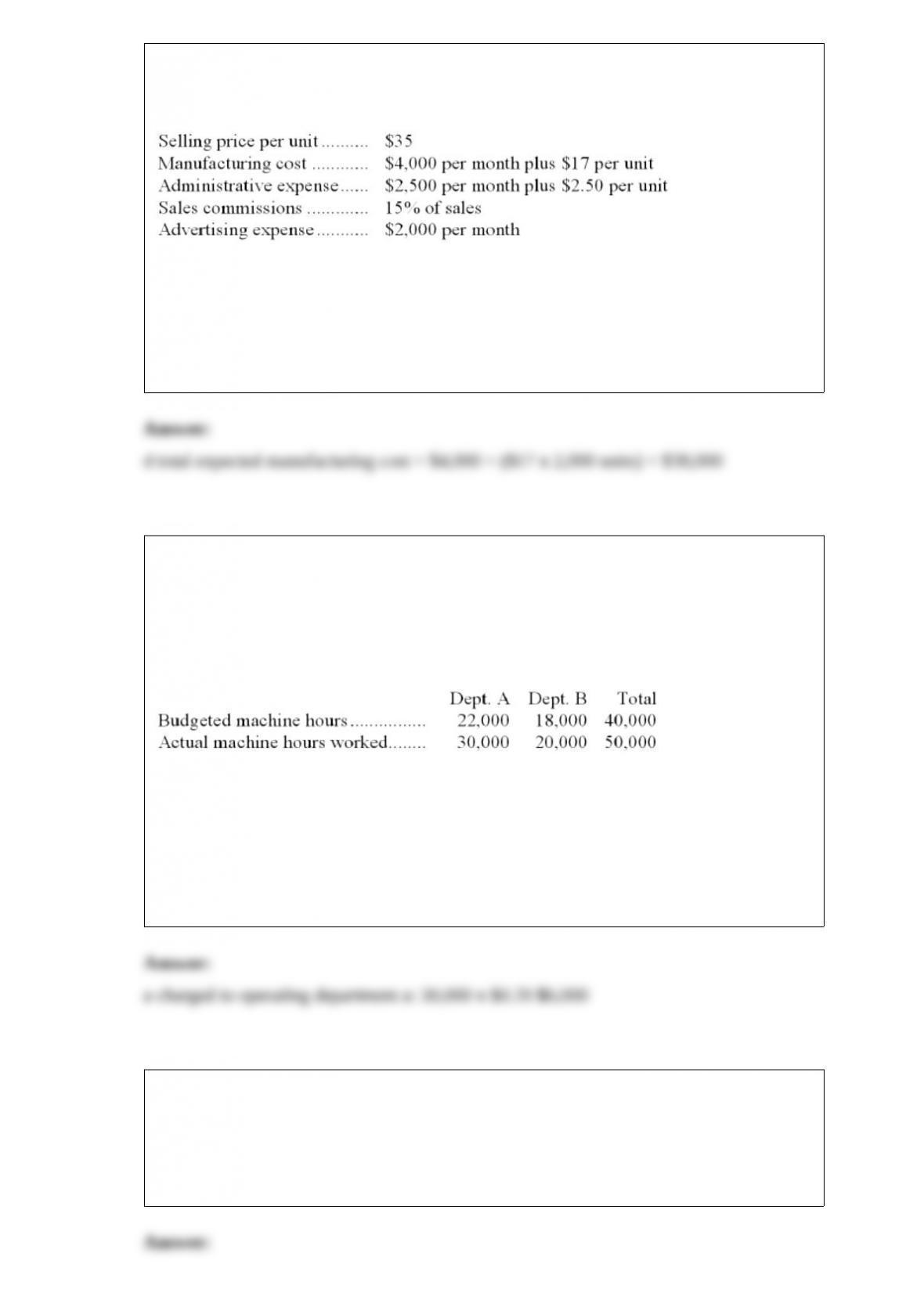

1) buffo company fabricates metal folding chairs. data concerning the company’s

revenue and cost structure follow:

if buffo expects to produce and sell 2,000 units next month, the total expected

manufacturing cost would be:

