Managers face ethical situations on a daily basis, while accountants face them

infrequently.

Answer:

The budget (or spending) variance for fixed production costs is the difference between

the actual fixed costs and the budgeted fixed costs on the master budget.

Answer:

It is more important for financial accounting information to be comparable between

firms than to be useful for managerial decision-making.

Answer:

The full cost fallacy occurs when a decision-maker fails to include fixed manufacturing

overhead in the product’s cost.

Answer:

Service organizations generally use the same job costing procedures as manufacturers.

Answer:

With constrained resources, the important measure of profitability is the contribution

margin per unit of scarce resource.

Answer:

A favorable variance is not necessarily good, and an unfavorable variance is not

necessarily bad.

Answer:

One reason financial measures are used to evaluate performance is that they are easily

quantifiable.

Answer:

The profit margin ratio is computed by dividing after-tax operating income by sales.

Answer:

Storing materials, work-in-process items, and finished goods in inventory are essential,

value-added activities in most companies.

Answer:

Accounting systems typically record opportunity costs as assets and treat them as

intangible items on the financial statements.

Answer:

Manufacturing cycle time is the total time involved in processing, moving, storing, and

inspecting a good or providing a service.

Answer:

The basic cost flow model applies only to physical units and not to costs.

Answer:

The weighted-average approach to process costing combines the work and costs done

in prior periods with the work and costs done in the current period.

Answer:

A basic assumption of most cost estimation methods is cost behavior patterns are linear

within the relevant range.

Answer:

Cost accounting information developed for managers to use in making decisions must

comply with generally accepted accounting principles (GAAP).

Answer:

Only variable costs can be differential costs.

Answer:

Individual product costs are relevant for managerial decision-making but irrelevant for

preparing the financial statements.

Answer:

The primary goal of the cost accounting system is to provide managers with

information to prepare their annual financial statements.

Answer:

Decentralization is the delegation of the authority to make decisions in the

organization’s name to subordinates.

Answer:

The Delphi technique uses highly sophisticated computerized time series analysis to

reduce the subjectivity surrounding the sales forecast.

Answer:

Estimates for direct labor costs are obtained from the engineering and production

management, as well as from the Personnel Department.

Answer:

Theoretical capacity is the amount of production possible assuming expected downtime

for scheduled maintenance and normal breaks and vacations.

Answer:

Historical costs are based on the original costs to acquire a long-term asset, while

current costs represent the costs to replace the long-term asset.

Answer:

A cost of quality system is based on the trade-off between incurring costs to meet

product (or service) specifications and the costs of failing to meet those specifications.

Answer:

There is no single accounting measure that can fully measure the performance of a

profit or investment center.

Answer:

In general, accounting records accumulate cost information according to its behavior

(i.e., variable and fixed).

Answer:

Variable marketing and administrative costs are included in determining full absorption

costs.

Answer:

A job is a product or service that can be easily and conveniently distinguished from

other products/services.

Answer:

Revenue minus cost of goods sold equals contribution margin.

Answer:

Sensitivity analysis is more likely to be used for sales forecasts than for fixed overhead

costs.

Answer:

The physical quantities method allocates joint costs so that each joint product has the

same gross margin as a percentage of sales.

Answer:

Dumping occurs when a company exports its product to consumers in another country

at an export price that is below the domestic price.

Answer:

The production volume variance is the difference between fixed costs on the flexible

budget and the fixed costs on the master budget.

Answer:

The number of products produced is an example of a facility-related cost driver in the

cost hierarchy.

Answer:

Period costs are those costs assigned to units of production in the period in which they

are incurred.

Answer:

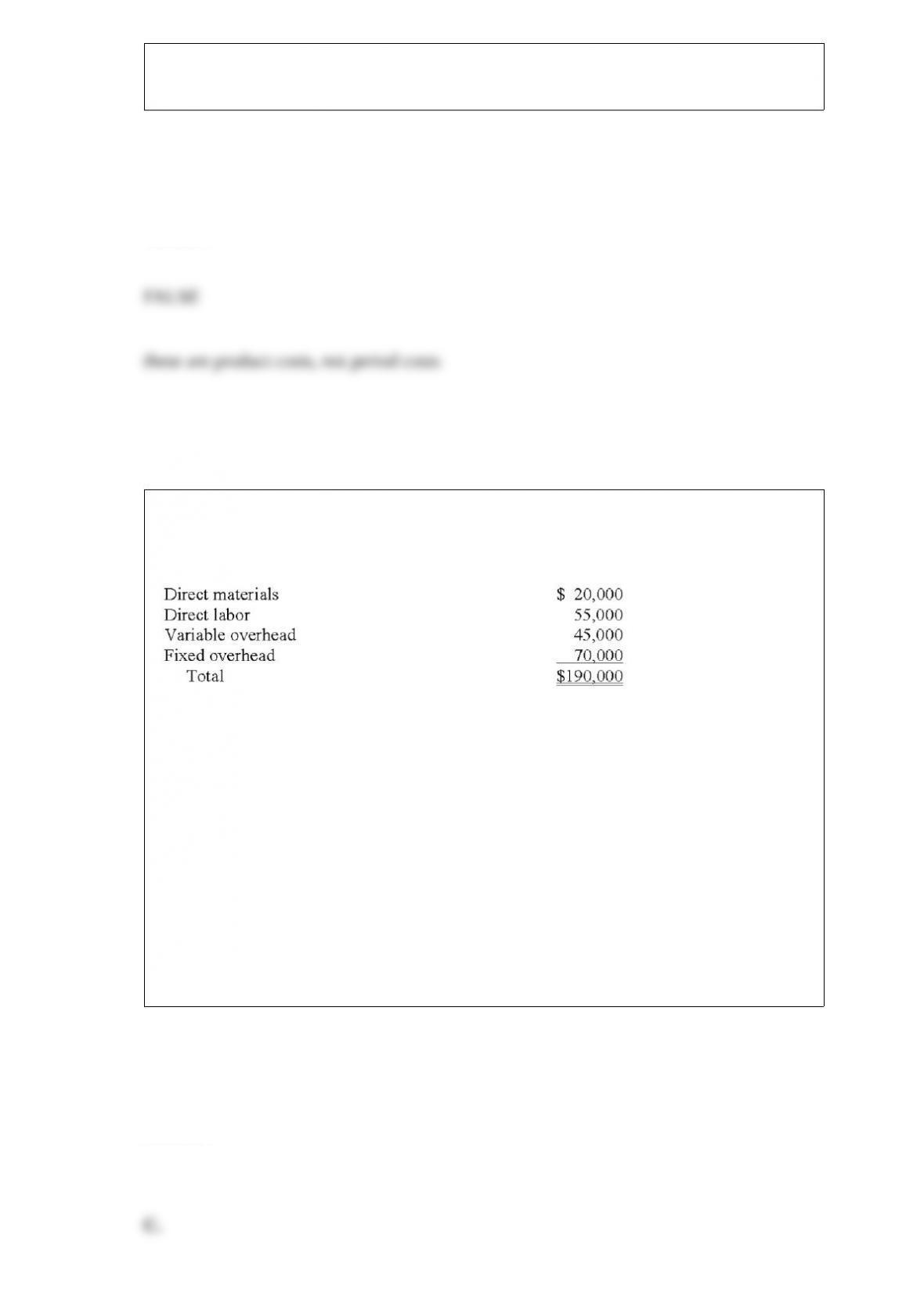

The CJP Company produces 10,000 units of item S10 annually at a total cost of

$190,000.

The XYZ Company has offered to supply 10,000 units of S10 per year for $18 per unit.

If CJP accepts the offer, $4 per unit of the fixed overhead would be saved. In addition,

some of CJP’s facilities could be rented to a third party for $15,000 per year. What are

the relevant costs for the “make” alternative?

A. $160,000

B. $165,000

C. $175,000

D. $185,000

Answer:

Which of the following statements regarding special orders is (are) false?

(A) The primary decision for special orders is determining whether the differential

revenue is greater than the differential costs associated with the order.

(B) The differential analysis approach to pricing for special orders will always lead to

underpricing in the long-run because fixed costs are not included in the analysis.

A. Only A.

B. Only B.

C. Neither A nor B is false.

D. Both A and B are true.

Answer:

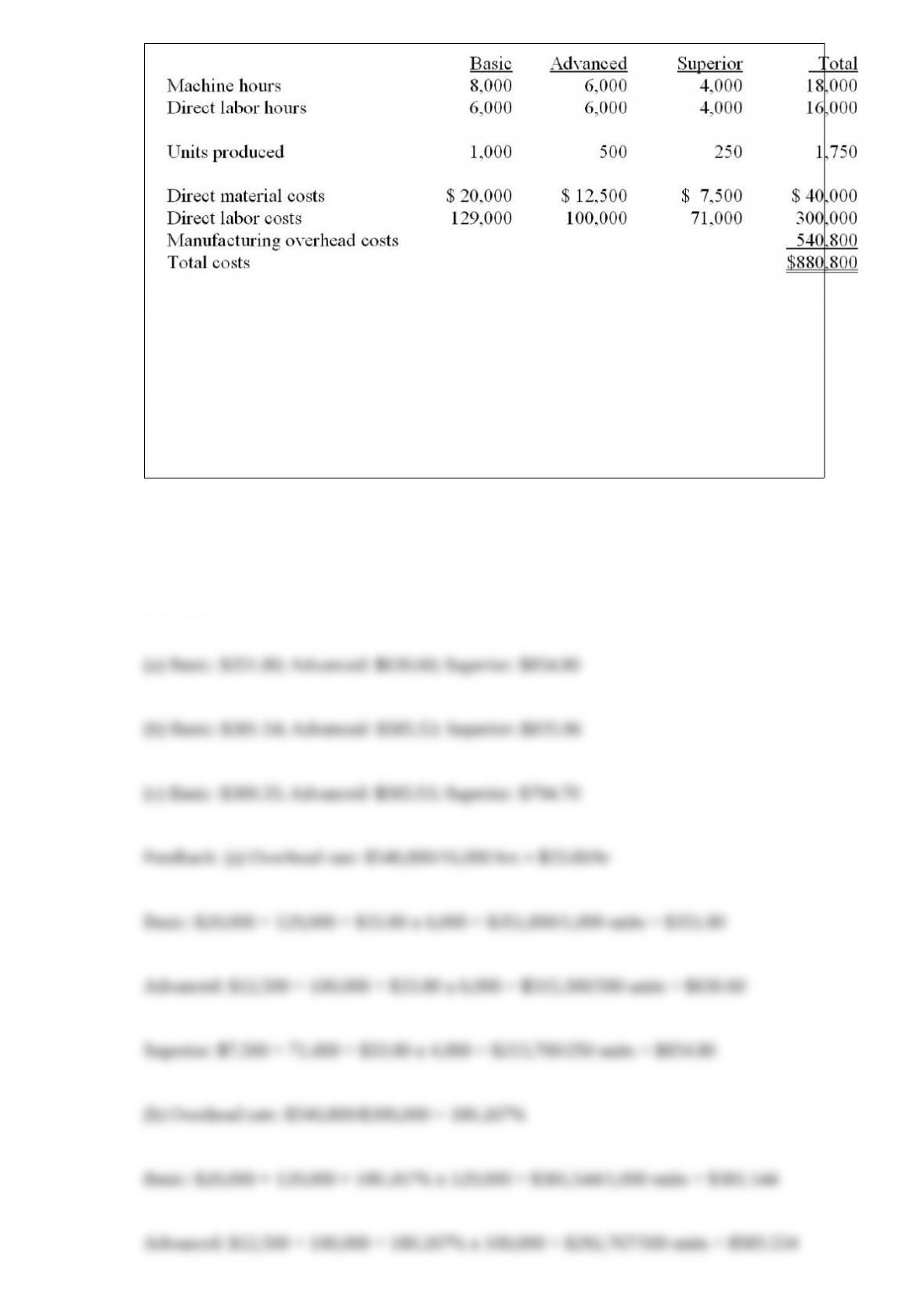

Lein Office Products produces three models of commercial shelving, the Basic, the

Advanced and the Superior. Data on operations and costs for the month are:

Required: Compute the unit cost for each model, assuming Lein Office Products uses:

(a) Direct labor hours to allocate overhead costs.

