1) When the amount in the petty cash account is immaterial, most auditors would

choose to test the account for reasons of client expectations.

A) True

B) False

2) When preparing a standard inquiry of client’s attorney letter, the client’s letterhead

should be used, and the letter should be signed by the client company’s officials.

A) True

B) False

3) CPAs must be independent to issue a review report.

A) True

B) False

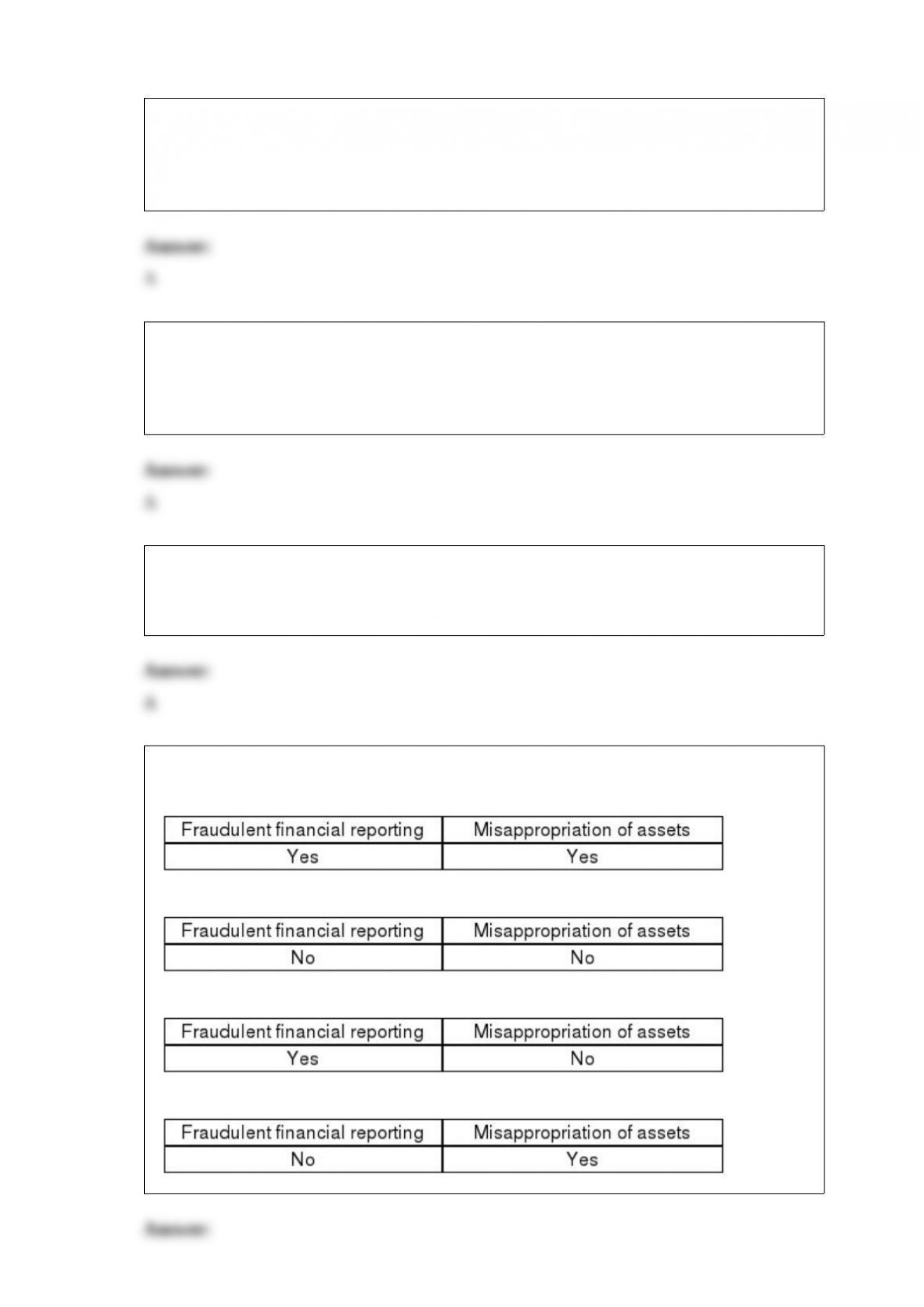

4) Which of the following is a category of fraud?

A)

B)

C)

D)

5) PPS samples can be obtained in an efficient manner using all but which of the

following?

