After issuing its financial statements, a company discovered that its beginning

inventory was overstated by $100,000. Its tax rate is 30%. As a result of this error, net

income was:

a. Understated by $70,000.

b. Overstated by $70,000.

c. Understated by $30,000.

d. Overstated by $30,000.

Sloan Company has owned an investment during 2016 that has increased in fair value.

After all closing entries for 2016 are completed, the effect of the increase in fair value

on total shareholders’ equity would be:

a. Higher under the available-for-sale approach than under the trading-securities

approach.

b. Lower under the available-for-sale approach than under the trading-securities

approach.

c. The same amount under the available-for-sale and trading-securities approaches.

d. Not possible to identify whether the available-for-sale or trading-securities

approaches yield higher shareholders’ equity given this information.

The purpose of closing entries is to transfer:

a. Accounts receivable to retained earnings when an account is fully paid.

b. Balances in temporary accounts to a permanent account.

c. Inventory to cost of goods sold when merchandise is sold.

d. Assets and liabilities when operations are discontinued.

In a statement of cash flows prepared under International Financial Reporting

Standards, each of the following items is typically classified as a financing cash flow

except:

a. Interest paid.

b. Dividends paid.

c. Proceeds from the issuance of long-term debt.

d. Dividends received.

Beagle Corporation has 20,000 shares of $10 par common stock outstanding and 10,000

shares of $100 par, 6% cumulative, nonparticipating preferred stock outstanding.

Dividends have not been paid for the past two years. This year, a $300,000 dividend

will be paid. What are the dividends per share payable to preferred and common,

respectively?

a. $6; $12.

b. $18; $6.

c. $6; $6.

d. None of these answer choices is correct.

Mandatorily redeemable preferred stock (preference shares) is reported as debt, with the

dividends reported in the income statement as interest expense, using:

a. U.S. GAAP.

b. IFRS.

c. Both U.S. GAAP and IFRS.

d. Neither U.S. GAAP nor IFRS.

When a product or service is delivered for which a customer advance has been

previously received, the appropriate journal entry includes:

a. A debit to a revenue and a credit to a liability account.

b. A debit to a revenue and a credit to an asset account.

c. A debit to an asset and a credit to a revenue account.

d. A debit to a liability and a credit to a revenue account.

How is the amortization of patents reported in a statement of cash flows that is prepared

using the direct method?

a. Not reported.

b. An increase in cash flows from operating activities.

c. A decrease in cash flows from operating activities.

d. A decrease in cash flows from investing activities.

Nichols Corporation purchased $100,000 of Holly Inc. 6% bonds at par with the intent

and ability to hold the bonds until they matured in 2020, so Nichols classifies its

investment as held to maturity. Unfortunately, a combination of problems at Holly and

in the debt market caused the fair value of the Holly investment to decline to $70,000

during 2016. Nichols calculates that, of the $30,000 decrease in fair value, $10,000 of it

relates to credit losses and $20,000 relates to noncredit losses. Assume that Nichols

concludes that the Holly bonds are other-than-temporarily impaired because Nichols

calculates that the bonds have incurred credit losses. Before-tax net income for 2016

will be reduced by: a. $0.

b. $10,000.

c. $20,000.

d. $30,000.

Acquiring land with a long-term note is:

a. Reported as an investing activity in the statement of cash flows.

b. Reported as a financing activity in the statement of cash flows.

c. Reported as a noncash investing and financing activity.

d. None of the above is correct.

Newjohn Company owns stock in several affiliated companies. Investments in some of

these affiliates are accounted for as securities available for sale while some are

accounted for using the equity method.

Required:

(1.) What factors determine which method should be used?

(2.) What events are recorded when the equity method is used?

(3.) What events are recorded when the securities are accounted for as available

for sale?

On January 2, 2016, MBH Inc. acquired 30% of the voting common stock of

Construction Corporation as a long-term investment. Data from Construction

Corporation’s financial statements for the year ended December 31, 2016, include the

following:

Net income $150,000

Dividends paid $75,000

Required:

Prepare any necessary journal entries for MBH at December 31, 2016, under the equity

method of accounting for investments.

If inventory is understated at the end of 2015 and the error is not discovered, how will

net income be affected in 2016?