(b) Direct labor costs to allocate overhead costs.

(c) Machine hours to allocate overhead costs.

Answer:

The Update Company does not maintain backup documents for its computer files. In

June, some of the current data were lost, and you have been asked to help reconstruct

the data. The following beginning balances on June 1 are known:

Reviewing old documents and interviewing selected employees have generated the

following additional information:

The production superintendent’s job cost sheets indicated that materials of $2,600 were

included in the June 30 Work-in-Process Inventory. Also, 300 direct labor hours had

been paid at $6.00 per hour for the jobs in process on June 30.

The Accounts Payable account is only for direct material purchases. The clerk

remembers clearly that the balance in the Accounts Payable on June 30 was $8,000. An

analysis of canceled checks indicated payments of $40,000 were made to suppliers

during June.

Payroll records indicate that 5,200 direct labor hours were recorded for June. It was

verified that there were no variations in pay rates among employees during June.

Records at the warehouse indicate that the Finished Goods Inventory totaled $16,000 on

June 30.

Another record kept manually indicates that the Cost of Goods Sold in June totaled

$84,000.

The predetermined overhead rate was based on an estimated 60,000 direct labor hours

for the year and an estimated $180,000 in manufacturing overhead costs.

What is the ending balance in the Direct Materials Inventory on June 30?

A. $6,000

B. $10,500

C. $11,000

D. $15,000

Answer:

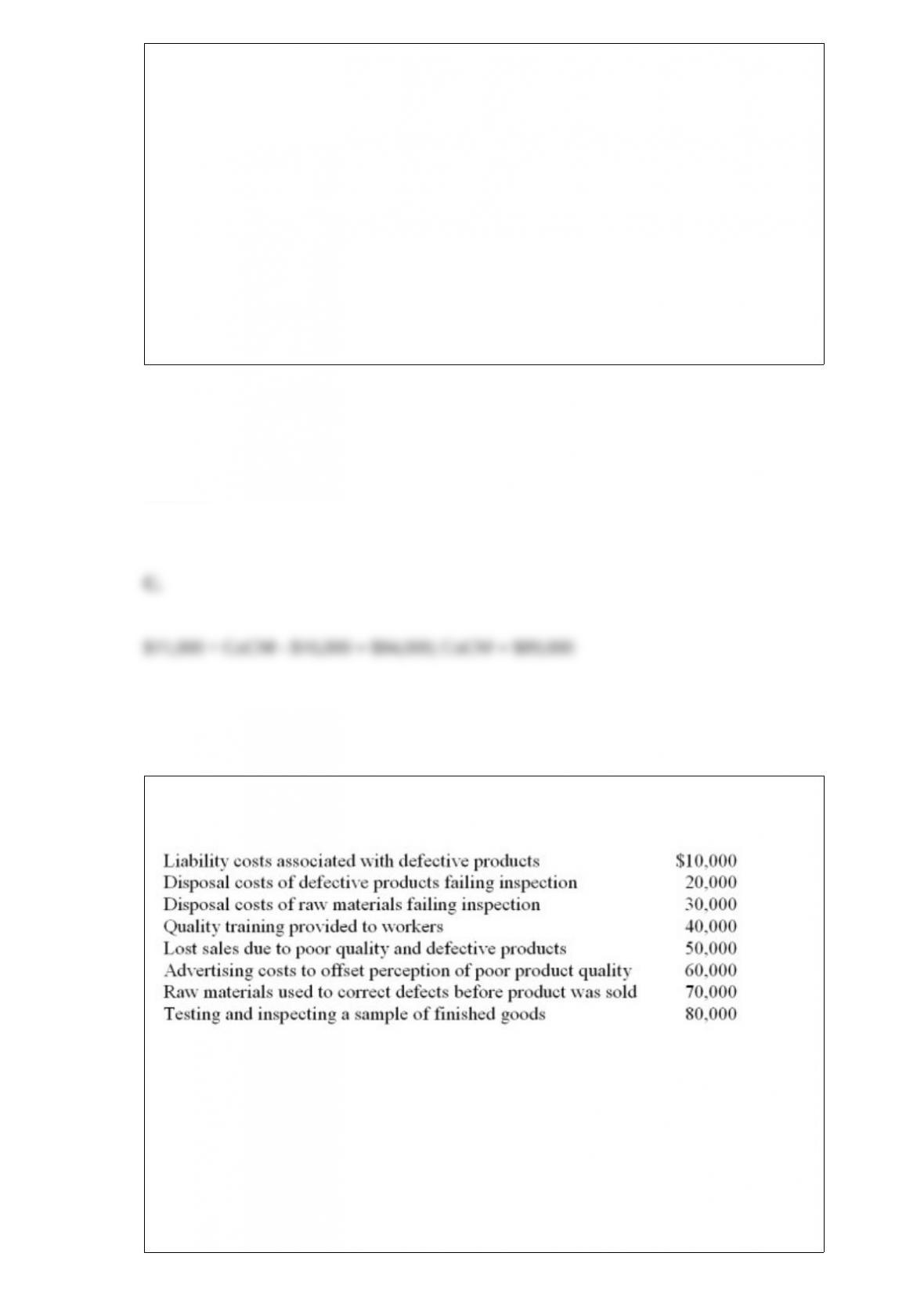

QC Enterprises quality control report for August contains the following items.

What would be the total of the internal failure costs on the August quality control report

for QC Enterprises?

A. $60,000

B. $90,000

C. $100,000

D. $120,000

Answer:

Which of the following statements is (are) true?

(1) Activity-based costs per unit are always greater than volume-based costs per unit.

(2) Volume-based costing has typically resulted in lower gross margins for high volume

products and higher gross margins for low volume products.

A. Only (1) is true.

B. Only (2) is true.

C. Both (1) and (2) are true.

D. Neither (1) nor (2) are true.

Answer:

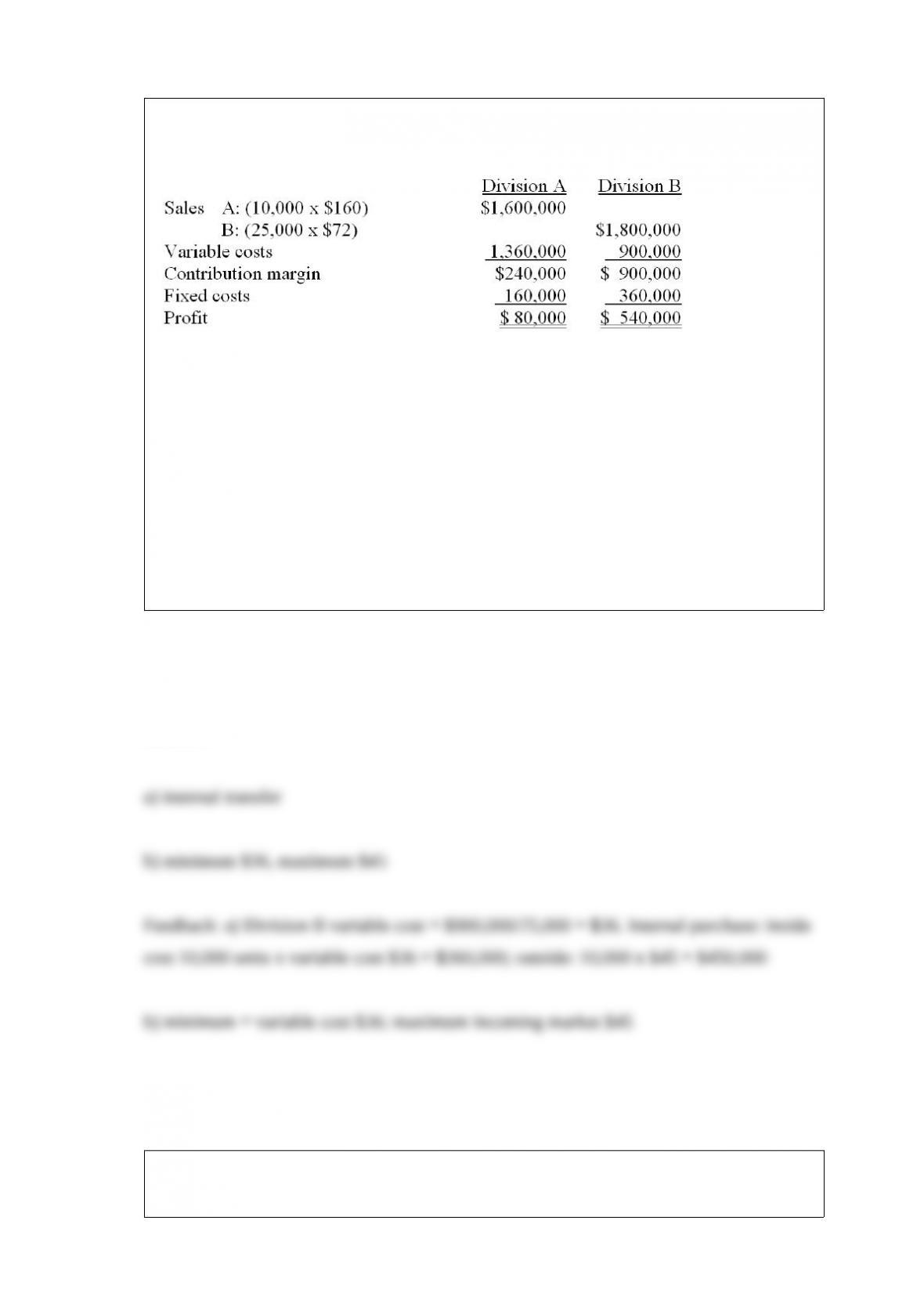

Stills Company expects the following results:

Included in Division A’s costs are 10,000 units of a subcomponent purchased from an

outside supplier for $45. The managers have recently initiated negotiations for Division

B to supply the components to Division A. Division B has a total capacity of 40,000

units.

