1) the public company accounting oversight board oversees the work of auditors of

public companies.

2) held-to-maturity investments are categorized as long-term assets on the balance

sheet, irrespective of the maturity date.

3) the asset turnover ratio is calculated by dividing cost of goods sold by average total

assets.

4) the beginning balance in the common stock account of alpha technologies inc. was

$80,000. the revenues and expenses amounted to $60,000 and $40,000, respectively.

during the year, the company did not declare any dividends or issue common stock. the

common stock account will have $100,000 at the end of the year.

5) the financing activities section of the statement of cash flows includes paying

dividends and paying off loans.

6) the interest period extends from the original date of the note to the maturity date.

7) which of the following statements helps analyze the business performance in terms

of profitability?

8) net sales revenue is equal to sales revenue less cost of goods sold.

9) an amortization schedule details each loan payment’s allocation between principal

and interest and also the beginning and ending balances of the loan.

10) which of the following types of stock is considered least risky for investors?

a) common stock

b) par value stock

c) no-par stock

d) preferred stock

11) a check for which a maker’s bank account has inadequate money to pay the check is

known as ________.

a) nonsufficient funds checks

b) outstanding checks

c) restrictive checks

d) canceled checks

12) marsh supply services received $1,000 cash from a customer which was owed to the

business from the previous month. what is the effect of the cash receipt on the

accounting equation?

a) accounts receivable decreases and stockholders’ equity decreases

b) cash account increases and accounts receivable decreases

c) accounts payable increases and stockholders’ equity decreases

d) cash account increases and accounts payable decreases

13) in a multi-step income statement, which of the following items is excluded from the

calculation of operating income?

