Moore Company.

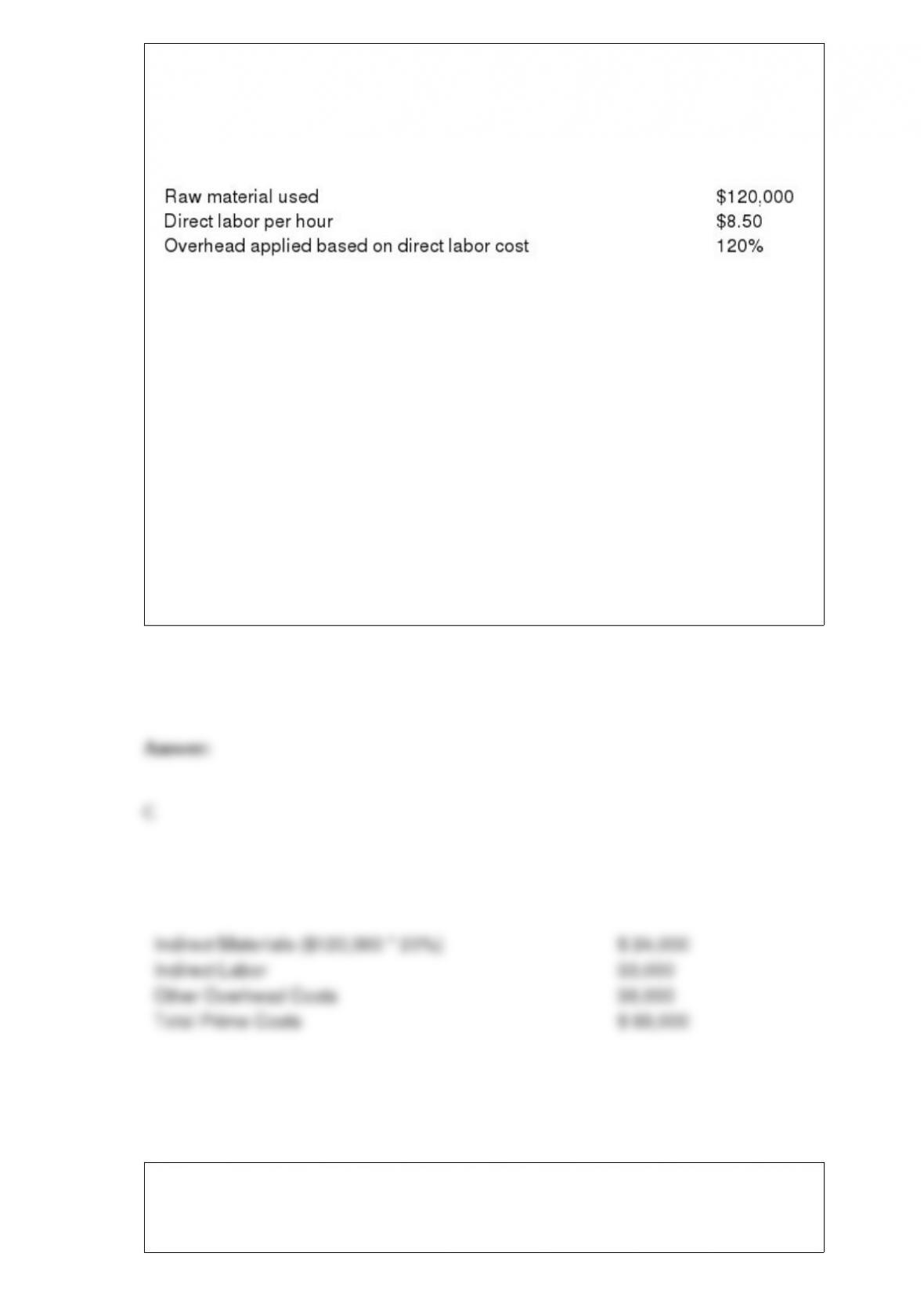

Moore Company uses a job-order costing system and the following information is

available from its records. The company has three jobs in process: #6, #9, and #13.

Direct material was requisitioned as follows for each job respectively: 30 percent, 25

percent, and 25 percent; the balance of the requisitions was considered indirect. Direct

labor hours per job are 2,500; 3,100; and 4,200; respectively. Indirect labor is $33,000.

Other actual overhead costs totaled $36,000.

Refer to Moore Company. What is the total amount of actual overhead?

a. $36,000

b. $69,000

c. $93,000

d. $99,960

If a new project generates a positive residual income, the

a. project’s return on investment is less than the target rate.

b. project’s return on investment is greater than the target rate.

c. project’s return on investment is equal to the target rate.

d. relationship between the project’s return on investment and the target rate cannot

necessarily be determined.