Required:

a) Would Stills Company prefer the subcomponent used by A to be purchased internally

from B or from the outside vendor?

b) What would be the maximum and minimum transfer prices?

Answer:

Monet Co. has provided the following information for last year:

The total labor cost (rounded) is:

A. $293,325

B. $482,500

C. $468,750

D. $200,021

Answer:

Withee produces a quick setting concrete powder. Production of 15,000 tons was

started in September, 14,000 tons were completed. Material costs were $394,670 for the

month while conversion costs were $201,730. There was no beginning work-in-process;

the ending work-in-process was 20% complete.

(a) What is the total cost of the product that was completed and transferred to finished

goods?

(b) What is the value of the ending work-in-process?

Answer:

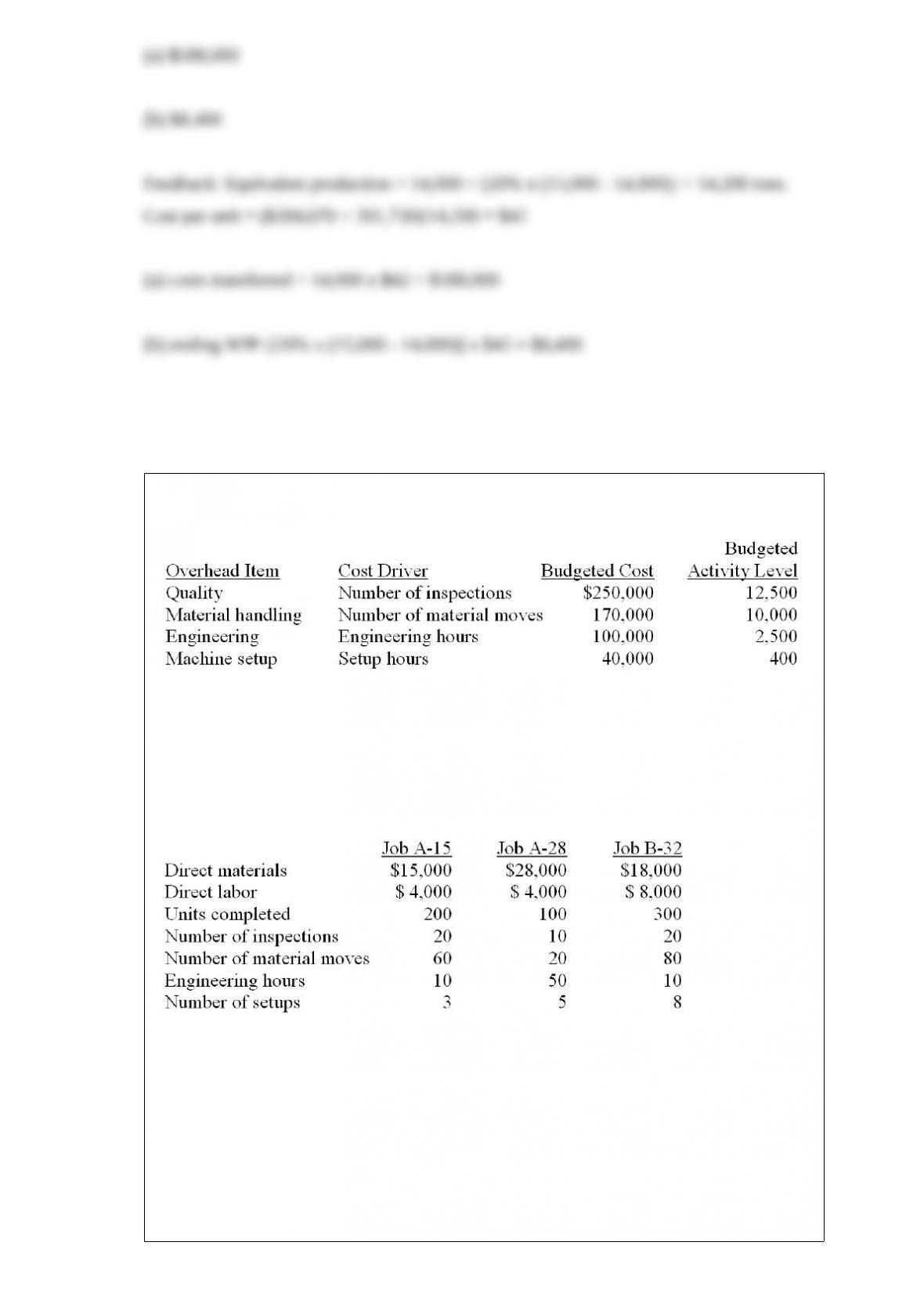

Scottso Enterprises has identified the following overhead costs and cost drivers for the

coming year:

Budgeted direct labor cost was $200,000 and budgeted direct material cost was

$800,000. The following information was collected on three jobs that were completed

during the month:

If the company uses traditional costing and allocates overhead using direct materials

cost, what is the cost of each unit of Job A-28?

A. $196.00

B. $516.00

C. $364.50

D. $352.00

Answer:

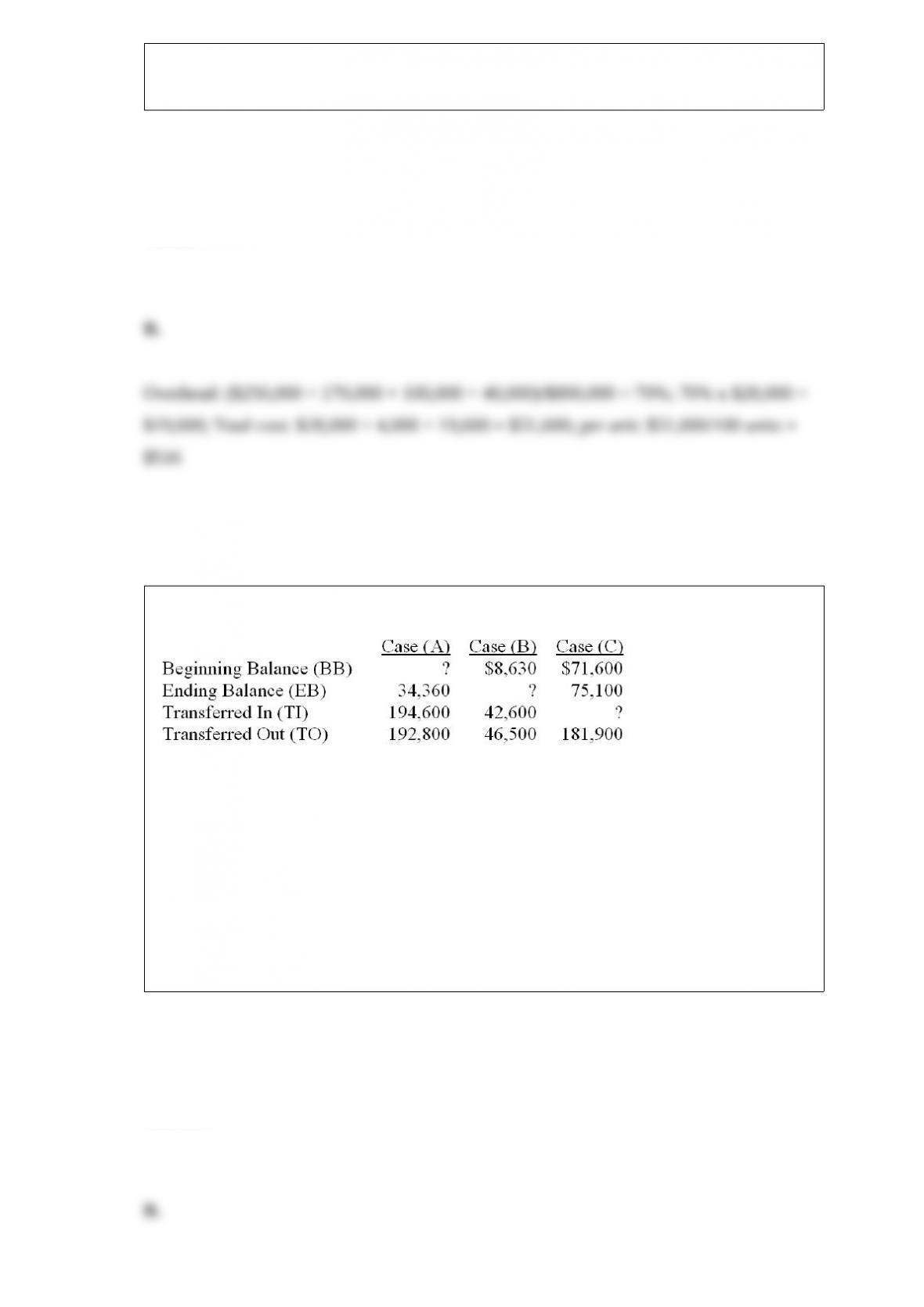

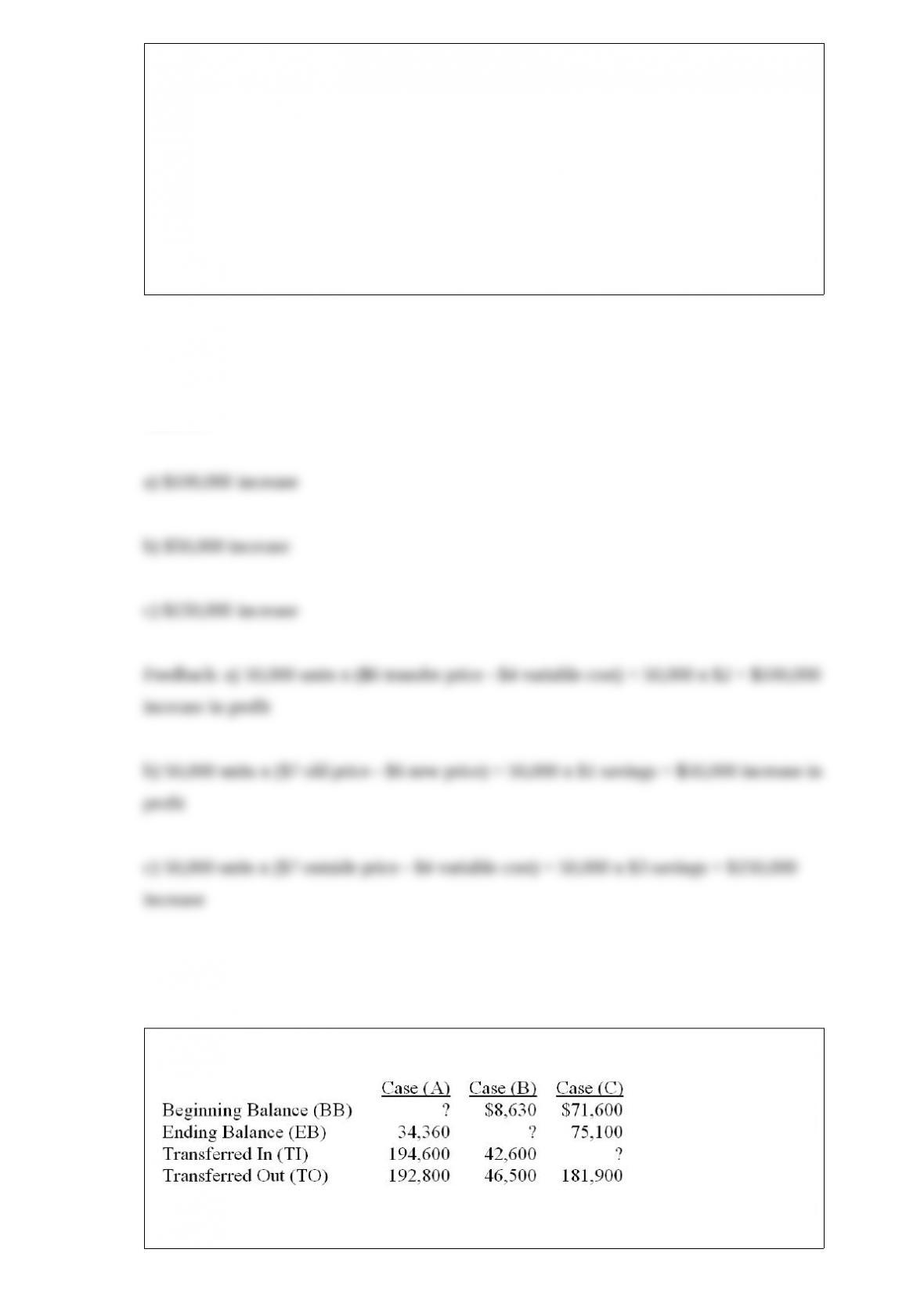

For Case (A) above, what is the Transferred-Out (TO)?

A. $185,600

B. $192,600

C. $126,100

D. $178,890

Answer:

Create a diagram of the value chain by putting the following components into the

correct order: a) purchasing; b) marketing and sales; c) research and development; d)

customer service; e) distribution; f) design; g) production.

Answer:

Rizzo Corporation had 17,000 units of brake calipers on hand at the end of 2008. The

company’s inventory policy was to maintain an ending inventory equal to 15% of the

current year’s sales. During 2009, Rizzo sold 210,000 units of calipers. How many units

did Rizzo purchase in 2009?

A. 224,500.

B. 210,000.

C. 196,150.

D. 194,700.

Answer:

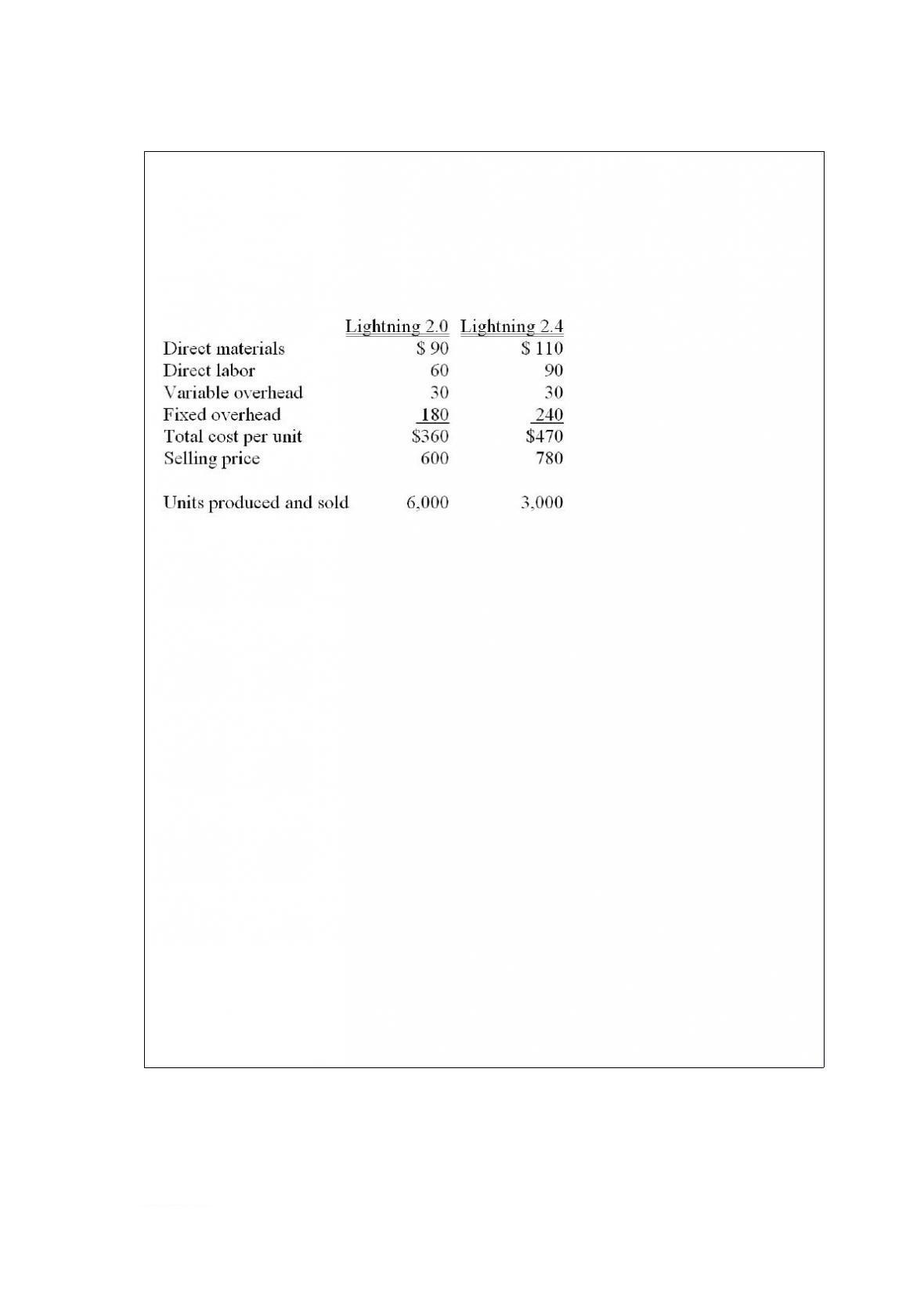

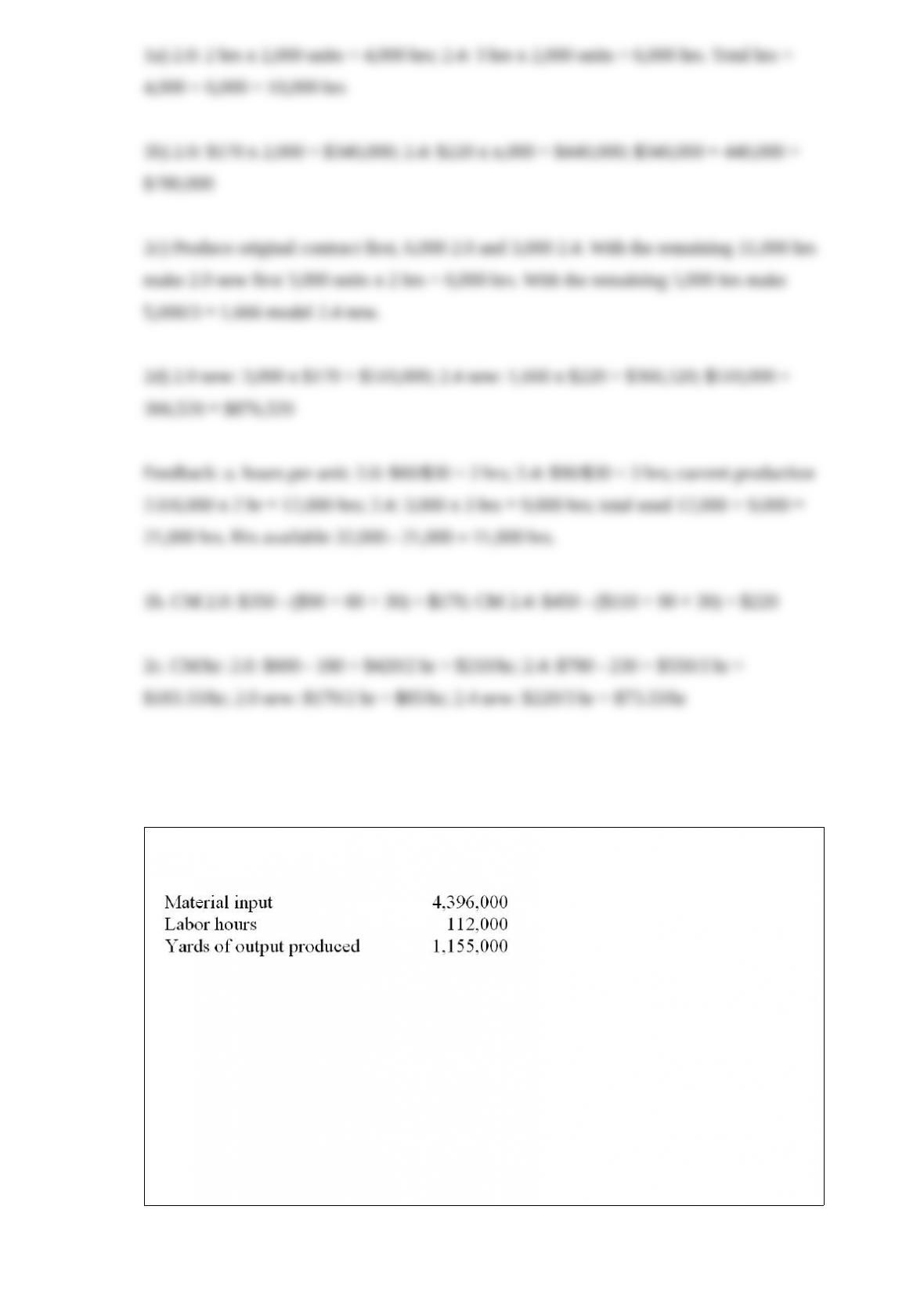

Hi-Speed Electronics manufactures low-cost, consumer-grade computers. It sells these

computers to various electronics retailers to market under store brand names. It

manufactures two computers, the Lightning 2.0 and the Lightning 2.4, which differ in

terms of speed, memory, and hard drive capacity. The following information is

available:

The average wage rate is $30 per hour. The plant has a capacity of 32,000 direct

labor-hours.

