1) If the actual level of activity is 4% less than planned, then the variable costs in the

static budget should be decreased by 4% before comparing them to actual costs.

2) The dividend payout ratio is equal to the dividend per share divided by the earnings

per share.

3) Product-level activities relate to how many batches are run or units of product are

made.

4) The higher the discount rate, the lower the present value of a given future cash flow.

5) The present value of an amount to be received in five years is greater than the present

value of the same amount to be received in ten years.

6) Assuming the LIFO inventory flow assumption, if production is less than sales for

the period, absorption costing net operating income will generally be greater than

variable costing net operating income.

7) Under the indirect method of determining the net cash provided by operating

activities on the statement of cash flows, a decrease in inventory would be added to net

income.

8) The engineering approach to the analysis of mixed costs involves a detailed analysis

of what cost behavior should be, based on an industrial engineers evaluation of the

production methods to be used, the materials specifications, labor requirements,

equipment usage, production efficiency, power consumption, and so on.

9) The price elasticity of demand is NOT used in the absorption costing approach to

cost-plus pricing to determine the markup over cost.

10) All other things the same, purchasing merchandise inventory would have no effect

on the accounts receivable turnover ratio at a retailer.

11) If the actual direct labor-hours used is less than the standard direct labor-hours

allowed for the actual output, then the journal entry to record the Labor Efficiency

Variance would be a credit.