a.$34,000

b.$39,000

c.$45,500

d.$38,000

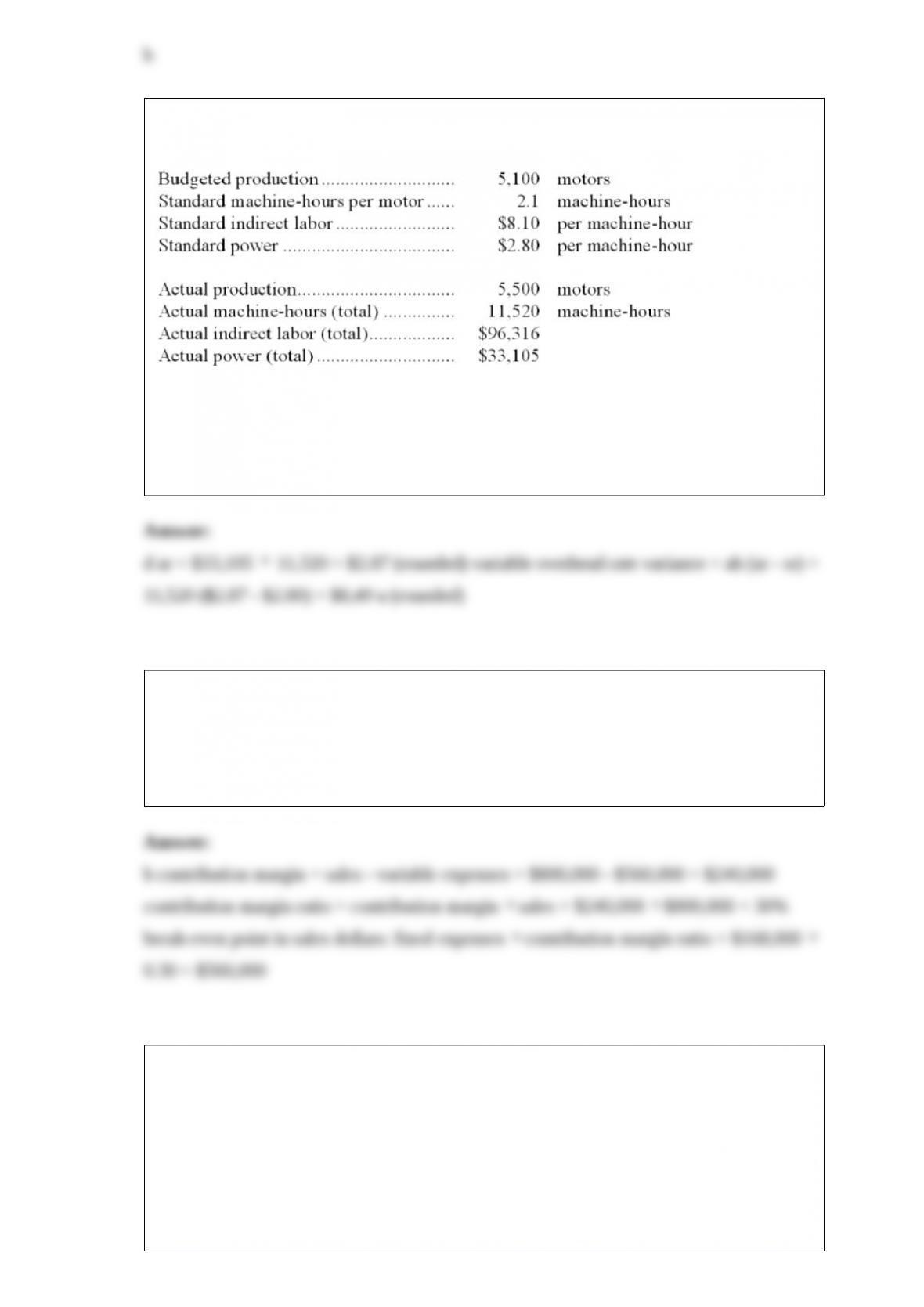

2) swift company has a maintenance department that does maintenance work on all

equipment in operating departments a and b. the maintenance department budgeted

variable maintenance costs of $0.20 per machine hour for june. actual variable

maintenance costs for the month totaled $15,000. budgeted and actual machine hours in

the operating departments for the month were:

how much variable maintenance cost for the month should be charged to department a

at the end of the month for performance evaluation purposes?

