In a consignment arrangement, revenue typically should not be recognized until sale to

a third party occurs, even though there has been a physical transfer of goods to the

consignee, because the consignor still retains legal title to the goods.

The gross profit ratio is calculated by dividing gross profit by average inventory.

The balance sheet reports a company’s financial position at a point in time.

Accrual accounting attempts to measure revenues and expenses that occurred during

accounting periods so they equal net operating cash flow.

Any method of depreciation should be both systematic and rational.

Revenue typically should not be recognized when payment is received but the goods are

warehoused at the seller’s facility.

The fair value option cannot be elected for significant-influence investments because

those must be accounted for under the equity method.

Which of the following does not reduce the balance in accounts receivable?

a. Returns on credit sales.

b. Collections from customers.

c. Recognizing bad debts expense.

d. Write-offs.

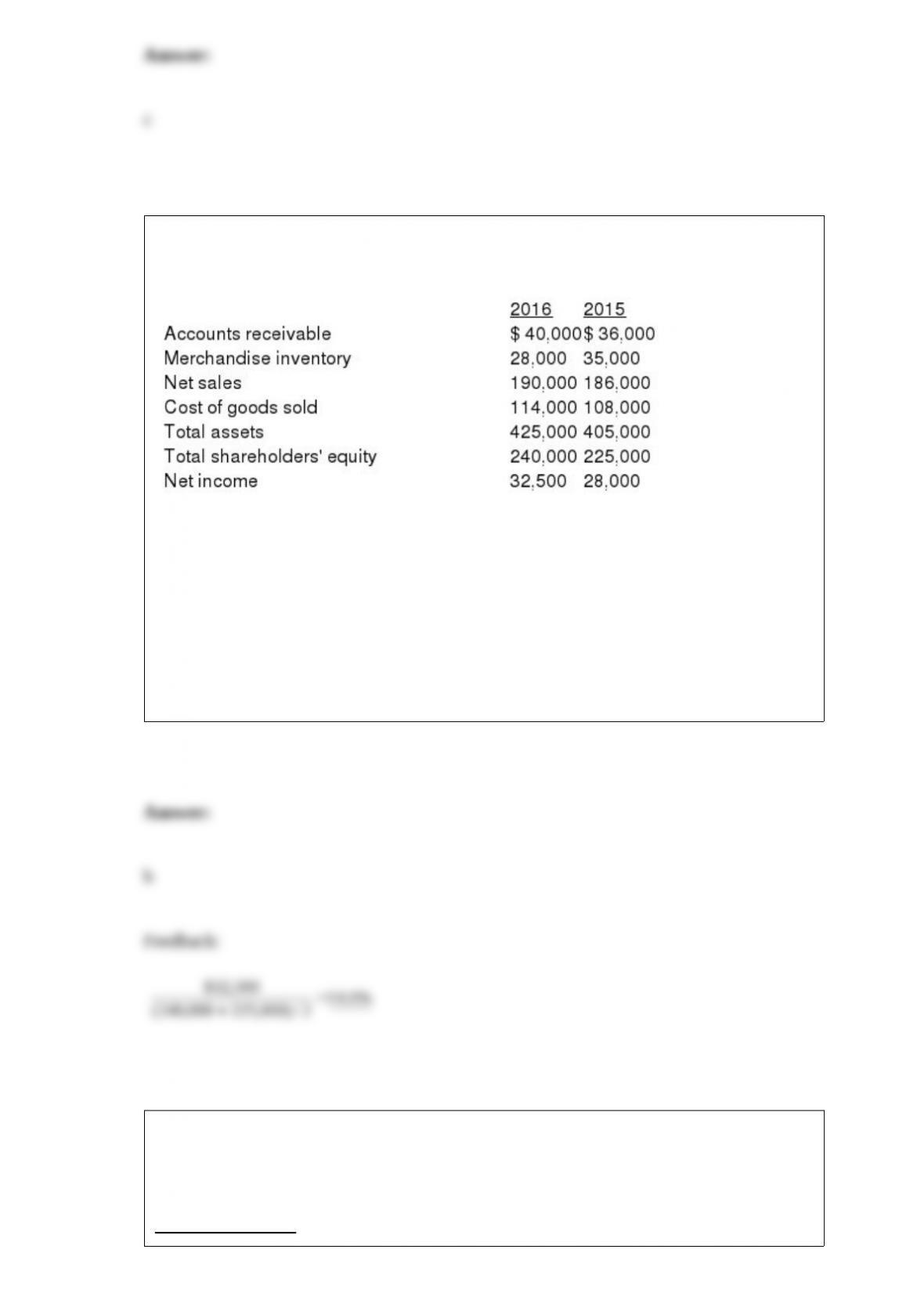

Excerpts from Hulkster Company’s December 31, 2016 and 2015, financial statements

are presented below:

Hulkster’s 2016 return on shareholders’ equity is (rounded):

a. 17.1%.

b. 14.0%.

c. 12.6%.

d. 7.1%.