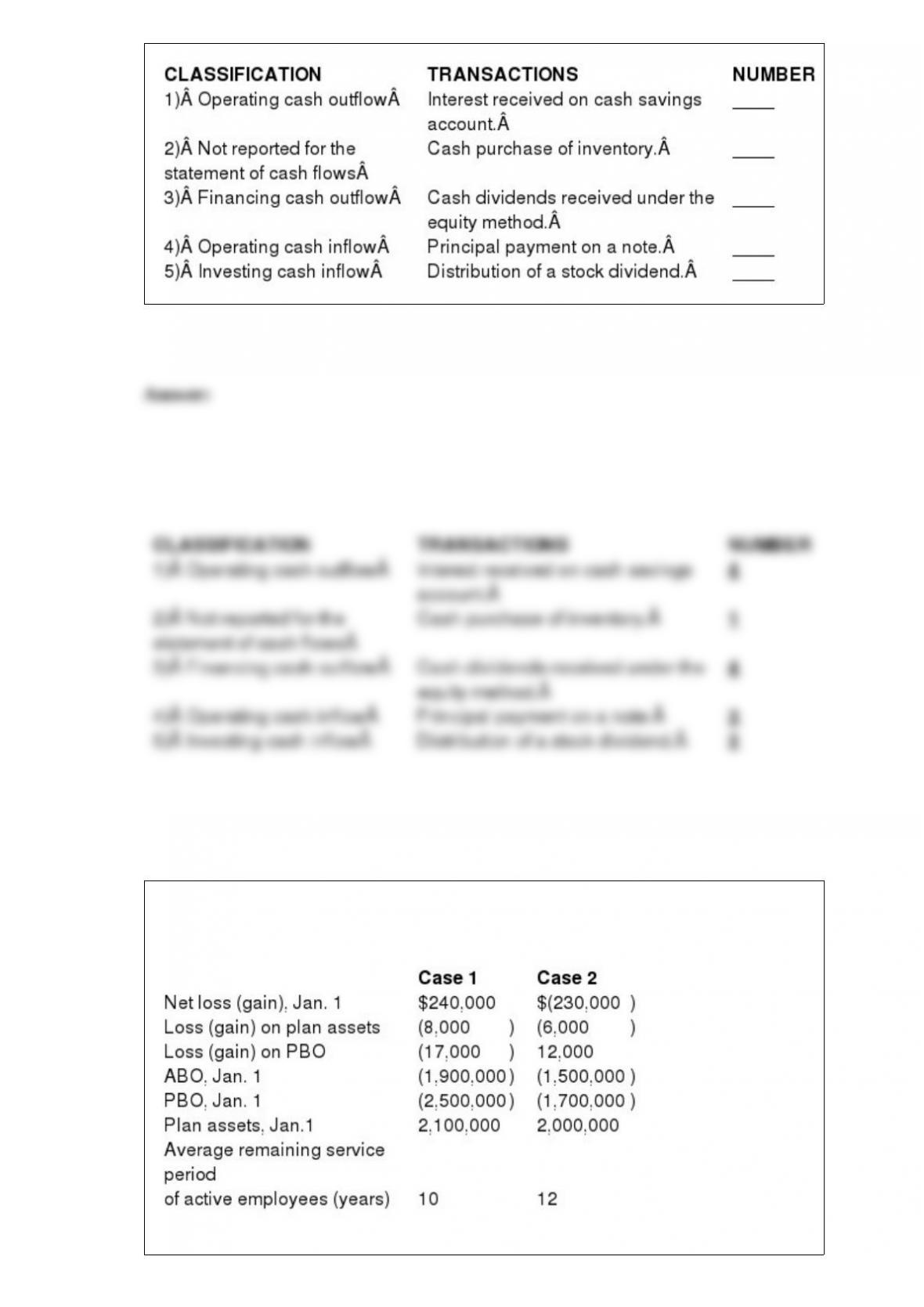

Listed below are the reporting classifications for a statement of cash flows using the

direct method for reporting operating cash flows. Indicate the reporting classification

that would apply to each of the five transactions described below by placing the number

of the reporting classification in the space provided by each transaction.

Vrable Corporation has a defined benefit pension plan. Two alternative possibilities for

pension-related data for the current calendar year are shown below:

Required:

For each independent case, calculate amortization of the net loss or gain that should be

included as a component of pension expense for the current year.

Price Mart is considering outsourcing its billing operations. A consultant estimates that

outsourcing should result in after-tax cash savings of $9,000 the first year, $15,000 for

the next two years, and $18,000 for the next two years. Interest is at 12%. Assume cash

flows occur at the end of the year.

Required: Calculate the total present value of the cash flows.

