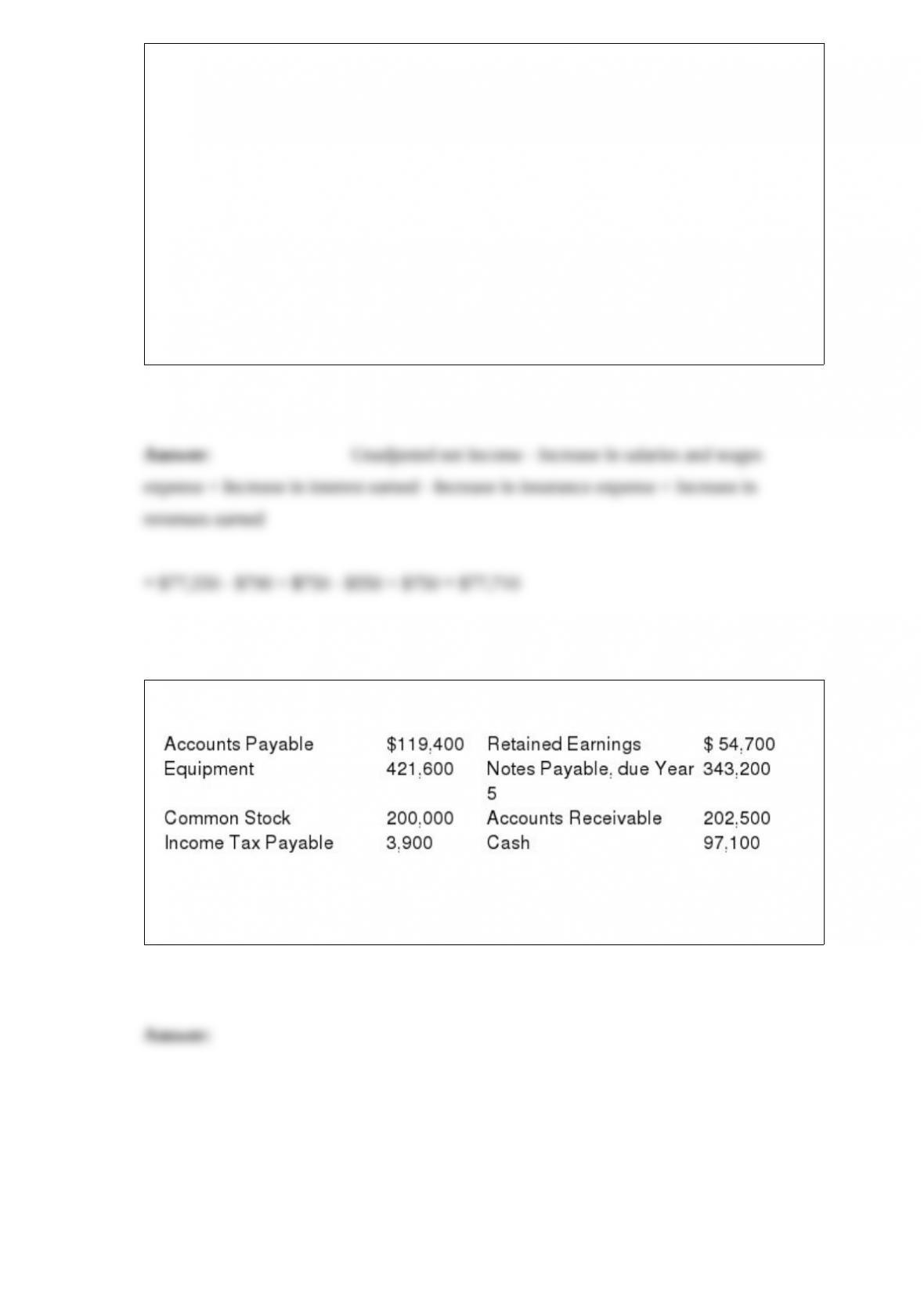

Consider the following account balances of Purrfect Pets, Inc., as of June 30, Year 3:

Required:

Prepare a classified balance sheet at June 30, Year 3.