Bond Company adopted the dollar-value LIFO inventory method on January 1, 2016. In

applying the LIFO method, Bond uses internal cost indexes and the multiple-pools

approach. The following data were available for Inventory Pool No. 3 for the two years

following the adoption of LIFO:

Ending Inventory

At Current At Base Year Cost Year Cost Cost Index

1/1/16 $300,000 $300,000 1.00

12/31/16 345,600 320,000 1.08

12/31/17 420,000 350,000 1.20 Under the dollar-value LIFO method, the inventory

at December 31, 2017, should be

a. $357,600.

b. $350,000.

c. $351,600.

d. None of these answer choices is correct.

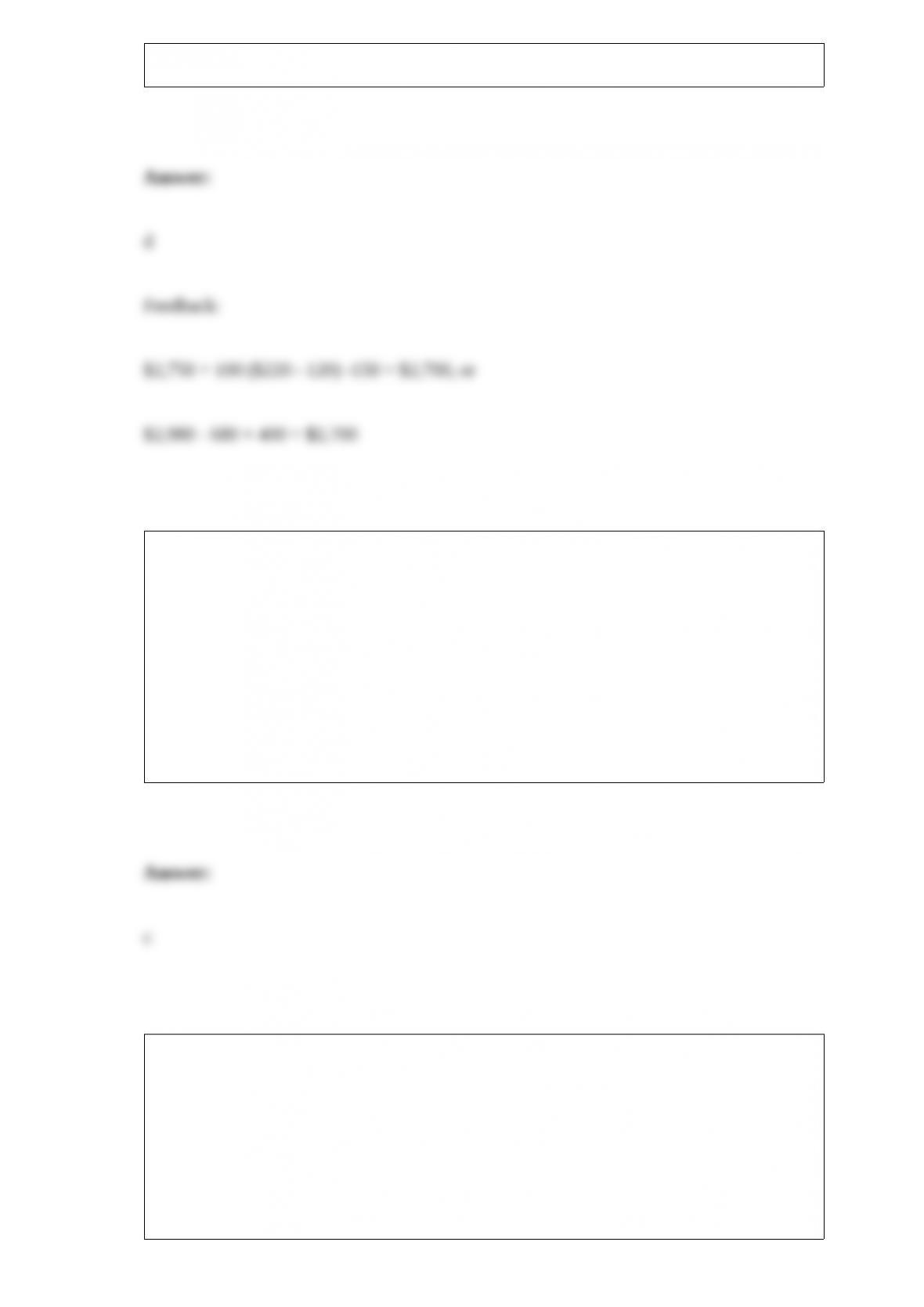

Brockton Carpet Cleaning prepares a bank reconciliation at the end of every month. At

the end of July, the balance in the general ledger checking account was $2,750 and the

bank balance on the bank statement was $2,980. Outstanding checks totaled $680 and

deposits in transited were $400. The bank statement revealed that a check written for

$120 was incorrectly recorded by Brockton as a $220 disbursement. The bank statement

listed service charges and NSF check charges totaling $150. The corrected cash balance

is:

a. $2,270.

b. $2,550.

c. $2,470.

d. $2,700.

