According to International Financial Reporting Standards, all research and development

expenditures are expensed in the period incurred.

With an annuity due, a payment is made or received on the date the agreement begins.

Income statements prepared according to both U.S. GAAP and International Financial

Reporting Standards require the separate reporting of discontinued operations.

Companies must always use the equity method when they hold between 25% and 50%

of the common stock of an investee.

Both debt and equity securities can be categorized as trading securities.

Securities classified as held to maturity could be reported as either current or long-term

in a classified balance sheet, depending upon their maturity dates.

Goods and services are distinct if they are either capable of being distinct or are

separately identifiable.

Intangible assets usually are reported in the balance sheet as current assets.

The sale of merchandise on account would be recorded in a sales journal.

Adjusting journal entries are recorded at the end of any period when financial

statements are prepared.

Except for tax considerations the potentially dilutive effect of convertible preferred

stock is handled in EPS calculations in much the same way as convertible debt.

Unlike the Social Security tax there is no maximum wage base for the Medicare portion

of the FICA tax.

The post-closing trial balance contains only permanent accounts.

When accounting for multiple-element software arrangements, the revenue for each

element is based on the separate prices stated for each element in the software contract.

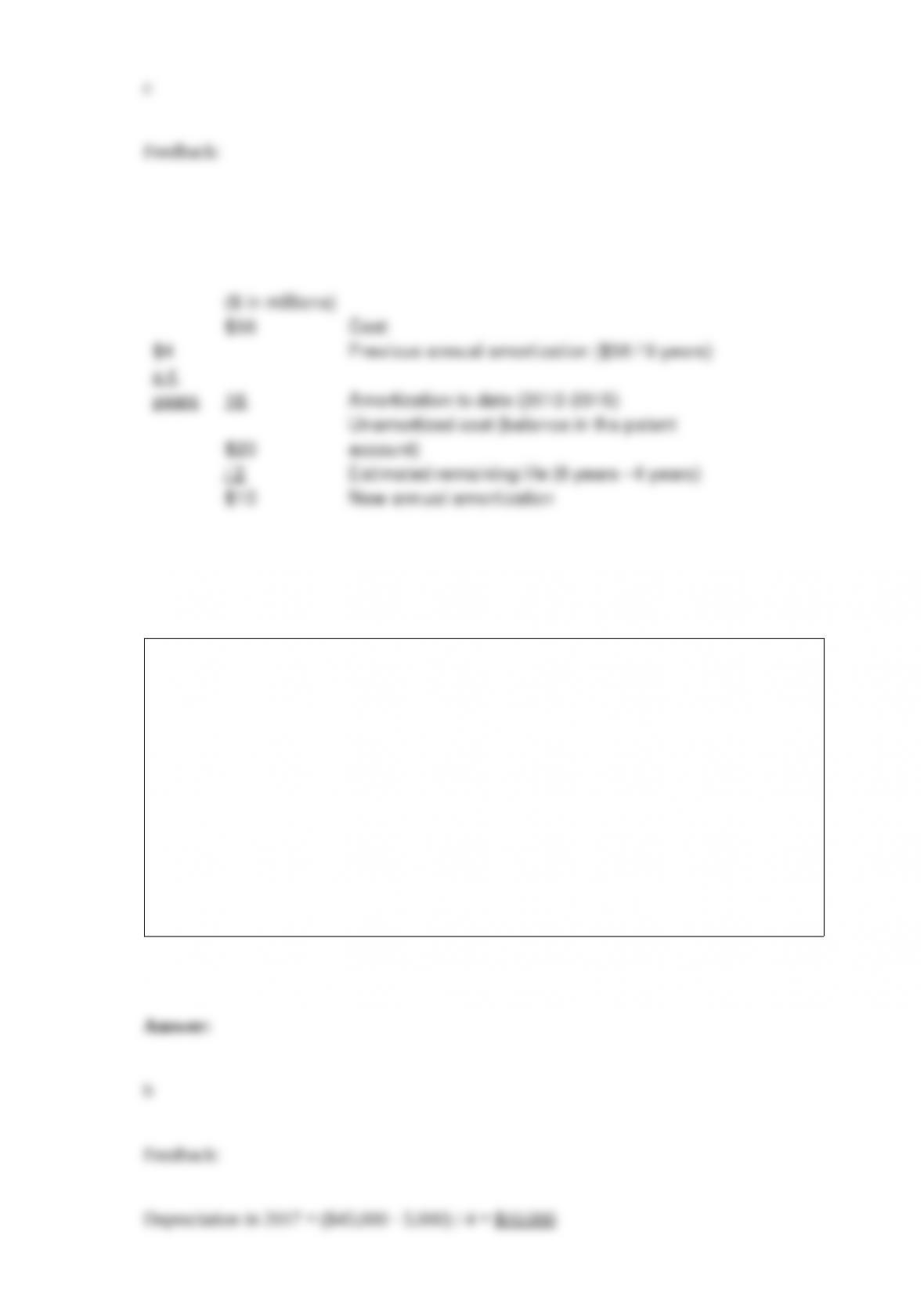

Blue Co. has a patent on a communication process. The company has amortized the

patent on a straight-line basis since 2012, when it was acquired at a cost of $36 million

at the beginning of that year. Due to rapid technological advances in the industry,

management decided that the patent would benefit the company over a total of six years

rather than the nine-year life being used to amortize its cost. The decision was made at

the end of 2016 (before adjusting and closing entries). What is the appropriate patent

amortization expense in 2016?