a.$6,000

b.$15,000

c.$8,250

d.$9,000

3) a flexible budget is a budget that:

a.is updated with actual costs as they occur during the period

b.is updated to reflect the actual level of activity during the period

c.is prepared using a computer spreadsheet application

d.contains only variable production costs

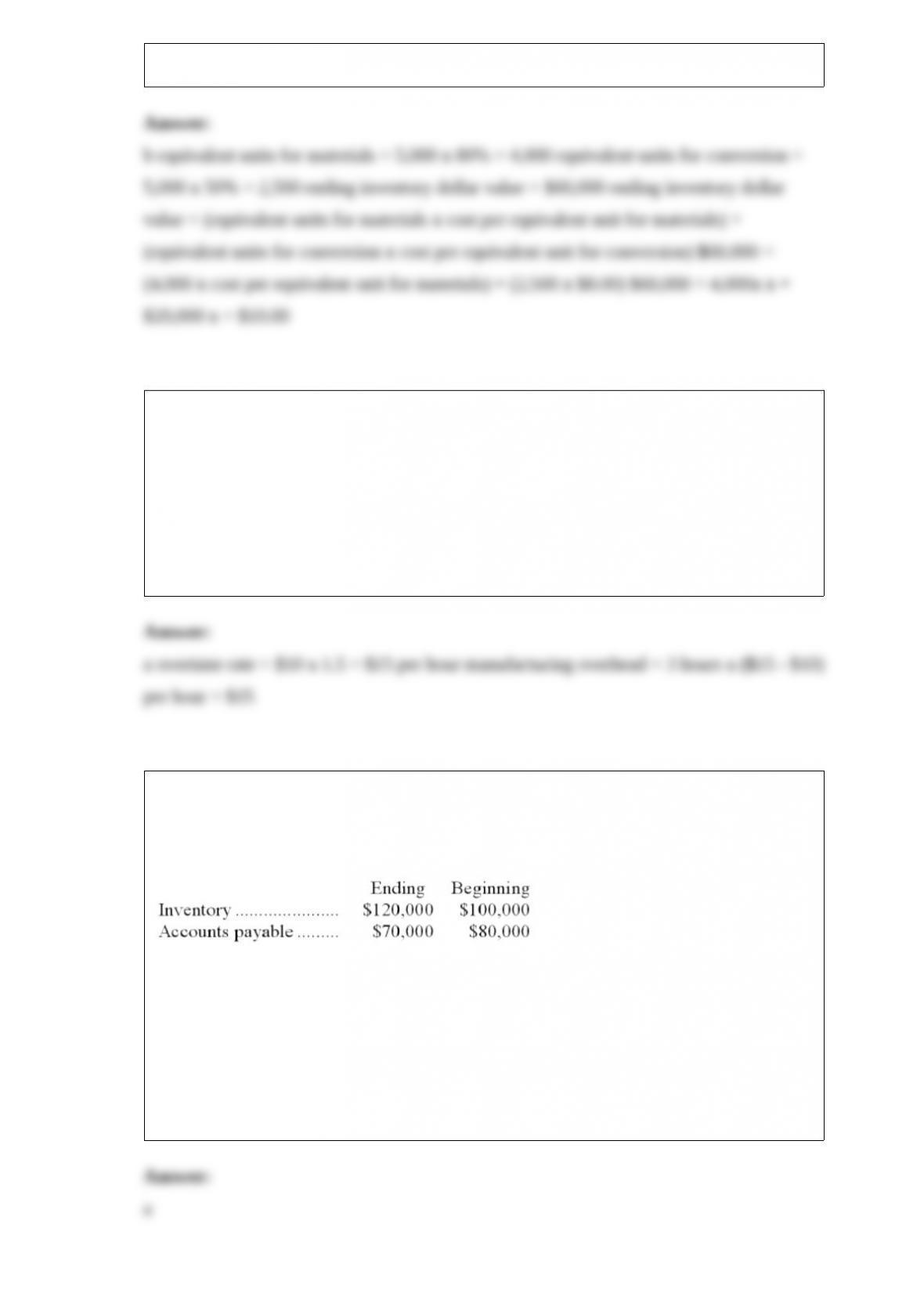

4) the following data have been provided by wordell corporation:

the variable overhead rate variance for power is closest to:

a.$84 f

b.$765 u

c.$765 f

d.$849 u

5) the break-even point in sales dollars is:

a.$240,000

b.$560,000

c.$728,000

d.$408,000

6) black company uses the weighted-average method in its process costing system. the

company’s ending work in process inventory consists of 5,000 units, 80% complete

with respect to materials and 50% complete with respect to labor and overhead. if the

total dollar value of the inventory is $60,000 and the cost per equivalent unit for labor

and overhead is $8.00, the cost per equivalent unit for materials must be:

a.$5.00

b.$10.00

c.$8.00

d.$4.00

7) bill harris works on the assembly line of the boothe company and earns $10 per hour.

he is paid time-and-a-half for work in excess of 40 hours per week. during a given week

he worked 43 hours and had no idle time. how much of his week’s wages would be

charged to manufacturing overhead?

a.$15

b.$45

c.$30

d.$0

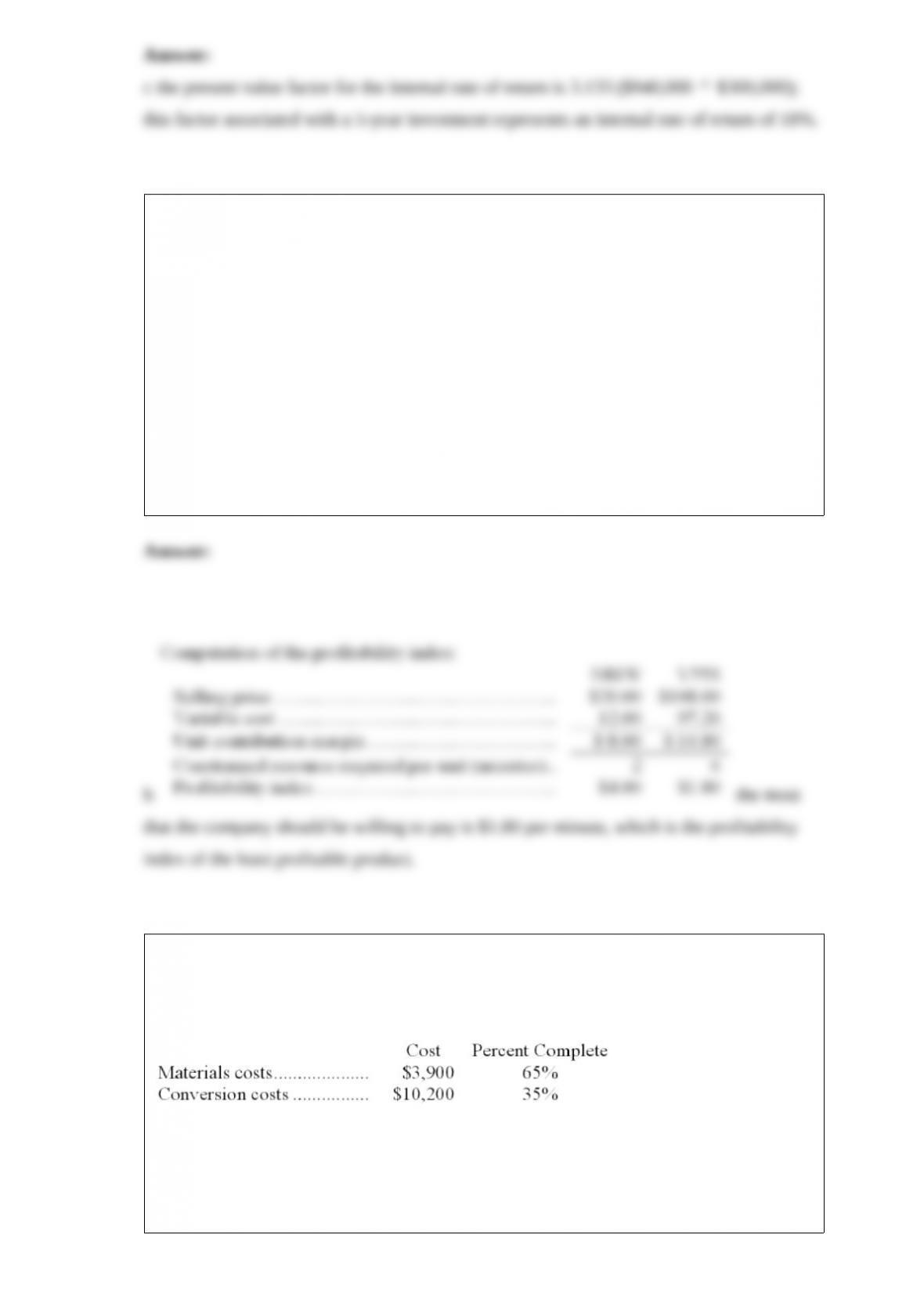

8) last year madson company reported a cost of goods sold of $800,000 on its income

