1) As the acceptable level of detection risk increases, an auditor may change the:

A) timing of substantive tests by performing them at an interim date rather than year

end

B) timing of the tests on controls by performing them throughout the year rather than at

one time

C) assess the level of inherent risk to a lower amount

D) increase the sample size to achieve a more effective test

2) Misstatements involving the completeness objective for sales lead to overstatements

of assets and income.

A) True

B) False

3) What distinguishes internal control evaluation and testing for financial and

operational auditing?

A) purpose of the work

B) scope of the work

C) both A and B

D) neither A nor B

4) A sample of all items in a population will have a zero sampling risk.

A) True

B) False

5) The two most important balance related objectives in notes payable are:

A) completeness and accuracy

B) existence and completeness

C) accuracy and classification

D) existence and occurrence

6) An audit generally provides no assurance that indirect-effect illegal acts will be

detected.

A) True

B) False

7) Which of the following would normally be discovered as part of the audit of the bank

reconciliation?

A) Failure to bill a customer

B) Failure to include a deposit in transit on the bank reconciliation

C) Duplicate payment of a vendor’s invoice

D) Payment to an employee for more hours than she worked

8) Systrust services are performed under the direction of the SSAEs.

A) True

B) False

9) The client’s trial balance has a balance of $410,000 for merchandise inventory. As the

auditor you are willing to accept a balance that is within $20,000 of either side of the

recorded balance. You compute a 95% confidence interval of $395,000 to $425,000.

You could therefore:

A) reject the trial balance amount

B) accept the trial balance amount

C) increase the sample size to assure more precision

D) use alternative audit procedures to satisfy yourself as to the correct balance

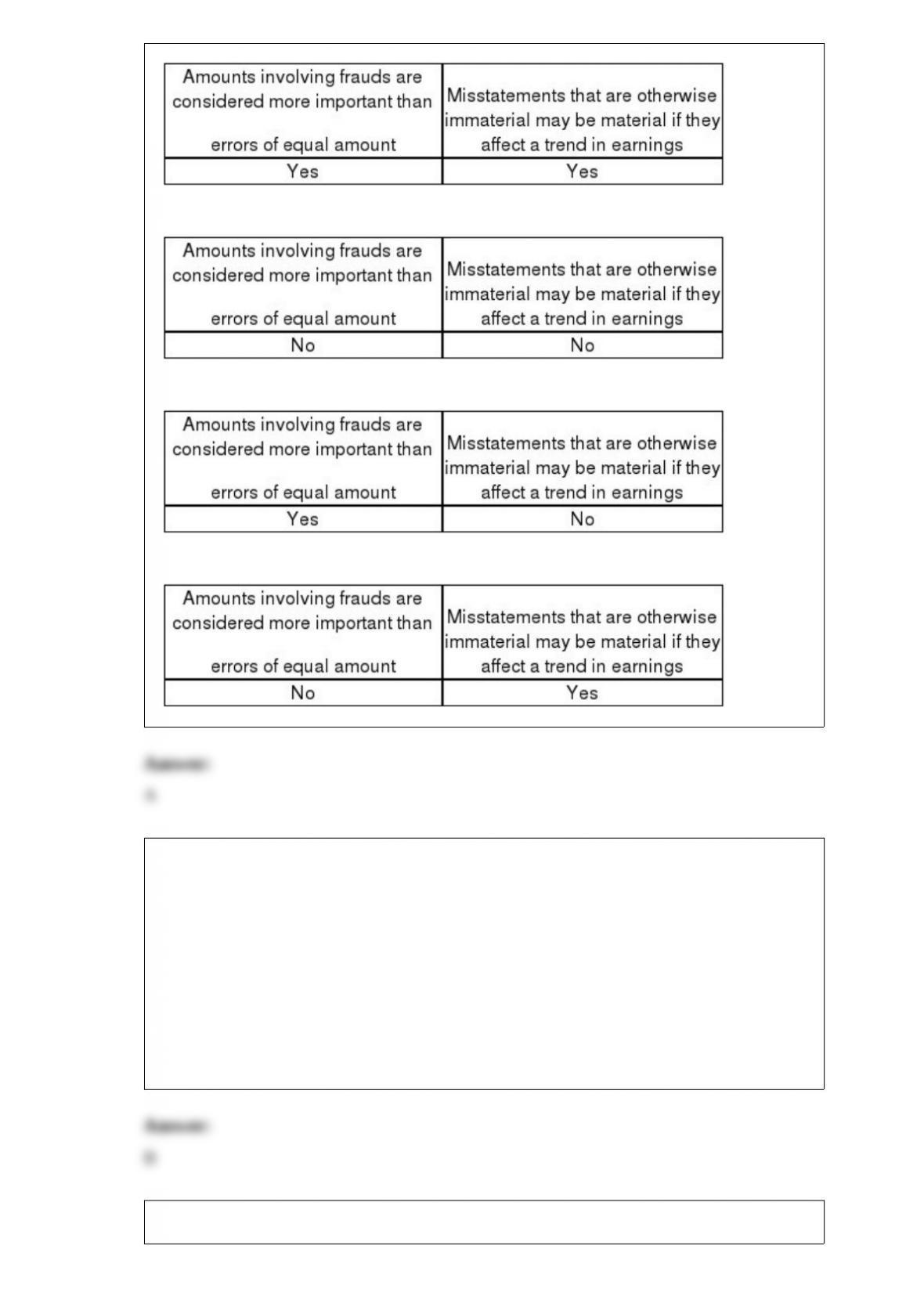

10) Certain types of misstatements are likely to be more important than other types to

users, even if the dollar amounts are the same. Which of the following demonstrates

this?