Required:

1) A nationwide discount chain has approached Hi-Speed with an offer to buy 2,000

Lightning 2.0 computers and 2,000 Lightning 2.4 computers if the price is lowered to

$350 and $450, respectively, per unit.

a) If Hi-Speed accepts the offer, how many direct labor-hours will be required to

produce the additional computers?

b) How much will the profit increase (or decrease) if Hi-Speed accepts this proposal?

All other prices will remain the same.

Suppose that the customer has offered instead to buy up to 3,000 each of the two

models at $350 and $450, respectively.

c) How many of each product should be manufactured and sold? Assume current

demand will not be affected by the special order. Also assume that the company cannot

increase its production capacity to meet the extra demand.

d) How much will the profits change if this order is accepted instead?

Answer:

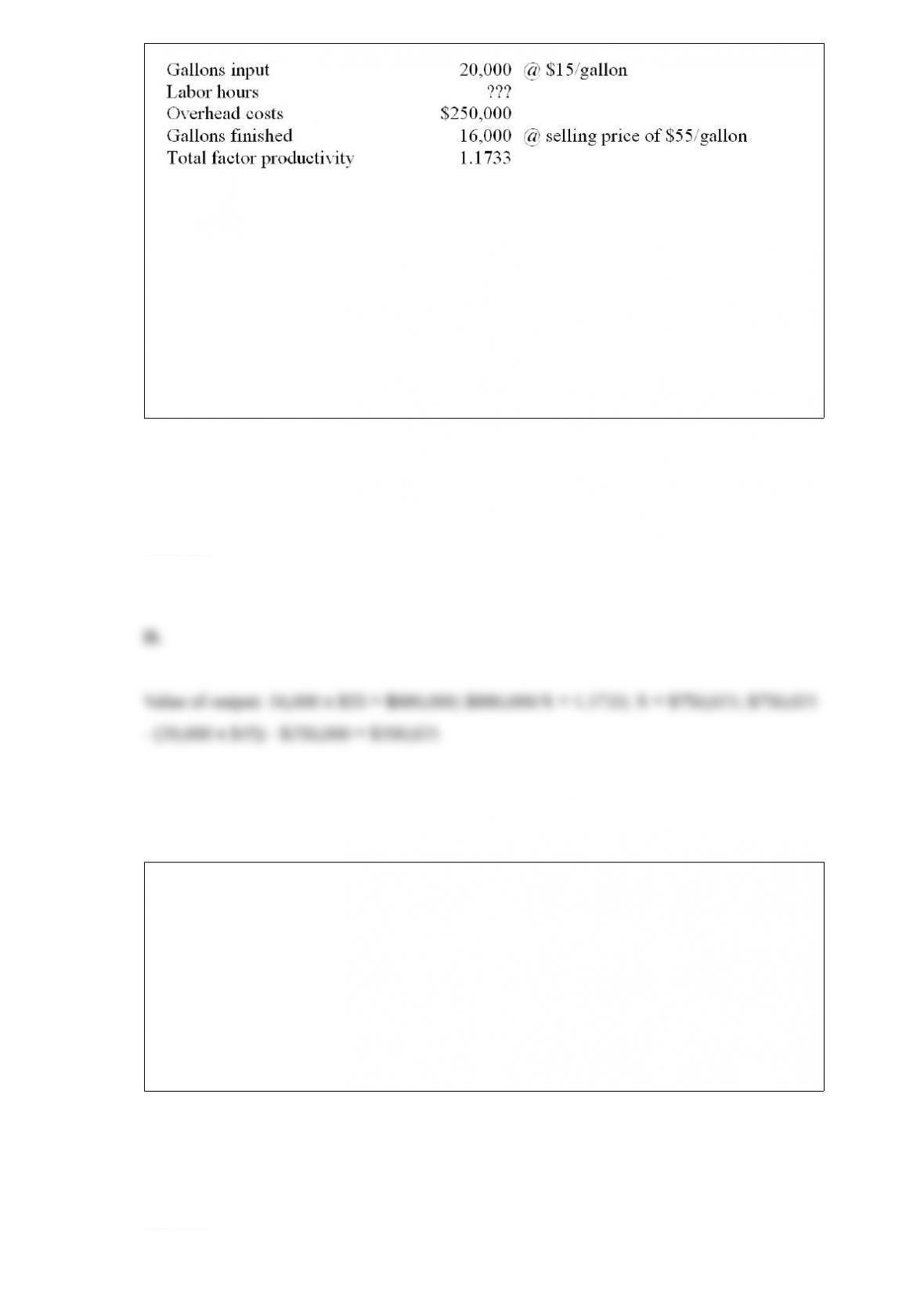

The Albertville Co has the following information for last year

The partial productivity for material is

A. 1.136

B. 0.288

C. 0.263

D. 3.802

Answer:

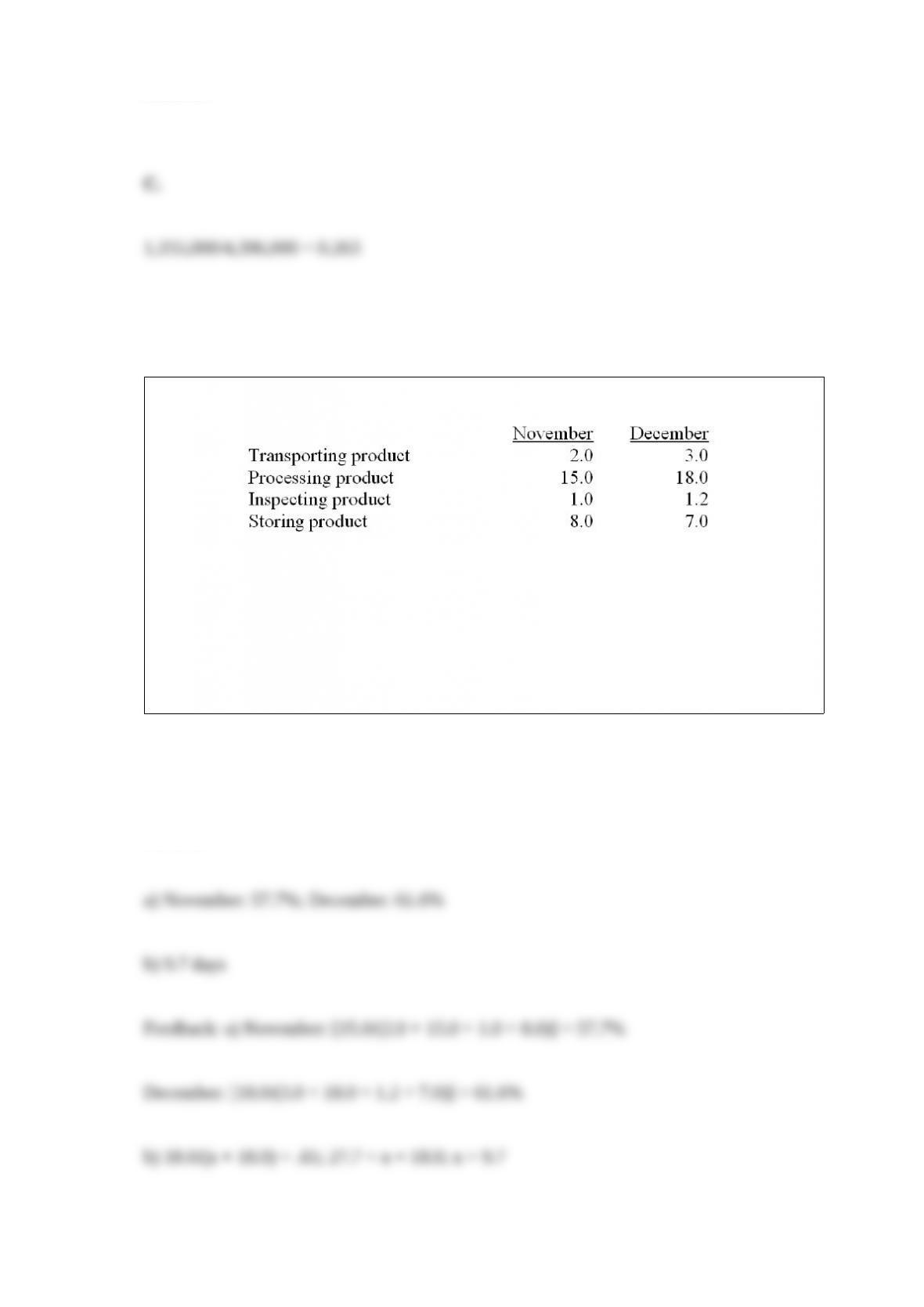

The Acme Company collected the following information (in days) for November and

December.

Required:

a) Calculate the manufacturing cycle efficiency for November and December.

b) Assume January’s processing time will be the same as December’s. If Acme’s target

for manufacturing cycle efficiency is 65%, what will January’s target for non-processing

times be?

Answer:

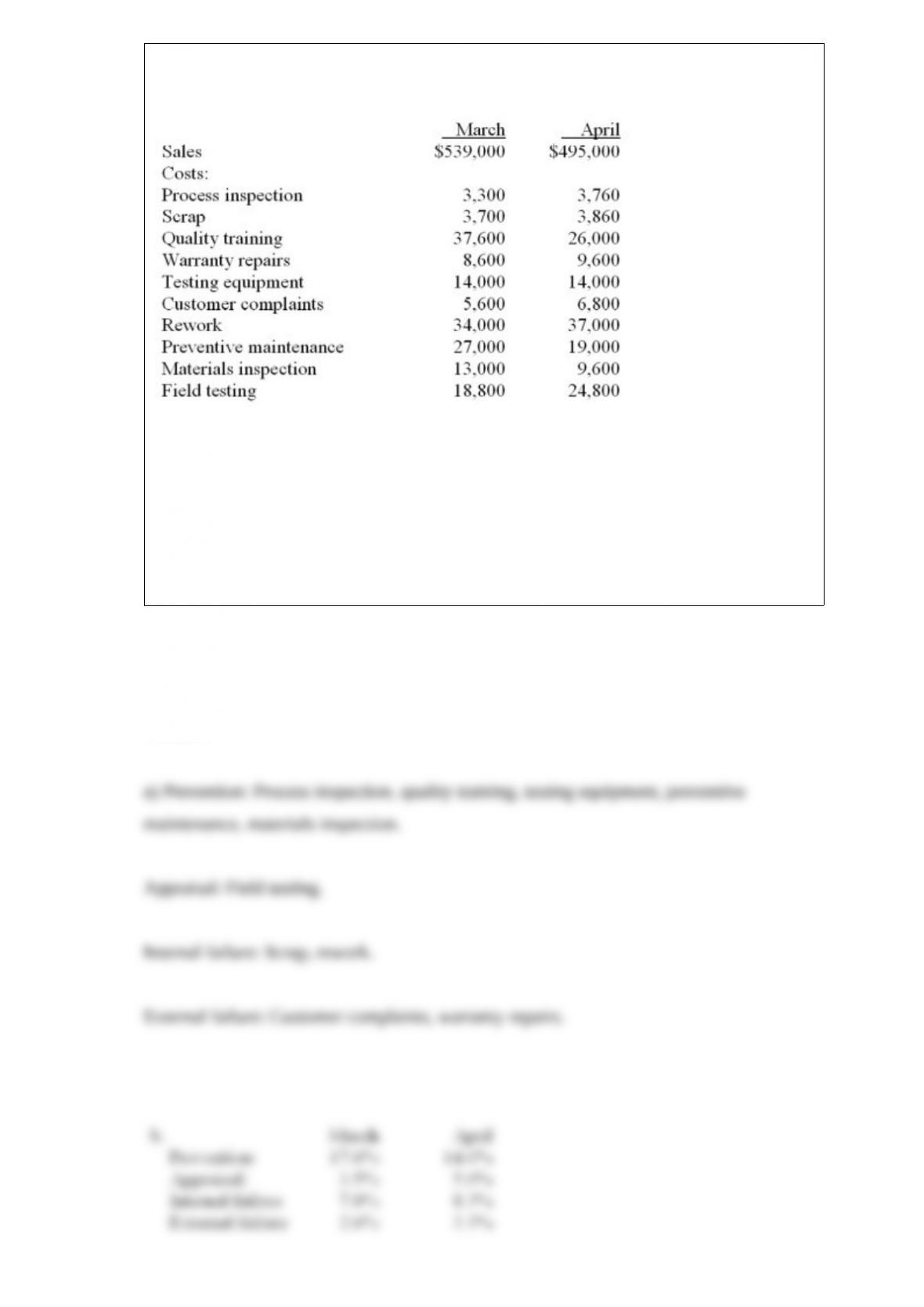

The following represents the financial information of Trovatore Corporation, a

manufacturer of electronic components, for two months:

Required

a) Classify these items into prevention, appraisal, internal failure, or external failure

costs.

b) Calculate the ratio of the prevention, appraisal, internal failure, and external failure

costs to sales for March and April.

Answer:

Howard Company operates several investment centers. The manager of Genco

Division expects the following results for the coming year.

Included in Genco’s variable cost is $7 for a component it buys from an outside

supplier. One of these components is required in each unit of Genco’s product. The

manager of Genco has just found that she can buy the component from Danner

Division, another division of Howard Company. Danner sells 300,000 units of the

component to outsiders at $8 and its variable cost is $4 per unit. Danner offers to sell

the component to Genco at a price of $6. Danner is operating well below capacity

Required

a) If Genco accepts the offer, what will happen to the income of Danner Division?

b) If Genco accepts the offer, what will happen to the income of Genco Division?

c) If Genco accepts the offer, what will happen to the income of Howard Company?

Answer:

For Case (C) above, what is the Beginning Balance (BB)?

A. $15,900

B. $2,100

C. $11,700

D. $13,800

Answer:

Which of the following statements regarding the trade-off between conformance and

nonconformance costs is (are) false?

(A) The optimal level for a company’s quality control program occurs when its

conformance costs equal its nonconformance costs.

(B) There is an inverse relationship between the costs spent on nonconformance costs

and the level of quality achieved.

A. Only A is false.

B. Only B is false.

C. Both A and B are false.

D. Neither A nor B is false.

Answer:

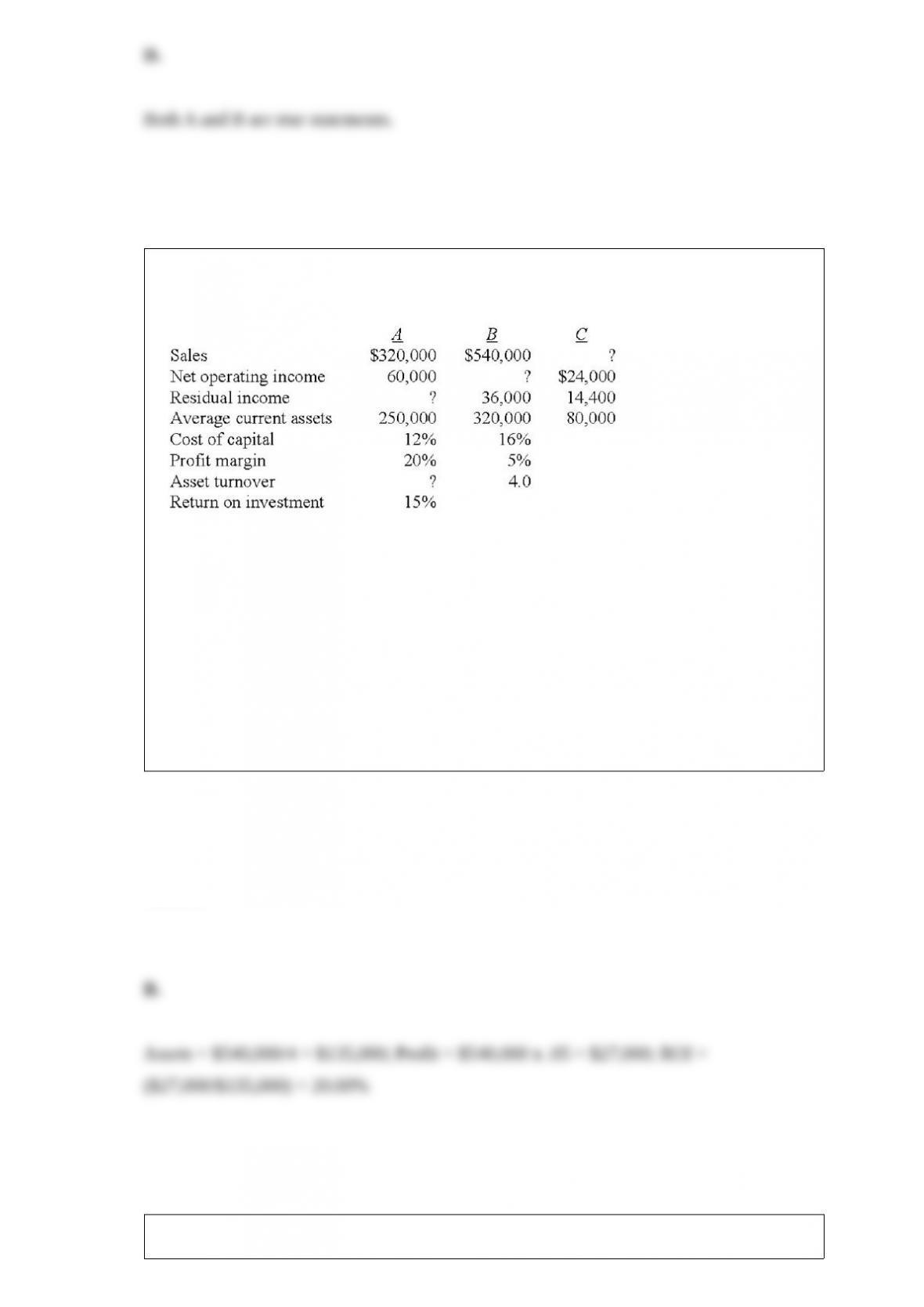

The ABC Company has three divisions: A Division, B Division, and C Division.

What was B Division’s return on investment (ROI) last year?

A. 16.00%.

B. 20.00%.

C. 24.00%.

D. 33.75%.

Answer:

Schroeder Forging Co. has provided the following information for last year:

Required: Calculate the partial productivity for:

a) Metal

b) Labor

Answer:

Residual income is similar to the _________ notion of profit as being the amount left

over after all costs, including the cost of the capital employed in the division, are

subtracted.

A. accountants’

B. manager’s

C. shareholder’s

D. economist’s

E. financial analyst’s

Answer:

You have been provided with the following information for Division Sell of a

decentralized company:

Division Buy would like to purchase all of its units internally. Division Buy needs

6,000 units each period and currently pays $84 per unit to an outside firm. What is the

lowest price that Division Sell could accept from Division Buy? Assume that Division

Buy wants to use a sole supplier and will not purchase less than 6,000 from a supplier.

A. $90.

B. $

C. $80.

D. $66.

E. $40.

Answer:

Scottso Corporation applies overhead using a normal costing approach based upon

machine-hours. Budgeted factory overhead was $232,750, budgeted machine-hours

were 17,500. Actual factory overhead was $227,830, actual machine-hours were

16,150. How much overhead would be applied to production?

A. $214,795

B. $227,830

C. $232,750

D. $246,875

Answer:

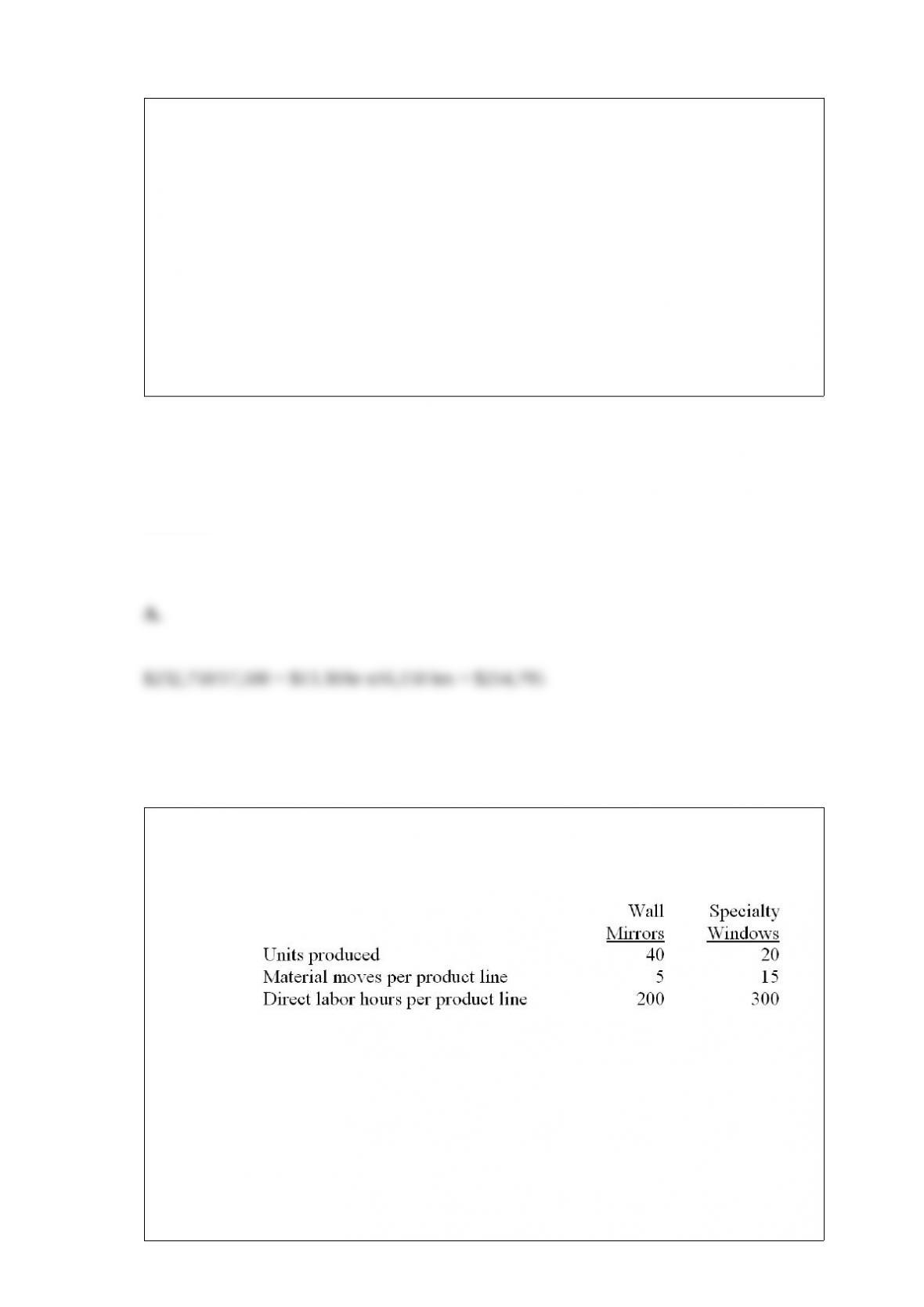

Zela Company is preparing its annual profit plan. As part of its analysis of the

profitability of individual products, the controller estimates the amount of overhead that

should be allocated to the individual product lines from the information provided below.