statement. the following additional data were taken from the company’s comparative

balance sheet for the year:

the company uses the direct method to determine the net cash provided by operating

activities on the statement of cash flows. the cost of goods sold adjusted to a cash basis

would be:

a.$830,000

b.$810,000

c.$770,000

d.$790,000

9) the management of pundt corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. the company’s controller

has provided an example to illustrate how this new system would work. in this example,

the allocation base is machine-hours and the estimated amount of the allocation base for

the upcoming year is 15,000 machine-hours. in addition, capacity is 19,000

machine-hours and the actual level of activity for the year is 15,100 machine-hours. all

of the manufacturing overhead is fixed and is $45,600 per year. for simplicity, it is

assumed that this is the estimated manufacturing overhead for the year as well as the

manufacturing overhead at capacity. it is further assumed that this is also the actual

amount of manufacturing overhead for the year. a number of jobs were worked on

during the year, one of which was job k41p. this job required 140 machine-hours.

if the company bases its predetermined overhead rate on capacity, the amount of

manufacturing overhead charged to the job k41p is closest to:

a.$336.00

b.$422.78

c.$389.27

d.$399.00

10) (ignore income taxes in this problem.) treads corporation is considering the

replacement of an old machine that is currently being used. the old machine is fully

depreciated but can be used by the corporation for five more years. if treads decides to

replace the old machine, picco company has offered to purchase the old machine for

$60,000. the old machine would have no salvage value in five years.

the new machine would be acquired from hillcrest industries for $1,000,000 in cash. the

new machine has an expected useful life of five years with no salvage value. due to the

increased efficiency of the new machine, estimated annual cash savings of $300,000

would be generated.

treads corporation uses a discount rate of 12%.

the internal rate of return of the project is closest to:

a.14%

b.16%

c.18%

d.20%

11) blomstrom products inc. makes two productsn81w and v55s. product n81w’s selling

price is $20.00 and its unit variable cost is $12.00. product v55s’s selling price is

$108.00 and its unit variable cost is $97.20. the monthly demand is 3,940 units for

product n81w and 1,140 units for v55s. the constrained resource is a particular machine

that is available for 10,400 minutes each month. each unit of product n81w requires 2

minutes on this machine and each unit of product v55s requires 6 minutes on this

machine.

up to how much should the company be willing to pay to obtain enough of the

constrained resource to satisfy demand for the two existing products?

a.$4.00 per minute

b.$1.80 per minute

c.$8.00 per minute

d.$10.80 per minute

12) ermoin corporation uses the weighted-average method in its process costing system.

this month, the beginning inventory in the first processing department consisted of 600

units. the costs and percentage completion of these units in beginning inventory were:

a total of 5,700 units were started and 4,700 units were transferred to the second

processing department during the month. the following costs were incurred in the first

processing department during the month:

the ending inventory was 75% complete with respect to materials and 20% complete

with respect to conversion costs.

note: your answers may differ from those offered below due to rounding error. in all

cases, select the answer that is the closest to the answer you computed. to reduce

rounding error, carry out all computations to at least three decimal places

what are the equivalent units for conversion costs for the month in the first processing

department?