A) hand selection by the auditor

B) computer software

C) random number tables

D) systematic sampling techniques

6) The auditors primary purpose in auditing the client’s system of internal control over

financial reporting is:

A) to prevent fraudulent financial statements from being issued to the public

B) to evaluate the effectiveness of the company’s internal controls over all relevant

assertions in the financial statements

C) to report to management that the internal controls are effective in preventing

misstatements from appearing on the financial statements

D) to efficiently conduct the Audit of Financial Statements

7) Illegal acts are defined in auditing standards as:

A) violations of laws or government regulations

B) violations of laws or government regulations other than errors

C) violations of laws or government regulations other than fraud

D) violations of law which would result in the arrest of the perpetrator

8) In the audit of historical financial statements, what accounting criteria is most

common?

A) Regulatory accounting principles

B) International financial reporting standards

C) Generally accepted accounting principles

D) B and C

E) All of the above

9) Which of the following statements regarding prospective financial statements is most

correct?

A) CPA’s are not attesting to the accuracy of the prospective financial statements

B) CPA’s are attesting to the accuracy of the prospective financial statements

C) CPA’s are performing a review on the company’s assumptions and hypothetical’s that

underlie the prospective financial statements

D) CPA’s are performing a review on the achievability of the prospective financial

statements

10) When the client fails to make adequate disclosure in the body of the statements or in

the related footnotes, it is the responsibility of the auditor to:

A) inform the reader that disclosure is not adequate, and to issue an adverse opinion

B) inform the reader that disclosure is not adequate, and to issue a qualified opinion

C) present the information in the audit report and issue an unqualified or qualified

opinion

D) present the information in the audit report and to issue a qualified or an adverse

opinion

11) Auditors usually obtain information about general and application controls through:

A) interviews with IT personnel

B) examination of systems documentation

C) reading program change requests

D) all of the above methods

12) Audit procedures related to contingent liabilities are initially focused on:

A) accuracy

B) completeness

C) existence

D) occurrence

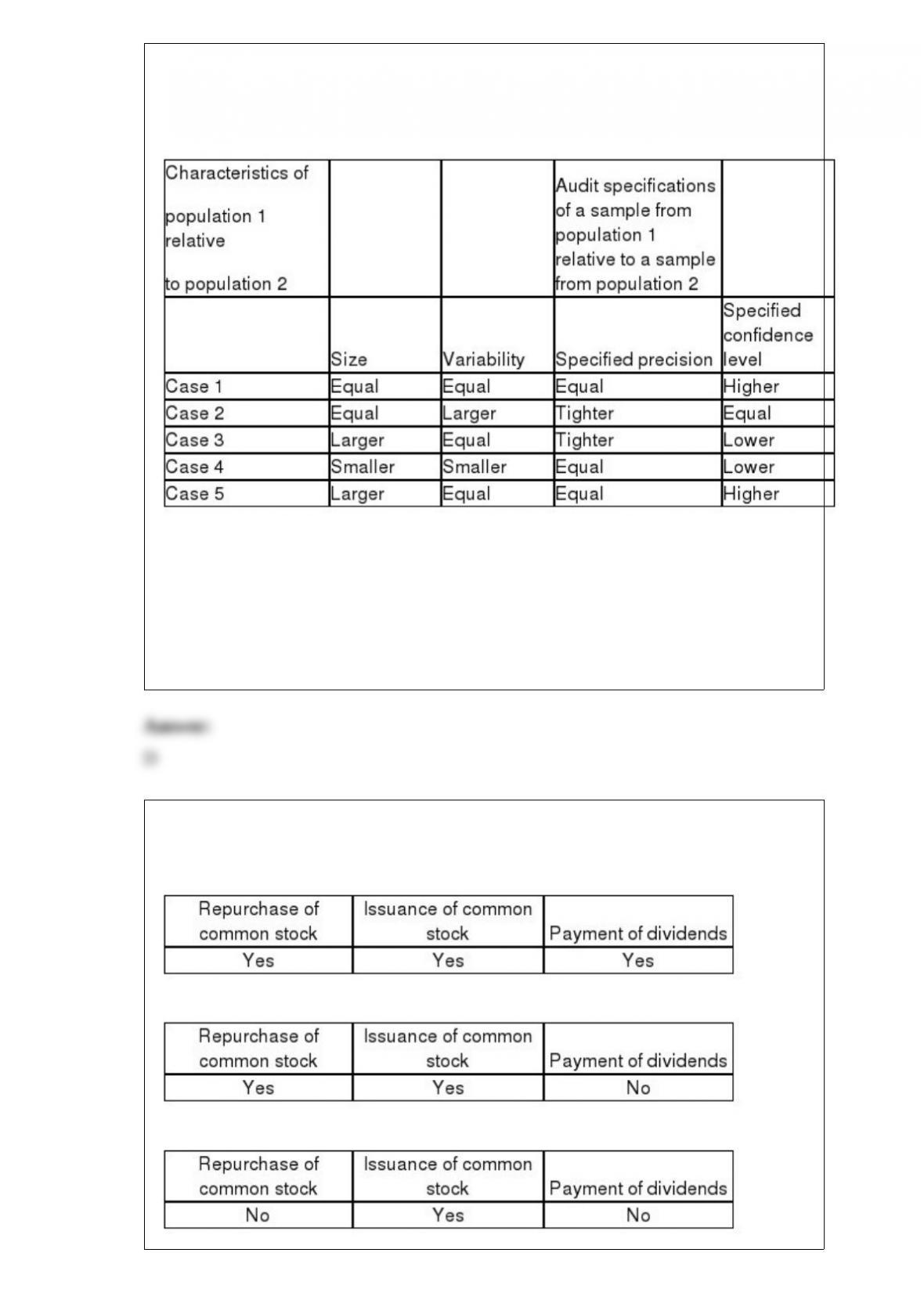

13) An audit partner is developing an office-training program to familiarize his

professional staff with statistical decision models applicable to the audit of dollar-value

balances. He wishes to demonstrate the relationship of sample sizes to population size

and variability and the auditor’s specifications as to precision and confidence level. The

partner prepared the following table to show comparative population characteristics and

audit specifications of two populations.

Based on the information presented above, you are to indicate for the specified case

from the table the required sample size to be selected from population 1 relative to the

sample from population 2 . In case 3, the required sample from population 1 is:

A) larger than the required sample size from population 2

B) equal to the required sample size from population 2

C) smaller than the required sample size from population 2

D) indeterminate relative to the required sample size from population 2

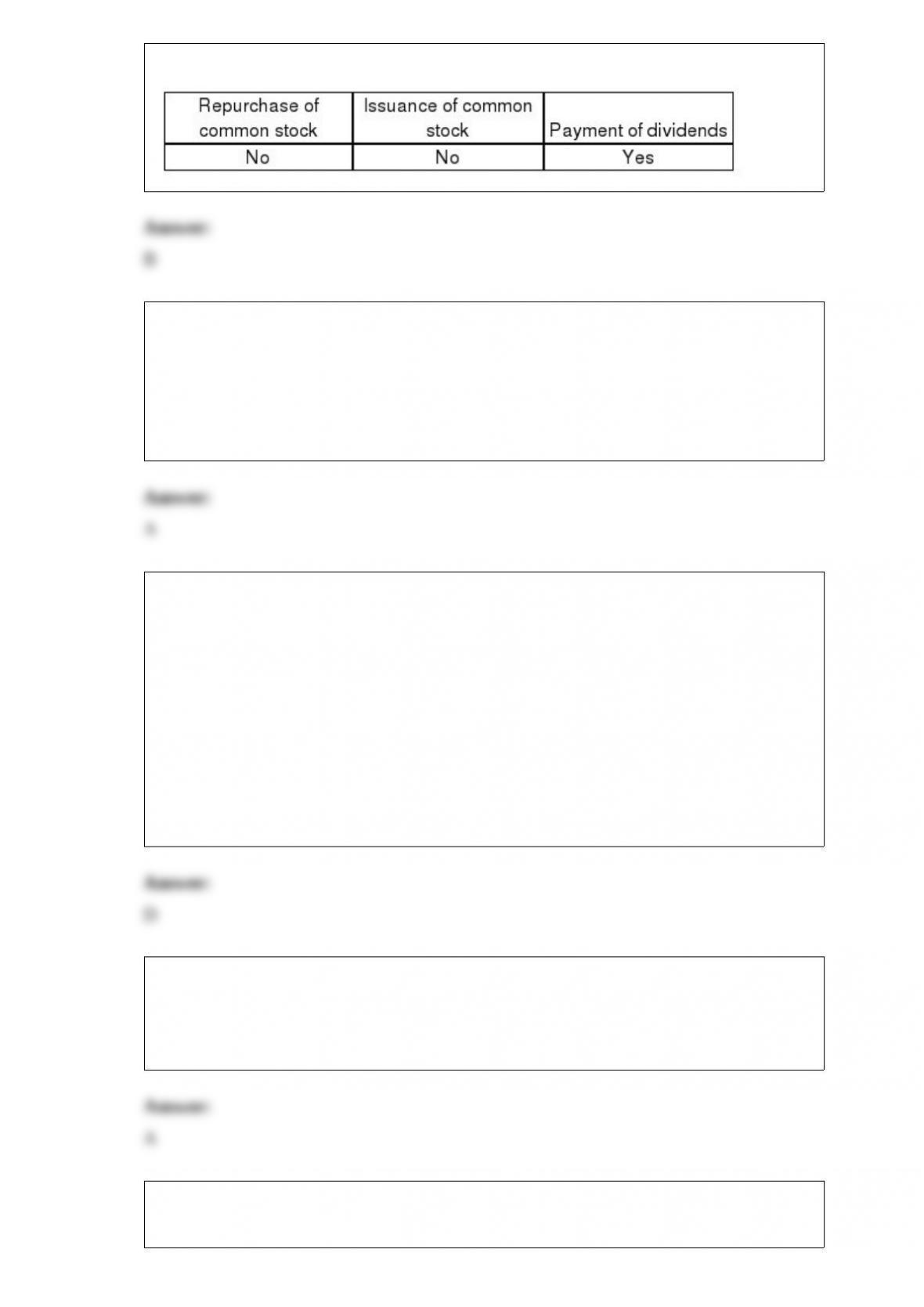

14) Which of the following owners’ equity transactions usually require specific

authorization from a company’s board of directors?

A)

B)

C)

D)

15) The primary difference between an audit of the balance sheet and an audit of the

income statement is that the audit of the income statement deals with the verification of:

A) transactions

B) balances

C) costs

D) cutoffs

16) Which of the following is an effective internal accounting control used to prove that

production department employees are properly validating payroll time cards at a

time-recording station?

A) Internal auditors should make observations of distribution of paychecks on a

surprise basis

B) Time cards should be carefully inspected by those persons who distribute pay

envelopes to the employees

C) One person should be responsible for maintaining records of employee time for

which salary payment is not to be made

D) Daily reports showing time charged to jobs should be approved by the supervisor

and compared to the total hours worked on the employee time cards

17) An acquisitions transaction file is a computer generated file that includes all

information entered into the system regarding acquisition transactions.

A) True

B) False

18) Which of the following audit tests would provide evidence regarding the

balance-related audit objective of existence for an audit of notes payable?

A) Examine due dates on duplicate copies of notes

B) Examine balance sheet for proper presentation and disclosure of notes payable

C) Examine corporate minutes for loan approval

D) Foot the notes payable list for notes payable and accrued interest

19) The financial statements may not correctly reflect accounting frameworks such as

AAP or IFRS if the:

A) controls affecting the reliability of financial reporting are inadequate

B) company’s controls do not promote efficiency

C) company’s controls do not promote effectiveness

D) company’s controls do not promote compliance with applicable rules and regulations

20) Subsequent to the close of Spacely Sprockets fiscal year ending October 31, 2012, a

major debtor has declared bankruptcy due to a series of events. The receivable is

significantly material in relation to the financial statements, and recovery is doubtful.

The debtor had confirmed the full amount due to Spacely Sprocket at the balance sheet

date. Because the account was confirmed at the balance sheet date, Spacely refuses to

disclose any information in relation to this subsequent event. The CPA believes that all

other accounts were stated fairly at the balance sheet date. In addition, Spacely changed

their method of inventory valuation from FIFO to LIFO. This change was disclosed in

Note X to the financial statements. Accordingly, what type of opinion should be

expressed?

A) Unqualified with an explanatory paragraph

B) Qualified due to a GAAP departure

C) Qualified due to a scope limitation

D) A combination of B and C

21) A CPA firm normally uses one or a combination of four defenses when there are

legal claims by clients. Which one of the following is generally not a defense?