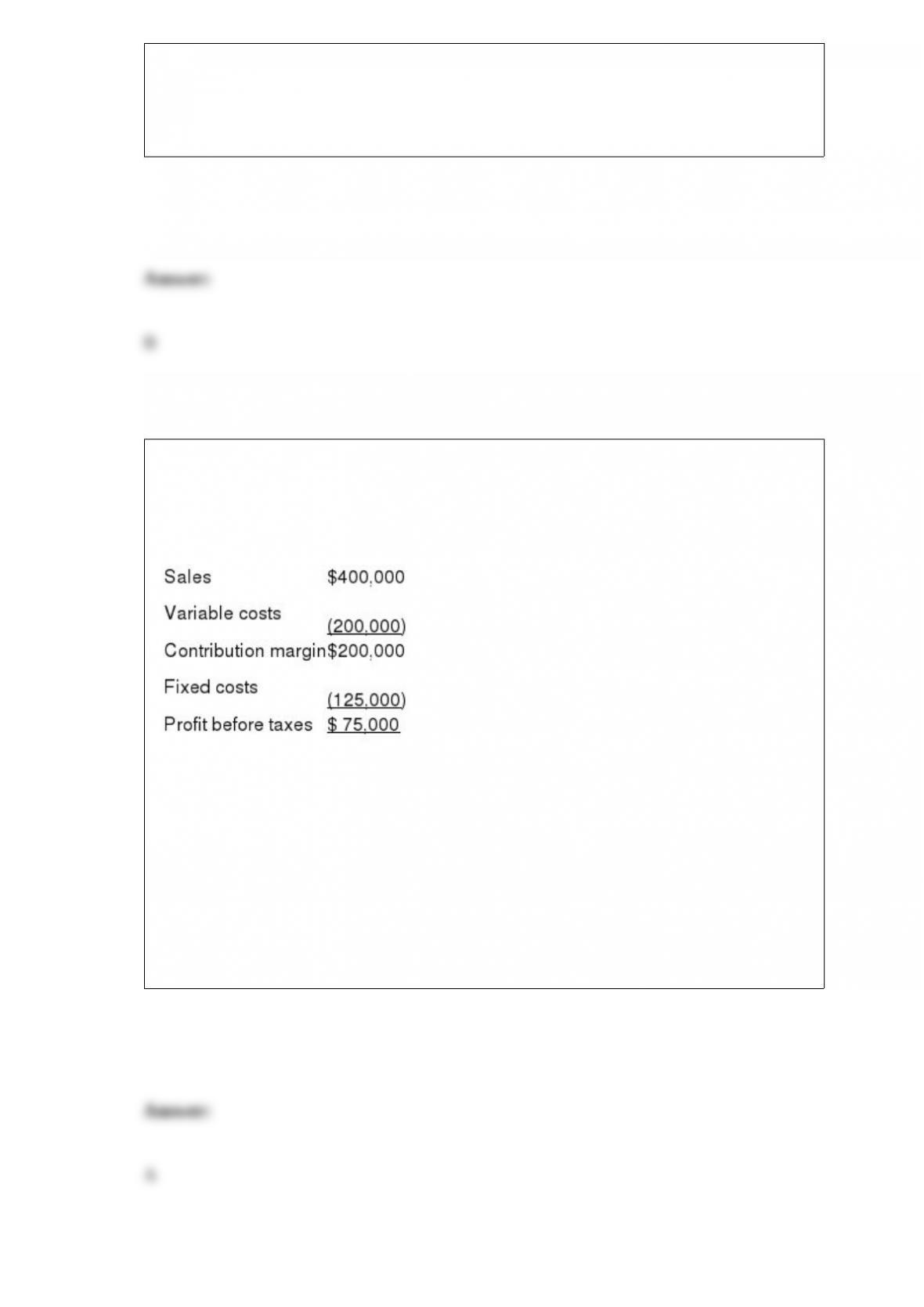

Robert Wilson Company

Below is an income statement for Robert Wilson Company:

Refer to Robert Wilson Company. What is the company’s degree of operating leverage

(DOL)?

a. 2.67

b. 3.2

c. 5.33

d. 10.67

Which service department cost allocation method assigns indirect costs to cost objects

after considering interrelationships of the cost objects?

a. no no

b. no yes

c. yes yes

d. yes no

Joint costs are allocated to which of the following products?

a. yes yes

b. yes no

c. no no

d. no yes

When a scarce resource, such as space, exists in an organization, the criterion that

should be used to determine production is

a. contribution margin per unit.

b. selling price per unit.

c. contribution margin per unit of scarce resource.

d. total variable costs of production.

Lead time minus production time is equal to

a. idle time.

b. storage time.

c. non-value-added time.

d. value-added time.