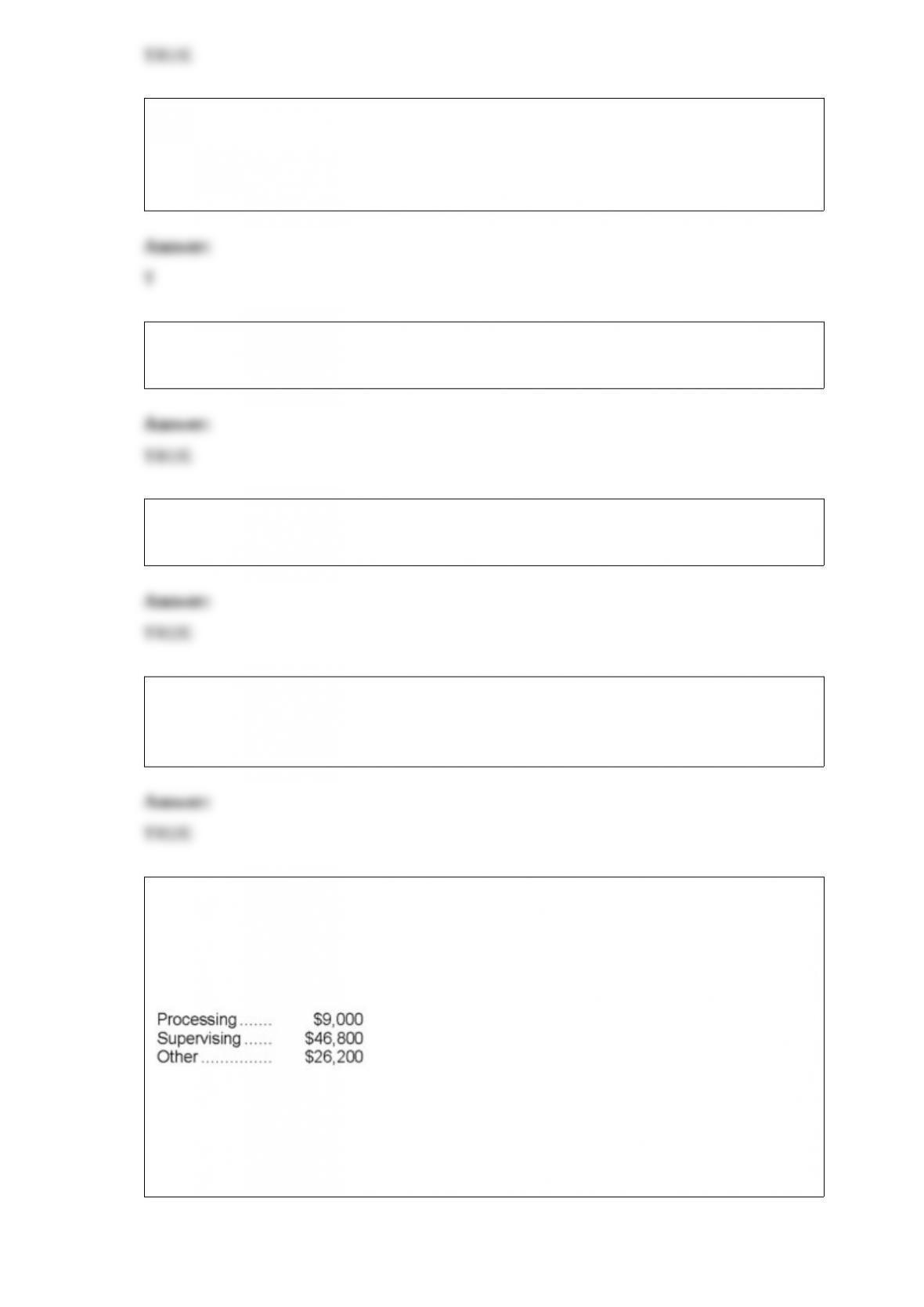

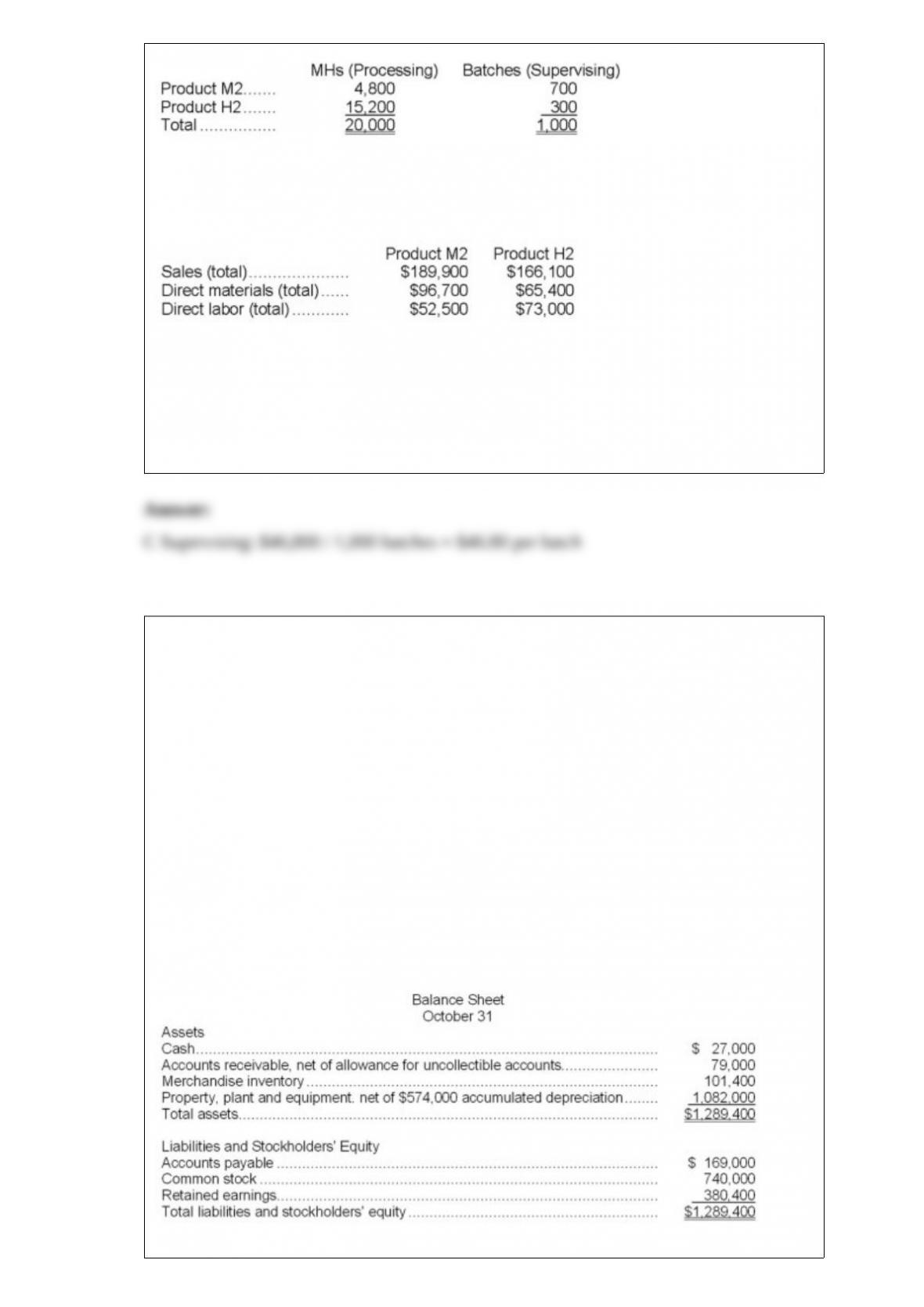

12) Zumbrunnen Corporation uses activity-based costing to compute product margins.

Overhead costs have already been allocated to the company’s three activity cost

pools-Processing, Supervising, and Other. The costs in those activity cost pools appear

below:

Processing costs are assigned to products using machine-hours (MHs) and Supervising

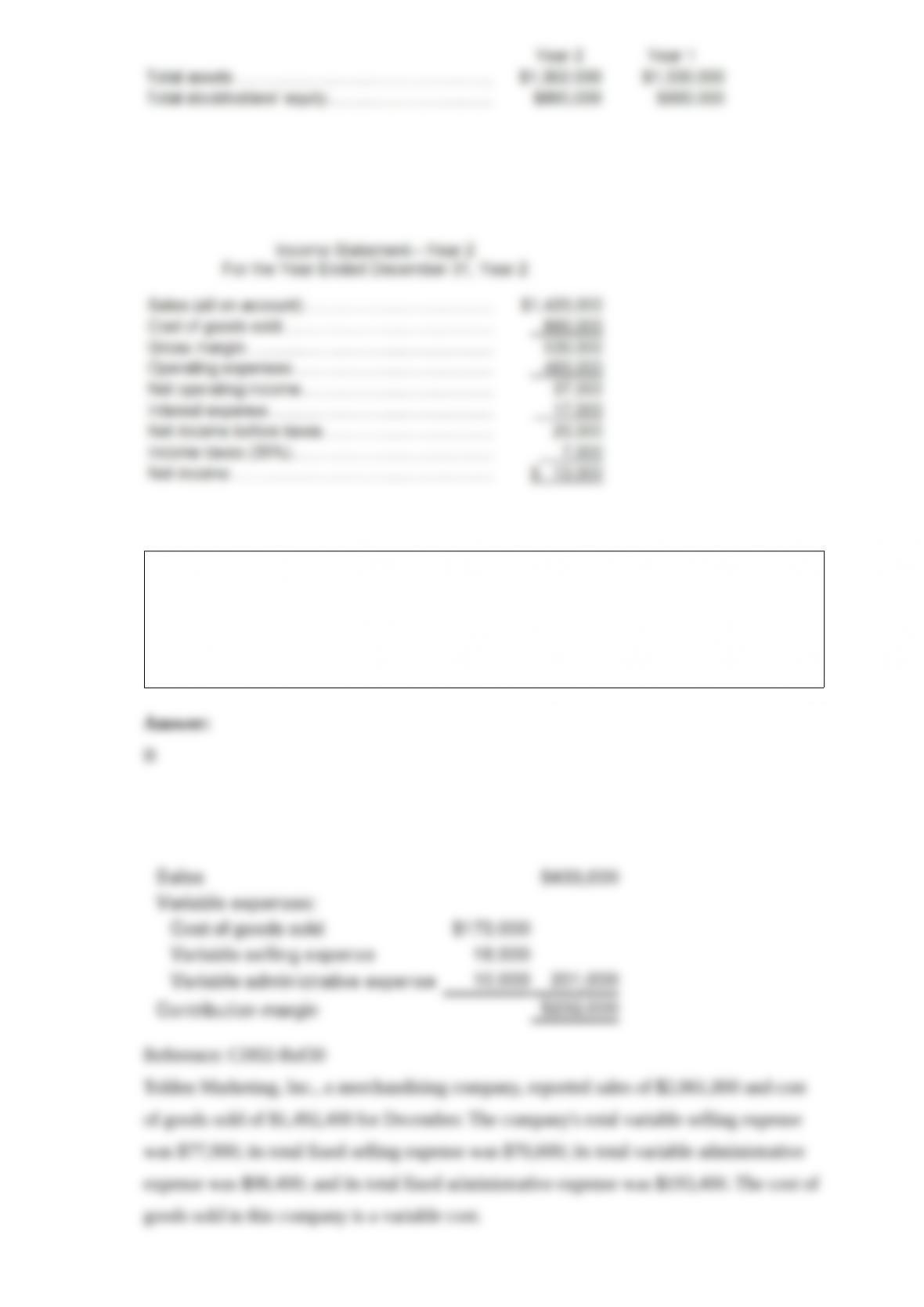

costs are assigned to products using the number of batches. The costs in the Other

activity cost pool are not assigned to products. Activity data appear below:

Finally, sales and direct cost data are combined with Processing and Supervising costs

to determine product margins.

The activity rate for the Supervising activity cost pool under activity-based costing is

closest to:

A.$8.00 per batch

B.$26.67 per batch

C.$46.80 per batch

D.$82.00 per batch

13) Dilbert Farm Supply is located in a small town in the rural west. Data regarding the

store’s operations follow:

Sales are budgeted at $260,000 for November, $230,000 for December, and $210,000

for January.

Collections are expected to be 80% in the month of sale, 19% in the month following

the sale, and 1% uncollectible.

The cost of goods sold is 65% of sales.

The company desires to have an ending merchandise inventory at the end of each

month equal to 60% of the next month’s cost of goods sold. Payment for merchandise is

made in the month following the purchase.

Other monthly expenses to be paid in cash are $20,300.

Monthly depreciation is $20,000.

Ignore taxes.