a) sales revenue

b) interest expense

c) selling expense

d) administrative expense

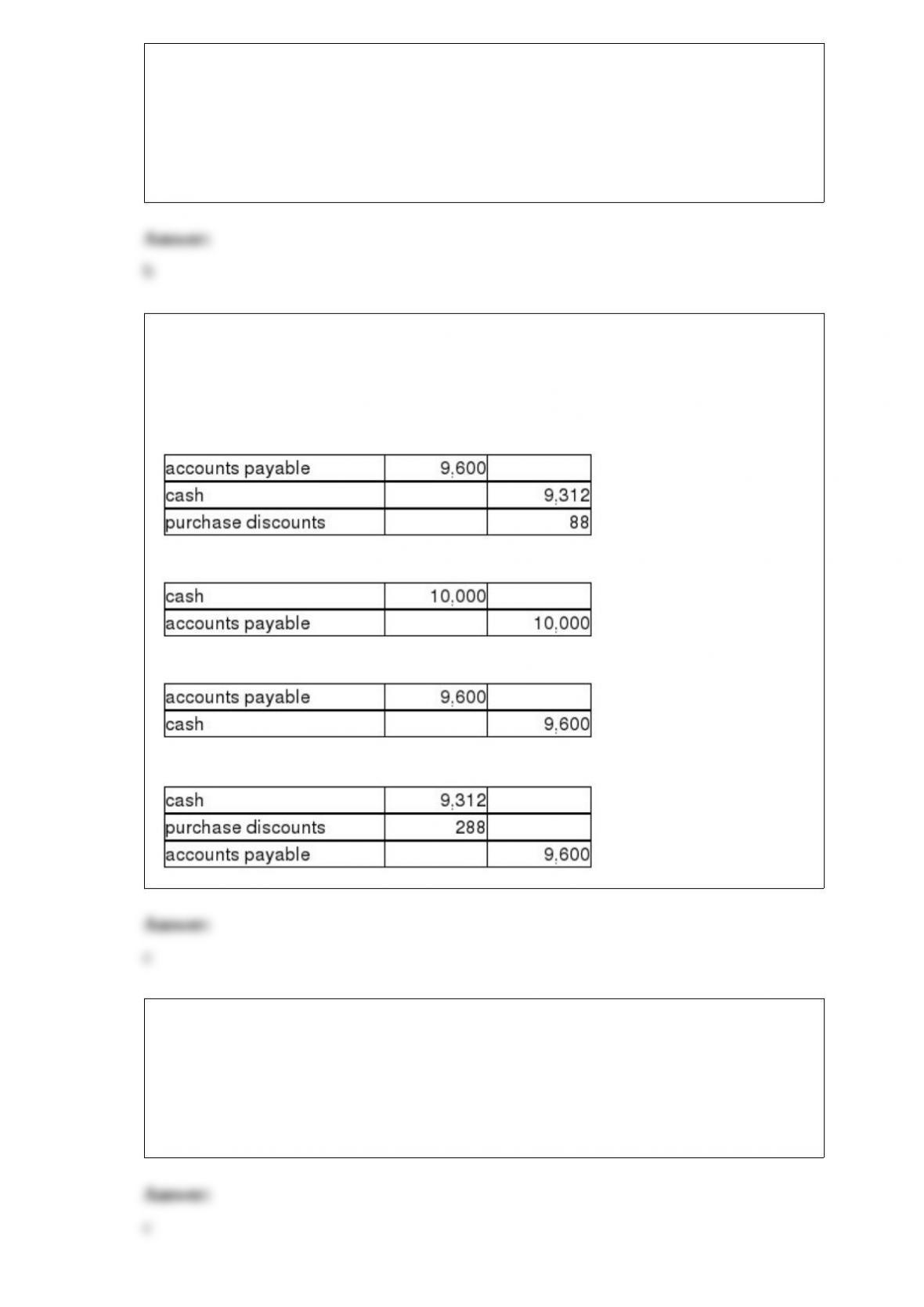

14) avery inc. uses the periodic inventory system. on february 1, the corporation

purchased inventory on account for $10,000. the terms were 3/10, n/30. on february 2, it

returned damaged goods worth $400 to the supplier and was granted an allowance. give

the journal entry for the payment if the invoice is paid after the discount period.

a)

b)

c)

d)

15) which of the following adjusted balances would appear in the balance sheet credit

column of a worksheet?

a) rent revenue

b) insurance expense

c) salaries payable

d) equipment

16) an income statement includes ________.

a) land and salaries payable

b) common stock, retained earnings, and dividends

c) furniture and cash

d) service revenue and utilities expense

17) on january 1, 2015, carter sales issued $15,000 in bonds for $15,800. they were

8-year bonds with a stated rate of 9%, and pay semiannual interest. carter sales uses the

straight-line method to amortize the bond premium. after the first interest payment on

june 30, 2015, what was the bond carrying amount?