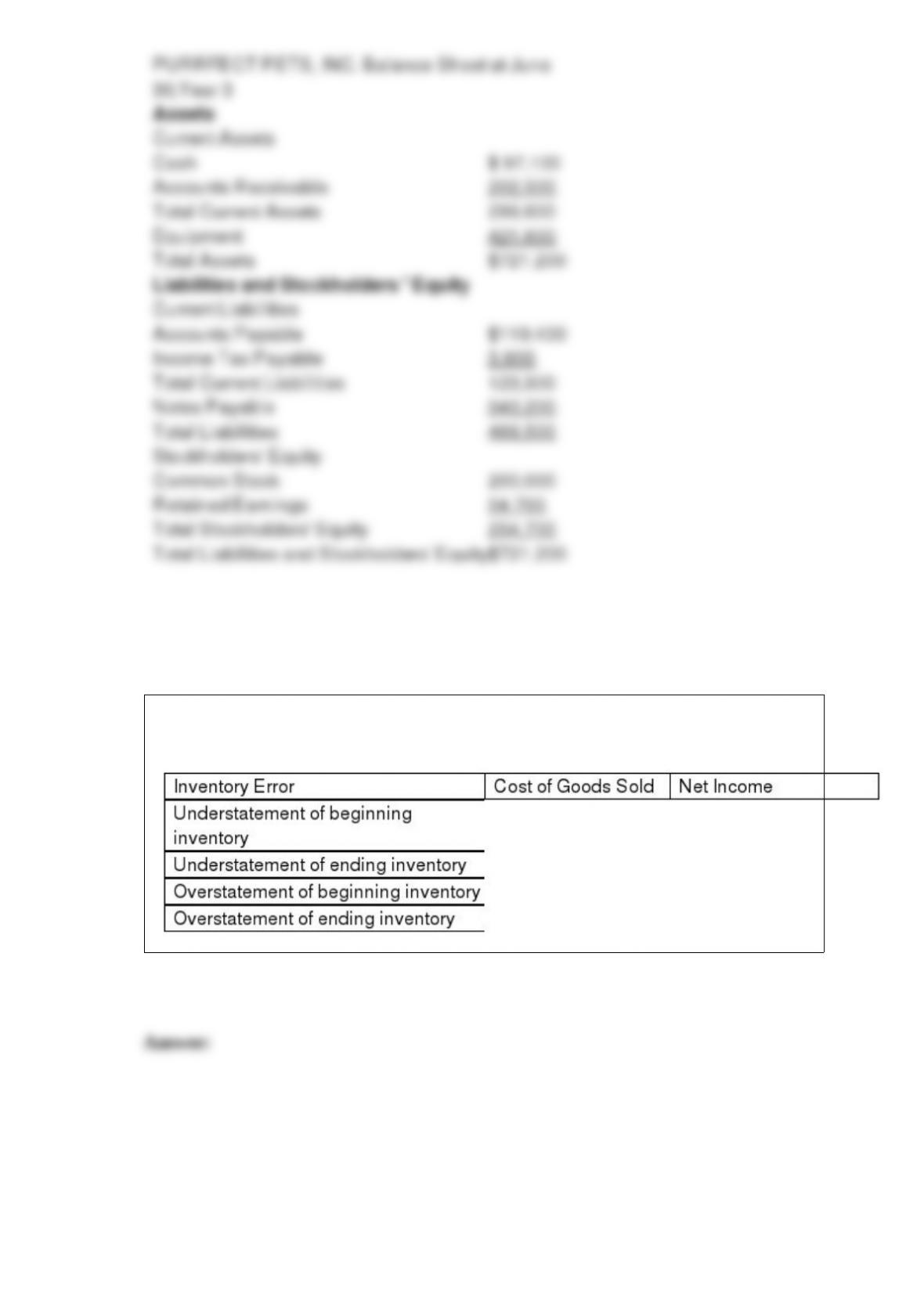

Evaluate each inventory error separately and determine whether it overstates or

understates cost of goods sold and net income.