(CMA based)

Budgeted material handling costs: $50,000

Under an activity-based costing (ABC) system, the materials handling costs allocated to

one unit of specialty windows would be

A. $1,875.00

B. $937.50

C. $312.50

D. $1,500.00

Answer:

Which of the following balanced scorecard perspectives focuses on shareholder’s

interests?

A. Financial

B. Customer

C. Internal Business Process

D. Learning and growth

Answer:

Economic value added (EVA) is a concept that is closely related to residual income.

EVA is computed by

A. subtracting the adjusted total cost of capital from the adjusted after-tax income.

B. subtracting adjusted after-tax income from total divisional investment.

C. dividing adjusted after-tax income by adjusted divisional investment.

D. dividing adjusted after-tax income by adjusted total cost of capital.

Answer:

Which of the following is not an internal control?

A. rotating personnel among tasks.

B. separation of duties.

C. setting limits on the amount of expenditures.

D. using absolute performance standards.

Answer:

Redimix Corporation has two producing centers, (A and B) Division A has a variable

cost of $12 for its products and a total fixed cost of $120,000. Division A also has idle

capacity for up to 50,000 units per month. Division B would like to purchase 20,000

units of Division A’s products per month, but is unable to convince Division A to

transfer units to Division B at $16 per unit. Division A has consistently argued that the

market price of $20 is nonnegotiable. What is A’s opportunity cost of not transferring

units to B?

A. $20

B. $12

C. $8

D. $4

Answer:

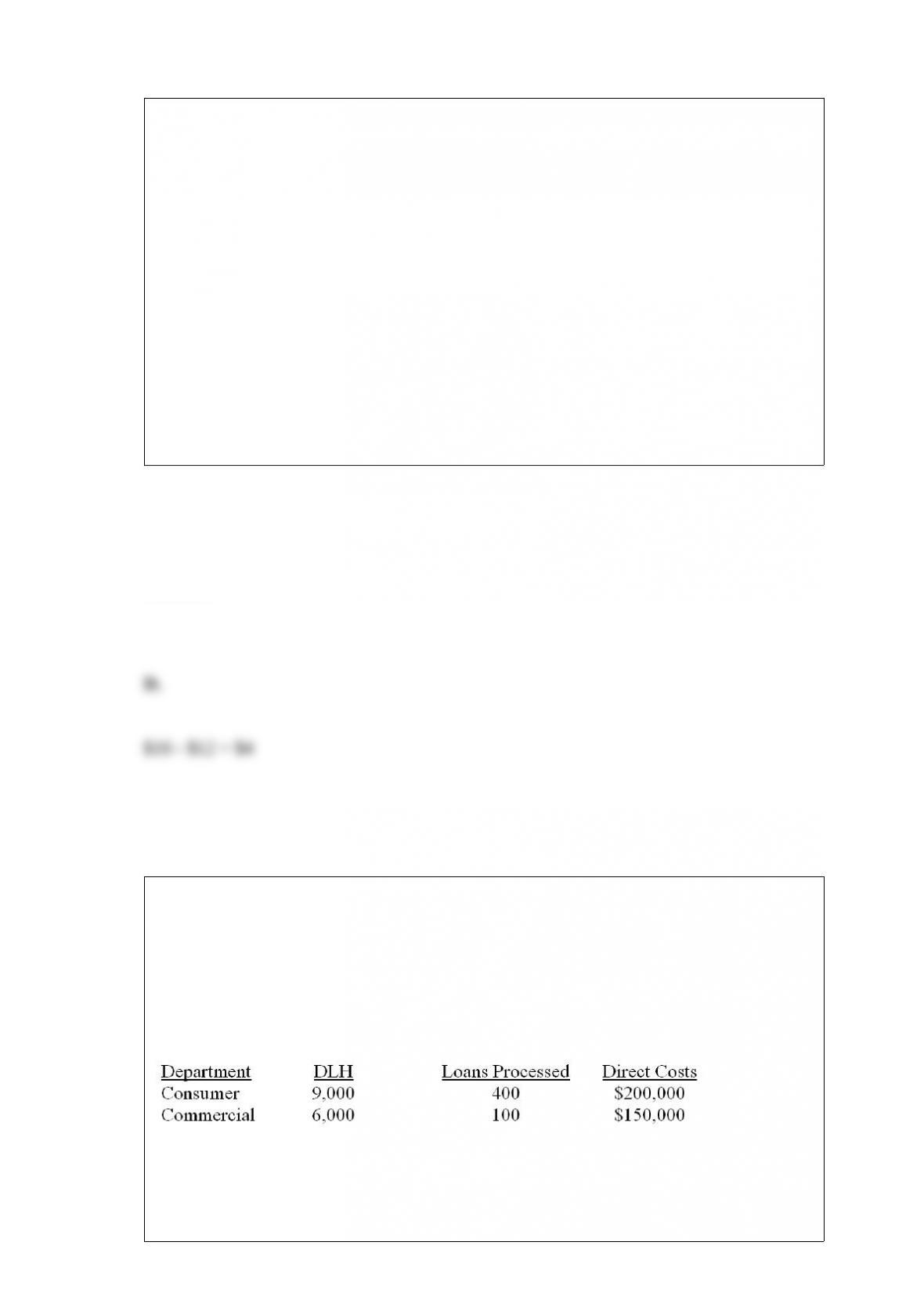

The Muskego National Bank is considering either a bankwide overhead rate or

department overhead rates to allocate $250,000 of indirect costs. The bankwide rate

could be based on either direct labor hours (DLH) or the number of loans processed.

The departmental rates would be based on direct labor hours for Consumer Loans and a

dual rate based on direct labor hours and the number of loans processed for Commercial

Loans. The following information was gathered for the upcoming period:

Management estimates that it costs $500 to analyze and close a commercial loan. This

amount has been included in the $250,000 of indirect costs. How much of the $250,000

indirect costs should be allocated to the Commercial Department?

A. $40,000

B. $50,000

C. $90,000

D. $120,000

Answer:

Which of the following statements is (are) true?

(A) The market share variance is more controllable by the marketing department than

the industry volume variance.

(B) The industry volume variance is the portion of the sales activity variance due to a

change in the company’s proportion of sales in the markets in which they operate.

A. Only A is true.

B. Only B is true.

C. Both A and B are true.

D. Neither A nor B is true.

Answer:

Why might a company use a predetermined rate for applying overhead rather than just

apply actual overhead?

Answer:

What is the difference between continuous improvement and benchmarking?

Answer:

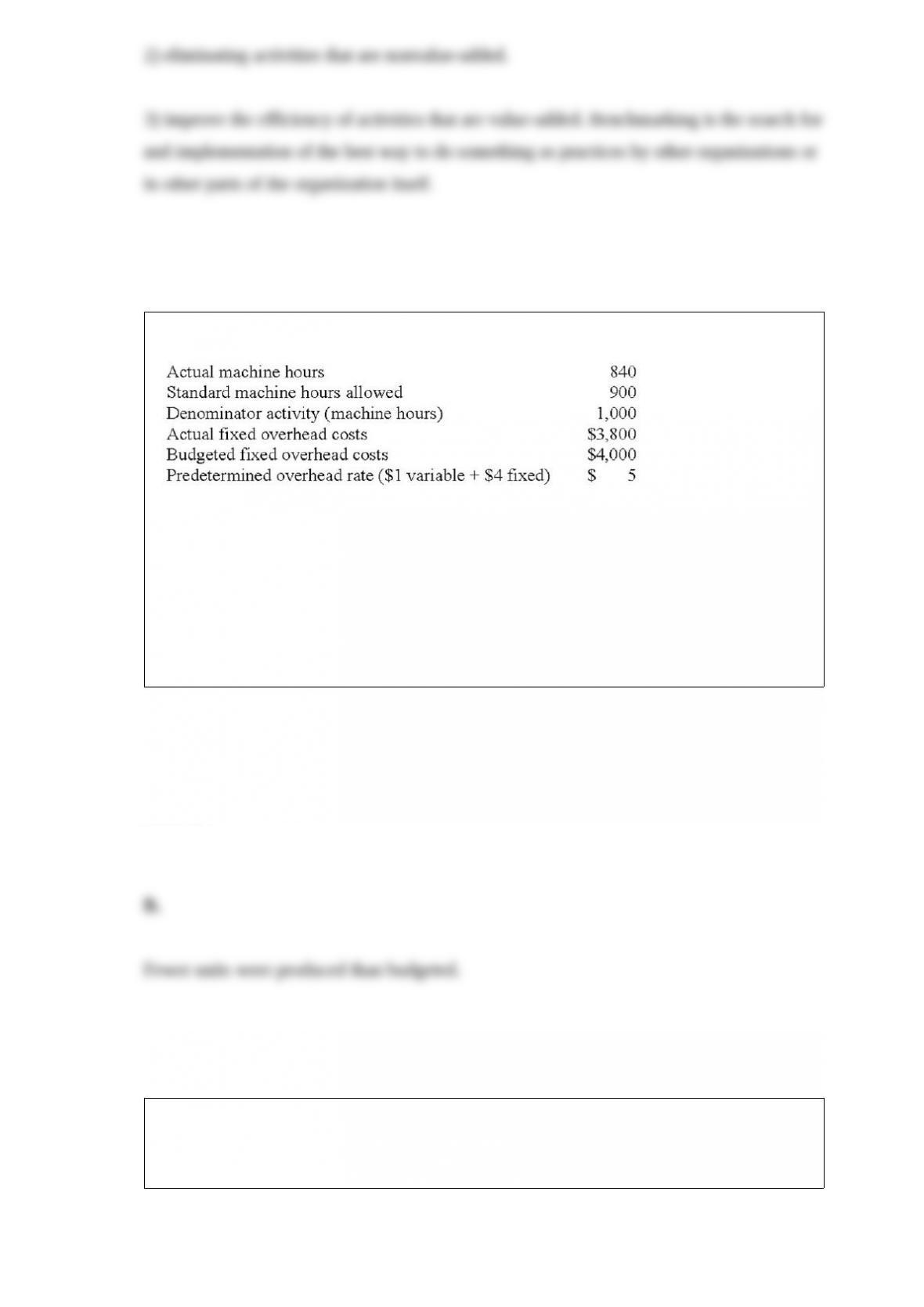

Is the production volume variance favorable or unfavorable?