a) $15,800

b) $15,750

c) $15,050

d) $15,000

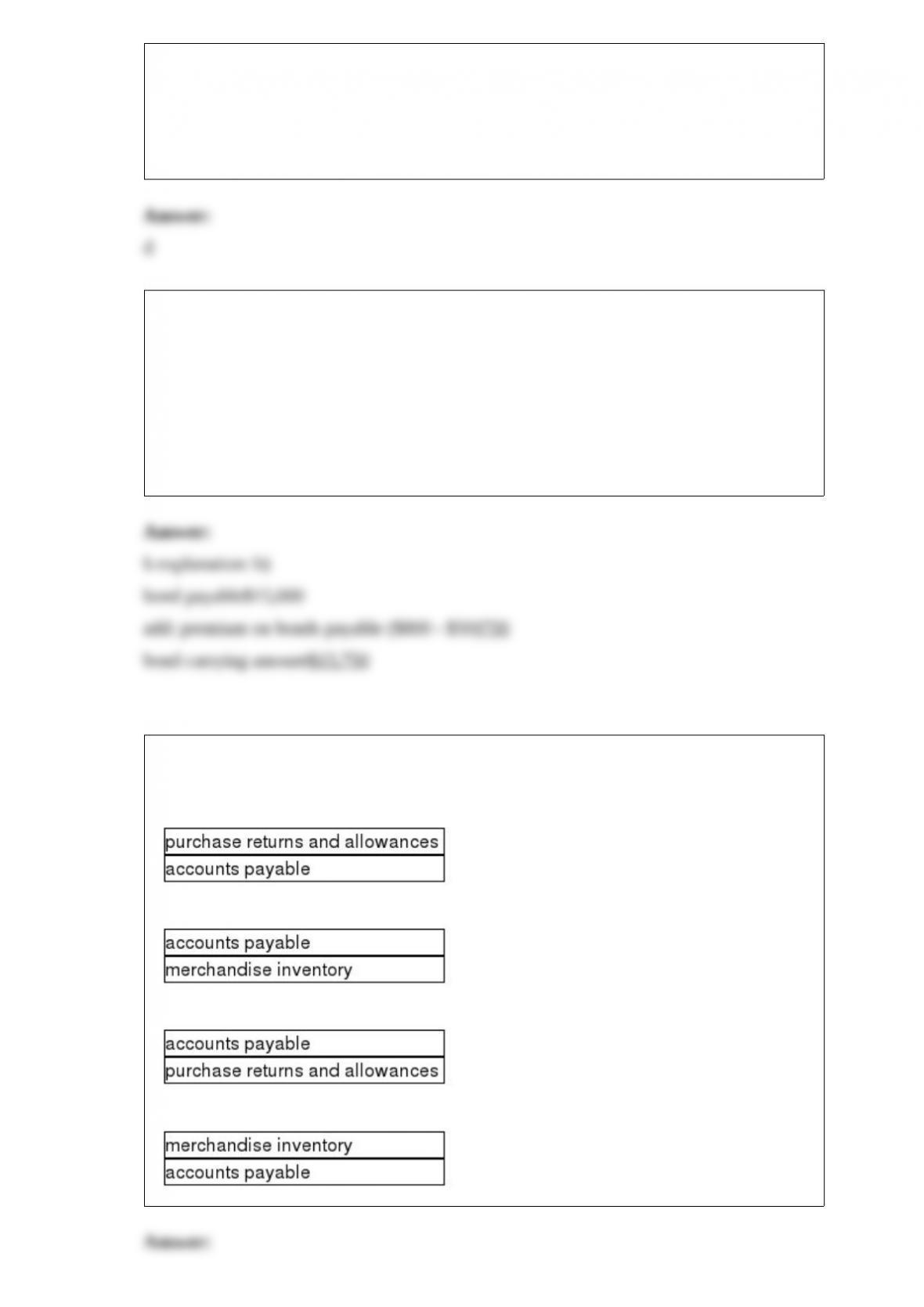

18) which of the following is the correct journal entry for purchase returns of goods

purchased on account under the periodic inventory system?

a)

b)

c)

d)

19) a company sold merchandise for $20,000 on account with terms of 3/10, n/30. the

company uses a perpetual inventory system. after two days, it received defective

merchandise worth $2,000. the journal entry to record the cash receipt for sale if the

payment is received within 10 days of the invoice date would include ________.

a) a debit to cash for $17,460, a credit to merchandise inventory for $540, and a credit

to sales revenue for $18,000

b) a debit to cash for $17,460, a debit to sales discount for $540, and a credit to

accounts receivable for $18,000

c) a debit to cash for $18,000, a debit to merchandise inventory for $2,000 and a credit

to accounts receivable

d) a debit to sales for $20,000, a credit to accounts receivable for $20,000, and a credit

to sales discount for $2,000

20) on january 1, 2015, carter sales issued $15,000 in bonds for $14,700. they were

6-year bonds with a stated rate of 9%, and pay semiannual interest. carter sales uses the

straight-line method to amortize the bond discount. on june 30, 2015, when carter

makes the first payment to bondholders, how much will they report as interest expense?

a) $675

b) $700

c) $25

d) $825

21) which of the following is the key significance of the acid-test ratio?

a) it measures a company’s ability to pay its current liabilities if they are due

immediately

b) it measures the ability of the company to earn profits out of the sales made by it