The net income for December would be:

A.$60,200

B.$37,900

C.$40,200

D.$55,800

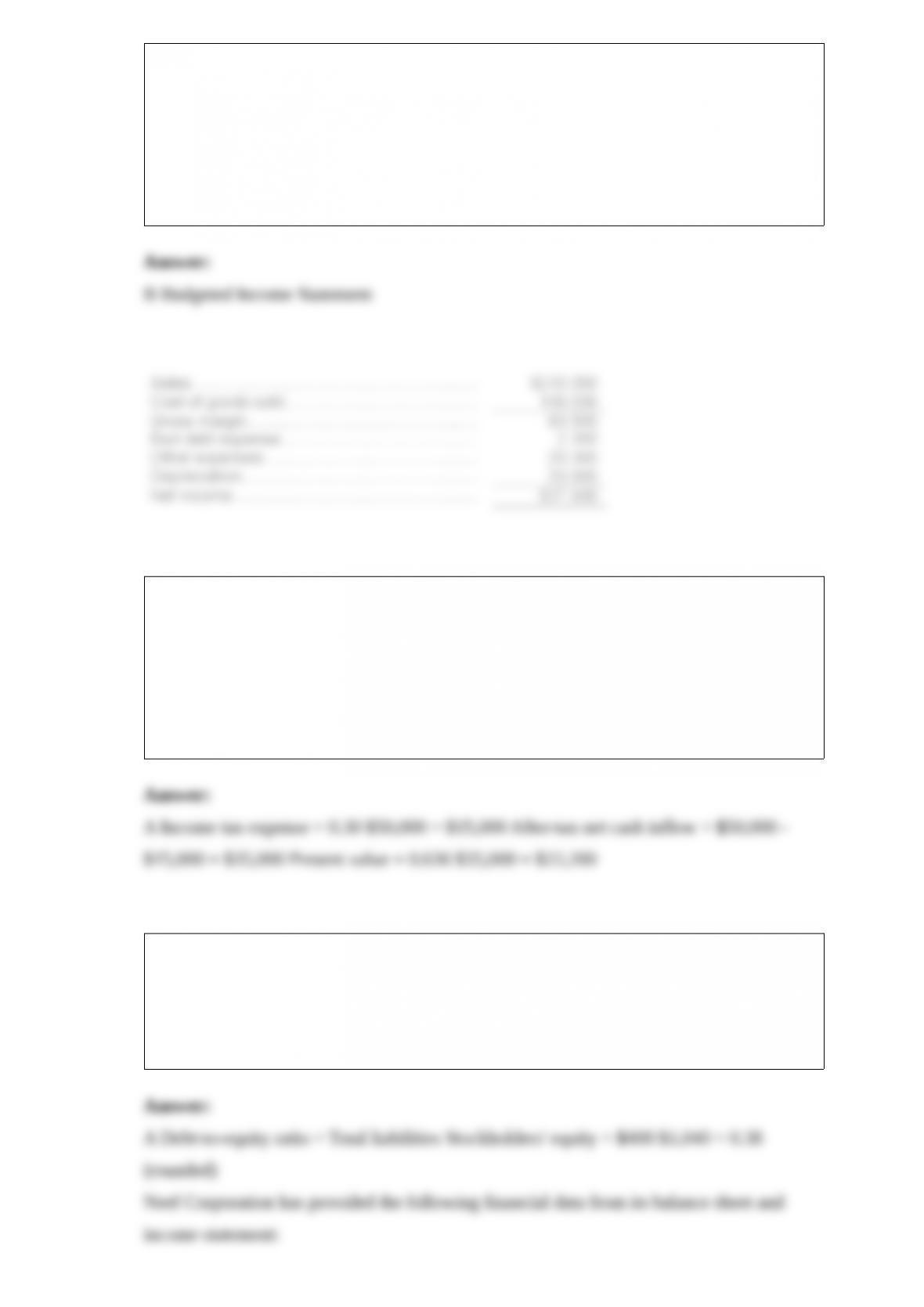

14) A company anticipates incremental net income (i.e., incremental taxable income) of

$50,000 in year 4 of a project. The company’s tax rate is 30% and its after-tax discount

rate is 12%. The present value of this future cash flow is closest to:

A.$22,260

B.$35,000

C.$9,533

D.$15,000

15) The debt-to-equity ratio at the end of Year 2 is closest to:

A.0.38

B.0.13

C.0.16

D.0.43

16) The contribution margin for October is:

A) $260,000

B) $232,000

C) $196,500

D) $369,500

17) The accounts receivable turnover for Year 2 is closest to:

A.6.62

B.1.10

C.6.32

D.0.91

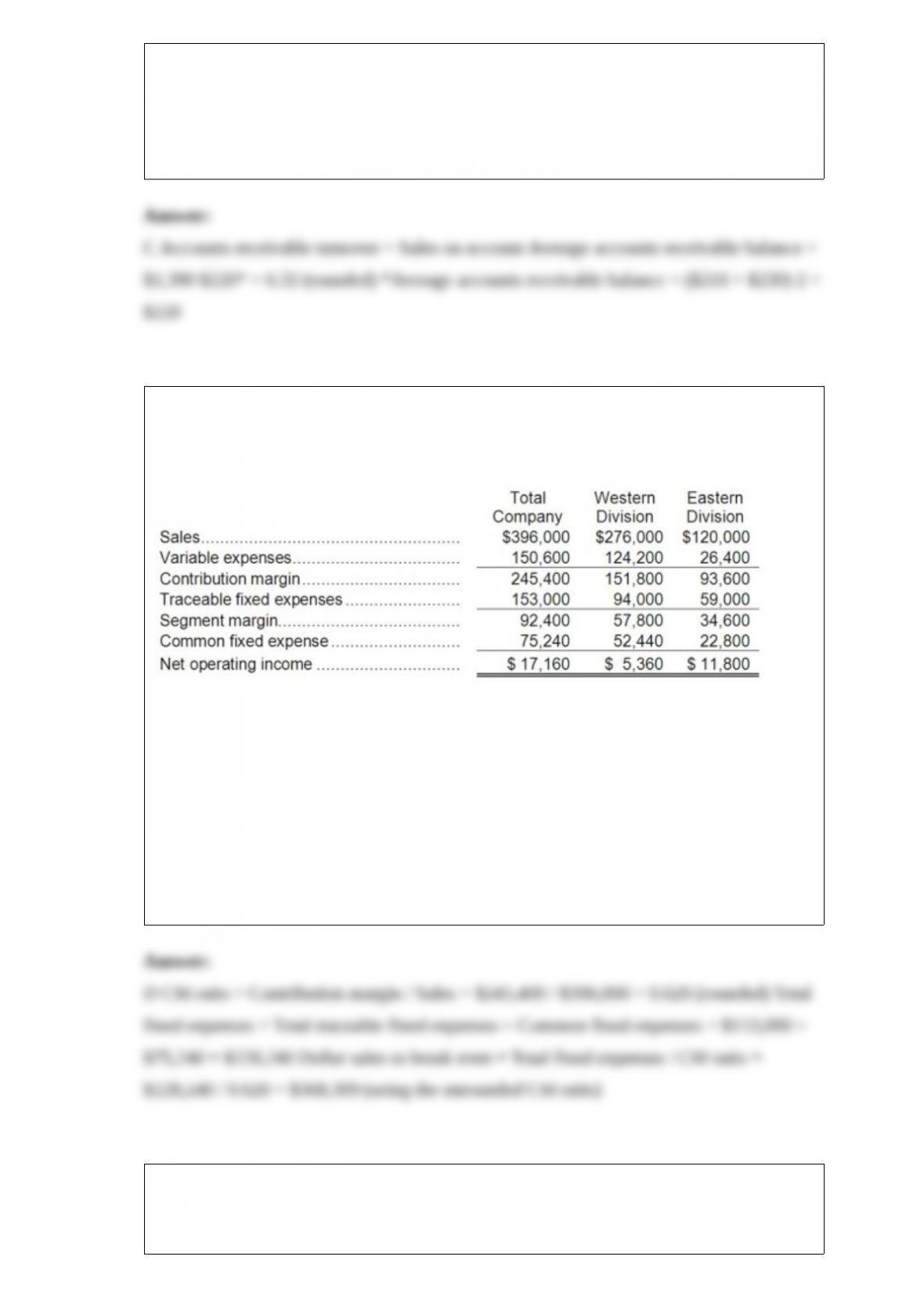

18) Keefe Corporation has two divisions: Western Division and Eastern Division. The

following report is for the most recent operating period:

The common fixed expenses have been allocated to the divisions on the basis of sales.