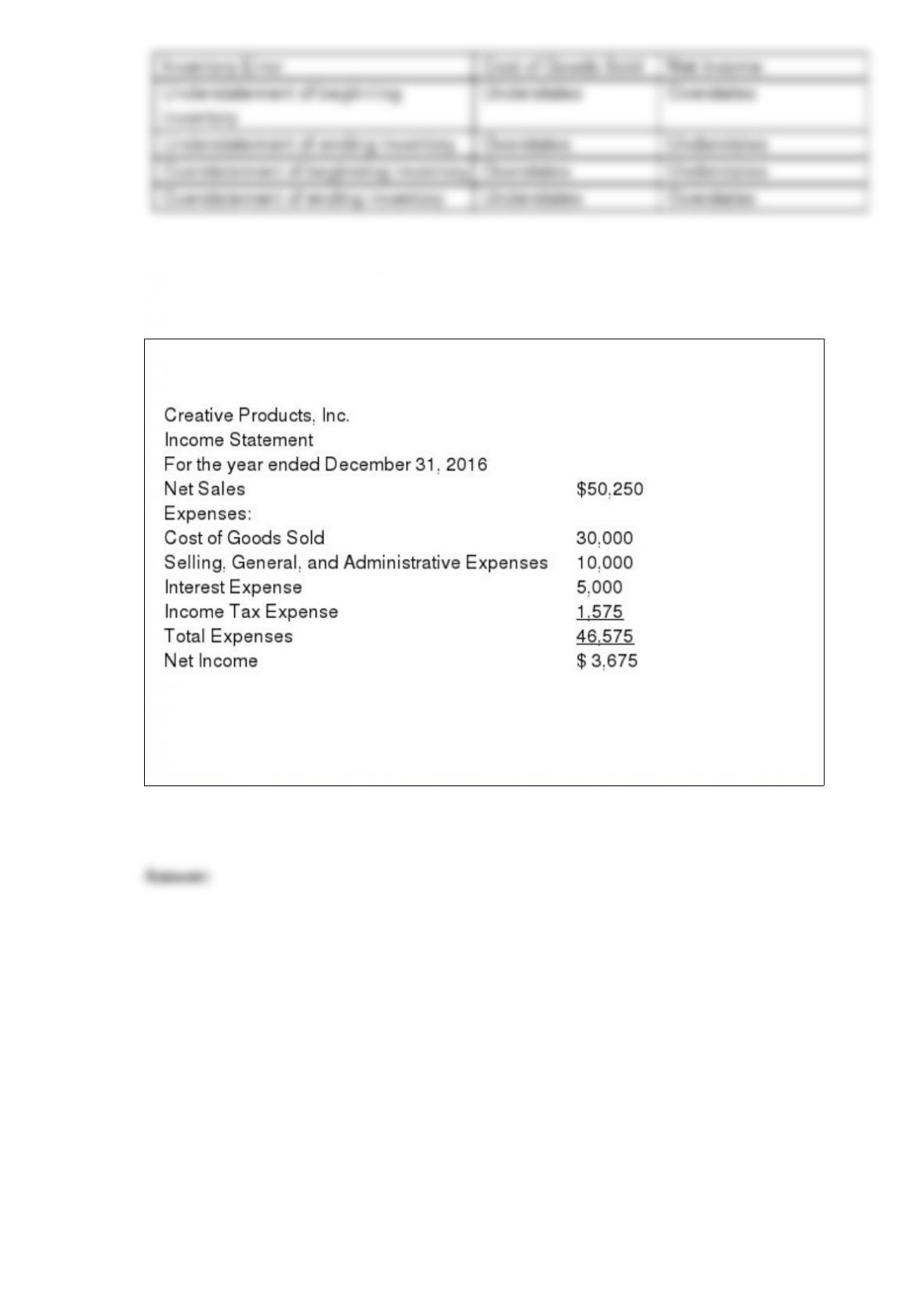

Consider the following single-step income statement.

Required:

Prepare a multistep income statement for Creative Tax Service for the year ended

December 31, 2016.

Pinkney Company updates its inventory periodically. The company ‘s beginning

inventory was $5,000 and purchases were $10,600 during the year. The company ‘s

ending inventory count was $7,000.

Required:

Determine the amount of cost of goods sold for the year.