Revenue and expense items and components of other comprehensive income can be

reported in a single statement of comprehensive income using:

a. U.S. GAAP.

b. IFRS.

c. Both U.S. GAAP and IFRS.

d. Neither U.S. GAAP nor IFRS.

An analyst compiled the following information for U Inc. for the year ended December

31, 2016:

– Net income was $1,700,000.

– Depreciation expense was $400,000.

– Interest paid was $200,000.

– Income taxes paid were $100,000.

– Common stock was sold for $200,000.

– Preferred stock (8% annual dividend) was sold at par value of $250,000.

– Common stock dividends of $50,000 were paid.

– Preferred stock dividends of $20,000 were paid.

– Equipment with a book value of $100,000 was sold for $200,000.

Using the indirect method, what was U Inc.’s net cash flow from operating activities for

the year ended December 31, 2016?

a. $2,000,000.

b. $2,030,000.

c. $2,080,000.

d. $2,100,000.

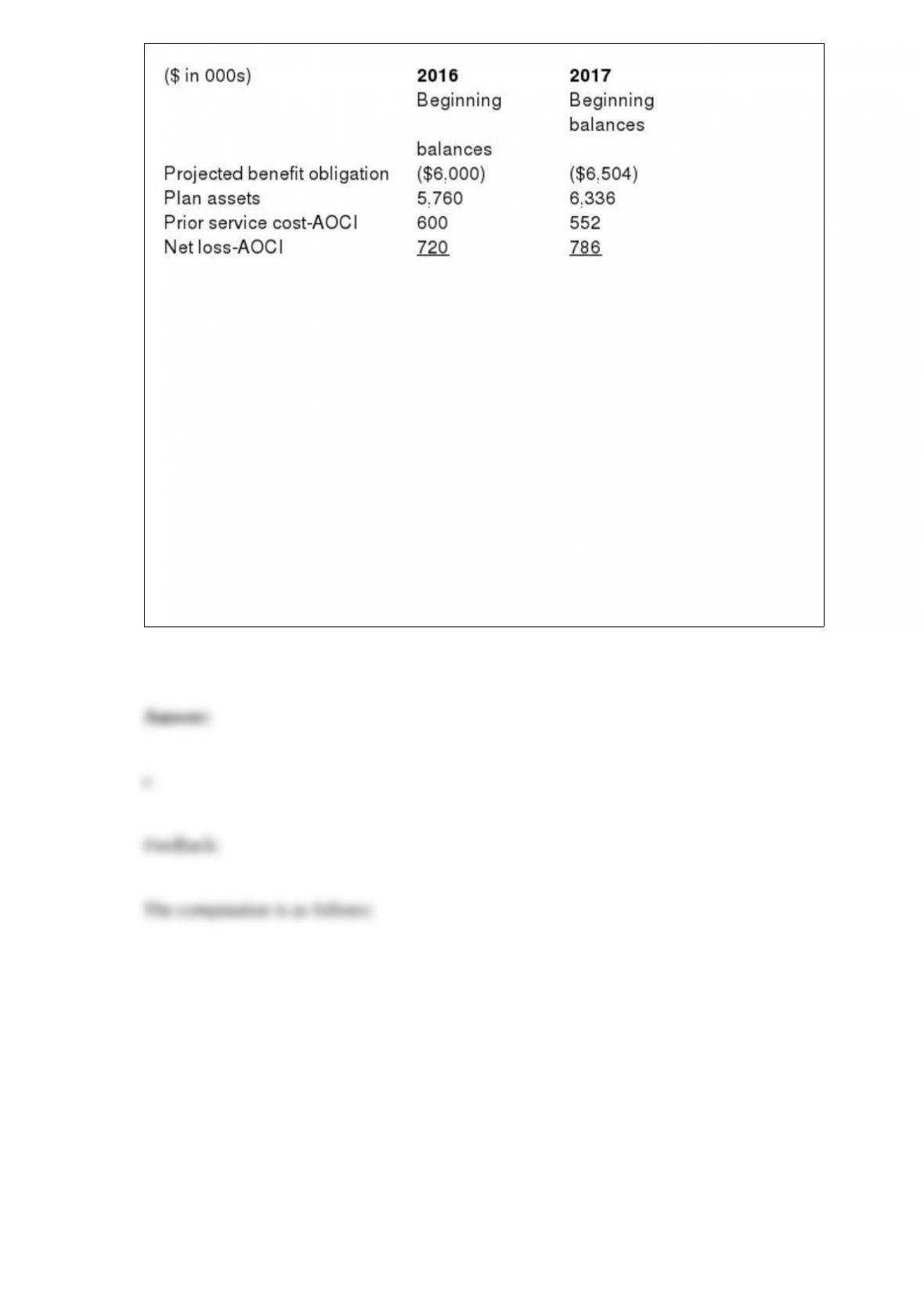

The following information pertains to Havana Corporation’s defined benefit pension

plan:

At the end of 2016, Havana contributed $696 thousand to the pension fund and benefit

payments of $624 thousand were made to retirees. The expected rate of return on plan

assets was 10%, and the actuary’s discount rate is 8%. There were no changes in

actuarial estimates and assumptions regarding the PBO.