a. $ 4 million.

b. $ 5 million.

c. $10 million.

d. $20 million.

Archie Co. purchased a framing machine for $45,000 on January 1, 2016. The machine

is expected to have a four-year life, with a residual value of $5,000 at the end of four

years. Using the straight-line method, depreciation for 2017 and book value at

December 31, 2017, would be:

a. $10,000 and $20,000.

b. $10,000 and $25,000.

c. $11,250 and $17,500.

d. $11,250 and $22,500.

An investment product promises to pay $42,000 at the end of 10 years. If an investor

feels this investment should produce a rate of return of 12%, compounded annually,

what’s the most the investor should be willing to pay for the investment? a. $ 15,146.

b. $ 13,523.

c. $ 42,000.

d. $130,446.

Which of the following is reported as an operating activity in the statement of cash

flows?

a. The purchase of long-lived assets.

b. The acquisition of treasury stock.

c. The retirement of bonds.

d. The payment of prepaid insurance.

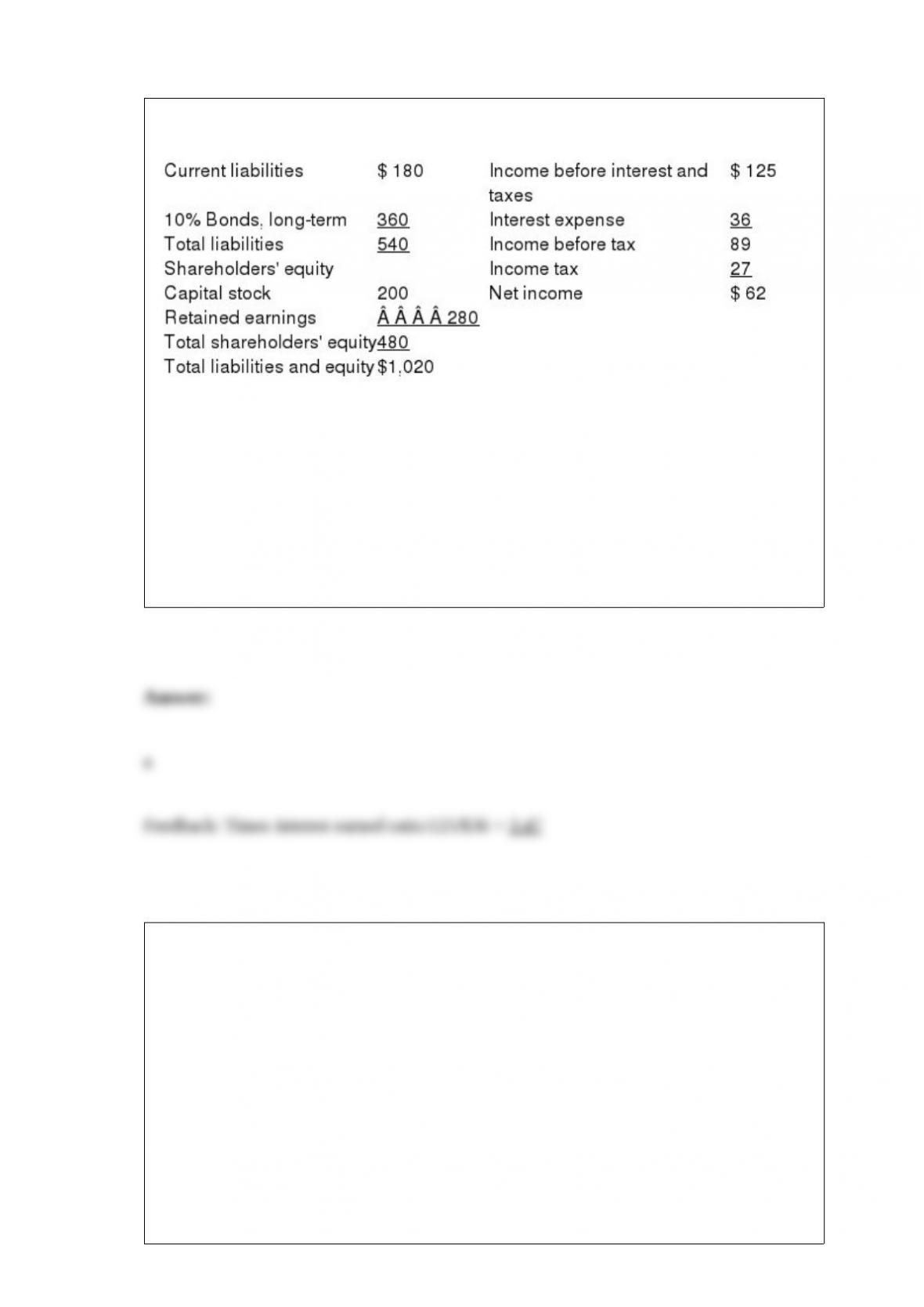

Recent financial statement data for Harmony Health Foods (HHF) Inc. is shown below.

HHF’s times interest earned ratio is (rounded):

a. 3.47.

b. 1.73.

c. 2.47.

d. 10.0.

Reliable Enterprises sells distressed merchandise on extended credit terms. Collections

on these sales are not reasonably assured, and bad debt losses cannot be reasonably

predicted. It is unlikely that repossessed merchandise is in condition to be re-sold.

Therefore, Reliable uses the cost recovery method. Merchandise costing $30,000 was

sold for $55,000 in 2015. Collections on this sale were $20,000 in 2015, $15,000 in

2016, and $20,000 in 2017.

In 2017, Reliable would recognize gross profit of:

a. $0.

b. $ 6,000.

c. $ 8,000.

d. $20,000.

To evaluate the risk and quality of an individual bond issue, savvy investors rely

heavily on:

a. Bond ratings provided by financial investment services such as Moody’s.

b. Newspaper articles.

c. Bond interest payments.

d. The company’s audit report.

Nickel Inc. bought $100,000 of 3-year, 6% bonds as an investment on December 31,

2015 for $106,000. Nickel uses straight-line amortization. On May 1, 2016, $10,000 of

the bonds were redeemed at 110. As a result of the retirement, MSG will report:

a. a $467 gain.

b. a $467 loss.

c. a $1,000 gain.

d. a $5,000 loss.

On January 1, 2016, Ozark Minerals issued $20 million of 9%, 10-year convertible

bonds at 101. The bonds pay interest on June 30 and December 31. Each $1,000 bond is

convertible into 40 shares of Ozark’s no par common stock. Bonds that are similar in all

respects, except that they are nonconvertible, currently are selling at 99. Ozark applies

