Which of the following situations best describes a familiarity threat?

A) Design and implementation of a new payroll system

B) Preparation and entry of bookkeeping transactions

C) Completion of corporate transactions for subsidiary companies

D) PA has been working with this client for ten years, first as a manager, now as a

partner

One of the ways to eliminate nonsampling risk is through

A) proper supervision and instruction of the client’s employees.

B) proper supervision and instruction of the audit team.

C) the use of attribute sampling rather than variables sampling.

D) controls which ensure that the sample drawn is random and representative.

In Canada, publicly traded companies are

A) required to have audits.

B) strongly encouraged to have audits.

C) not required to have an audit if they have a review.

D) not required to have an audit.

An adverse opinion is issued when the auditor believes

A) some parts of the financial statements are materially misstated or misleading.

B) the financial statements will be found to be misleading or misstated, if an adequate

investigation is performed.

C) the overall financial statements are so materially misstated or misleading as a whole

that they do not present fairly the financial position or results of operations and changes

in financial position.

D) the audit firm is not independent.

Jessica is a summer junior at Branes & Castle, a PA firm. Jessica has only completed 3

accounting courses in university and has not yet taken her auditing class. A team of

auditors from Branes & Castle are starting the audit and Jessica was sent to help them.

Jessica

A) can perform work for the audit engagement as long as she is supervised and proper

review of her work is performed.

B) should not perform any work pertaining to the audit engagement since she doesn’t

have sufficient knowledge.

C) should be limited to assisting the audit team with support functions such as

photocopies and file assembly.

D) can perform work for the audit engagement on cycles where risk was assessed as

low.

An example of an external document is

A) a cancelled cheque.

B) employees’ time reports.

C) inventory receiving reports.

D) the minutes of the Board of Directors’ meetings.

Inquiries of management are used to help identify subsequent events. To help obtain

meaningful answers

A) the standard firm checklist should be followed.

B) these inquiries must be conducted with the proper client personnel.

C) the inquiries should be conducted by senior audit personnel.

D) they should be asked after the effective date of the audit report.

Sean Clem has done a review engagement and prepared the tax return for your web

design business for the last five years. The books and records have always been well

organized, although year end adjusting entries have been required. You do some of the

accounting yourself and the rest of the accounting records are handled by your wife,

who is also an employee of the business.

This year, you would like to expand your business to provide ISP (internet service

provider) services to your clients. This would entail you purchasing additional computer

equipment and software. You are also considering hiring an additional employee (you

currently have three), and you are looking at obtaining a loan for $100,000 from the

bank. The bank says that you should have your records audited, but you are not sure

what this will mean.

Required:

A) What would Sean say to you about the differences between an audit and a review?

B) Identify the issues that Sean needs to consider during the planning of the audit.

Audit risk is assessed at which level of the audit?

A) account

B) cycle

C) transaction-related audit objective

D) overall audit

In addition to including on each working paper the name of the client, the period

covered, the date of preparation and an index code, each working paper should clearly

include

A) the name of the preparer and a description of the contents.

B) symbols used and a reconciliation to the general ledger balance.

C) audit working paper steps that were completed.

D) the nature of the transaction-based risk that is being audited.

All other factors held constant, if the auditor decreases audit risk then

A) there will be less documentation in the audit file.

B) total audit evidence and audit costs will increase.

C) it will also be necessary to decrease either control risk or inherent risk.

D) less supervision will be required of the audit team.

The auditor has determined that the perpetual inventory master files are high quality,

assessing control risk related to physical observation of inventory as low. How does this

affect audit testing? The auditor may

A) reduce the extent of control tests over data entry to the master file.

B) reduce the extent of the tests of physical inventory.

C) reduce the extent of control tests with respect to program change controls.

D) increase assessed inherent risks over the tests of physical inventory.

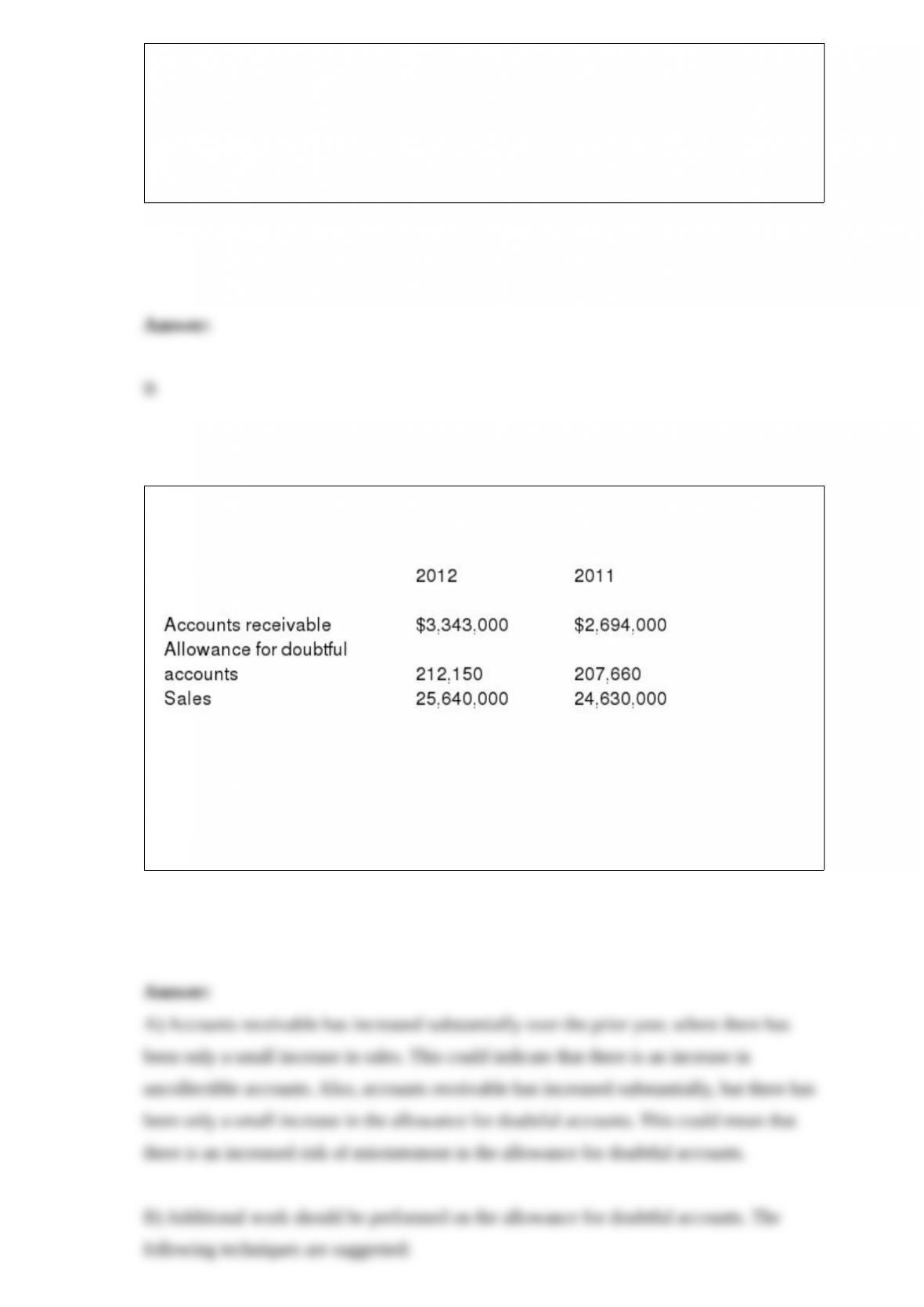

You are conducting an audit and have obtained the following figures with respect to

sales and accounts receivable:

Required:

A) What are the audit implications of these figures?

B) Identify key audit steps that you would perform for any of the above accounts.

The accuracy of the results of the accounting system (account balances) is heavily

dependent upon the

A) knowledge and skills of the auditor.

B) adequacy of the entity level controls.

C) accuracy of the inputs and processing (transactions).

D) training provided to the personnel.

As part of the audit of sales, the auditor has used attribute sampling to select a sample

of sales invoices. The auditor has examined the duplicate sales invoice to determine

whether it was approved for credit. Which of the following would be termed the

“exception?” The

A) sales invoice number.

B) approval initials.

C) name of the person who approves credit.

D) absence of an authorization.

Analytical procedures are substantive tests and, if the results of the analytical

procedures are favourable, they will reduce

A) the extent of tests of details of balances.

B) the extent of tests of controls.

C) the analytical procedures.

D) all of the other tests.

Which portions of the code of professional conduct are enforceable?

A) Principles and rules

B) The rules of conduct

C) Interpretations

D) Rules and interpretations

Which of the following is the best example of objective evidence?

A) a letter written by a client’s lawyer discussing the likely outcome of outstanding

lawsuits

B) the physical count of securities and cash by the auditor

C) inquiries of the credit manager about the collectability of noncurrent accounts

receivable

D) observation of cobwebs on some inventory bins

The methods that management uses to supervise the entity’s activities are called

A) personnel practices.

B) management control methods.

C) methods of assigning authority and responsibility.

D) management’s operating style.

Frank has discovered that his employer is part of a group of banks that is manipulating

interest rates. He would like to stop this practice at his employer, and is not sure how

best to talk to his boss. He has heard of the GVV (Giving Voice to Values) approach,

and thinks he may be able to use it successfully because his company has recently

implemented new initiatives to empower employees to speak of improvements to

business practices Frank has identified who is affected, what is at stake for them, and

how to connect with them. What is his next step, using the GVV analysis framework?

A) list the values underpinning the different positions in the conflict

B) consider his personal and professional purpose and choice in this situation

C) practice what he is going to say, with help from a mentor or coach

D) craft a useful, powerful response that he could use, taking into account multiple

options

The fact that a client has a material accounting departure for failure to follow ASPE

would require the accountant to disclose that fact in a separate reservation paragraph,

when the accountant is performing

A) a compilation.

B) a review and an audit.

C) either a compilation or a review.

D) neither a compilation nor a review, only an audit.

Heavy Manufacturing Company is in the business of making steel plates, forming

heavy metal slabs and drilling and scoring metals. Recently, it upgraded many of its

forming machines. There were five machines purchased on four different invoices.

Unfortunately, one of the invoices was recorded twice, resulting in five invoices being

recorded. The general balance-related audit objective affected by this activity is

A) completeness.

B) accuracy.

C) classification.

D) existence.

What is the size of most public accounting firms in Canada?

A) fewer than 25 employees

B) between 25 and 49 employees

C) between 50 and 75 employees

D) more than 75 employees

The test of details of balance procedure which requires the auditor to perform tests of

lower-of-cost-or-market, selling price, and obsolescence is an attempt to satisfy the

objective of

A) existence.

B) completeness.

C) accuracy.

D) valuation.

A common inventory observation procedure is to record in the working papers for

subsequent follow-up the last shipping document number used at year-end. The audit

objective being achieved by this procedure is

A) inventory as recorded exists.

B) existing inventory is counted and tagged.

C) information is obtained to make sure sales and inventory purchases are recorded in

the proper period.

D) tags are accounted for to make sure none is missing.

One of the causes of nonsampling error is

A) the use of inappropriate or ineffective audit procedures.

B) failure to draw a random sample.

C) failure to draw a representative sample.

D) the use of attribute sampling instead of variables sampling.

The auditing standards indicate that

A) it is preferable to use statistical sampling instead of non-statistical sampling.

B) it is preferable to use non-statistical sampling instead of statistical sampling.

C) it is equally acceptable to use either statistical or non-statistical sampling.

D) non-statistical sampling should only be used if statistical sampling is too costly to

use.

You are working on the testing of internal controls over price changes in the inventory

system. You completed the controls testing to determine whether all price changes were

approved by the senior accountant, by reference to master file change forms.

In order to place reliance on this control, your audit supervisor has decided that the

error rate in the population should be less than 1%. When you calculated your sample

size, you used a confidence level of 90% and predicted an error rate in the population of

less than one percent. Based on these decisions, you examined 150 inventory price

master file change forms.

In your testing, you uncovered two deviations. Based on these results, you calculate that

the actual error rate in the population could be as high as 2.33 %.

Required:

A) What actions are available to you regarding your planned reliance on the master file

change controls?

B) What are the advantages and disadvantages of each action?

C) How would you decide which action to take?

The acceptable risk of incorrect acceptance (ARIA) has a significant effect on sample

size. The relationship of ARIA to sample size is

A) direct (larger ARIA = larger sample).

B) inverse (larger ARIA = smaller sample).

C) variable (sometimes larger, sometimes smaller).

D) not determinable.

The two primary classes of transactions in the sales and collection cycle are

A) sales and sales returns.

B) sales and sales discounts.

C) sales and accounts receivable.

D) sales and cash receipts.

After the auditor has completed all the procedures, it is necessary to combine the

information obtained to reach an overall conclusion as to whether the financial

statements are fairly presented. This is a highly subjective process that relies heavily on

A) generally accepted auditing standards.

B) the provincial institutes’ Rules of Professional Conduct.

C) generally accepted accounting principles.

D) the auditor’s professional judgment.

If the amount of a probable loss on a contingent liability cannot be estimated, but the

event is likely, the liability should be

A) accrued and indicated in the body of the financial statements.

B) disclosed in footnotes, but not accrued.

C) neither accrued nor disclosed in footnotes.

D) disclosed in the auditor’s report but not disclosed on the financial statements.

Evidence is generally considered appropriate when

A) it has the qualities of being relevant, objective, and free from known bias.

B) there is enough of it to afford a reasonable basis for an opinion on financial

statements.

C) it has been obtained by random selection.

D) it consists of written statements made by managers of the enterprise under audit.