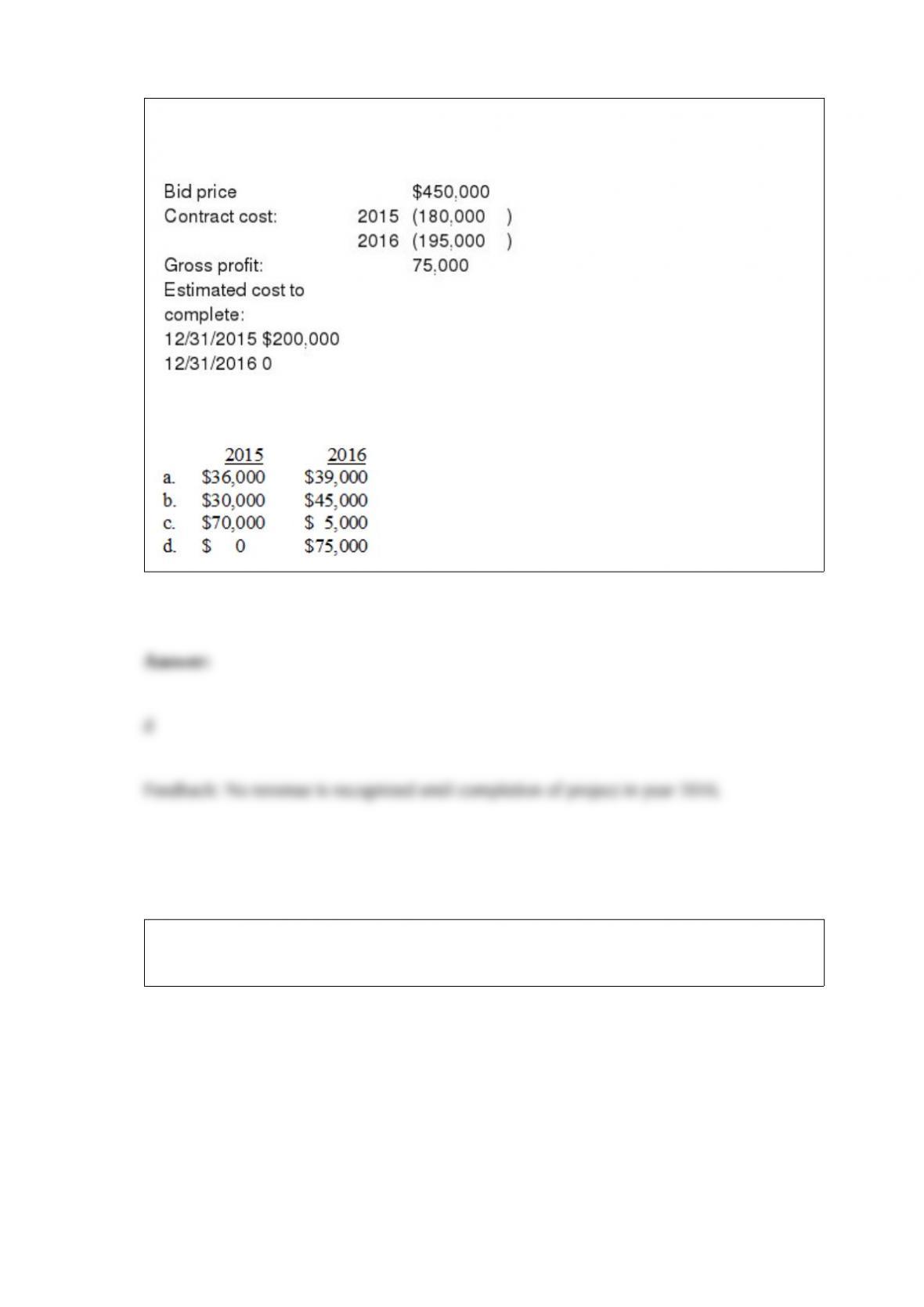

Summary data for Benedict Construction Co.’s (BCC) Job 1227, which was completed

in 2016, are presented below:

Assuming BCC used the cost recovery method to recognize revenue under IFRS, what

would gross profit have been in 2015 and 2016 (rounded to the nearest thousand)?

Listed below are six terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the most correct term.

In its 2016 annual report to shareholders, Health Foods, Inc., disclosed the following

information about some of its indebtedness: The fair value of convertible subordinated

debentures is estimated using quoted market prices. Book amounts and estimated fair

values of our financial instruments other than those for which book amounts

approximate fair values as noted above are as follows (in thousands)

In addition, the company disclosed the following: We have outstanding zero coupon

convertible subordinated debentures which had a book amount of approximately $158.8

million and $151.4 million at September 26, 2016, and September 28, 2015,

respectively. The debentures have an effective yield to maturity of 5 percent and a

principal amount at maturity on March 2, 2030, of approximately $308.8 million. The

debentures are convertible at the option of the holder, at any time on or prior to

maturity, unless previously redeemed or otherwise purchased. The debentures have a

conversion rate of 10.64 shares per $1,000 principal amount at maturity, representing

3,285,632 shares. The debentures may be redeemed at the option of the holder on

March 2, 2020, or March 2, 2025, at the issue price plus accrued original discount

totaling approximately $188 million and $241 million, respectively.

Required: What amount of interest expense will Health Foods accrue on the debentures

during fiscal year 2017?