c) it reflects how much long-term debt a company has

d) it indicates how much cash could be realized by selling the inventory

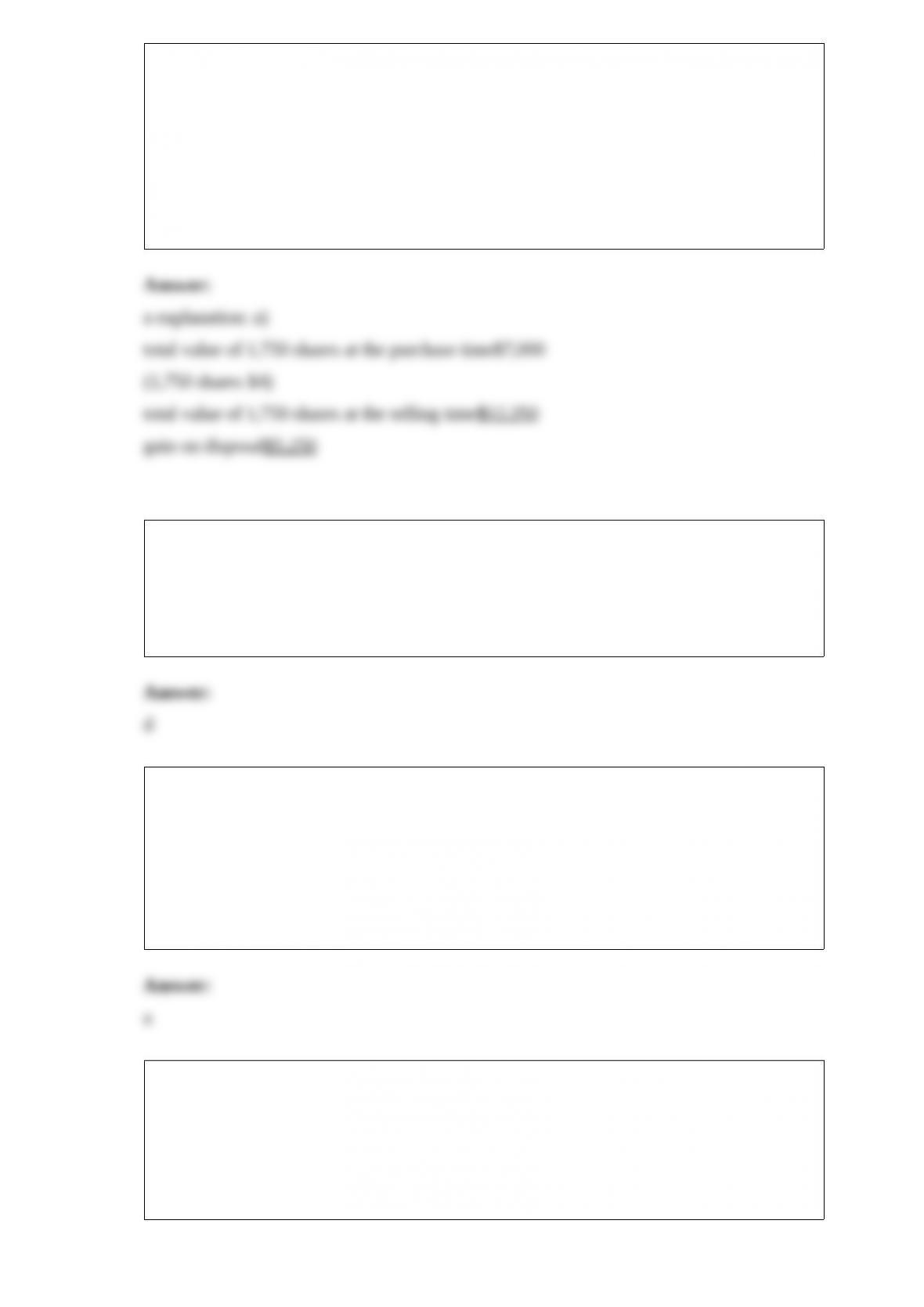

22) gray financial services inc. invested $15,000 to acquire 3,750 shares of mitt

investments inc. on march 15, 2012. this investment represents less than 20% of the

investee’s voting stock. on may 7, 2016, greg financial services inc. sells 1,750 shares

for $12,250. when the transaction is recorded in a journal entry, ________.

a) gain on disposal will be credited

b) long-term investmentsavailable-for-sale will be debited

c) cash will be credited

d) long-term investmentsheld-to-maturity will be debited

23) which of the following is true of goodwill?

a) goodwill must be capitalized when acquired, and amortized over 7 years or less

b) both created and acquired goodwill must be recorded in the books

c) goodwill must be expensed when acquired

d) goodwill is not amortized

24) the accountant for jones auto repair inc. failed to make an adjusting entry to record

$5,000 of unpaid salaries for the last 2 weeks of the year. which of the following is an

impact of this omission?

a) the net income will be overstated

b) the total assets will be understated

c) the net income will be understated

d) the total assets will be overstated

25) what is the term used for the difference between the equipment account and the

accumulated depreciation account?

a) contra asset

b) market value

c) historical cost

d) book value

26) a parent company is a company that ________.

a) is controlled by another corporation

b) owns a controlling interest in another company

c) is the first to begin operations in an industry

d) has a trading investment in another company

27) which of the following account’s balance is carried forward to the next accounting

period?