What is the 2016 service cost for Havana’s plan?

a. $276 thousand.

b. $528 thousand.

c. $648 thousand.

d. Cannot be determined from the given information.

Under the conventional retail method, the denominator in the cost-to-retail percentage

includes:

a. Net markups and net markdowns.

b. Neither net markups nor net markdowns.

c. Net markups, but not net markdowns.

d. Net markdowns, but not net markups.

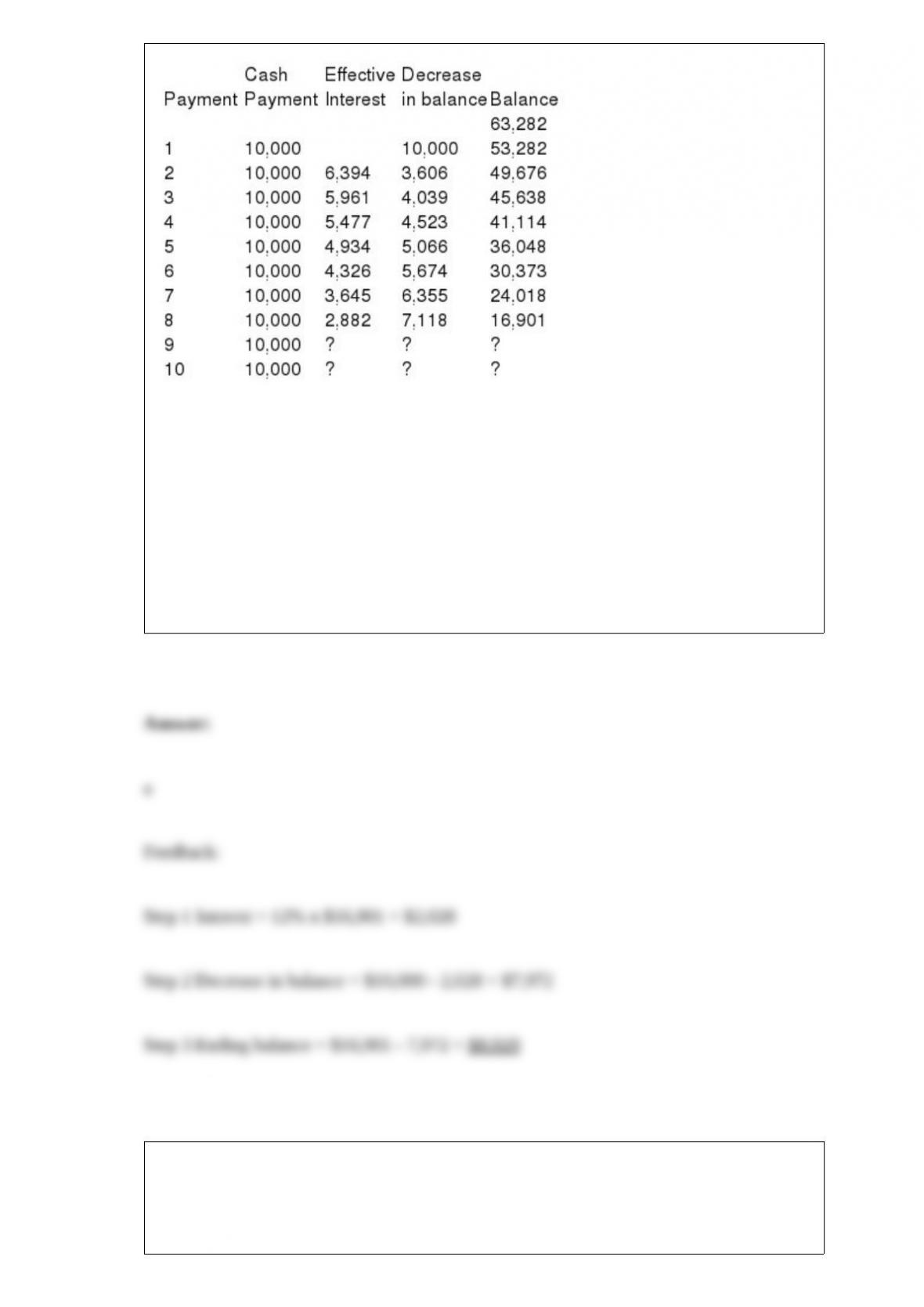

Refer to the following lease amortization schedule. The 10 payments are made annually

starting with the inception of the lease. Title does not transfer to the lessee and there is

no bargain purchase option or guaranteed residual value. The asset has an expected

economic life of 12 years. The lease is noncancelable.

What is the outstanding balance after payment 9?

a. $ 8,929.

b. $13,463.

c. $ 5,000.

d. $ 5,537.