International Financial Reporting Standards (IFRS). Upon issuance, Ozark should:

a. Credit bonds payable $19,800,000.

b. Credit premium on bonds payable $200,000.

c. Credit equity $200,000.

d. Credit bonds payable $20,200,000.

Lake Power Sports sells jet skis and other powered recreational equipment. Customers

pay one-third of the sales price of a jet ski when they initially purchase the ski, and then

pay another one-third each year for the next two years. Because Lake has little

information about the ability to collect these receivables, it uses the cost recovery

method to recognize revenue on these installment sales. In 2015, Lake began operations

and sold jet skis with a total price of $900,000 that cost Lake $450,000. Lake collected

$300,000 in 2015, $300,000 in 2016, and $300,000 in 2017 associated with those sales.

In 2016, Lake sold jet skis with a total price of $1,500,000 that cost Lake $900,000.

Lake collected $500,000 in 2016, $400,000 in 2017, and $400,000 in 2018 associated

with those sales. In 2018, Lake also repossessed $200,000 of jet skis that were sold in

2016. Those jet skis had a fair value of $75,000 at the time they were repossessed.

In 2015, Lake would recognize realized gross profit of:

a. $150,000.

b. $0.

c. $300,000.

d. $450,000.

Assume a contract for the sale of goods specifies that payment is to be made 15 months

prior to delivery of a product. The seller is likely to do which of the following with

respect to the time value of money over the life of the contract?

a. Recognize interest expense.

b. Recognize interest revenue.

c. Recognize additional cost of goods sold.

d. Ignore the time value of money.

“VSOE” is necessary to separately recognize revenue in multiple-element contracts for:

a. All service contracts.

b. All product contracts.

c. All contracts that involve at least one non-software element.

d. Software contracts.

The reporting of earnings per share is required only for:

a. Private companies.

b. Companies with complex capital structures.

c. Publicly traded corporations.

d. Medium-sized and large corporations.

In which of the following is the option described not a performance obligation?

a. Customers accumulate points for every dollar spent at Madeline’s Book Store. The

points can be redeemed for books once certain levels are met.

b. Customers can get 5% cash back for every $100 spent on eco-friendly products.

c. Customers can “buy two, get one free” at a menswear store.

d. Upon purchase of any name-brand TV, customers can purchase a 5-year extended

warranty at a 25% discount.