a) accumulated depreciation

b) depreciation expense

c) dividends

d) sales revenue

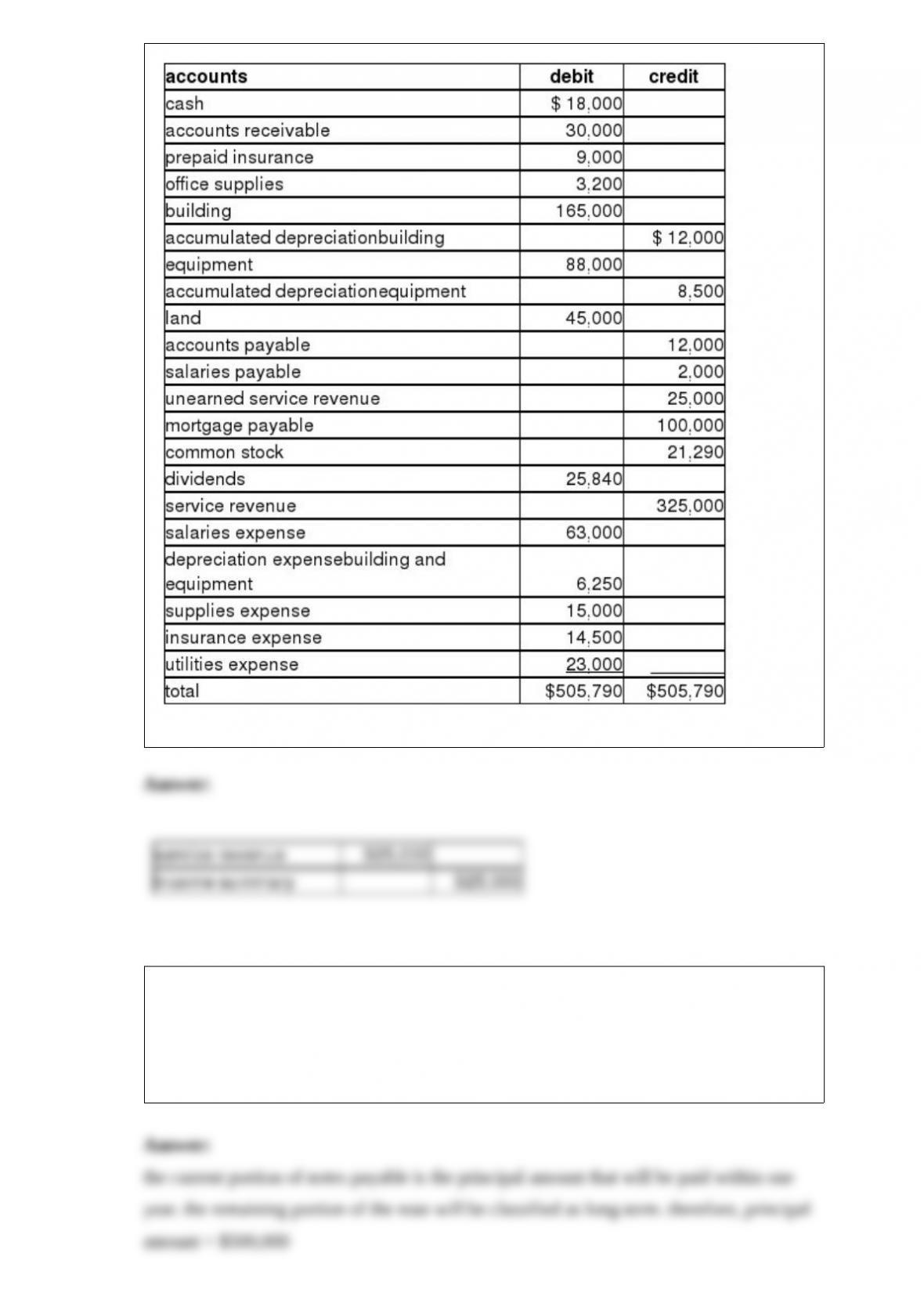

28) the following is the adjusted trial balance as of december 31, 2015 of martin watch

inc.:

provide the closing entry for service revenue.

29) on december 31, 2014, ferrero inc. borrowed $500,000 by signing a note payable.

the note is for 5 years and bears interest at the rate of 8%. the note is payable in 5 yearly

installments of $100,000 plus interest due at the end of every year beginning on

december 31, 2015. which portion is classified as the long-term portion of notes

payable at december 31, 2014?

