1) Section 10 and Rule 10b-5 of the Securities Exchange Act of 1934 are often referred

to as:

A) the antifraud provisions

B) the new issues provisions

C) the full-employment act for accountants

D) the RICO provisions

2) A positive confirmation is more reliable evidence than a negative confirmation

because:

A) fewer confirmations can be sent out

B) the auditor has a document which can be used in court

C) the debtor’s lack of response indicates agreement with the stated balance

D) follow-up procedures are performed if a response is not received from the debtor

3) In most audits, payroll tax expense is not tested because the audit risk does not

justify the time required to perform the tests.

A) True

B) False

4) An auditor would be least likely to use confirmations in connection with the

examination of:

A) inventories

B) long-term debt

C) property, plant, and equipment

D) stockholders’ equity

5) Which of the following would have the least impact in determining sample size for

tests of controls?

A) Expected population exception rate

B) Risk of assessing control risk too low

C) Tolerable exception rate

D) Population size

6) Under which of the following circumstances would it be advisable for the auditor to

confirm accounts payable with creditors?

A) Internal accounting control over accounts payable is adequate, and there is sufficient

evidence on hand to minimize the risk of a material misstatement

B) Confirmation response is expected to be favorable, and accounts payable balances

are of immaterial amounts

C) Creditor statements are not available and internal control over payables is

unsatisfactory

D) The majority of accounts payable balances are with associated companies

7) Internal controls are not designed to provide reasonable assurance that:

A) all frauds will be detected

B) transactions are executed in accordance with management’s authorization

C) access to assets is permitted only in accordance with management’s authorization

D) company personnel comply with applicable rules and regulations

8) What typically initiates the acquisitions and payment cycle?

A) issuance of a purchase requisition or request for purchase of goods/services

B) issuance of payment to vendor

C) approval of a new vendor

D) purchase requisition

9) The auditor may estimate the “estimated population exception rate” by taking a small

preliminary sample from the current year’s data or by using the prior year’s experience

with the client.

A) True

B) False

10) The use of positive assurance is appropriate in review reports.

A) True

B) False

11) Which of the following types of evidence is not available when using substantive

tests of transactions?

A) Documentation

B) Confirmation

C) Inquiries of the client

D) Reperformance

12) Significant deficiencies need to be communicated to the company’s audit committee

because:

A) they represent material weaknesses that allow fraud to be perpetrated

B) they represent significant design flaws in internal controls

C) they represent falsification of accounting records

D) they represent disclosure of information related to issuance of a “going-concern”

opinion

13) Total estimated misstatements include known misstatements and projected

misstatements plus a sampling error.

A) True

B) False

14) The auditor has considerable responsibility for notifying users as to whether or not

the statements are properly stated. This imposes upon the auditor a duty to:

A) provide reasonable assurance that material misstatements will be detected

B) be a guarantor of the fairness in the statements

C) be equally responsible with management for the preparation of the financial

statements

D) be an insurer of the fairness in the statements

15) Acceptable risk of incorrect acceptance (ARIA) is directly related to the computed

precision interval in difference estimation; that is, as ARIA increases, the computed

precision interval decreases.

A) True

B) False

16) When the auditor is determining appropriate depreciation calculations for the

classifications in the client’s fixed asset master file she is testing the audit objective of:

A) completeness

B) existence

C) classification

D) valuation and allocation

17) ________ accumulate costs by individual jobs as material is issued into production

and labor costs are incurred.

A) Just-in-time production systems

B) Job order cost systems

C) Process cost systems

D) Manufacturing systems

18) You are auditing the company’s purchasing process for goods and services. You are

primarily concerned with the company not recording all purchase transactions. Which

audit procedure below would be the most effective audit procedure in this case?

A) Vouching from the accounts payable account to the vendor invoices

B) Tracing vendor invoices to recorded amounts in the accounts payable account

C) Confirmation accounts payable recorded amounts

D) Reconciling the accounts payable subsidiary ledger to the accounts payable account

19) Under common law, an individual or company that (1) does not have a contract

with an auditor, (2) is known by the auditor in advance of the audit, and (3) will use the

auditor’s report to make decisions about the client company has:

A) no rights unless an auditor is grossly negligent

B) no rights unless an auditor is fraudulent

C) no rights against an auditor

D) the same rights against an auditor as a client

20) The primary purpose of allocating the preliminary judgment about materiality to

financial statement accounts is to help the auditor decide the appropriate evidence to

accumulate.

A) True

B) False

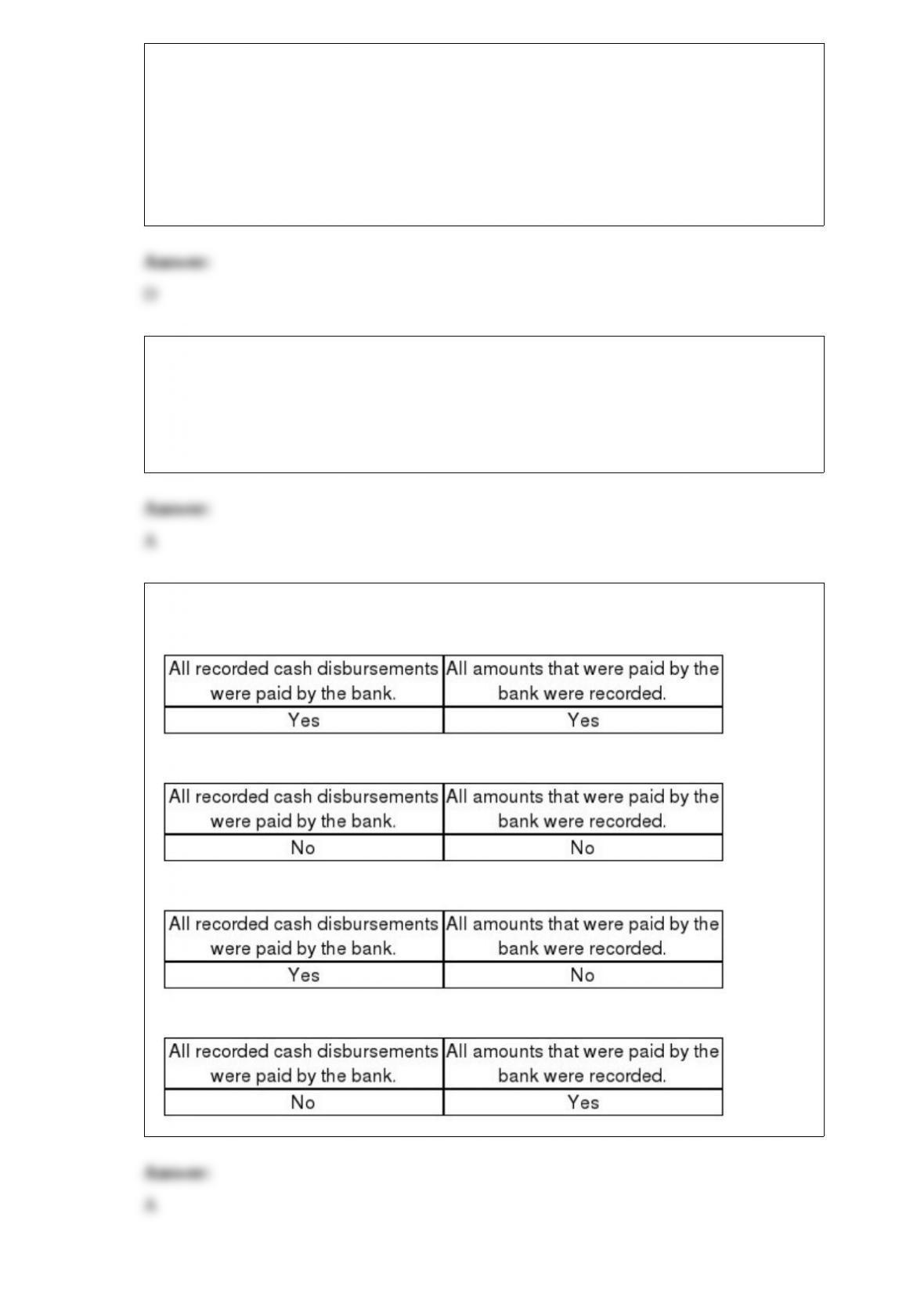

21) The auditor uses a proof of cash to determine whether:

A)

B)

C)

D)

22) Under the Securities Act of 1933, the auditor’s responsibility for making sure the

financial statements were fairly stated extends to:

A) the date of the financial statements

B) the date the registration statement becomes effective

C) the date of the audit report

D) one year beyond the date of the financial statements

23) Which of the following is not a risk specific to IT environments?

A) reliance on the functioning capabilities of hardware and software

B) increased human involvement

C) loss of data due to insufficient backup

D) unauthorized access

24) When should auditors not perform alternative procedures in testing the accounts

receivable balance?

A) When customers do not return positive confirmation requests

B) When customers do not return negative confirmation requests

C) When confirmations are deemed to be ineffective as an audit procedure

D) When confirmations are too costly to use

25) When a client uses an outside payroll service for processing payroll, professional

auditing standards require the auditor to rely on the internal controls of the service

organization if the service organization’s auditor has issued a favorable report on

internal controls.

A) True

B) False

26) Discuss what is meant by the term “control environment” and identify four control

environment subcomponents that the auditor should consider.

27) The design of tests of details of balances for inventory is affected by audit results

from multiple cycles. Identify the cycles, other than the inventory and warehousing

cycle that affect the audit of inventory.

28) Material misstatement is the magnitude of misstatement that makes a reasonable

person either change their mind or be influenced by the misstatement. Audit standards

require the auditor to consider the combined amount of misstatement early in the audit.

This is known as preliminary materiality judgment. List and discuss the three main

factors that affect an auditor’s preliminary judgment about materiality.

29) Define forecast and projection.

30) When performing an attestation engagement a CPA is required to adhere to the

Statements on Standards for Attestation Engagements. Describe below the Standards of

Field Work for attestation engagements.

31) Discuss each of the four defenses a CPA firm can normally use when facing legal

claims by clients. Which of these defenses is ordinarily not available against third-party

suits?

32) Identify and describe each of the four parts to the

33) Discuss the overall objectives of the audit of notes payable.

34) An important balance related objective is realizable value. Describe what is the

purpose of this audit objective, what it is concerned with, and give an example.

35) What are the four steps auditors follow when they plan to reduce assessed control

risk?