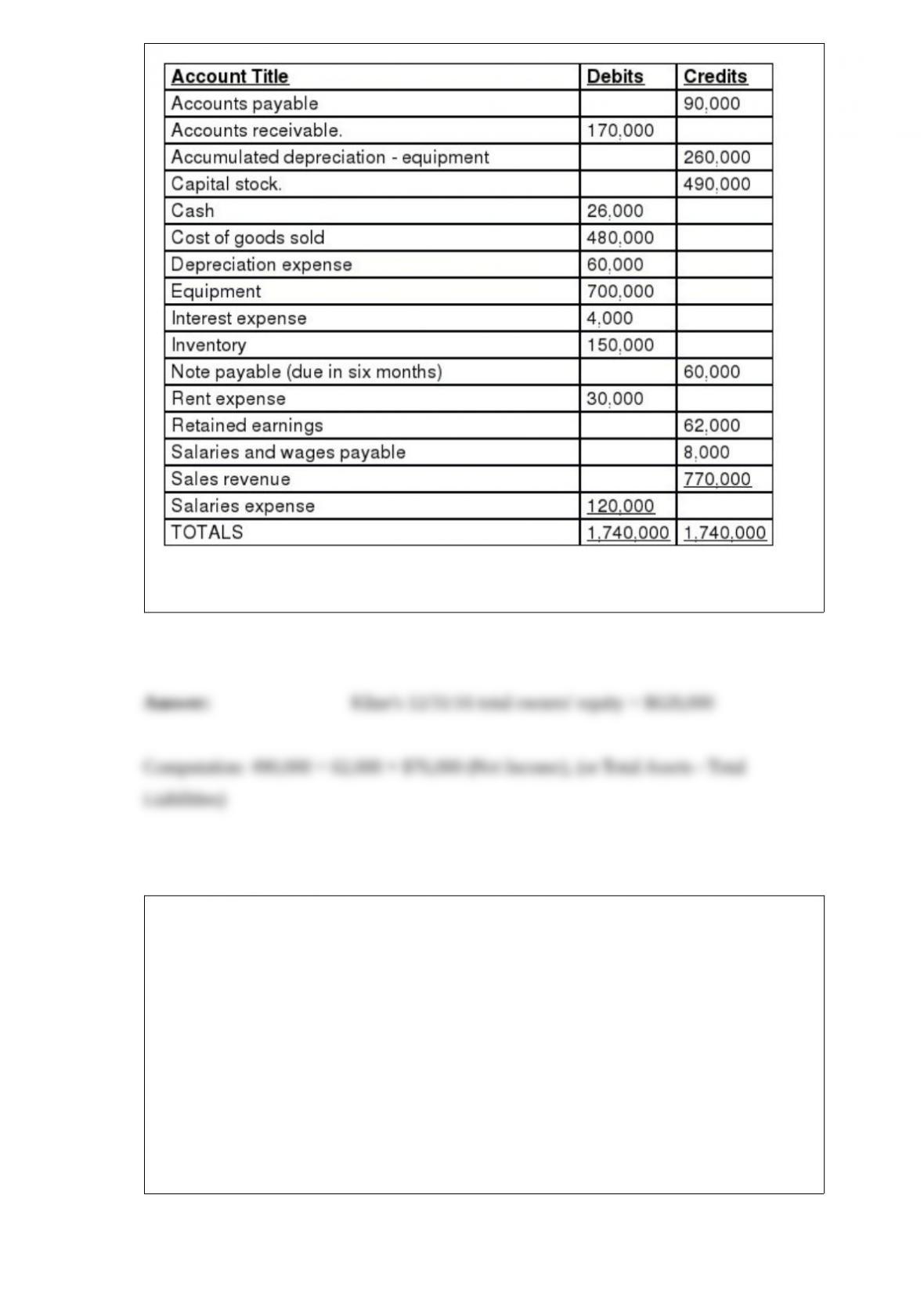

The December 31, 2016 (pre-closing) adjusted trial balance for Kline Enterprises was

as follows:

Required: Assuming no income taxes, compute the following, and place your answer

in the space provided: Kline’s 12/31/16 total shareholders’ equity:

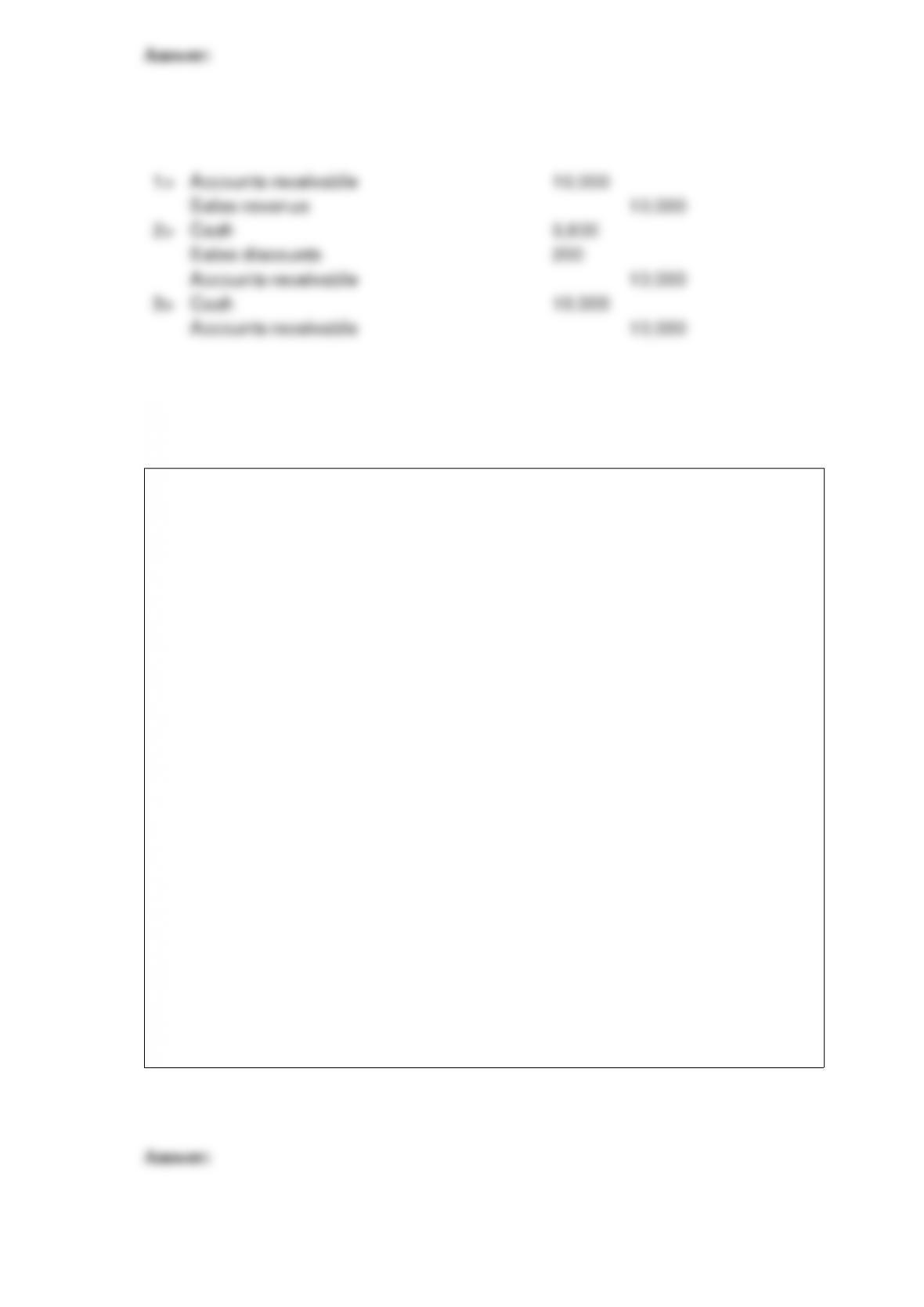

On March 12, 2016, Admiral Electronics sold 20 fax machines to Cool Stuff Co. for

$10,000, subject to terms 2/10, n/30. Admiral uses the gross method of accounting for

sales discounts.

Required:

1> Prepare the journal entry to record the sale.

2> Prepare the journal entry to record receipt of the payment, assuming the correct

amount was received on March 20, 2016.

3> Prepare the journal entry to record receipt of the payment, assuming the correct

amount was received on April 5, 2016.

The following income statement items appeared on the adjusted trial balance of

Foxworthy Corporation for the year ended December 31, 2016 ($ in 000s): sales

revenue, $22,300; cost of goods sold, $14,500; selling expenses, $2,300; general and

administrative expenses, $1,200; dividend revenue from investments, $200; interest

expense, $300. Income taxes have not yet been accrued. The company’s income tax rate

is 40% on all items of income or loss. These revenue and expense items appear in the

company’s income statement every year. The company’s controller, however, has asked

for your help in determining the appropriate treatment of the following nonrecurring

transactions that also occurred during 2016 ($ in 000s). All transactions are material in

amount. 1> Investments were sold during the year at a loss of $300. Foxworthy also had

unrealized losses of $200 for the year on investments.

2> One of the company’s factories was closed during the year. Restructuring costs

incurred were $2,000.

3> During the year, Foxworthy completed the sale of one of its operating divisions that

qualifies as a component of the entity according to GAAP regarding discontinued

operations. The division had incurred operating income of $800 in 2016 prior to the

sale, and its assets were sold at a loss of $1,800.

4> Foreign currency translation gains for the year totaled $600. Required:

Prepare Foxworthy’s single, continuous statement of comprehensive income for 2016,

including earnings per share disclosures. Use a multiple-step income statement format.