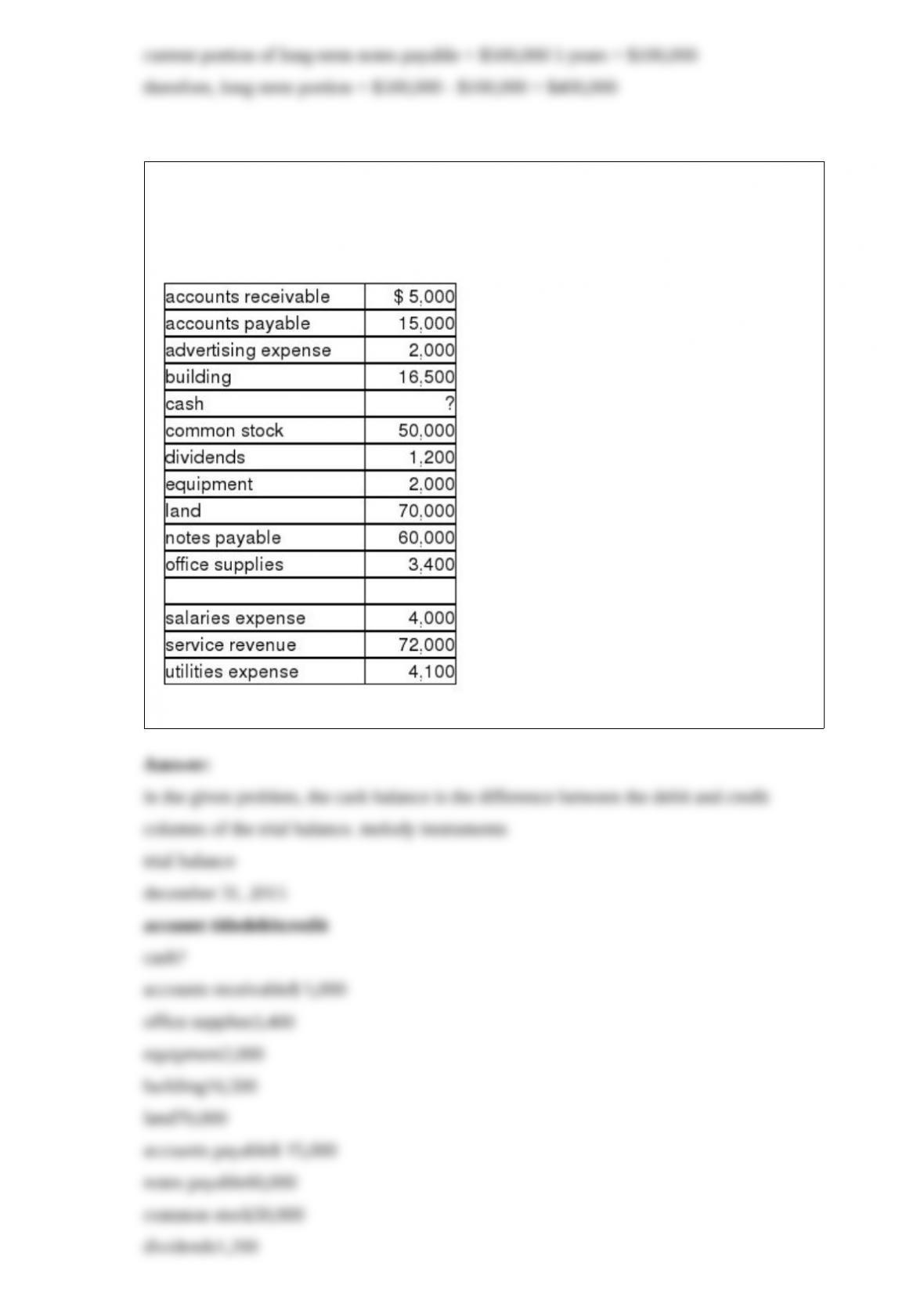

30) melody instruments inc. sells musical instruments. on december 31, 2015, after its

first month of business, melody instruments inc. had the following balances in its

accounts, listed alphabetically.

determine the balance in the cash account and prepare the trial balance.

31) clark sales sold 450 units of product to a customer on account. the company uses

the perpetual inventory system. the selling price was $28 per unit, and the cost,

according to the company’s inventory records, was $12 per unit. provide the journal

entry to record the sales revenue.

32) prepare the vertical analysis report of the balance sheet data given below. (round off

the percentages to two decimal places.)

balance sheet

december 31, 2015

2015

assets

current assets:

cash and cash equivalents$10,000

accounts receivable, net15,600

merchandise inventory38,000

total current assets$63,600

long-term investments$15,000

property, plant, and equipment, net195,000

total assets$273,600

liabilities

current liabilities:

accounts payable$8,500

notes payable1,400

total current liabilities$9,900

long-term liabilities$54,000

total liabilities$63,900

stockholders’ equity

common stock$161,000

retained earnings48,700

total stockholders’ equity209,700

total liabilities and stockholders’ equity$273,600

33) on july 1, alpha inc. paid rent of $15,000 for a small equipment storage area for the

period of july 1 till december 31. provide the adjusting journal entry on july 31. (ignore

explanation) assume the prepaid expense is initially recorded as an asset.