A) Lack of duty

B) Non-negligent performance

C) Contributory negligence

D) Foreseeable users

22) Fraud is more prevalent in smaller businesses and not-for-organizations because it

is more difficult for them to maintain:

A) adequate separation of duties

B) adequate compensation

C) adequate financial reporting standards

D) adequate supervisory boards

23) A typical objective of an operational audit is to determine whether an entity’s:

A) internal control is adequately operating as designed

B) financial statements present fairly the results of operations

C) specific operating units are functioning efficiently and effectively

D) operational information is in accordance with generally accepted government

auditing standards

24) If the preliminary judgment of materiality increases, the amount of audit evidence

required will decrease.

A) True

B) False

25) In auditing debits and credits to retained earnings, OTHER than net income and

dividends, the auditors first concern is:

A) whether the transactions should have been included in retained earnings

B) whether the transactions have been accurately recorded

C) whether the transactions are classified correctly in the footnotes

D) whether the transactions existed as of the balance sheet date

26) Which one of the following is not one of the three General Standards?

A) Proper planning and supervision

B) Independence of mental attitude

C) Adequate training and proficiency

D) Due professional care

27) Current professional auditing standards allow external auditors to use internal

auditors for direct assistance on external audits.

A) True

B) False

28) When there is uncertainty about a company’s ability to continue as a going concern,

the auditor’s concern is the possibility that the client may not be able to continue its

operations or meet its obligations for a “reasonable period of time.” For this purpose, a

reasonable period of time is considered not to exceed:

A) six months from the date of the financial statements

B) one year from the date of the financial statements

C) six months from the date of the audit report

D) one year from the date of the audit report

29) If the perpetual inventory master files show lower quantities of inventory than the

physical count, an explanation of the difference might be unrecorded:

A) sales

B) sales discounts

C) purchases

D) purchase discounts

30) The test data approach requires the auditor to insert an audit module in the client’s

application system to test how transaction data is processed.

A) True

B) False

31) Which one of the following is not true regarding the American Institute of Certified

Public Accountants peer review requirement?

A) A CPA firm must develop and adhere to quality control standards

B) Peer reviews are mandatory

C) A CPA firm will lose

D) Firms required to be registered with and inspected by the PCAOB are exempt

32) A sample in which every possible combination of items in the population has an

equal chance of constituting the sample is a:

A) random sample

B) statistical sample

C) judgment sample

D) representative sample

33) In the audit of notes payable, it is common to include tests of principal and interest

payments as a part of the audit of the acquisitions and payment cycle because the

payments are in the cash disbursements journal that is being sampled. It is also normal

to test these transactions as part of the capital acquisitions and repayment cycle

because:

A) it is not unusual for the auditor to duplicate a process, thereby gathering a larger

quantity of evidence

B) replicating the evidence will provide the auditor with a higher level of assurance

C) the tests done in the acquisitions and payments cycle will look only at the cash credit

side so the tests done in the capital acquisitions and repayment cycle will look at the

debit side of the transaction

D) due to the infrequency of these transactions, in many cases no transactions involving

notes payable are included in the sample tests of acquisitions and payments

34) If tests of controls and substantive tests of transactions related to perpetual

inventory records reveal controls over perpetuals are effective, the auditor is justified in

reducing the extent of tests of details of inventory.

A) True

B) False

35) In a review service where the client has failed to follow GAAP, the accountant is:

A) not required to determine the effect of a departure if management has not done so,

but that fact must be disclosed in the report

B) required to determine the effect of a departure if management has not done so, and

that fact must be disclosed in the report

C) not required to determine the effect of a departure if management has not done so,

and that fact need not be disclosed in the report

D) required to determine the effect of a departure if management has not done so, and

that fact need not be disclosed in the report

36) The organization that is responsible for providing oversight for auditors of public

companies is called the ________.

A) Auditing Standards Board

B) American Institute of Certified Public Accountants

C) Public Oversight Board

D) Public Company Accounting Oversight Board

37) Julie and Lisa are sisters. Julie is a CPA auditing the company where Lisa works.

Julie’s independence is impaired if:

A) Lisa is the controller

B) Lisa owns 25% of the company

C) Lisa is the marketing manager

D) All of the above

38) The risk that audit evidence for a segment will fail to detect misstatements

exceeding tolerable misstatement is:

A) Audit risk

B) Control risk

C) Inherent risk

D) Planned detection risk

39) Which of the following procedures would most likely be performed in response to

the auditor’s assessment of the risk of monetary misstatements in the financial

statements?

A) Ratio analysis

B) Tests of controls

C) Tests of details of balances

D) Risk assessment procedures