Two million shares of common stock were outstanding throughout the year.

Briefly explain when and why intraperiod tax allocation is necessary.

Veras Bus Transportation provides on-campus bus services for universities. On January

1, it enters into a one-year contract with Moose University to operate five bus lines

traveling throughout the campus. Under the contract, Veras will be paid $100,000 on the

last day of each month. In addition, Veras will receive an additional $120,000 at the end

of each six-month period, provided it remains free of accidents. – On January 1, based

on historical experience, Veras estimated that there is a 75% chance that it will remain

free of accidents for the entire year.

– On March 20, three of the most senior drivers at Veras abruptly left. As a result, Veras

had to hire inexperienced drivers to fill the vacant positions. Consequently, Veras

revised its estimate to a 30% chance that it would earn the semiannual bonus.

– On June 30, Moose confirmed that there was no accident between January and June,

so Veras would be entitled to the semiannual bonus. Veras bases estimates of variable

consideration on the most likely amount it expects to receive.

Prepare Veras’ March 31 journal entry to record the revenue earned from March 1 –

March 31, as well as any appropriate adjustments to the revenue already presumed

recorded as earned from January 1 – February 28.

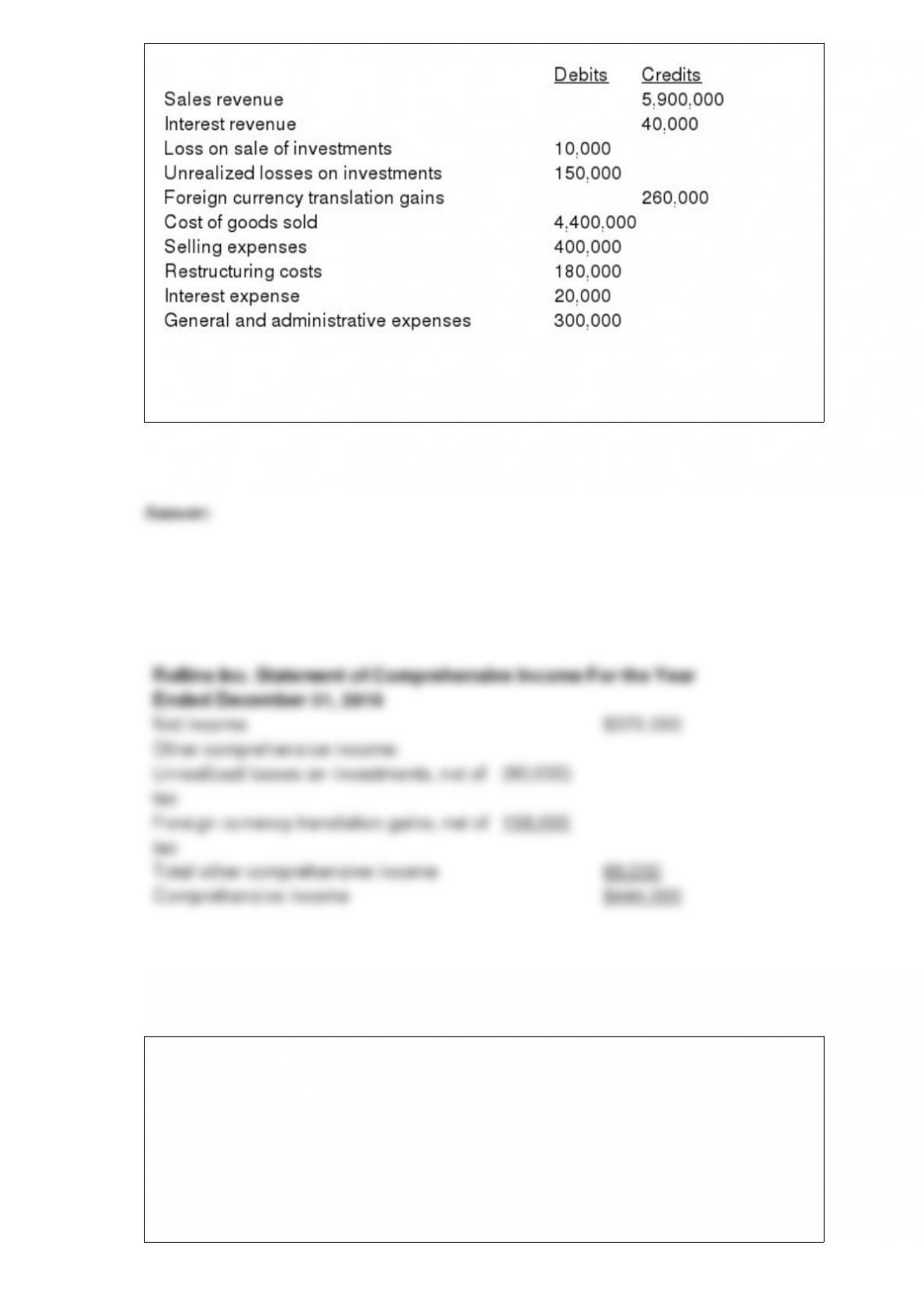

The trial balance of Rollins Inc. included the following accounts as of December 31,

2016:

Rollins had 100,000 shares of stock outstanding throughout the year. Income tax

expense has not yet been accrued. The effective tax rate is 40%.