The company’s overall break-even sales is closest to:

A.$121,759

B.$322,457

C.$246,550

D.$368,309

19) The standards for product F88W specify 3.4 direct labor-hours per unit at $13.00

per direct labor-hour. Last month 800 units of product F88W were produced using

2,500 direct labor-hours at a total direct labor wage cost of $30,500.

Required:

a. What was the labor rate variance for the month?

b. What was the labor efficiency variance for the month?

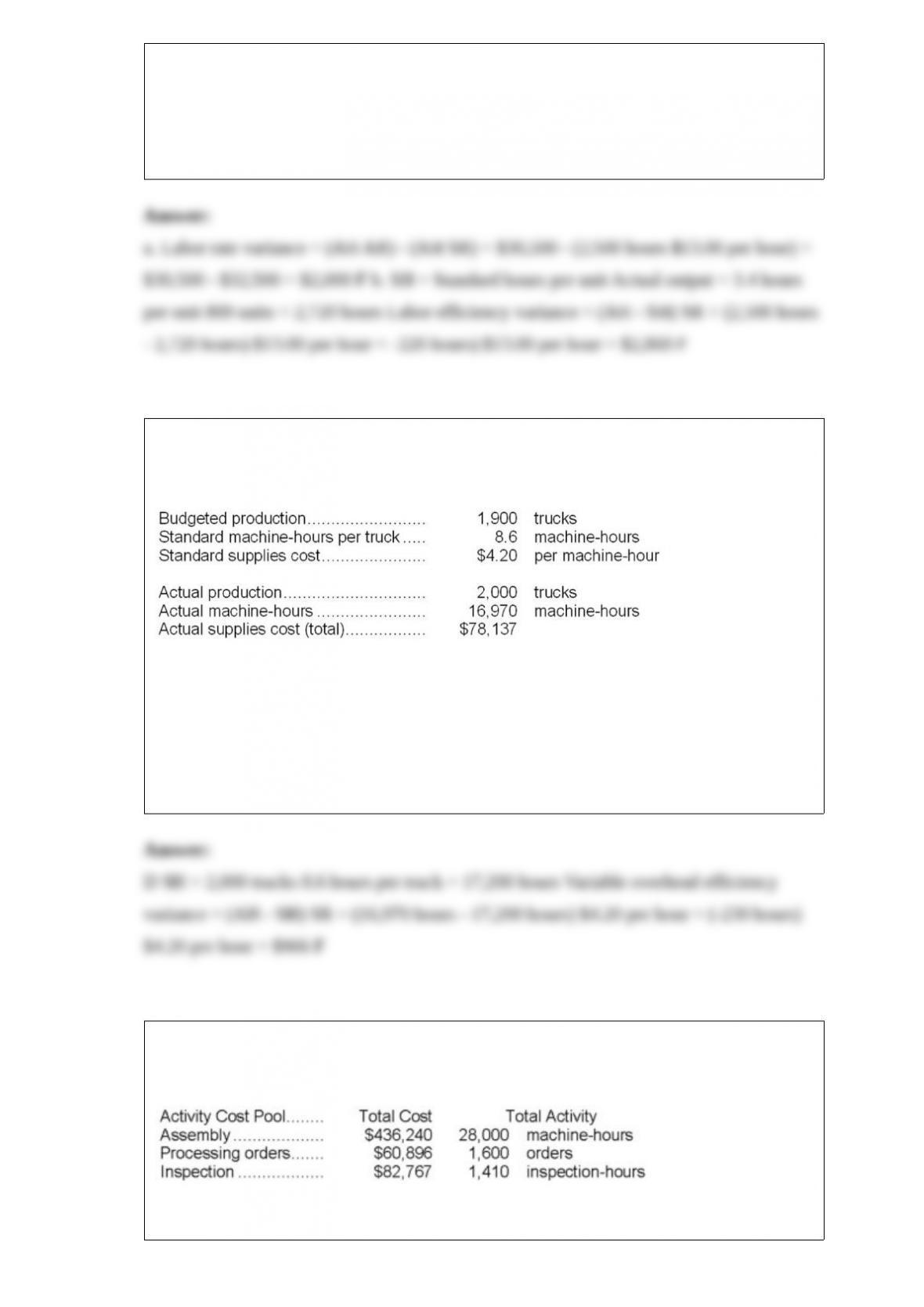

20) The following data have been provided by Gerlach Corporation, a company that

produces forklift trucks:

Supplies cost is an element of variable manufacturing overhead. The variable overhead

efficiency variance for supplies cost is:

A.$966 U

B.$5,897 U

C.$5,897 F

D.$966 F

21) Radakovich Corporation has provided the following data from its activity-based

costing system:

The company makes 230 units of product F60N a year, requiring a total of 480

machine-hours, 50 orders, and 30 inspection-hours per year. The product’s direct

materials cost is $12.70 per unit and its direct labor cost is $45.93 per unit. The product

sells for $126.60 per unit.

According to the activity-based costing system, the product margin for product F60N is:

A.$6,251.70

B.$4,490.70

C.$6,393.70

D.$15,633.10

22) Cabal Products is a division of a major corporation. Last year the division had total

sales of $10,040,000, net operating income of $582,320, and average operating assets of

$4,000,000. The company’s minimum required rate of return is 14%.

The division’s return on investment (ROI) is closest to:

A.4.1%

B.14.6%

C.36.6%

D.0.9%

23) What would be the total variable maintenance cost at an activity level of 8,600

machine-hours in a month? Assume that this level of activity is within the relevant

range.

A) $777,212

B) $220,448

C) $576,888

D) $228,416

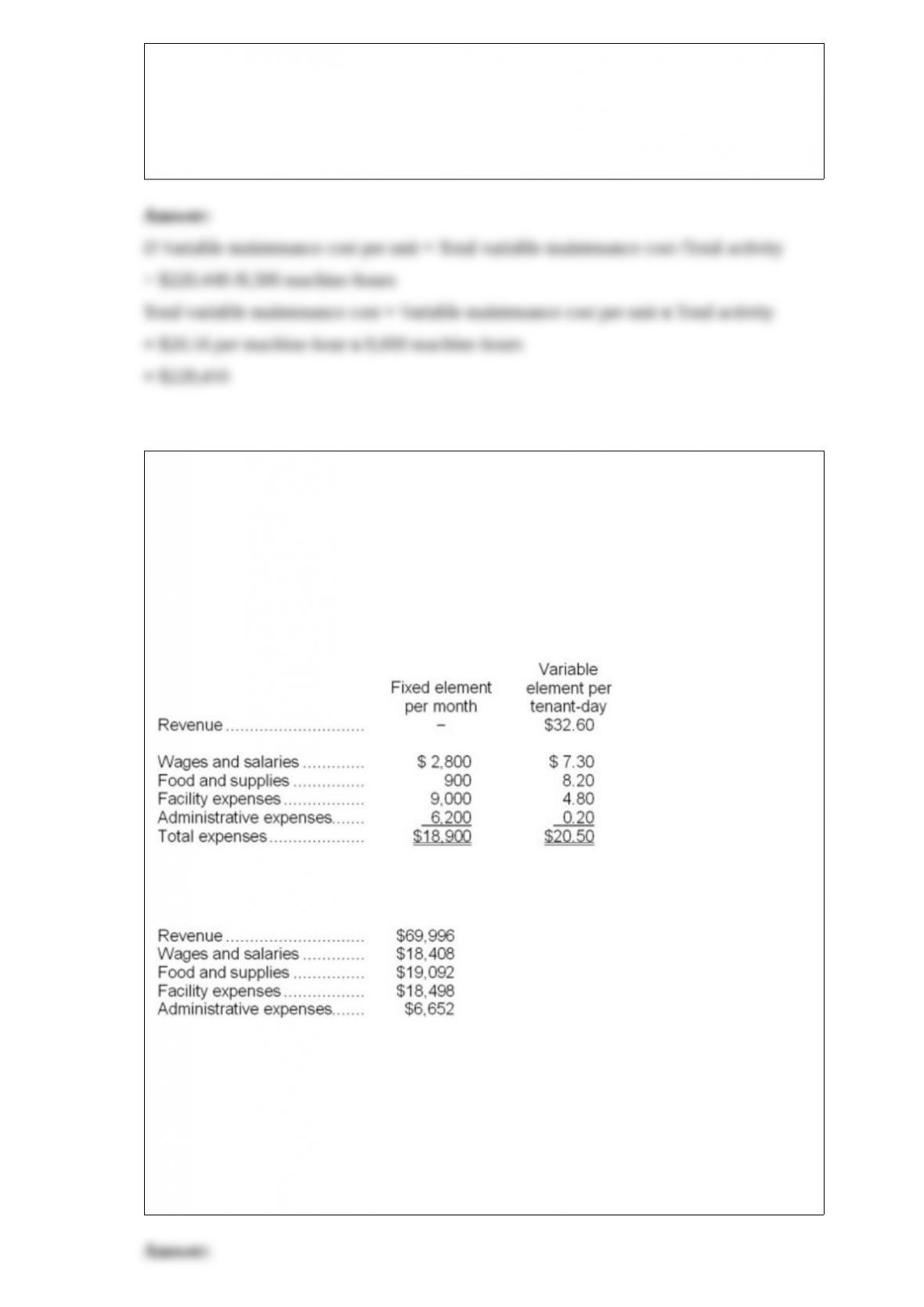

24) Perla Kennel uses tenant-days as its measure of activity; an animal housed in the

kennel for one day is counted as one tenant-day. During March, the kennel budgeted for

2,200 tenant-days, but its actual level of activity was 2,160 tenant-days. The kennel has

provided the following data concerning the formulas used in its budgeting and its actual

results for March:

Data used in budgeting:

Actual results for March:

The wages and salaries in the planning budget for March would be closest to:

A.$18,860

B.$18,749

C.$18,568

D.$18,408

25) The net present value of the entire project is closest to:

A.$39,675

B.$68,280

C.$25,515

D.$65,000

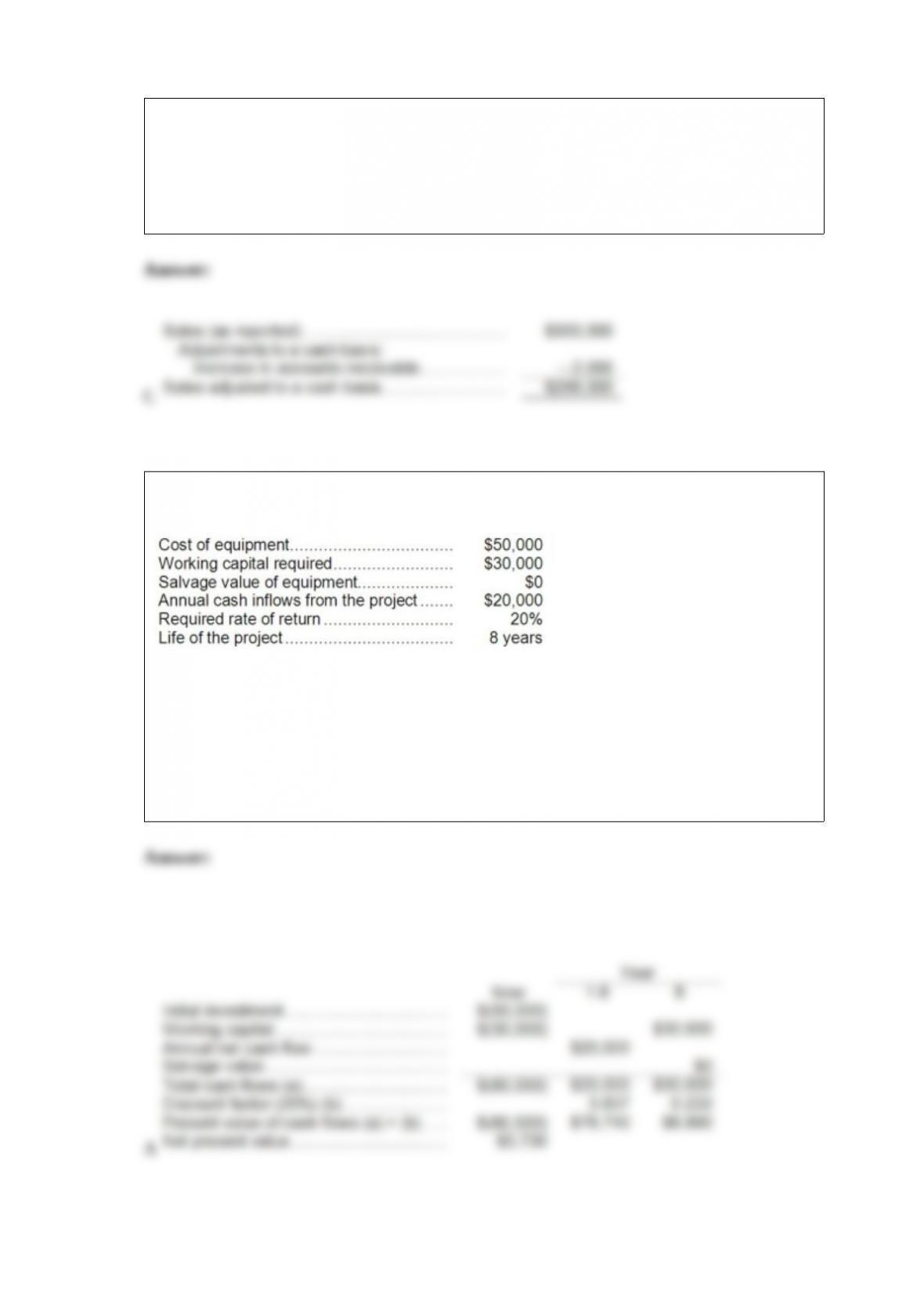

26) Using the direct method, sales adjusted to a cash basis would be:

A.$300,000

B.$302,000

C.$298,000

D.$305,000

27) ( The following data on a proposed investment project have been provided:

The working capital would be released for use elsewhere at the end of the project. The

net present value of the project is closest to:

A.$3,730

B.$0

C.$32,450

D.$88,370

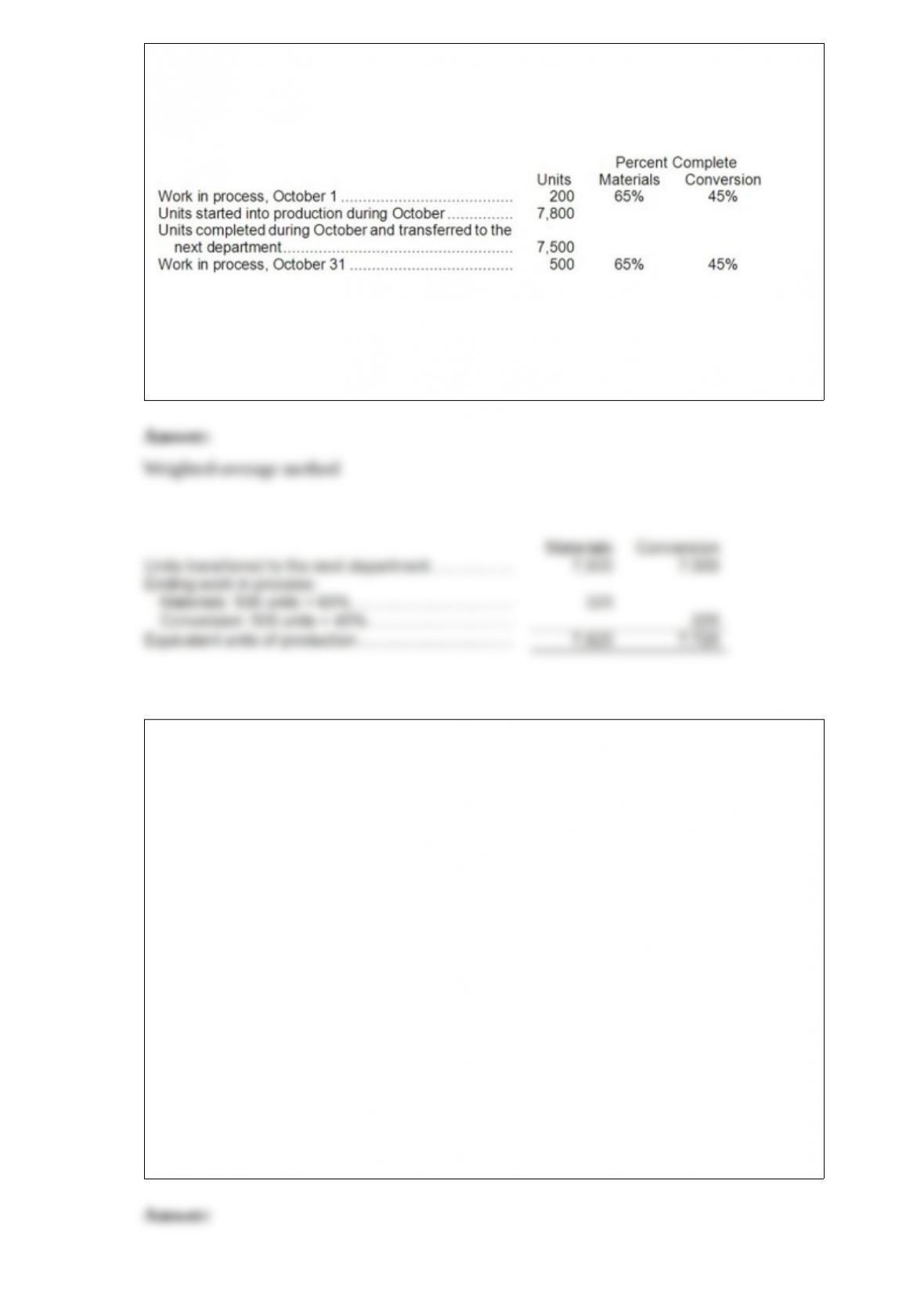

28) The following data have been provided by Allton Corporation, which uses the

weighted-average method in its process costing. The data are for the company’s Shaping

Department for October.

Required:

Compute the equivalent units of production for both materials and conversion costs for

the Shaping Department for October using the weighted-average method.

29) Zhang Corporation uses process costing. A number of transactions that occurred in

June are listed below.

(1) Raw materials that cost $41,700 are withdrawn from the storeroom for use in the

Mixing Department. All of these raw materials are classified as direct materials.

(2) Direct labor costs of $47,700 are incurred, but not yet paid, in the Mixing

Department.

(3) Manufacturing overhead of $56,900 is applied in the Mixing Department using the

department’s predetermined overhead rate.

(4) Units with a carrying cost of $128,300 finish processing in the Mixing Department

and are transferred to the Drying Department for further processing.

(5) Units with a carrying cost of $133,800 finish processing in the Drying Department,

the final step in the production process, and are transferred to the finished goods

warehouse.

(6) Finished goods with a carrying cost of $129,200 are sold.

Required:

Prepare journal entries for each of the transactions listed above.

30) Harmison Urban Diner is a charity supported by donations that provides free meals

to the homeless. The diner’s budget for July was based on 3,000 meals, but the diner

actually served 3,500 meals. The diner’s director has provided the following cost data to

use in the budget: groceries, $2.60 per meal; kitchen operations, $4,300 per month plus

$1.80 per meal; administrative expenses, $3,100 per month plus $0.80 per meal; and

fundraising expenses, $1,200 per month.

Required:

Prepare a report showing the activity variances for each of the expenses and for total

expenses for July. Label each variance as favorable (F) or unfavorable (U).

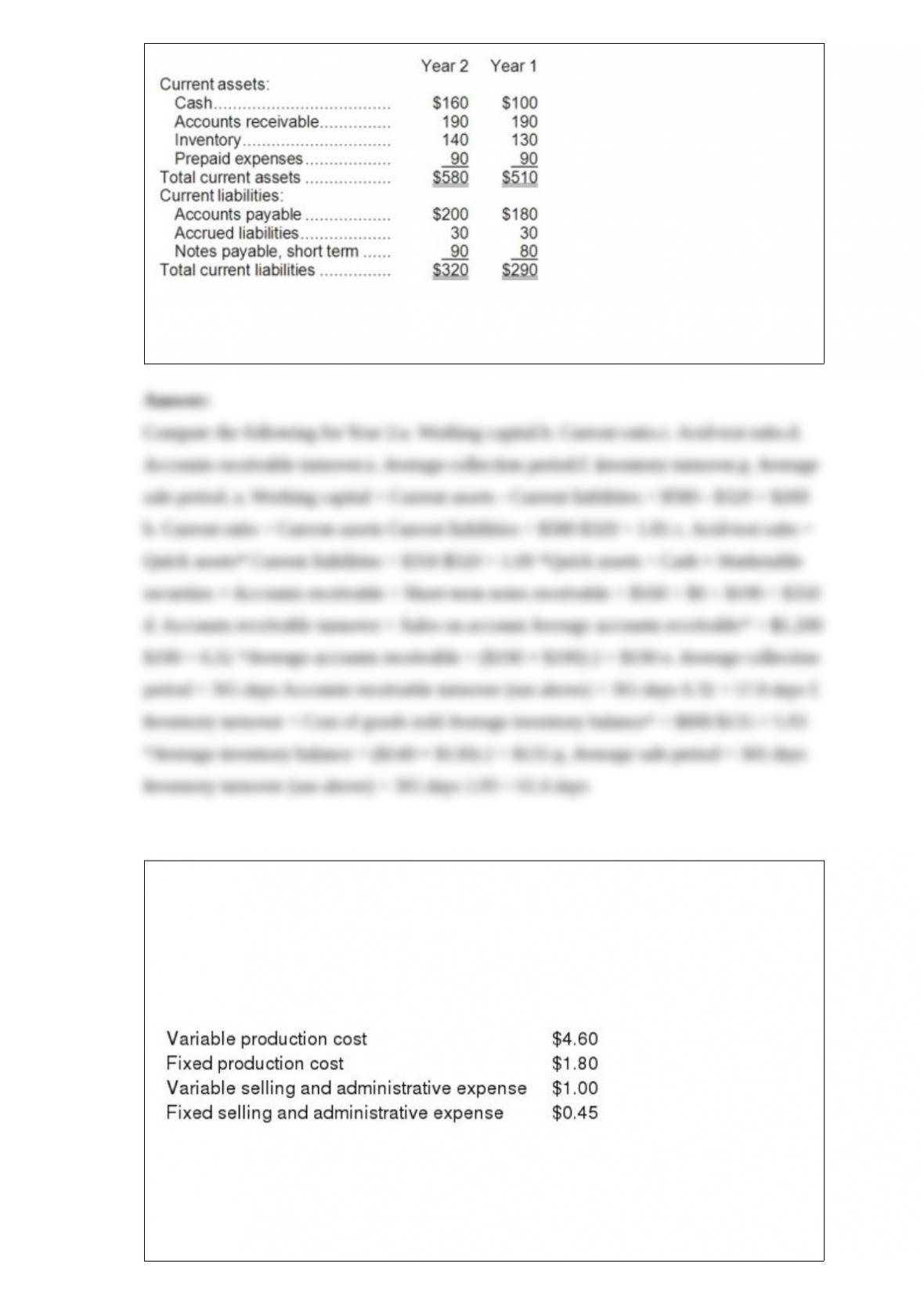

31) Excerpts from Candle Corporation’s most recent balance sheet (in thousands of

dollars) appear below:

Sales on account during the year totaled $1,200 thousand. Cost of goods sold was $800

thousand.

32) Globe Manufacturing Company has just obtained a request for a special order of

12,000 units to be shipped at the end of the current year at a discount price of $7.00

each. The company has a production capacity of 90,000 units per year. At present,

Globe is only selling 80,000 units per year through regular channels at a selling price of

$11.00 each. Globe’s per unit costs at an 80,000 unit level of production and sales are as

follows:

Variable selling and administrative expense will drop to $0.30 per unit on the special

order units. The special order has to be taken in its entirety. This means that by

accepting the special order, Globe will be forced to not sell 2,000 units to its regular

customers.

Required:

If Globe accepts this special order, by what amount will its net operating income

increase or decrease? SHOW YOUR COMPUTATIONS.

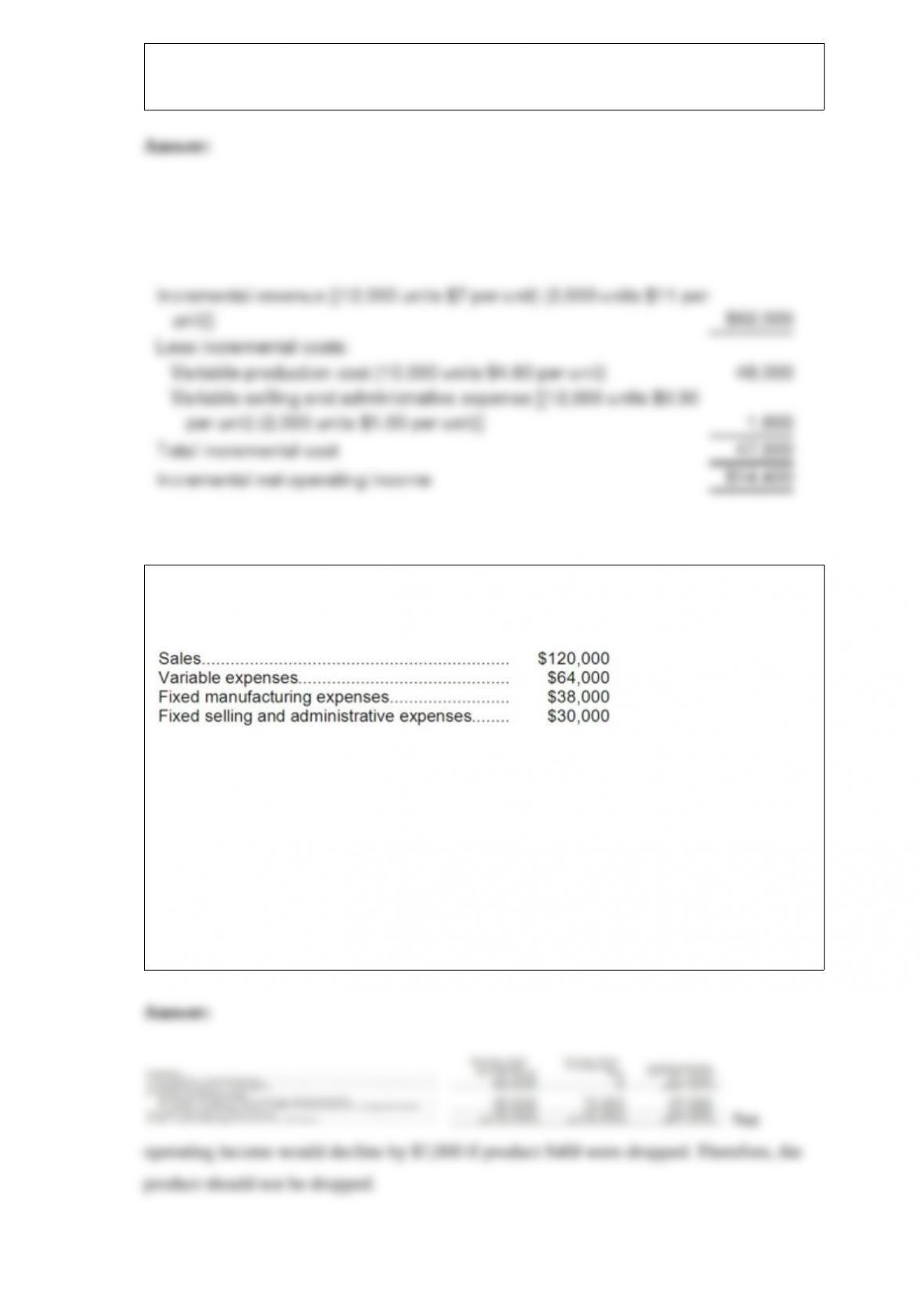

33) The management of Leinberger Corporation is considering dropping product S48J.

Data from the company’s accounting system appear below:

All fixed expenses of the company are fully allocated to products in the company’s

accounting system. Further investigation has revealed that $28,000 of the fixed

manufacturing expenses and $21,000 of the fixed selling and administrative expenses

are avoidable if product S48J is discontinued.

Required:

What would be the effect on the company’s overall net operating income if product

S48J were dropped? Should the product be dropped? Show your work!

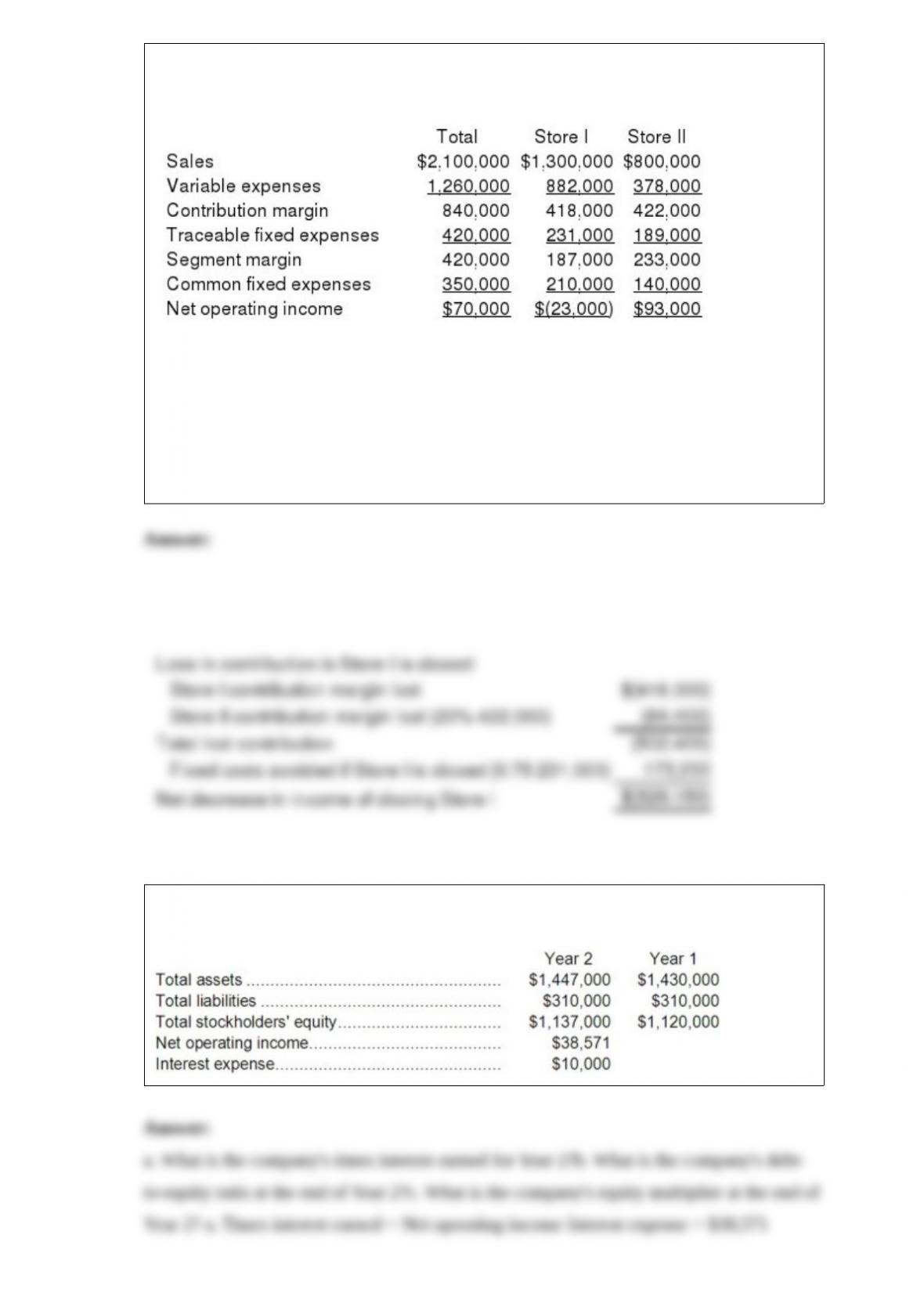

34) Northern Stores is a retailer in the upper Midwest. The most recent monthly income

statement for Northern Stores is given below:

Northern is considering closing Store I. If Store I is closed, one-fourth of its traceable

fixed expenses would continue. Also, the closing of Store I would result in a 20%

decrease in sales in Store II. Northern allocates common fixed expenses on the basis of

sales dollars and none of these costs would be saved if a store were shut down.

Required:

Compute the overall increase or decrease in the net operating income of Northern

Stores if Store I is closed.

35) Fraction Corporation has provided the following financial data:

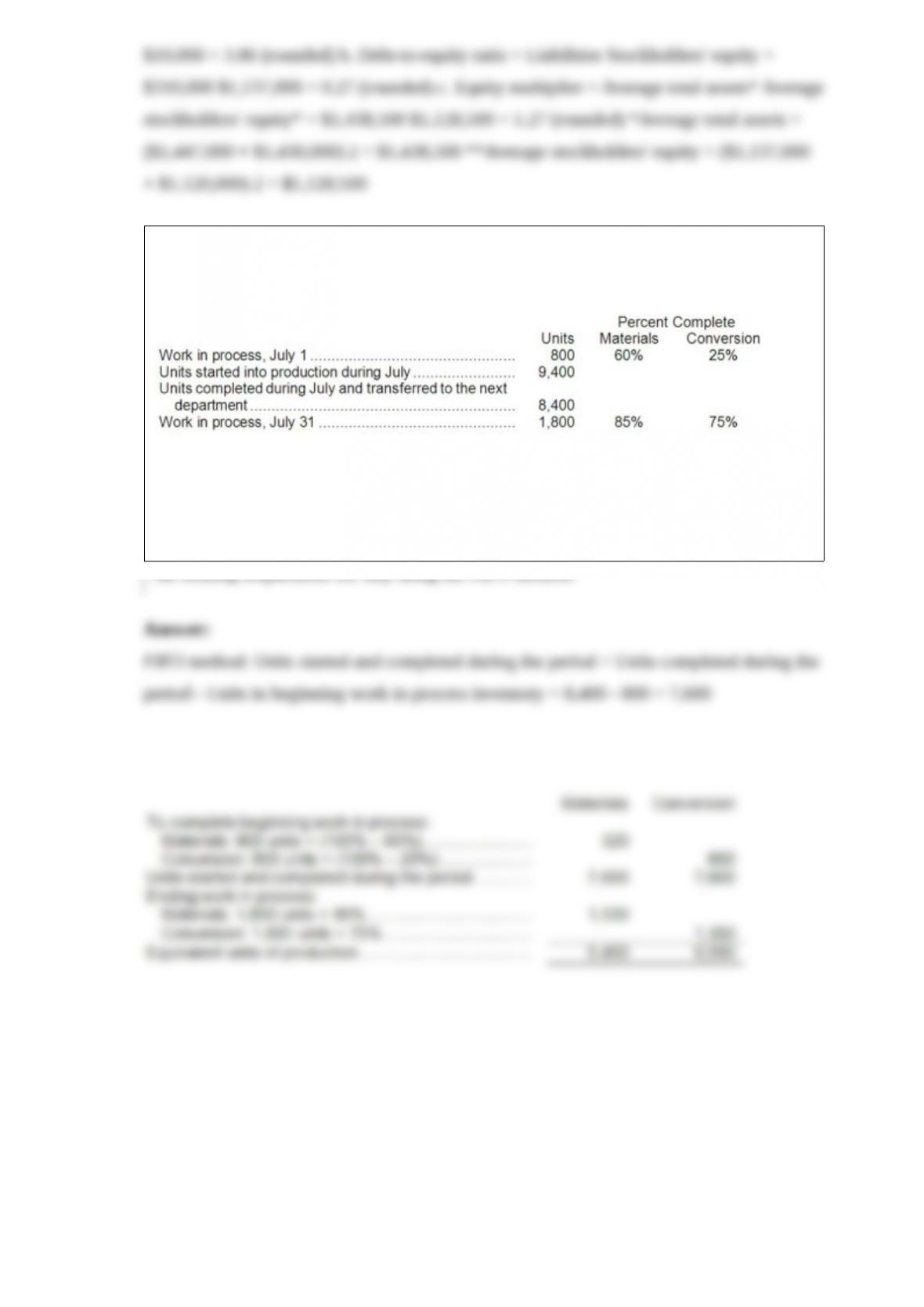

36) The following data pertain to the Milling Department of Vario Corporation for July.

The company uses the FIFO method in its process costing.

Required:

Compute the equivalent units of production for both materials and conversion costs for

the Milling Department for July using the FIFO method.