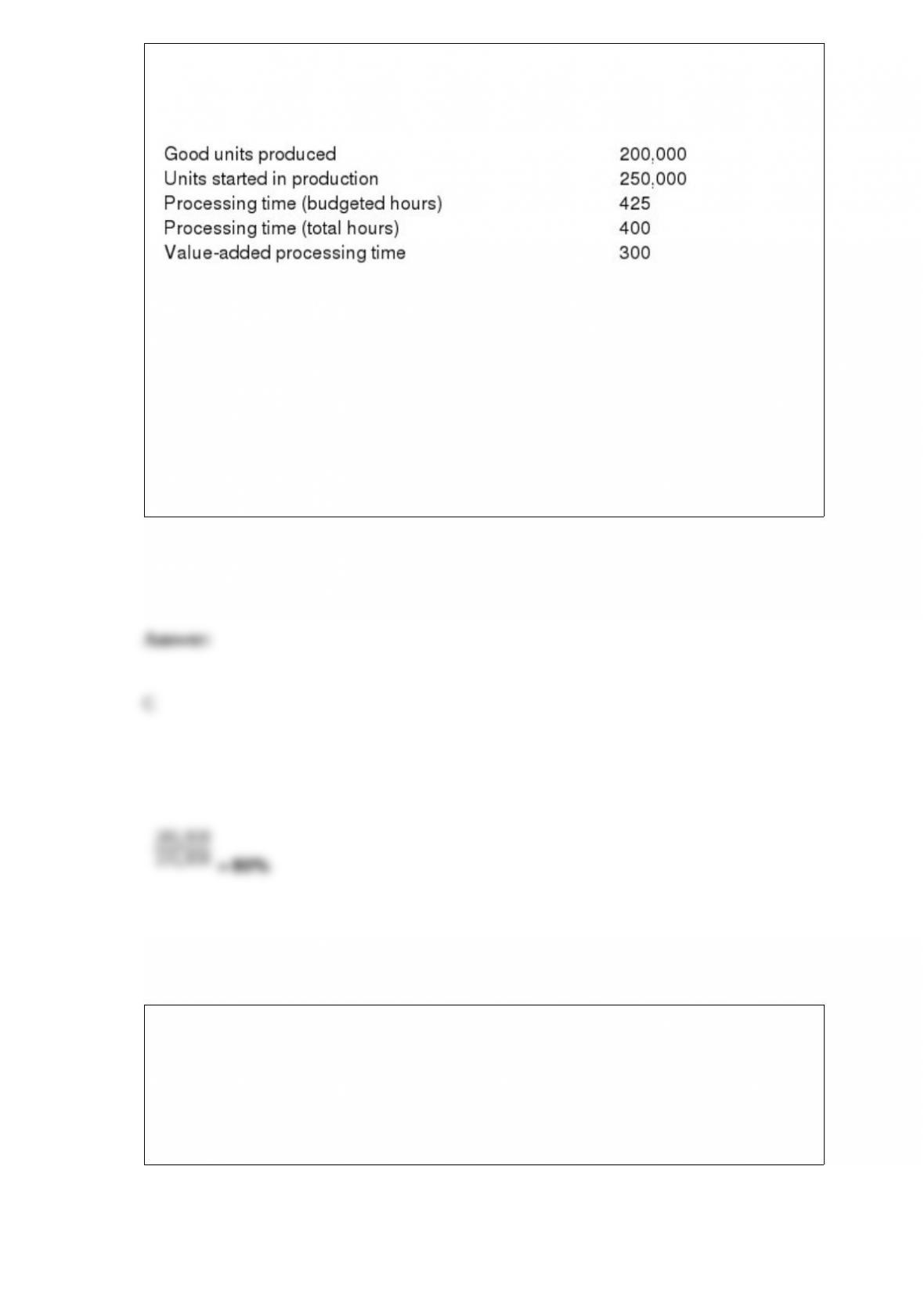

Buxton Company

One of the products manufactured by Buxton Company is a plastic tray. The

information below relates to the Tray Production Department:

Refer to Buxton Company. What is the process quality yield in the Tray Production

Department?

a. 75%

b. 44%

c. 80%

d. 125%

The final figure in the Schedule of Cost of Goods Manufactured represents the

a. cost of goods sold for the period.

b. total cost of manufacturing for the period.

c. total cost of goods started and completed this period.

d. total cost of goods completed for the period.

Hogan Company uses a weighted average process costing system and started 30,000

units this month. Hogan had 12,000 units that were 20 percent complete as to

conversion costs in beginning Work in Process Inventory and 3,000 units that were 40

percent complete as to conversion costs in ending Work in Process Inventory. What are

equivalent units for conversion costs?

a. 37,800

b. 40,200

c. 40,800

d. 42,000

Which of the following is necessary for any valid performance measurement?

a. It must be part of the financial accounting system in use.

b. It must be quantifiable.

c. Goal congruence must be promoted by its use.

d. It must be financial in nature.