Required: Prepare a 2016 separate statement of comprehensive income for Rollins Inc.

Olde Corporation provides an executive stock option plan. Under the plan, the company

granted options on January 1, 2016, that permit executives to acquire 2 million of the

company’s $1 par value common shares within the next five years, but not before

December 31, 2017 (the vesting date). The exercise price is the market price of the

shares on the date of the grant, $14 per share. The fair value of the options, estimated by

an appropriate option pricing model, is $2 per option. No forfeitures are anticipated.

Ignore taxes.

Required:

(1) Determine the total compensation cost pertaining to the options, assuming the fair

value approach has been selected.

(2) Prepare the appropriate journal entry to record the award of the options on January

1, 2016.

(3) Prepare the journal entry to record compensation expense on December 31, 2016.

(4) Prepare the journal entry to record compensation expense on December 31, 2017.

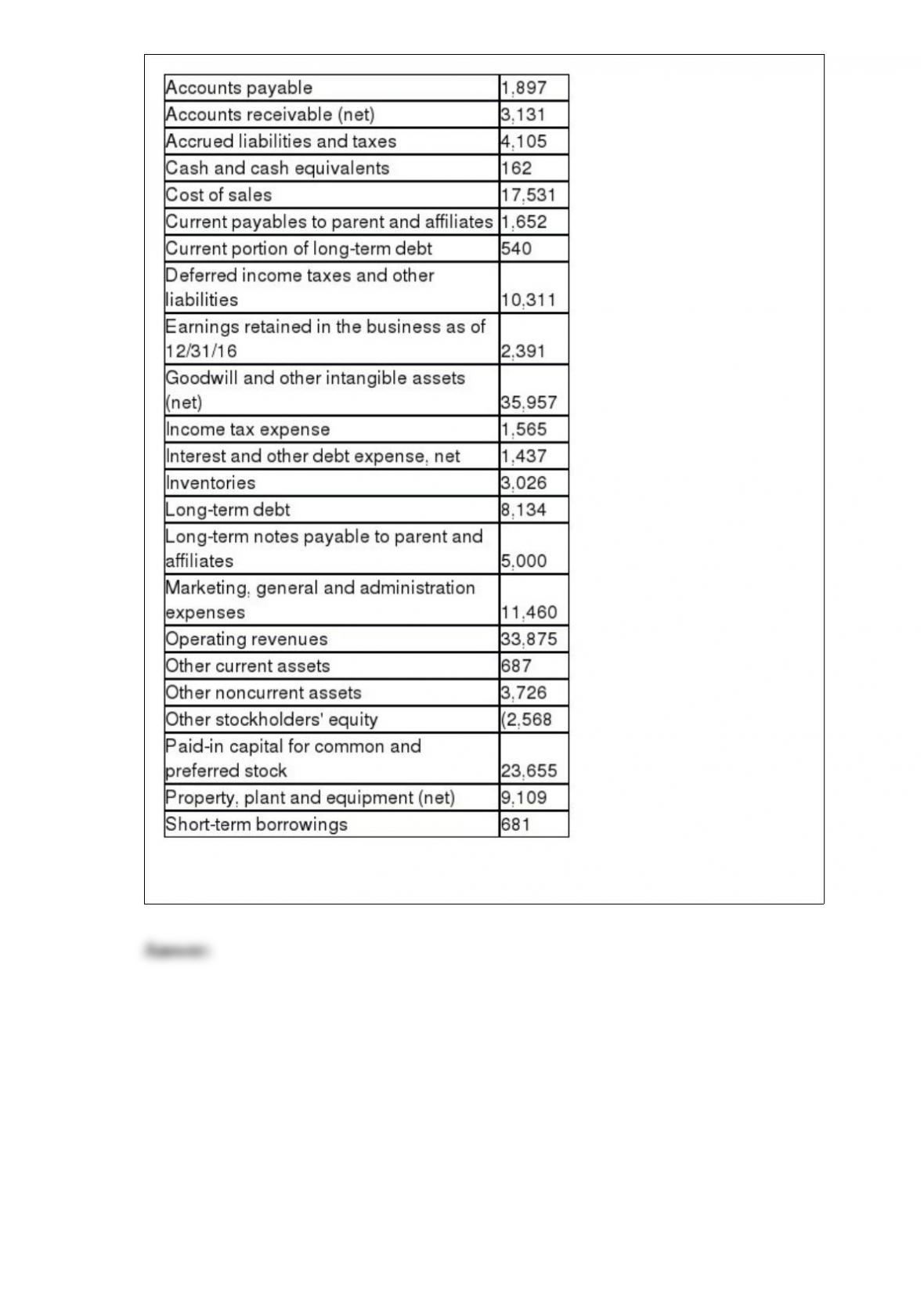

The following information, based on the 12/31/16 Annual Report to Shareholders of

Krafty Foods ($ in millions):

Based on the information presented above, prepare the 12/31/16 Balance Sheet for

Krafty Foods.