Cash equivalents would not include:

a. Cash not available for current operations.

b. Money market funds.

c. U.S. treasury bills.

d. Bank drafts.

When a registrant company submits its annual filing to the SEC, it uses:

a. Form 10-A.

b. Form 10-K.

c. Form 10-Q.

d. Form S-1.

Under IFRS, the role of the conceptual framework:

a. Primarily involves guiding standard setters to make sure that standards are consistent

with each other.

b. Includes serving as a guide for practitioners when a specific standard does not apply.

c. Is less important than in U.S. GAAP.

d. Has resulted primarily from a convergence with U.S. GAAP.

National Hoopla Company switches from sum-of-the-years’ digits depreciation to

straight-line depreciation. As a result:

a. Current income tax payable increases.

b. The cumulative effect decreases current period earnings.

c. Prior periods’ financial statements are restated.

d. None of these answer choices is correct.

At December 31, 2015, Mongo, Inc., reported in its balance sheet a net loss of $3

million related to its pension plan. The actuary for Mongo at the end of 2016 increased

her estimate of future salary levels. Mongo’s entry to record the effect of this change

will include:

a. A debit to loss-OCI and a credit to PBO.

b. A debit to PBO and a credit to loss-OCI.

c. A debit to pension expense and a credit to PBO.

d. A debit to pension expense and a credit to loss-OCI.

The most political issue in the FASB’s most recent deliberations and amendments to

GAAP on business combinations was:

a. The negative effects on subsequent earnings of amortizing goodwill if firms were

required to use the purchase method of accounting for the combination.

b. The negative effects on subsequent earnings of amortizing goodwill if firms were

required to use the pooling method of accounting for the combination.

c. The unrealistic balance sheet assets that would be created if firms were required to

use the purchase method of accounting for the combination.

d. The unrealistic balance sheet assets that would be created if firms were required to

use the pooling method of accounting for the combination.

Matrix, Inc., acquired 25% of Neo Enterprises for $2,000,000 on January 1, 2016. The

fair value and book value of 25% of Neo’s identifiable net assets was $2,000,000 and

$1,600,000 on that date, and the difference was attributable to assets that would be

depreciated over 10 years. During 2016 Neo recognized net income of $500,000 and

paid dividends of $400,000. Neo had a total fair value of $10,000,000 as of December

31, 2016.

Required:

(1.) Prepare the journal entries necessary to account for the Neo investment, assuming

that Matrix elects the fair-value option.

(2.) Prepare the journal entries necessary to account for the Neo investment, assuming

that Matrix elects the fair-value option.

On March 17, 2015, Union Corporation purchased 5,000 shares of AZQ common stock

as a long-term investment at $40 per share. On December 31, 2015, and December 31,

2016, the market value of the AZQ stock is $42 and $43, respectively.

Required:

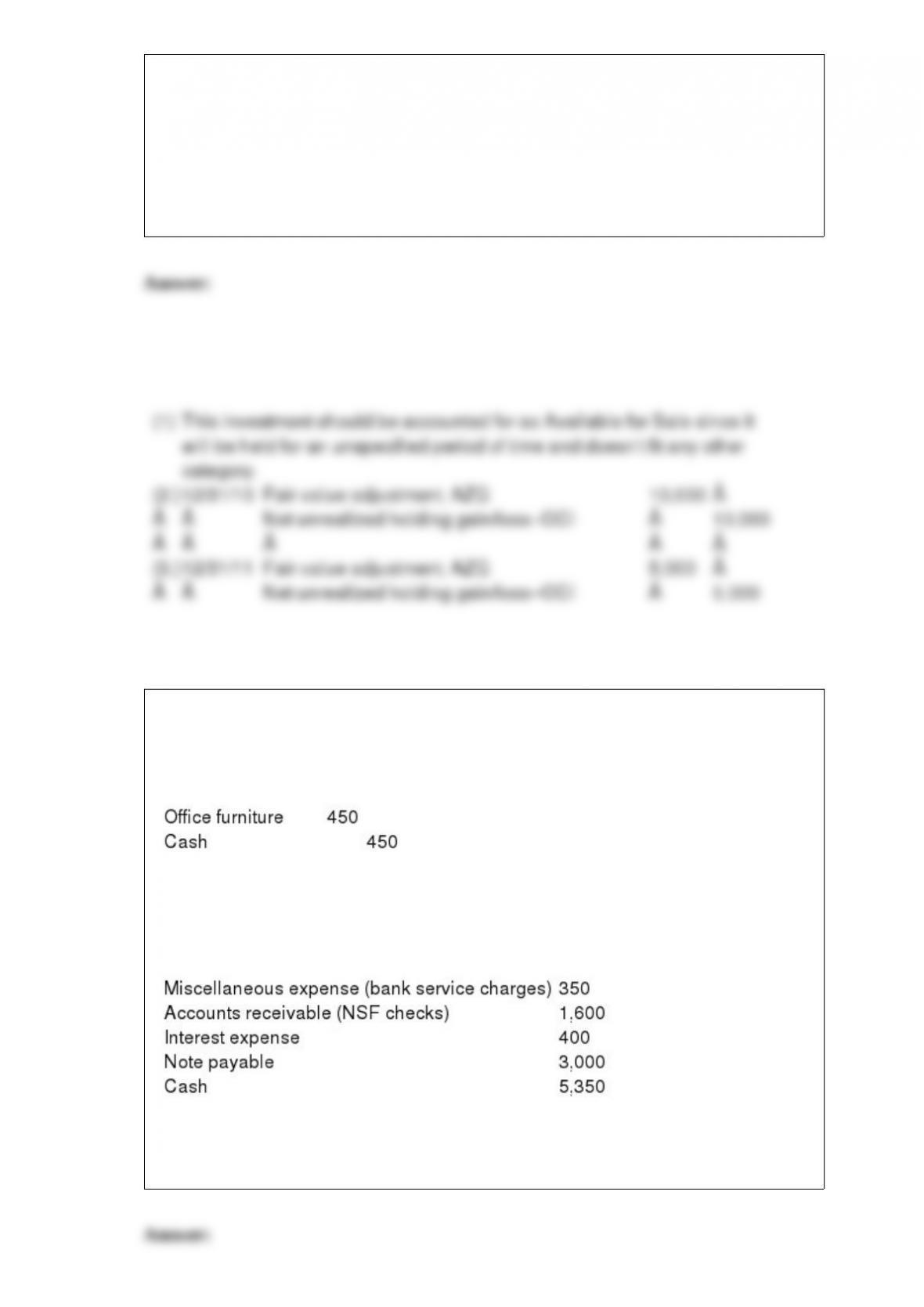

(1.) What is the appropriate reporting category for this stock? Why?

(2.) Prepare the adjusting entry on December 31, 2015.

(3.) Prepare the adjusting entry on December 31, 2016.

To correct error in recording cash disbursement.

To record credits to cash revealed by the bank reconciliation.

Note: Each of the adjustments to the book balance required journal entries.

None of the adjustments to the bank balance require entries.