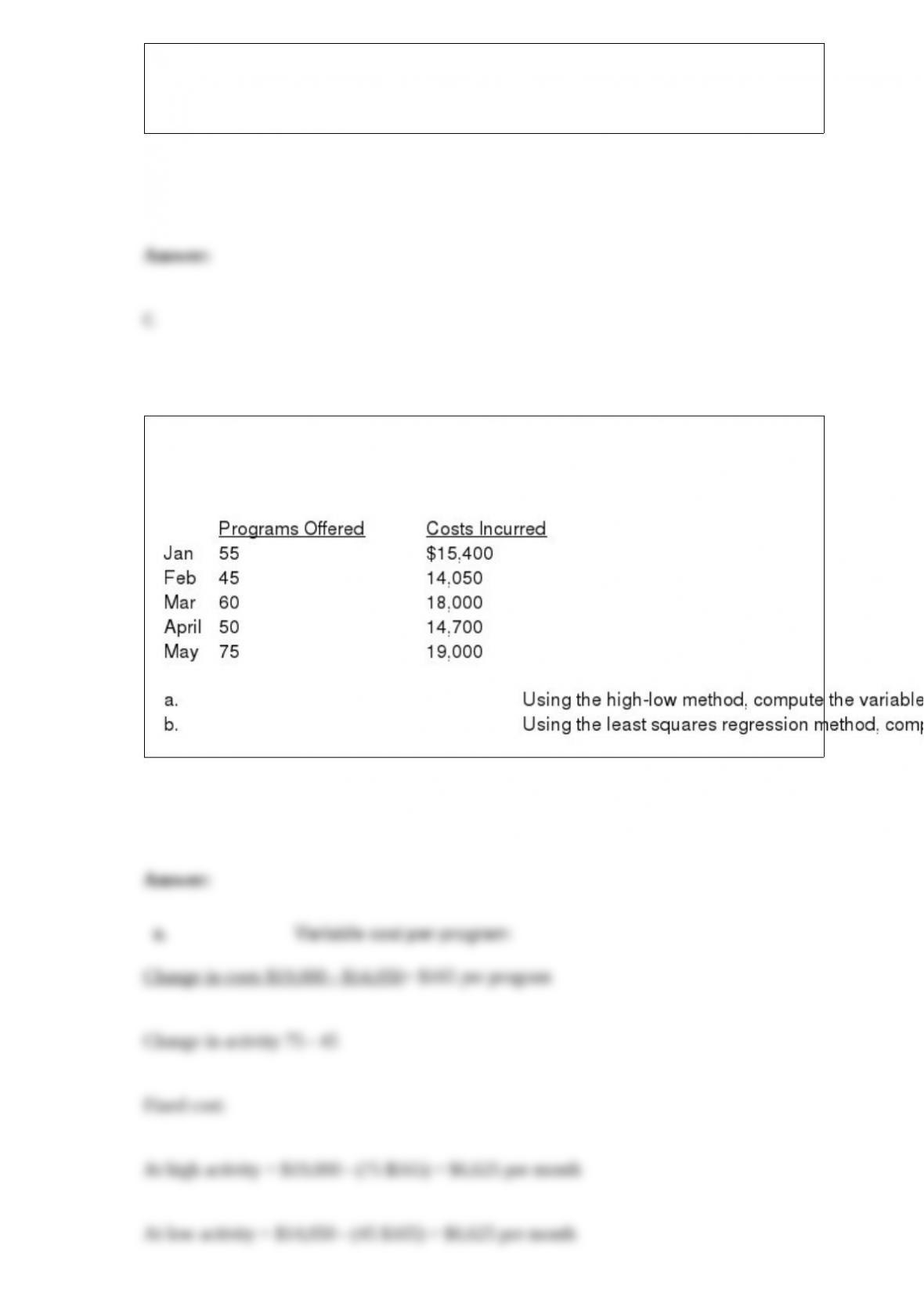

Dollarwise Trainers provides a personalized training program that is popular with many

companies. The number of programs offered over the last five months, and the costs of

offering these programs are as follows:

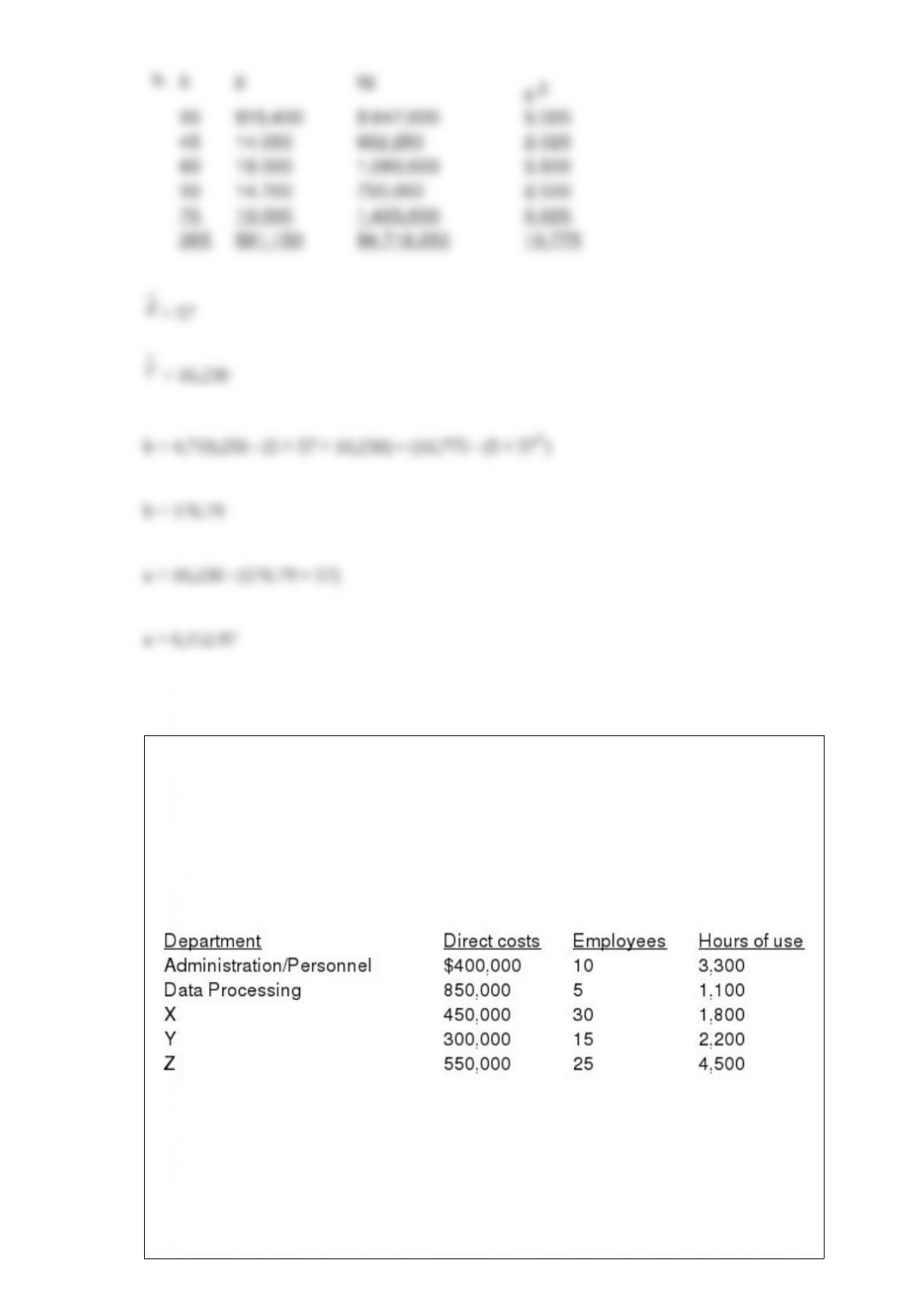

Crosby Corporation

Crosby Corporation has two service departments: Data Processing and

Administration/Personnel. The company also has three divisions: X, Y, and Z. Data

Processing costs are allocated based on hours of use and Administration/Personnel costs

are allocated based on number of employees.

Assume that Data Processing provides more service than Administration/Personnel.

Refer to Crosby Corporation. Using the direct method, what amount of Data Processing

costs is allocated to Y (round to the nearest dollar)?

a. $158,475

b. $0

c. $220,000

d. $103,529

Costs forgone when an individual or organization chooses one option over another are

a. budgeted costs.

b. sunk costs.

c. historical costs.

d. opportunity costs.

In a standard cost system, Work in Process Inventory is ordinarily debited with

a. actual costs of material and labor and a predetermined overhead cost for overhead.

b. standard costs based on the level of input activity (such as direct labor hours

worked).

c. standard costs based on production output.

d. actual costs of material, labor, and overhead.

Annual after-tax corporate net income can be converted to annual after-tax cash flow by

a. adding back the depreciation amount.

b. deducting the depreciation amount.

c. adding back the quantity (t depreciation deduction), where t is the corporate tax rate.

d. deducting the quantity [(1- t) depreciation deduction], where t is the corporate tax

rate.

All of the following objectives are reasons to allocate service department costs to

compute full cost except to

a. provide information on cost recovery.

b. abide by regulations that may require full costing in some instances.

c. provide information on controllable costs.

d. reflect production’s “fair share” of costs.

Which of the following costing methods is the most effective in controlling a product’s

total life-cycle cost?

a. kaizen costing

b. target costing

c. standard costing

d. process costing

Hickman Company uses a FIFO process costing system. The company had 6,000 units

that were 75 percent complete as to conversion costs at the beginning of the month. The

company started 25,000 units this period and had 8,000 units in ending Work in Process

Inventory that were 40 percent complete as to conversion costs. What are equivalent

units for material, if material is added at the beginning of the process?

a. 18,500

b. 25,000

c. 26,500

d. 31,000

In relationship to changes in activity, fixed overhead changes

a. yes yes

b. no no

c. no yes

d. yes no

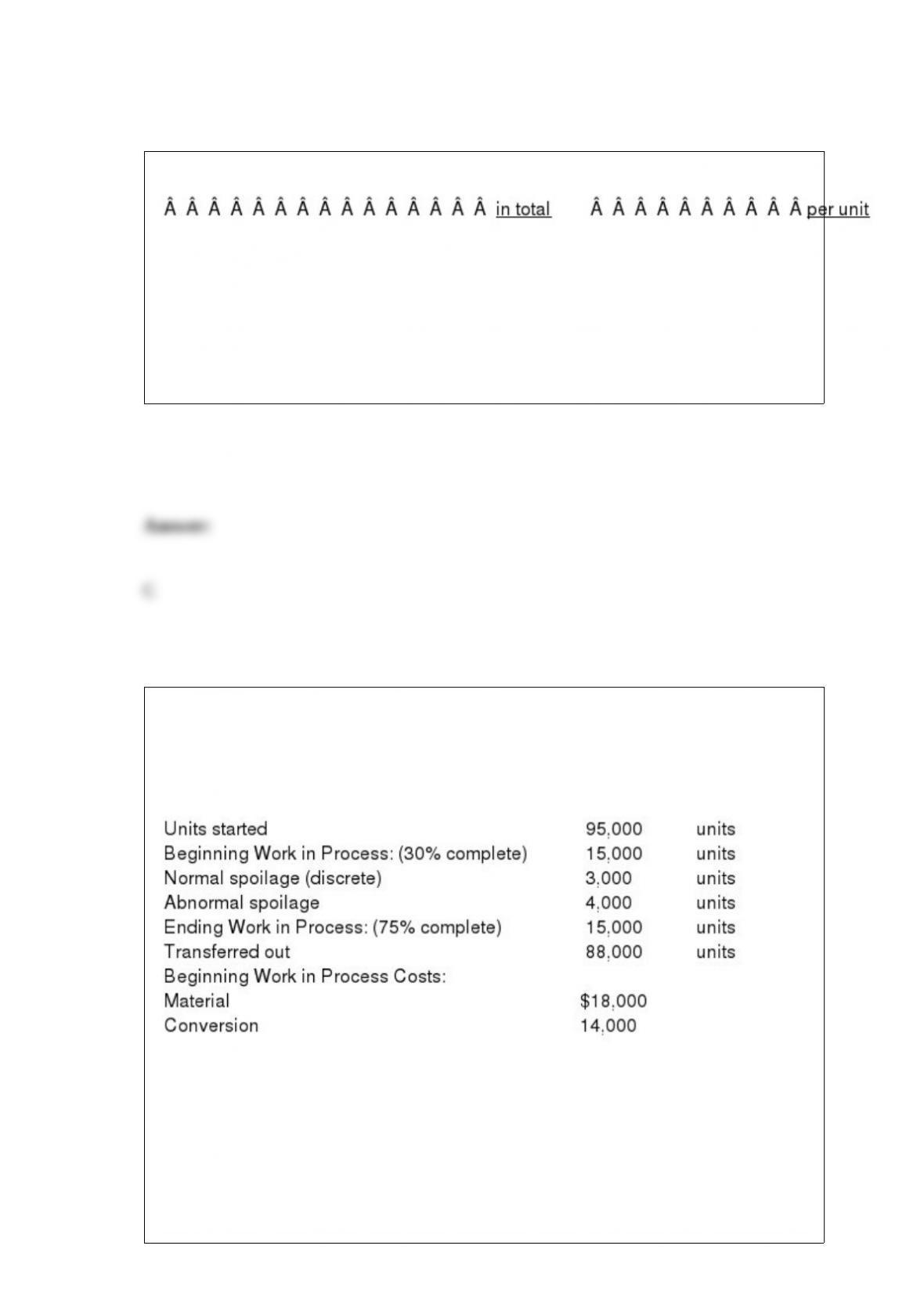

Andersen Corporation

Andersen Corporation has the following information for the current month:

All materials are added at the start of the production process. Andersen Corporation

inspects goods at 75 percent completion as to conversion.

Refer to Andersen Corporation. What are equivalent units of production for material

assuming weighted average is used?

a. 105,500

b. 106,000

c. 107,000

d. 110,000

An organization plans to produce and sell 50,000 units. It actually produces and sells

45,000 units. Total costs would be expected to be below the planned level due to cost

a. consciousness.

b. control.

c. reductions.

d. behavior.

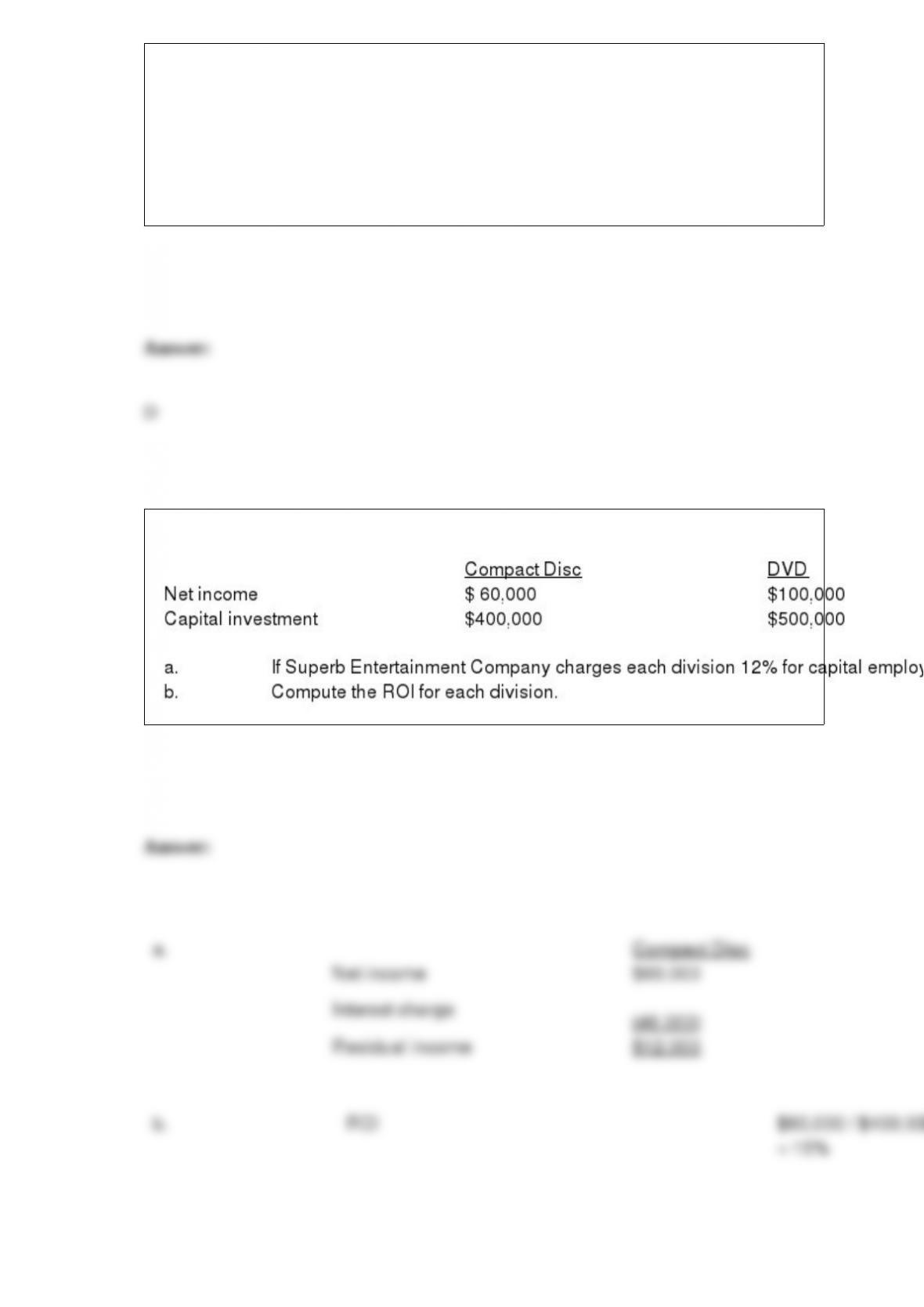

Information for two divisions of Superb Entertainment Company is given below:

Managers may be more willing to accept a budget if

a. it is continuous.

b. it is imposed.

c. it is very hard to attain.

d. they can participate in its development.

Data mining

a. is packaged software.

b. is a method of examining processes.

c. uses statistical techniques to solve problems.

d. is a way to downsize.

The total labor variance can be subdivided into all of the following except

a. rate variance.

b. yield variance.

c. learning curve variance.

d. mix variance.

Incremental separate costs are defined as all costs incurred between ____ and the point

of sale.

a. inception

b. split-off point

c. transfer to finished goods inventory

d. point of addition of disposal costs

Sullivan Company

Sullivan Company is preparing its Manufacturing Overhead budget for the second

quarter of the year. Budgeted variable factory overhead is $3.00 per unit produced;

budgeted fixed factory overhead is $75,000 per month, with $16,000 of this amount

being factory depreciation.

Refer to Sullivan Company. If the budgeted production for April is 6,000 units, then the

total budgeted factory overhead for April is:

a. $77,000

b. $82,000

c. $85,000

d. $93,000

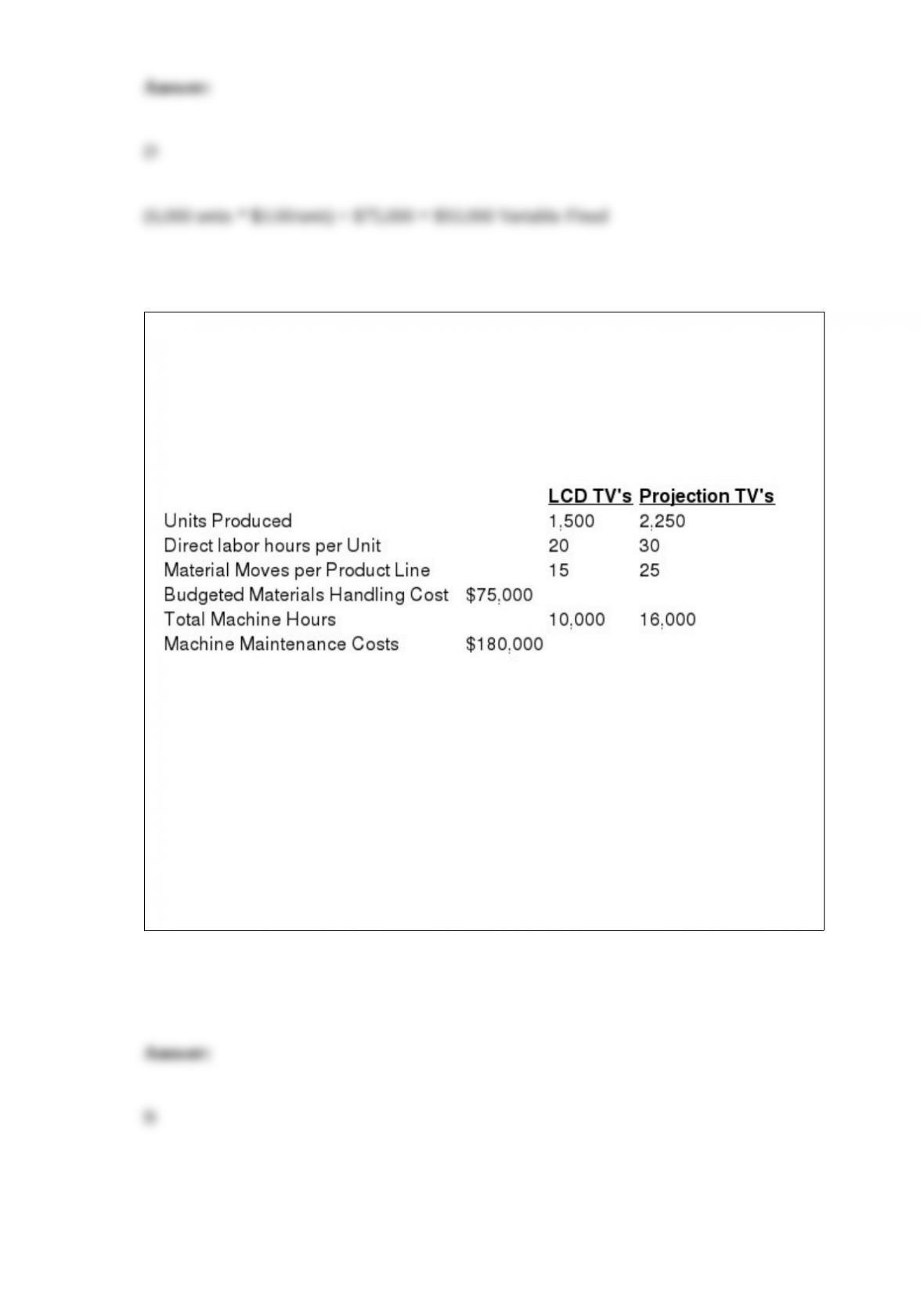

Ultimate Vision Corporation

Ultimate Vision Corporation has two product lines: LCD televisions and projection

televisions. The company has budgeted the following production and overhead costs for

the upcoming year:

Refer to Ultimate Vision Corporation. If the company uses an activity-based costing

(ABC) system to allocate factory overhead, the materials handing cost allocated to LCD

TVs would be:

a. $23,077

b. $28,125

c. $30,000

d. $45,000

The variance least significant for purposes of controlling costs is the

a. material quantity variance.

b. variable overhead efficiency variance.

c. fixed overhead spending variance.

d. fixed overhead volume variance.

The source document that records the amount of raw material that has been requested

by production is the

a. job-order cost sheet.

b. bill of lading.

c. interoffice memo.

d. material requisition.

Profit under absorption costing may differ from profit determined under variable

costing. How is this difference calculated?

a. Change in the quantity of all units in inventory times the relevant fixed costs per unit.

b. Change in the quantity of all units produced times the relevant fixed costs per unit.

c. Change in the quantity of all units in inventory times the relevant variable cost per

unit.

d. Change in the quantity of all units produced times the relevant variable cost per unit.

Costs incurred to correct defects in products after shipment are referred to as

________________________________________.

The assumed range of activity that reflects the company’s normal operating range is

referred to as the ______________________________.

The internal business perspective of the balanced scorecard addresses stakeholder

concerns about profitability and organizational growth.

A chart that indicates each step in a production process is referred to as a

_________________________.

A one-variance approach calculates only a total overhead variance.

Statistical data about the steps that will create the results desired as referred to as

___________________________________.

The amount of revenue that differs across decision choices is referred to as

______________________________.

The learning and growth perspective of the balanced scorecard focuses on using an

organization’s intellectual capital to adapt to or influence customer needs and

expectations.

On what needs do (1) management accounting and (2) financial accounting focus?

When management by exception is employed, favorable variances should notbe

investigated.

Discuss how establishing standards benefits the following management functions:

performance evaluation and decision making.

A series of activities that when performed together satisfy a specific objective is

referred to as a ____________________.

Inspection of incoming inventory is a value-added activity.

In a manufacturing organization, the budget that is prepared after the sales budget is the

______________________________.