a.5,020

b.6,300

c.4,700

d.320

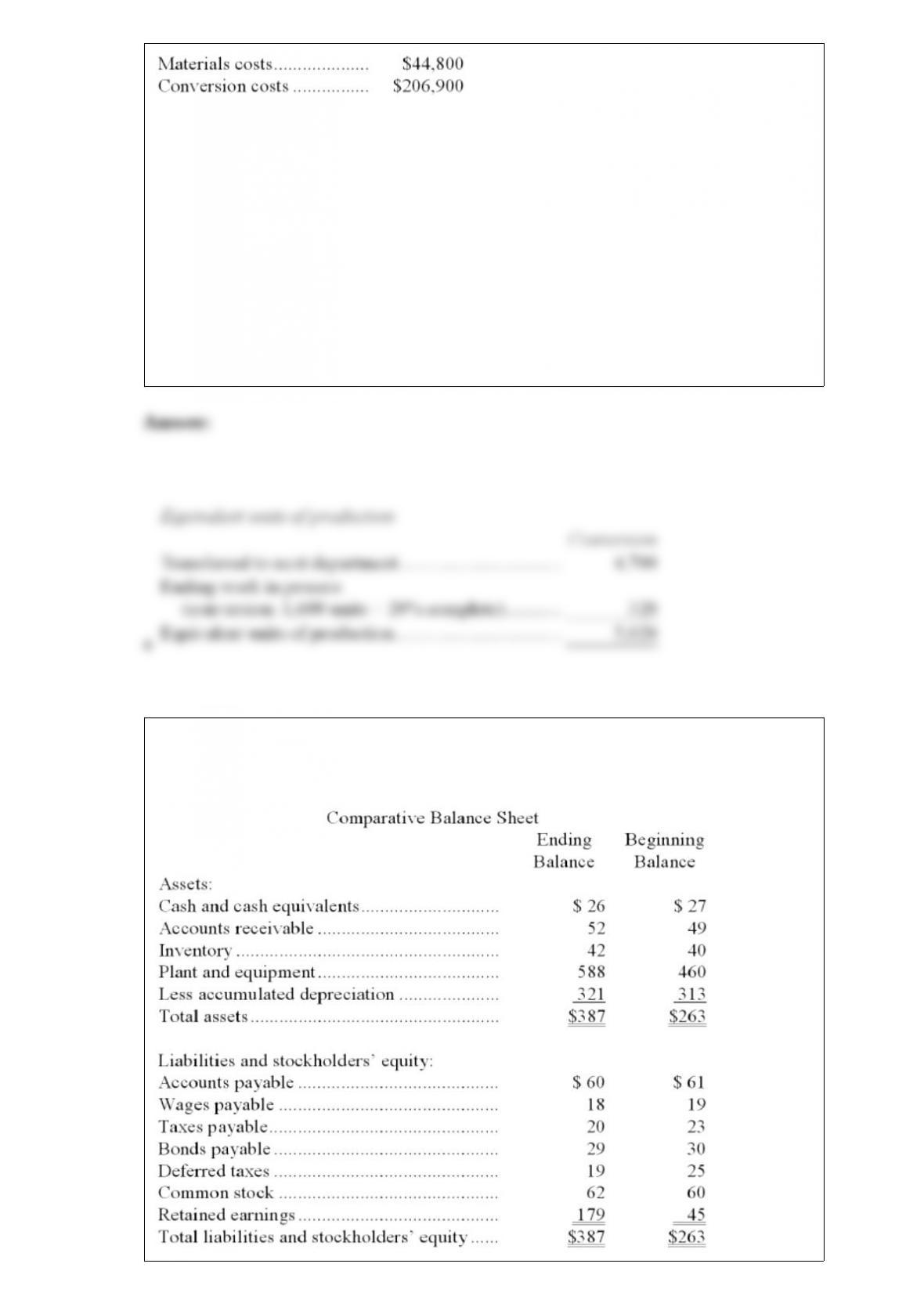

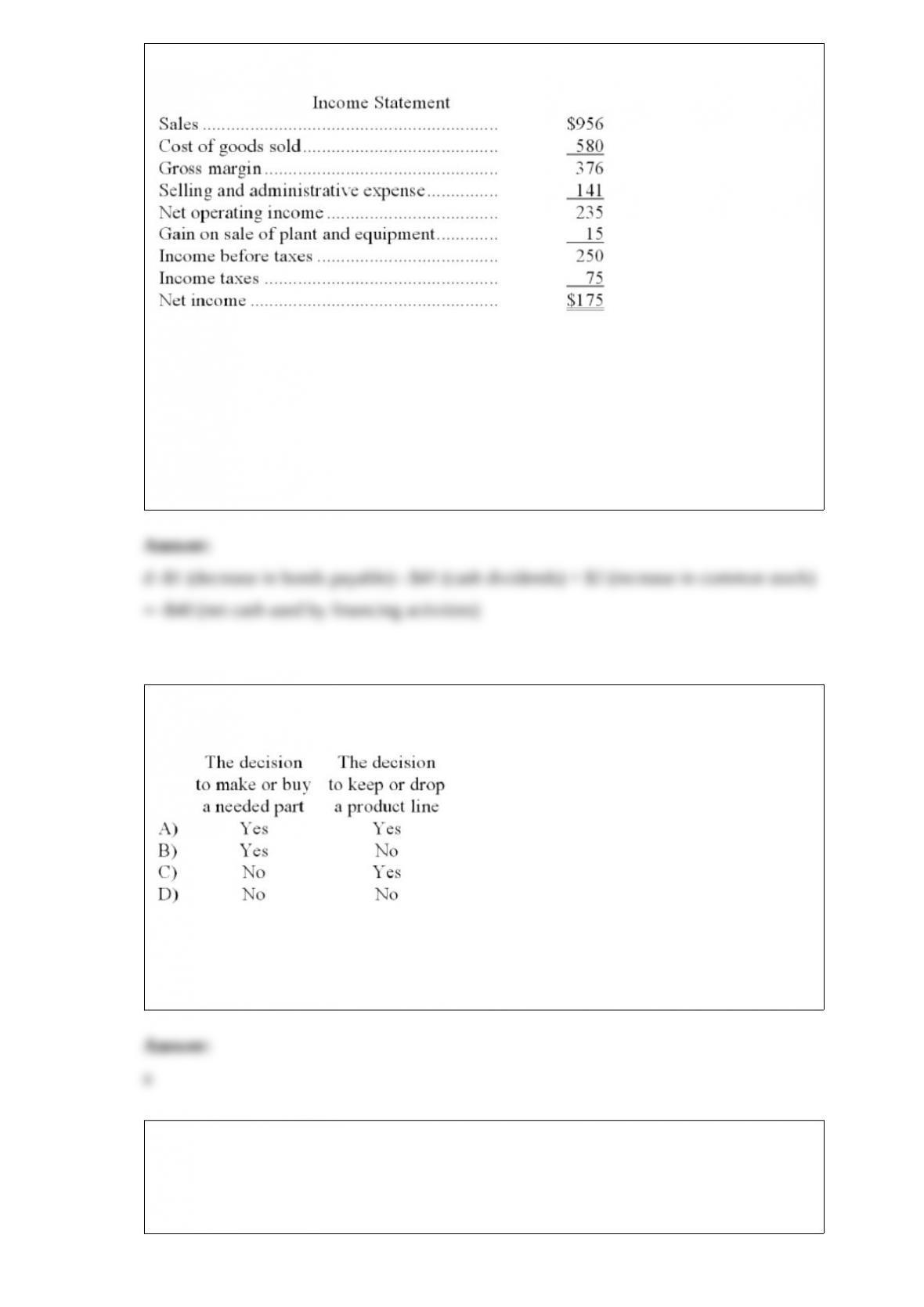

13) burgett corporation’s balance sheet and income statement appear below:

cash dividends were $41. the company sold equipment for $15 that was originally

purchased for $4 and that had accumulated depreciation of $4.

the net cash provided by (used by) financing activities for the year was:

a.($1)

b.($41)

c.$2

d.($40)

14) for which of the following decisions are opportunity costs relevant?

a.choice a

b.choice b

c.choice c

d.choice d

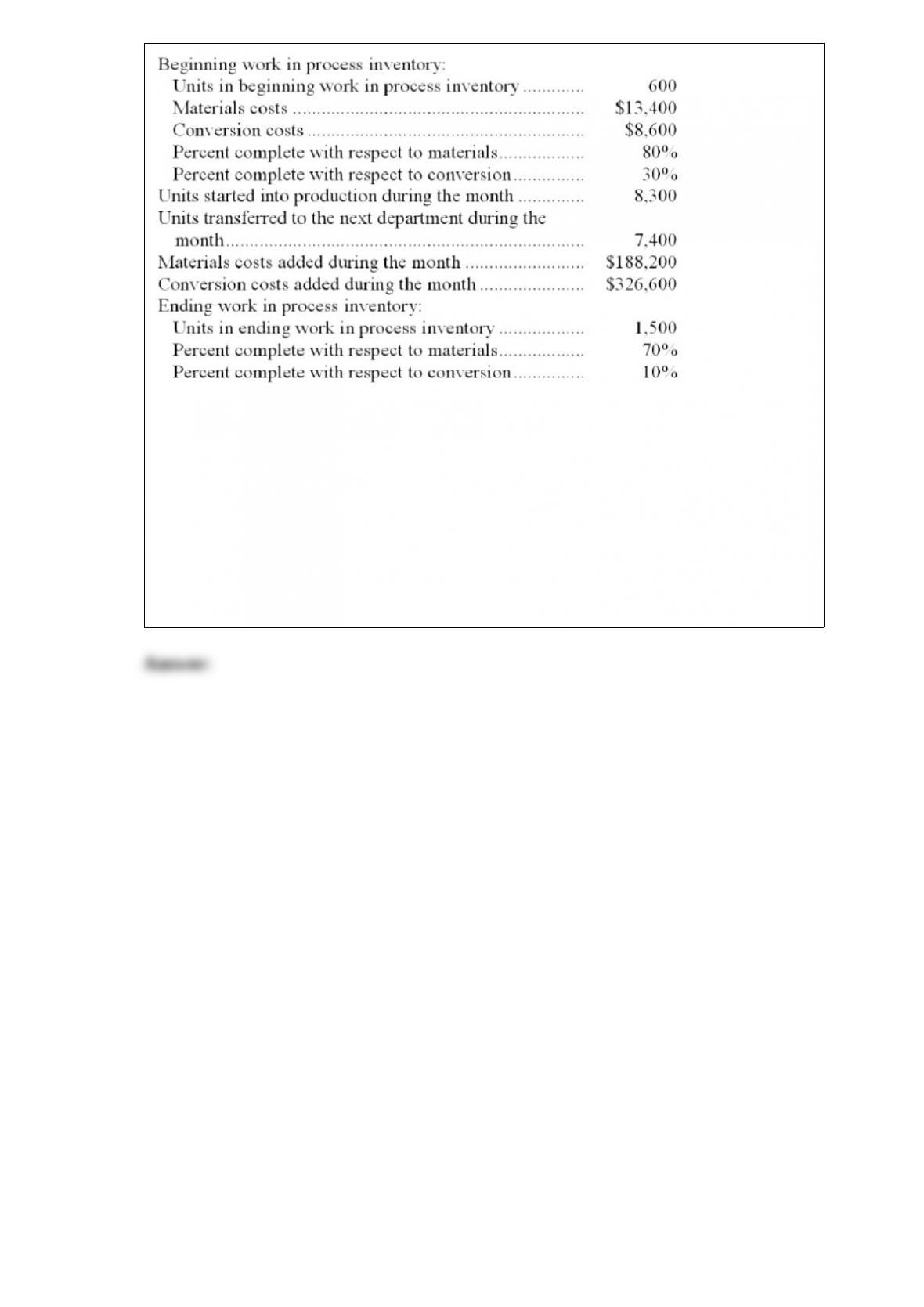

15) lowler corporation uses the weighted-average method in its process costing system.

data concerning the first processing department for the most recent month are listed

below:

note: your answers may differ from those offered below due to rounding error. in all

cases, select the answer that is the closest to the answer you computed. to reduce

rounding error, carry out all computations to at least three decimal places.

the cost of ending work in process inventory in the first processing department

according to the company’s cost system is closest to:

a.$102,383

b.$71,668

c.$31,711

d.$10,238

16) products a, b, and c are produced from a single raw material input. the raw material

costs $90,000, from which 5,000 units of a, 10,000 units of b, and 15,000 units of c can

be produced each period. product a can be sold at the split-off point for $2 per unit, or it

can be processed further at a cost of $12,500 and then sold for $5 per unit. product a

should be:

a.sold at the split-off point, since further processing would result in a loss of $0.50 per

unit

b.processed further, since this will increase profits by $2,500 each period

c.sold at the split-off point, since further processing will result in a loss of $2,500 each

period

d.processed further, since this will increase profits by $12,500 each period