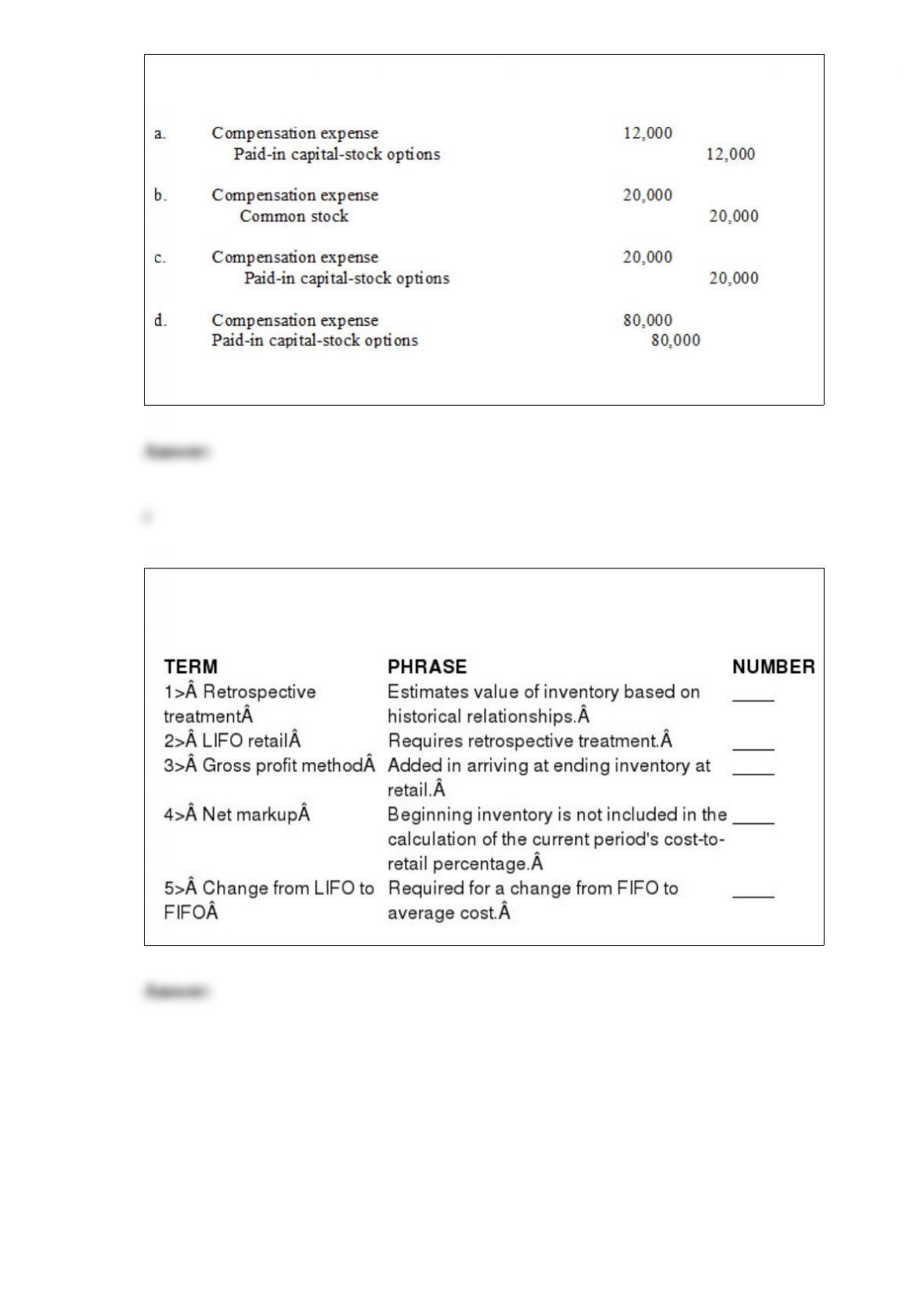

Which is the correct entry to record compensation expense for the year 2016?

Wall Drugs offered an incentive stock option plan to its employees. On January 1, 2016,

options were granted for 60,000 $1 par common shares. The exercise price equals the

$5 market price of the common stock on the grant date. The options cannot be exercised

before January 1, 2019, and expire December 31, 2020. Each option has a fair value of

$1 based on an option pricing model.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the correct term.