A. favorable

B. unfavorable

Answer:

Respond to this comment: “Since cost accountants just prepare accounting data for

internal management, cost accountants do not need to be concerned with GAAP or

IFRS.”

Answer:

Is the direct materials efficiency (quantity) variance favorable or unfavorable?

A. favorable

B. unfavorable

Answer:

Describe the five basic types of decentralized units in responsibility accounting.

Answer:

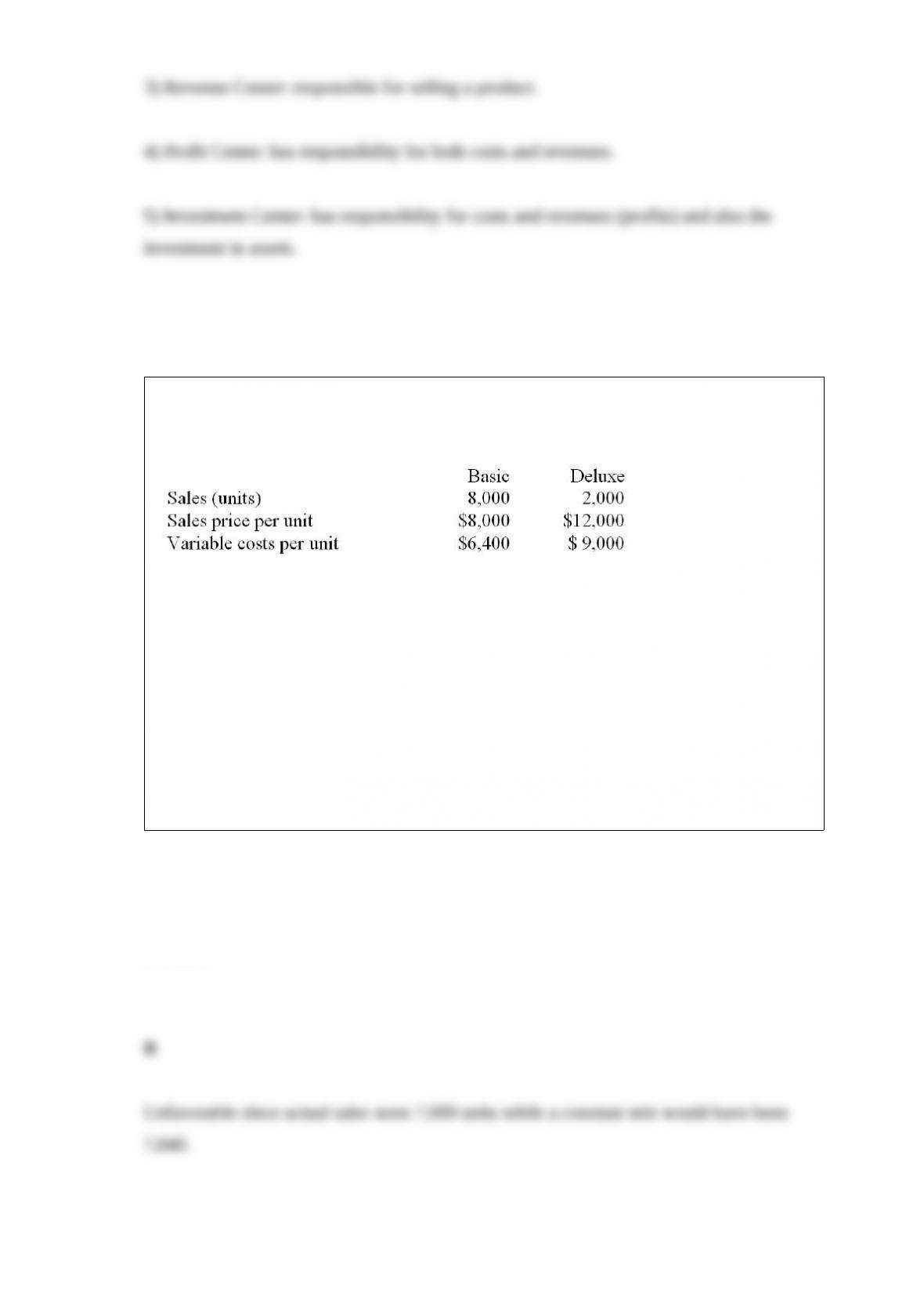

A machine distributor sells two models, basic and deluxe. The following information

relates to its master budget.

Actual sales were 7,000 basic models and 2,800 deluxe models. The actual sales prices

were the same as the budgeted sales prices for both models.

Is the sales mix variance for the basic model favorable or unfavorable?

A. favorable.

B. unfavorable.

Answer:

Explain what is meant by “the full-cost fallacy” in making pricing decisions.

Answer:

The IMA Code of Ethics describes three basic steps a cost accountant should take when

faced with an ethical conflict: Discuss, clarify, consult. Describe each of these three

steps.

Answer:

The sales manager of Acme Enterprises is considering expanding sales by producing

three different versions of their product. Each will be targeted by the marketing

department to different income levels and will be produced from three different

qualities of materials. After reviewing the sales forecasts, the sales department feels that

40% of units sold will be the original product, 35% will be new model #1 and the

remainder will be new model #2.

The following information has been assembled by the sales department and the

production department.

The fixed costs associated with the manufacture of these three products are $175,000

per year.

Required:

Determine the number of units of each product that would be sold at the break-even

point.

Answer:

Cindy’s Limo Service provides transportation services in and around Middleville. Its

profits have been declining, and management is planning to add a package delivery

service that is expected to increase revenue by $275,000 per year. The total cost to lease

additional delivery vehicles from the local dealer is $60,000 per year. The present

manager will continue to supervise all services. Due to expansion, however, the labor

costs and utilities would increase by 40%. Rent and other costs will increase by 15%.

Required:

Prepare a report of the differential costs and revenues if the delivery service is added.

Should management start up the delivery service? Explain your answer.

Answer:

Why is it important to consider opportunity costs in a make-or-buy decision?

Answer:

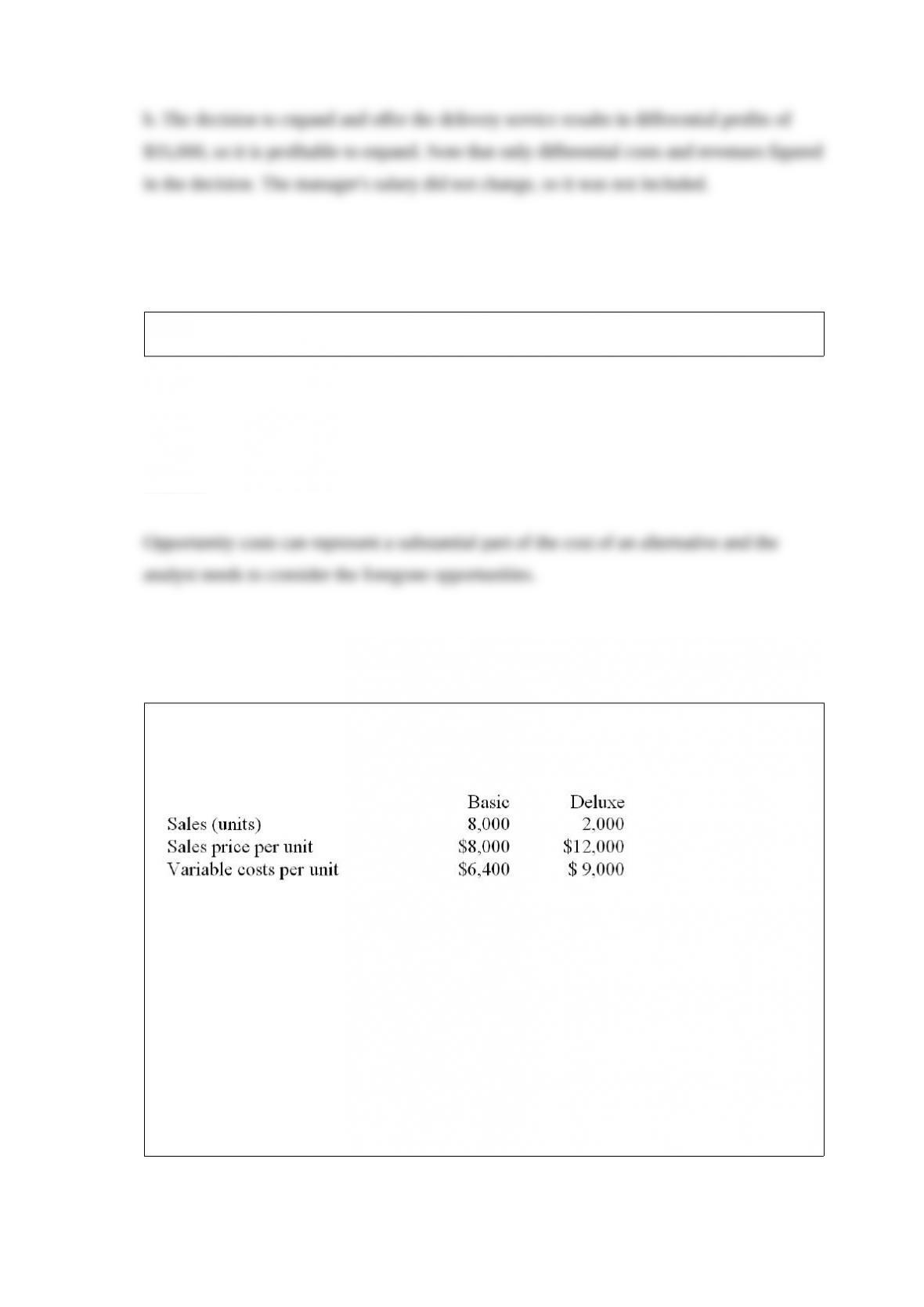

A machine distributor sells two models, basic and deluxe. The following information

relates to its master budget.

Actual sales were 7,000 basic models and 2,800 deluxe models. The actual sales prices

were the same as the budgeted sales prices for both models.

Is the sales activity variance for the basic model favorable or unfavorable?

A. favorable.

B. unfavorable.

Answer:

Explain the difference between full costs and differential costs.

Answer:

Answer: