Orange Inc. offers a discount on an extended warranty on its oPhone when the warranty

is purchased at the time the oPhone is purchased. The warranty normally has a price of

$150, but Orange offers it for $120 when purchased along with an oPhone. Orange

anticipates a 75% chance that a customer will purchase the extended warranty along

with the oPhone. Assume Orange sells to 1,000 oPhones with the extended warranty

discount offer. What is the total stand-alone selling price that Orange would use for the

extended warranty discount option for purposes of allocating revenue among the

performance obligations in those 1,000 oPhone contracts?

a. $0

b. $22,500

c. $30,000

d. $120,000

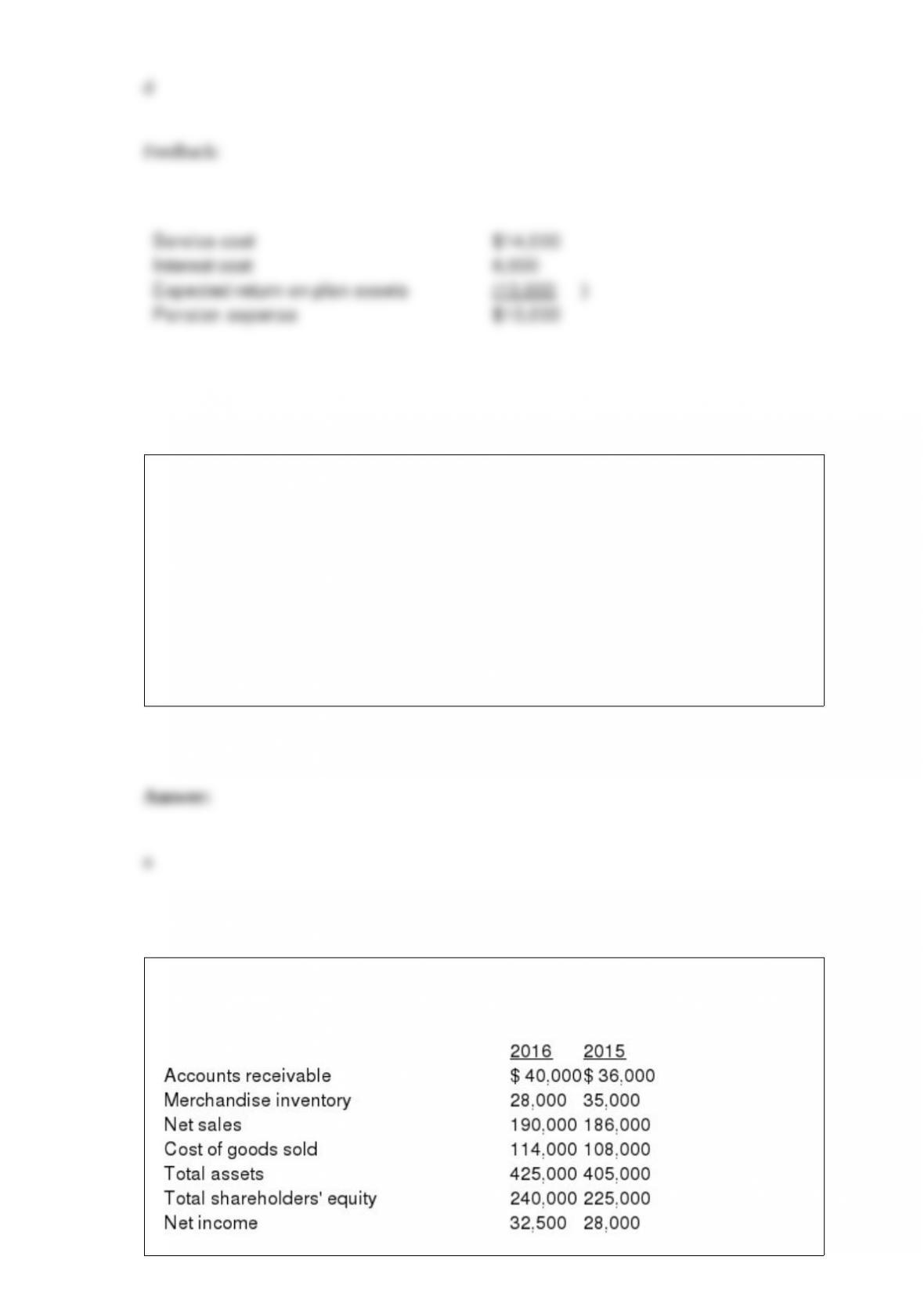

Colombo Enterprises has a defined benefit pension plan. At the end of the reporting

year, the following data were available: beginning PBO, $75,000; service cost, $14,000;

interest cost, $6,000; benefits paid for the year, $9,000; ending PBO, $89,000; and the

expected return on plan assets, $10,000. There were no other pension-related costs. The

journal entry to record the annual pension costs will include a debit to pension expense

for:

a. $20,000.

b. $15,000.

c. $12,000.

d. $10,000.

In the first year of an asset’s life, which of the following methods has the smallest

depreciation?

a. Straight-line.

b. Declining balance.

c. Sum-of-the-years’ digits.

d. Composite or group.

Excerpts from Hulkster Company’s December 31, 2016 and 2015, financial statements

are presented below:

Hulkster’s 2016 inventory turnover is (rounded):

a. 3.62.

b. 3.96.

c. 4.07.

d. 6.03.

The principal benefit of separately reporting discontinued operations is to enhance:

a. Predictive ability of future profitability.

b. Consistency in reporting.

c. Intraperiod continuity.

d. Comprehensive reporting.

On October 1, 2016, Chief Corporation declared and issued a 10% stock dividend.

Before this date, Chief had 80,000 shares of $5 par common stock outstanding. The

market value of Chief Corporation on the date of declaration was $10 per share. As a

result of this dividend, Chief’s retained earnings will:

a. Decrease by $80,000.

b. Not change.

c. Decrease by $40,000.

d. Increase by $80,000.

Which of the following is not a concern expressed by the SEC regarding IFRS adoption

by the U.S.?

a. Need for the U.S. to have strong influence on the standard-setting process and ensure

that standards meet U.S. needs.

b. The language barriers associated with cooperation among many countries in

developing IFRS.

c. The high costs to companies of converting to IFRS.

d. The fact that many laws, regulations and private contracts reference U.S. GAAP.

Assume a company has been maintaining a receivables factoring program for the past

five years and has been experiencing the same level of sales, factoring, and bad debts

over that period. Customers typically pay their receivables within 60 days. Which of the

following is true with respect to the current period (all else equal)?

a. The accounts receivable balance will decrease.

b. Cash flow from operations is stable.

c. Net income is likely to decline.

d. Accounts receivable payable within 60 days cannot be factored.

In the statement of cash flows, inflows and outflows of cash from buying and selling

available for sale securities are considered:

a. Operating activities.

b. Financing activities.

c. Investing activities.

d. Noncash financing activities.

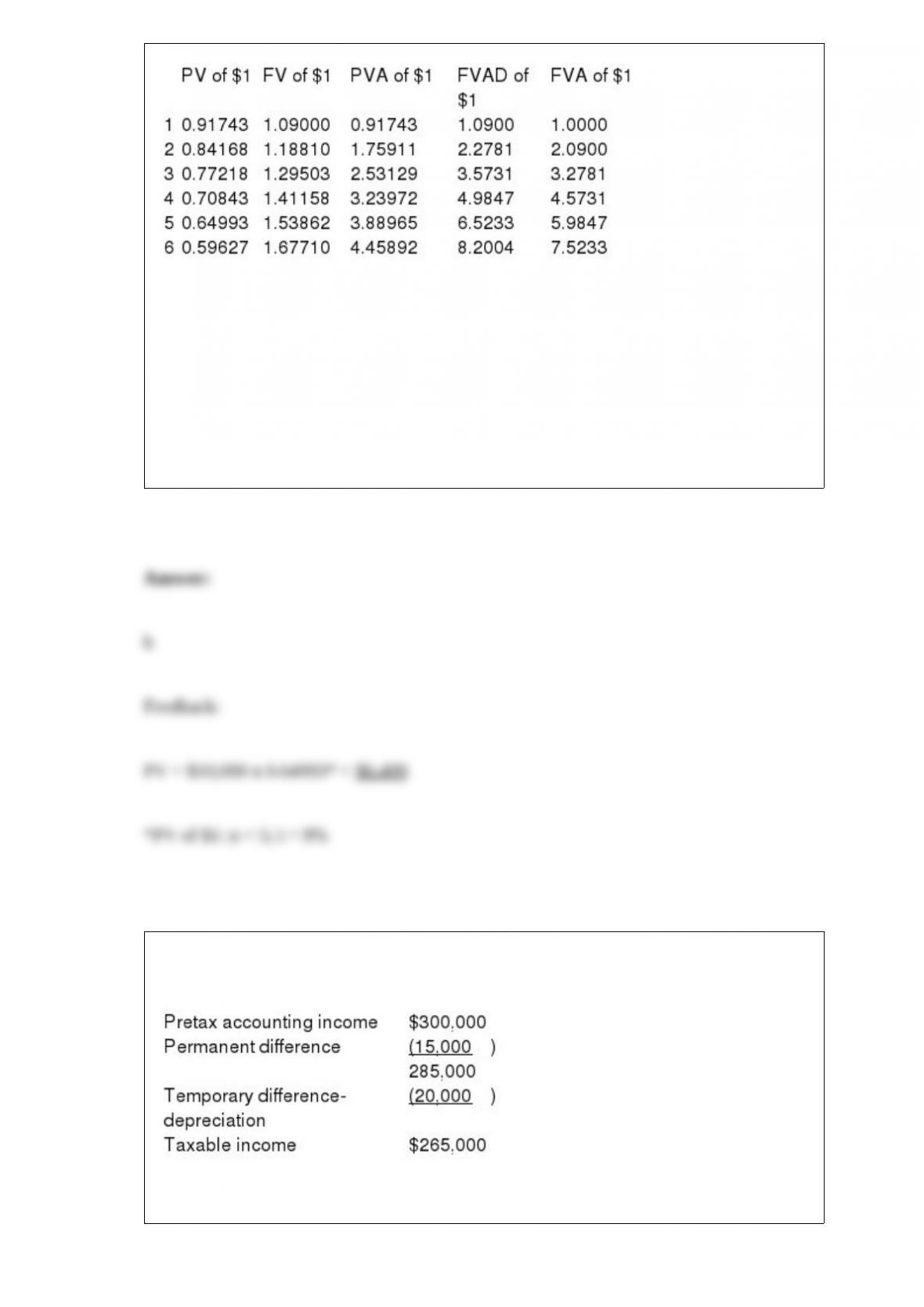

Present and future value tables of 1 at 9% are presented below.

How much must be invested now at 9% interest to accumulate to $10,000 in five years?

a. $9,176.

b. $6,499.

c. $5,500.

d. $5,960.

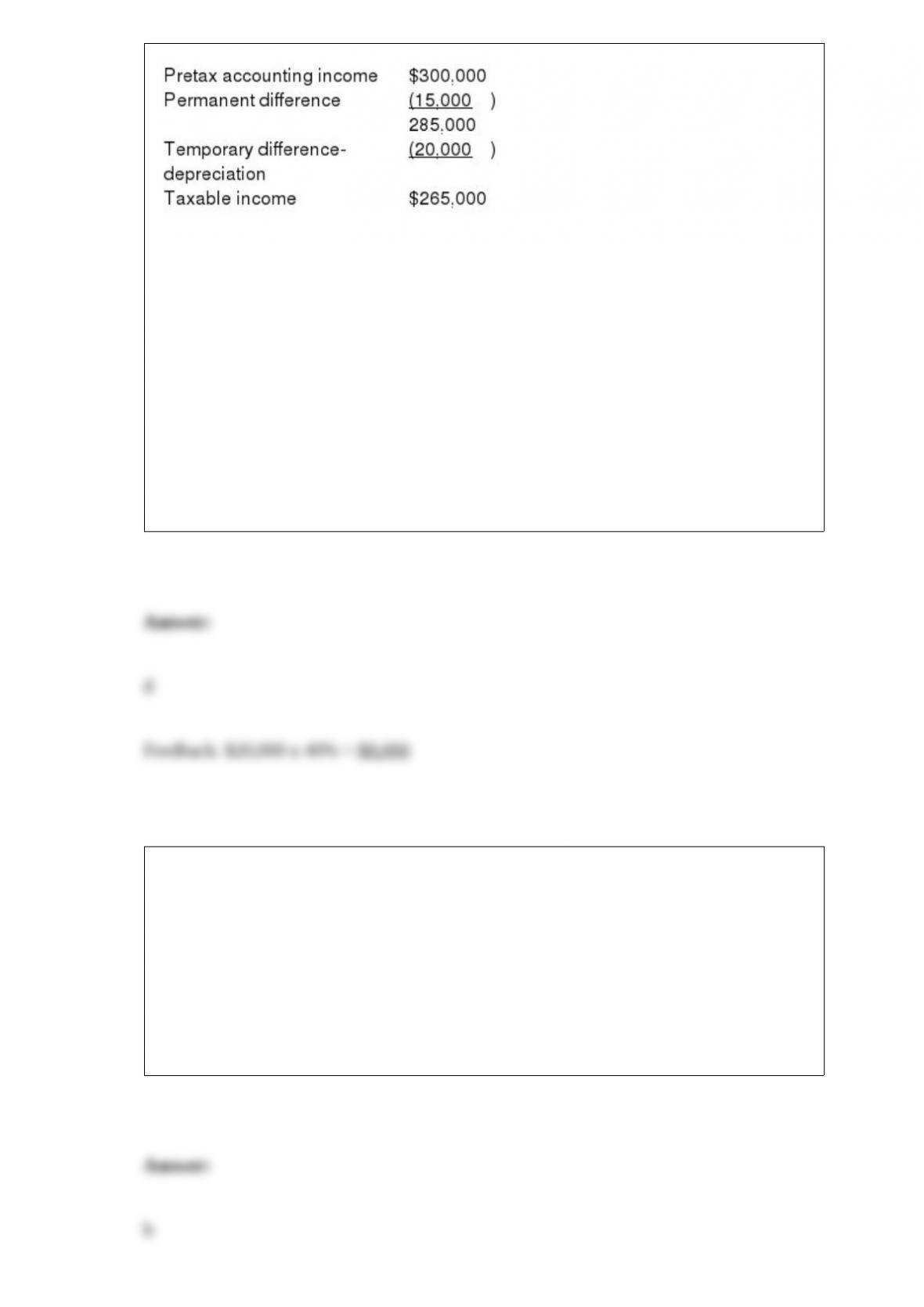

For its first year of operations, Tringali Corporation’s reconciliation of pretax

accounting income to taxable income is as follows:

Tringali’s tax rate is 40%. Assume that no estimated taxes have been paid.

Tringali’s tax rate is 40%.

What should Tringali report as its deferred income tax liability as of the end of its first

year of operations?

a. $35,000.

b. $20,000.

c. $14,000.

d. $ 8,000.

An example of an error would be:

a. Purchasing inventory from a related party.

b. Counting an inventory item twice when taking a physical inventory.

c. Holding back invoices so that accounts payable are understated.

d. Receiving kickbacks in exchange for issuing a purchase order to a vender.

Reba wishes to know how much would be in her savings account if she deposits a given

sum in an account and leaves it there at 6% interest for five years. She should use a

table for the:

a. Future value of an ordinary annuity of 1.

b. Future value of 1.

c. Future value of an annuity of 1.

d. Present value of an annuity due of 1.

Moonland Company’s income statement contained the following errors:

Ending inventory, December 31, 2016, understated by $6,000

Depreciation expense for 2016 overstated by $1,000

What is the effect of the errors on 2016 net income before taxes?

a. Overstated by $5,000.

b. Understated by $5,000.

c. Understated by $7,000.

d. Overstated by $7,000.

On September 30, 2016, Bricker Enterprises purchased a machine for $200,000. The

estimated service life is 10 years with a $20,000 residual value. Bricker records

partial-year depreciation based on the number of months in service. Depreciation for

2016, using the straight-line method is:

a. $13,500.

b. $15,000.

c. $ 4,500.

d. $ 5,000.

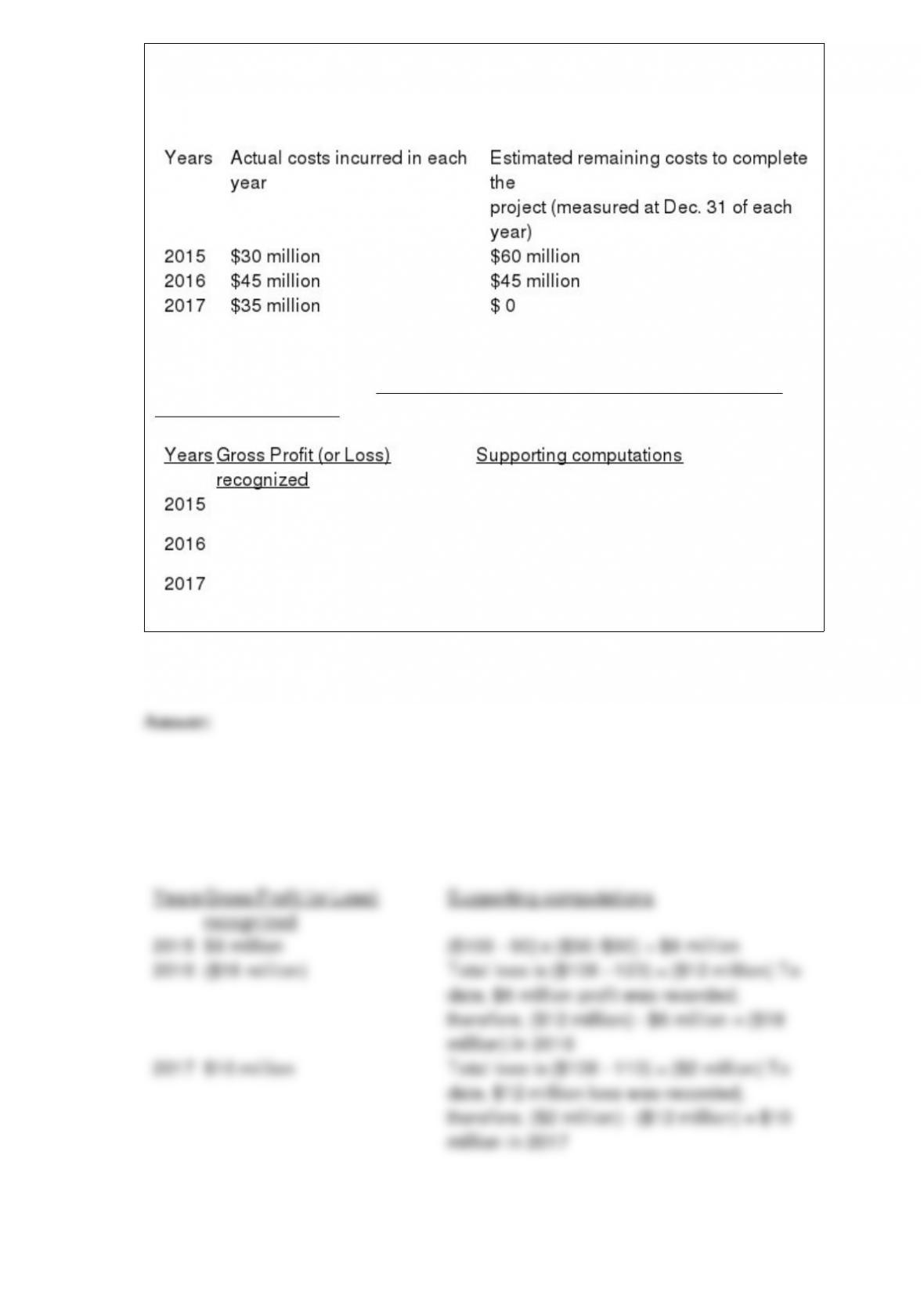

Beck Construction Company began work on a new building project on January 1, 2015.

The project is to be completed by December 31, 2017, for a fixed price of $108 million.

The following are the actual costs incurred and estimates of remaining costs to

complete the project that were made by Beck’s accounting staff:

Required: What amount of gross profit (or loss) would Beck record on this project in

each year, assuming that Beck recognizes revenue for this project over time according

to percentage of completion? Place answers in the spaces provided below and show

supporting computations.

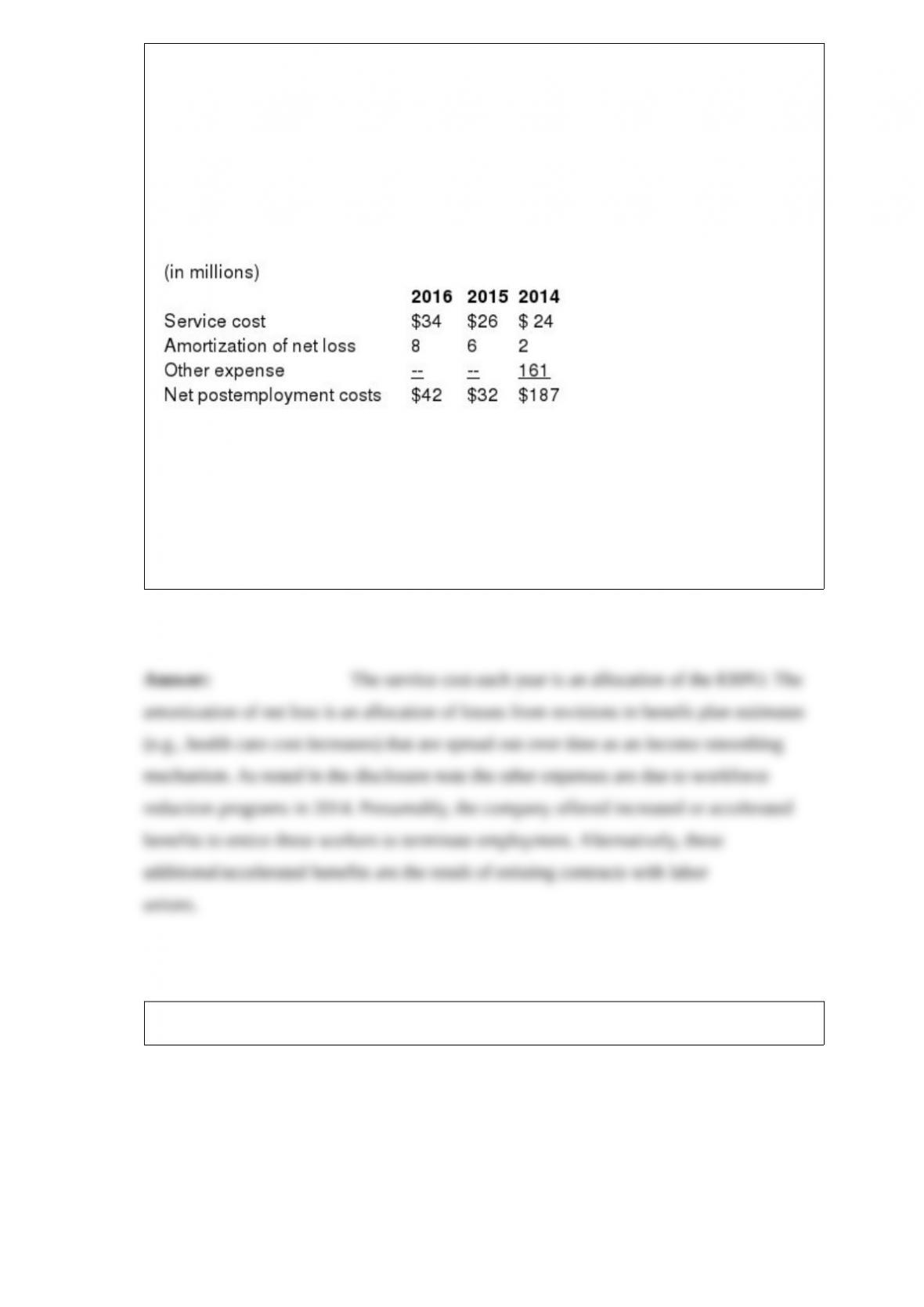

In its 2016 annual report to shareholders, Livey Companies Inc. (LCI) disclosed the

following information regarding its postemployment benefit plans:

The Company and certain of its affiliates sponsor postemployment benefit plans

covering substantially all salaried and certain hourly employees. The cost of these plans

is charged to expense over the working life of the covered employees. Net

postemployment costs consisted of the following for the years ended December 31,

2016, 2015, and 2014:

The company instituted workforce reduction programs in its North American food

operations in 2014. These actions resulted in incremental postemployment costs, which

are shown as other expense above.

Required:

Describe the three components in the net postemployment costs disclosed by LCI.

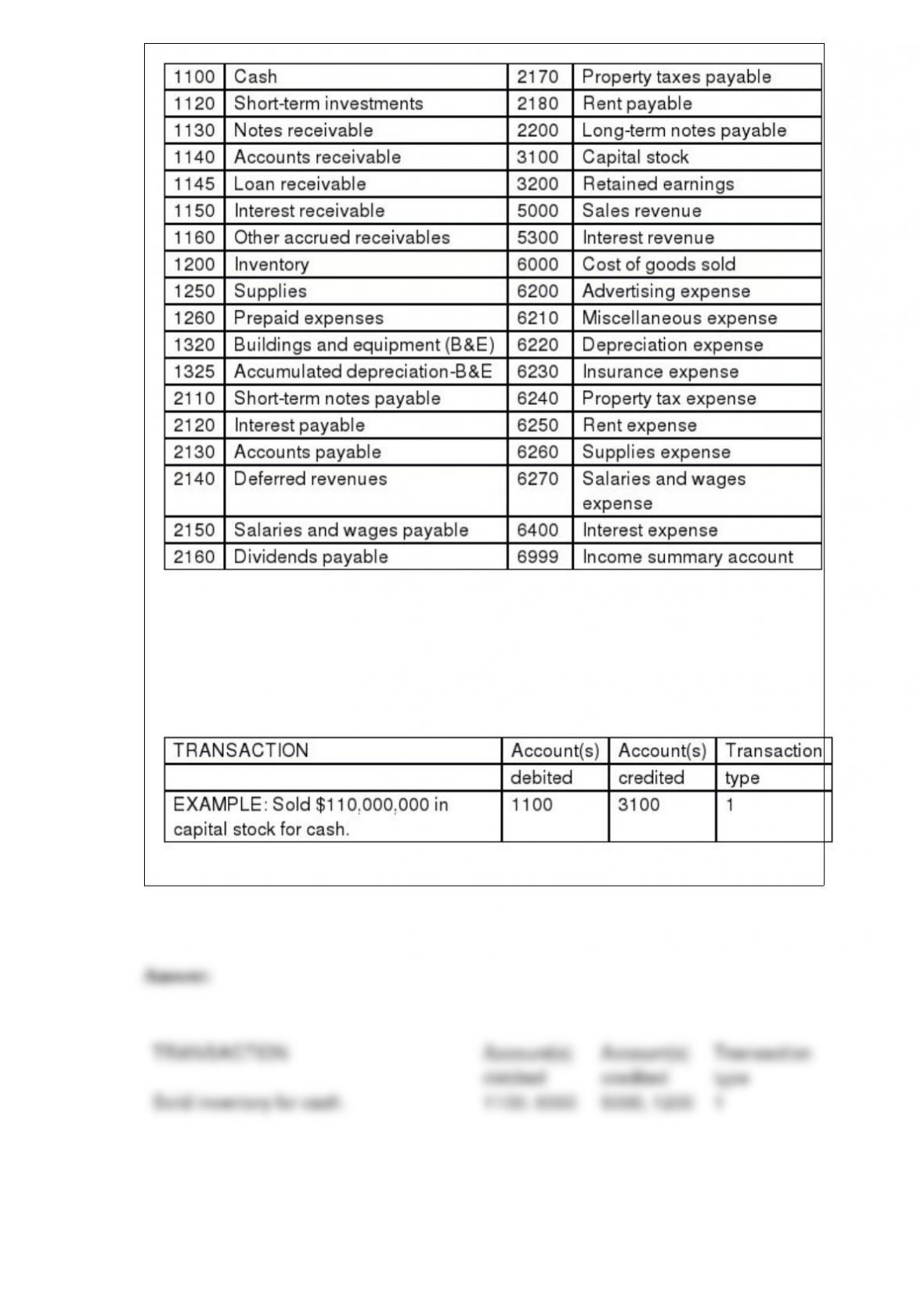

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Sold inventory for cash.

Diversified Industries sells perishable electronic products. Some must be shipped in

reusable containers. Customers pay a deposit for each container. The deposit is equal to

the container’s cost. Customers receive a refund when the container is returned. During

2016, deposits collected on containers shipped were $700,000. Deposits are forfeited if

containers are not returned in 18 months. Containers held by customers on January 1,

2016, were $330,000. During 2016, $410,000 was refunded and deposits of $25,000

were forfeited.

Required:

1> Prepare the appropriate journal entries for the deposits received and returned during

2016.

2> Determine the liability for refundable deposits to be reported in the December 31,

2016, balance sheet.