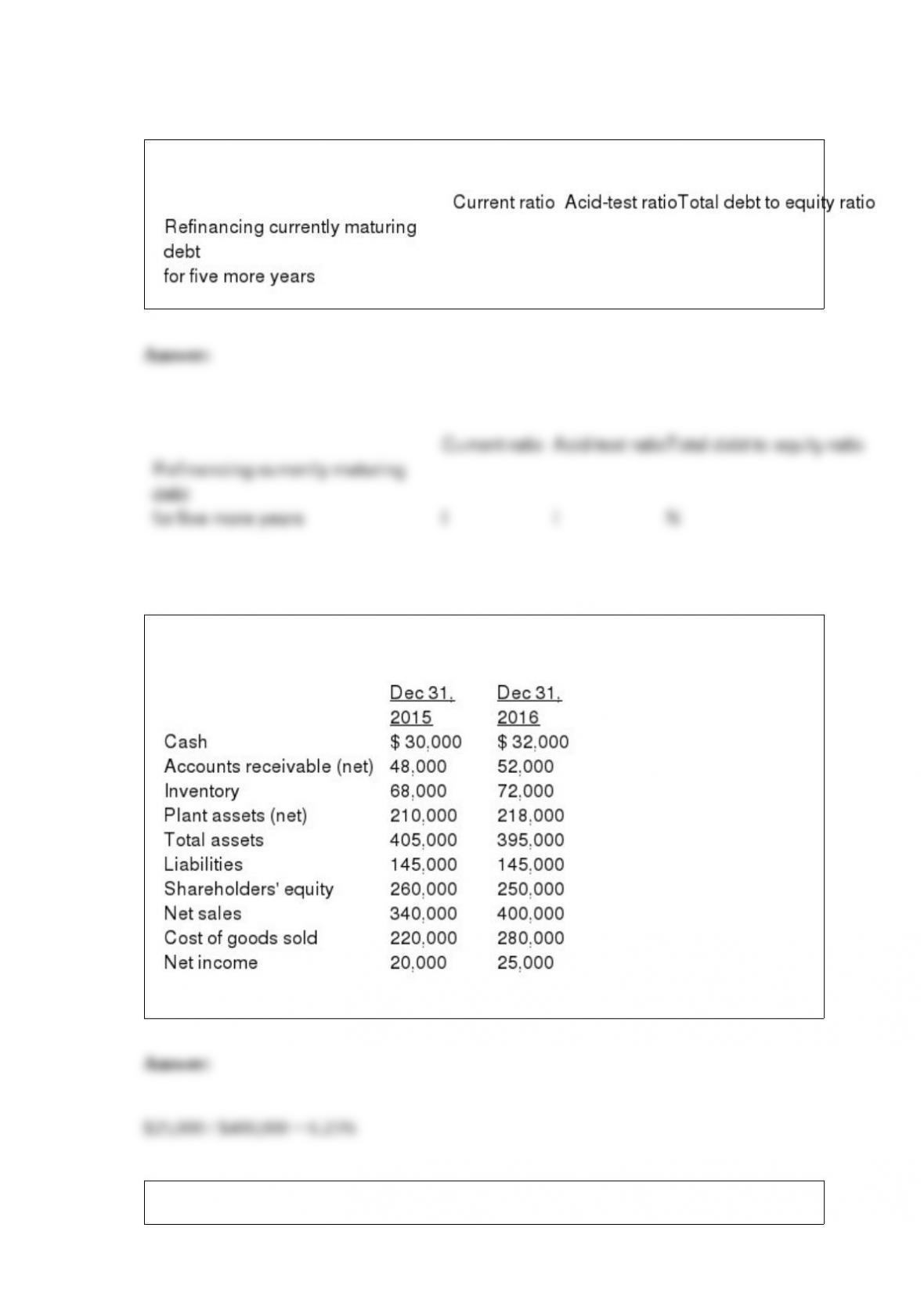

Missoula Inc. reported the following selected financial statement data:

Required: Compute the profit margin on sales for 2016.

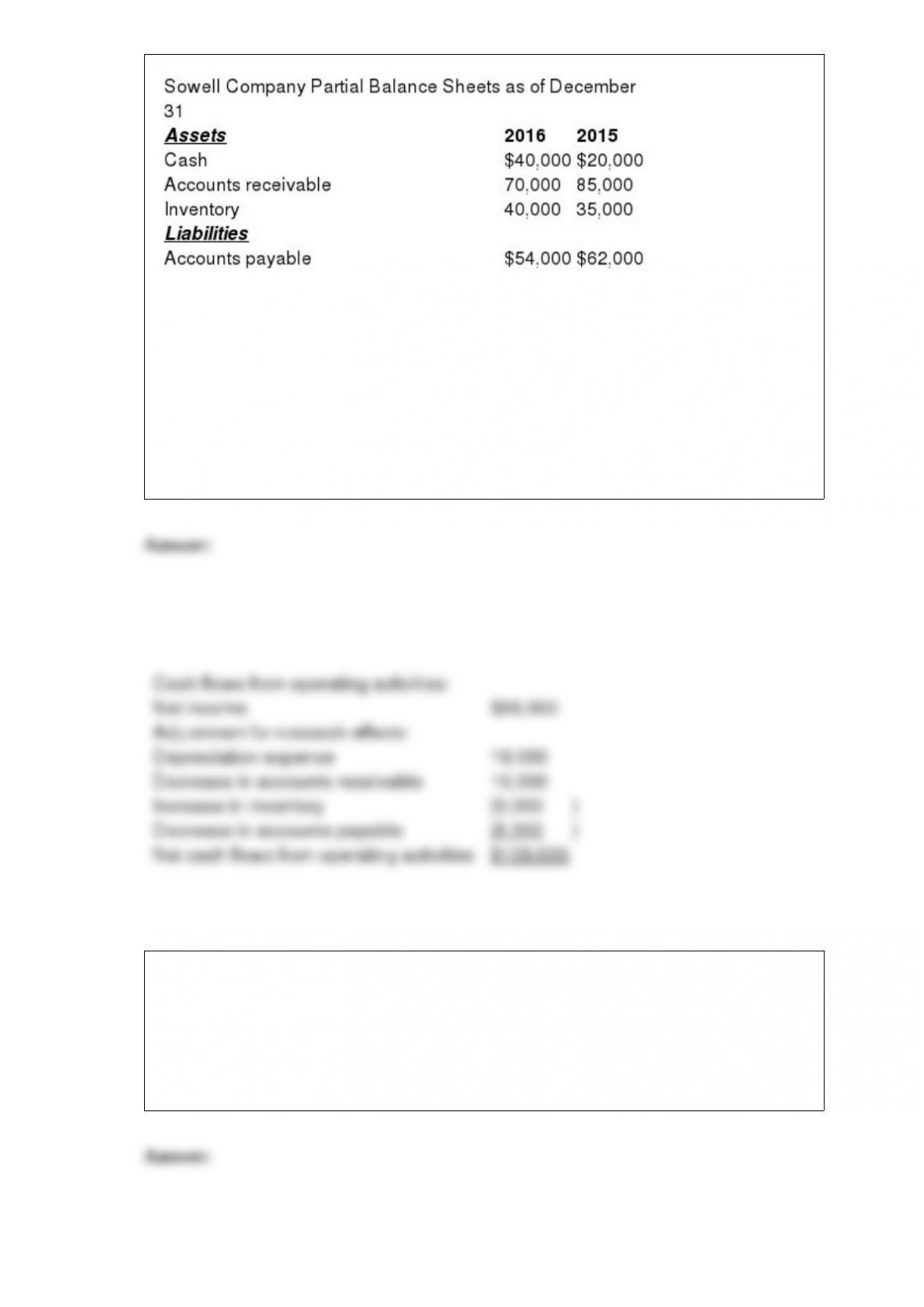

Partial balance sheets and additional information are listed below for Sowell Company.

Additional information for 2016:

Net income was $88,000.

Depreciation expense was $19,000.

Required:

Prepare the operating activities section of the statement of cash flows for 2016 using the

indirect method.

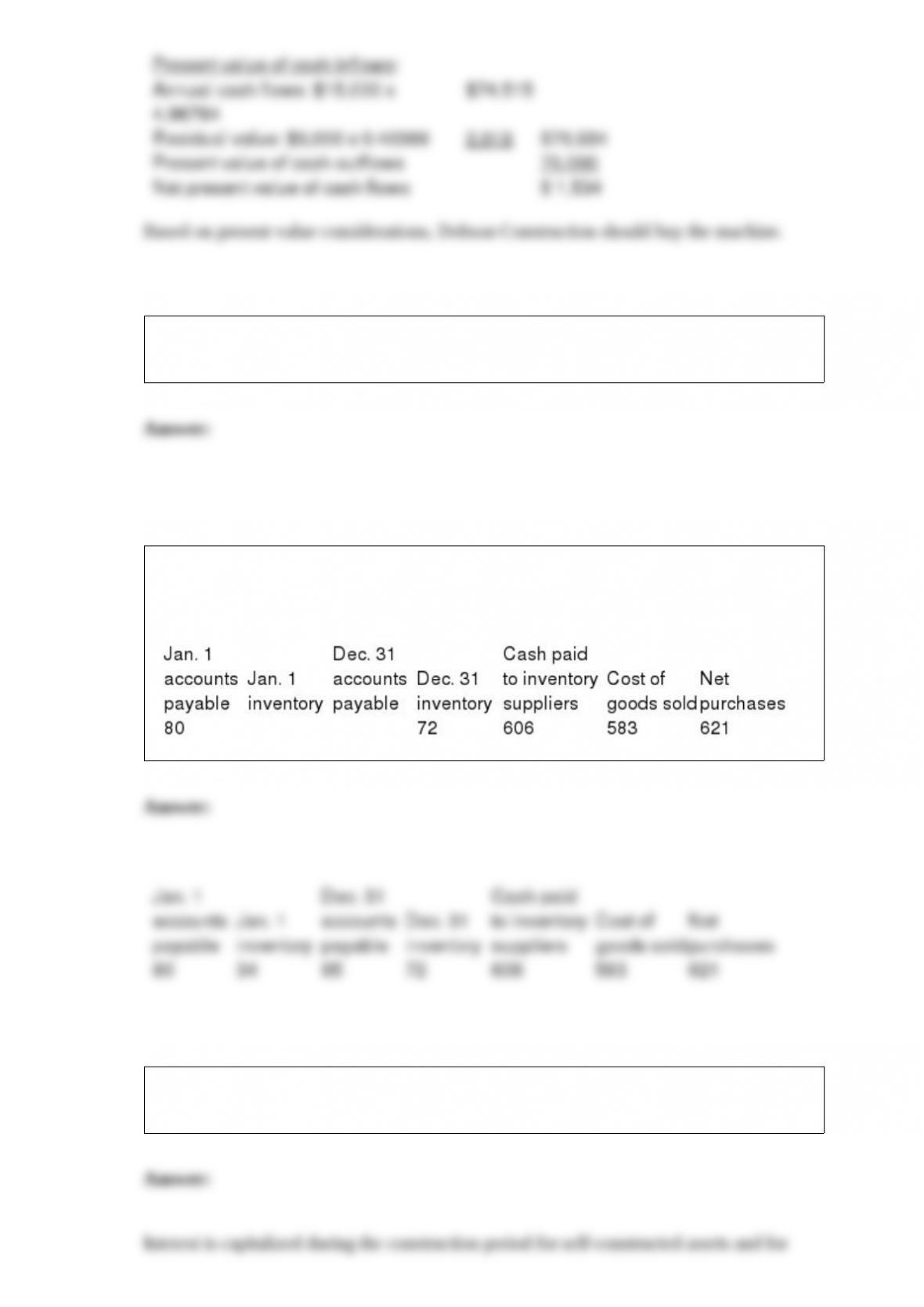

Dobson Contractors is considering buying equipment at a cost of $75,000. The

equipment is expected to generate cash flows of $15,000 per year for eight years and

can be sold at the end of eight years for $5,000. Interest is at 12%. Assume the

equipment purchase would be paid for on the first day of year one, but that all other

cash flows occur at the end of the year. Ignore income tax considerations.

Required: Determine if Dobson should purchase the machine.

Would your response to question 2 differ if Open Arms prepares its financial statements

according to International Financial Reporting Standards (IFRS)?

The following information is taken from the accounting records of Madeline Inc. for the

year 2016. Missing information has been left blank. Inventory is the only supply that

Madeline purchases on credit. Required: Compute the missing amounts.

When is interest capitalized? Briefly describe how the amount to be capitalized is

computed.