A)

B)

C)

D)

11) In which of the following circumstances would a CPA be ethically bound to refrain

from disclosing any confidential client information?

A) The CPA is issued a summons enforceable by a court order which orders the CPA to

present confidential information

B) A major stockholder of a client company seeks accounting information from the CPA

after management declined to disclose the requested information

C) Confidential client information is made available as part of a quality review of the

CPA’s practice by a peer review team authorized by the

D) An inquiry by a disciplinary body of a state CPA society requests confidential client

information

12) The auditing procedures generally used for the physical observation of inventory

and the pricing and compilation of inventory are:

A) analytical procedures and tests of transactions

B) analytical procedures and tests of details of balances

C) analytical procedures and control tests

D) tests of transactions and tests of details of balances

13) The most important part of the observation of inventory is to determine whether:

A) all counts are accurate

B) the inventory-takers are qualified

C) obsolete inventory has been identified

D) the physical count is being taken in accordance with the client’s instructions

14) Which of the following statements is true?

I.The auditor is required to issue a disclaimer of opinion in the event of a material

uncertainty.

II.The auditor is required to issue a disclaimer of opinion in the event of a going

concern problem.

A) I only

B) II only

C) I and II

D) Neither I nor II

15) Elise-Greer, LLP is an affiliate of the audit client and is audited by another firm of

auditors. Which of the following is most likely to be used by the auditor to obtain

assurance that all guarantees of the affiliate’s indebtedness have been detected?

A) Send the standard bank confirmation request to all of the client’s lender banks

B) Review client minutes and obtain a representation letter

C) Examine supporting documents for all entries in intercompany accounts

D) Obtain written confirmation of indebtedness from the auditor of the affiliate

16) Auditors of public company financial statements must issue separate reports on

internal control over financial reporting.

A) True

B) False

17) Processing controls is a category of application controls.

A) True

B) False

18) Accounts with zero or negative year-end balances have no chance of being included

in a standard probability proportional to size (PPS) sample.

A) True

B) False

19) The risk of material misstatement refers to:

A) control risk and acceptable audit risk

B) inherent risk

C) the combination of inherent risk and control risk

D) inherent risk and audit risk

20) When analytical procedures reveal unusual fluctuations in an account balance, the

auditor will probably perform fewer tests of details for that account and increase the

tests of controls related to the account.

A) True

B) False

21) Many clients have outsourced the IT functions. The difficulty the independent

auditor faces when a computer service center is used is to:

A) gain the permission of the service center to review their work

B) find compatible programs that will analyze the service center’s programs

C) determine the adequacy of the service center’s internal controls

D) try to abide by the Code of Professional Conduct to maintain the security and

confidentiality of client’s data

22) The Sarbanes-Oxley Act of 2002 requires that public companies issue an internal

control report.

A) True

B) False

23) The three most important audit objectives for cash are accuracy, existence, and

classification.

A) True

B) False

24) Which of the following is not a type of statistical method that provides results in

dollar terms?

A) Variables sampling

B) Attributes sampling

C) Monetary-unit sampling

D) Sampling with probability proportional to size

25) Which of the following is likely to be detected as part of the audit of the bank

reconciliation?

A) Failure to bill a customer

B) Duplicate payment of a vendor invoice

C) Cash received by the client after year end, but included in cash receipts in the current

year

D) An embezzlement of cash by intercepting cash receipts from customers before they

are recorded

26) Internal control over payroll is normally highly structured and well controlled.

A) True

B) False

27) During your audit of Williams Company you are trying to determine whether all

accounts payable were recorded in the proper period. Which assertion are you gathering

evidence for?

A) Occurrence

B) Completeness

C) Cutoff

D) Rights and Obligations

28) Current professional standards prohibit accountants from performing engagements

to review forecasts or projections.

A) True

B) False

29) The Securities and Exchange Commission requires quarterly financial information

as a part of the:

A) 10-K report

B) 10-Q report

C) 8-K report

D) auditor’s report

30) Customer billing is a critical process which auditors must understand. What are the

most important aspects of billing and what are the related objectives?

31) Discuss the four aspects of the audit of cost accounting with which the auditor is

most concerned.

32) What events initiate and terminate the payroll and personnel cycle?

33) Discuss the key internal controls for prepaid insurance that affect the auditor’s

extent of testing of the prepaid insurance account.

34) Discuss the actions an auditor should take when the auditor discovers an illegal act.

35) Why is the appropriateness of audit evidence obtained by the auditor important in

forming an audit opinion? Describe the qualities information should have to be

considered appropriate by the auditor.