Transactions are initially recorded in the

a. general ledger.

b. trial balance.

c. general journal.

d. balance sheet.

Answer:

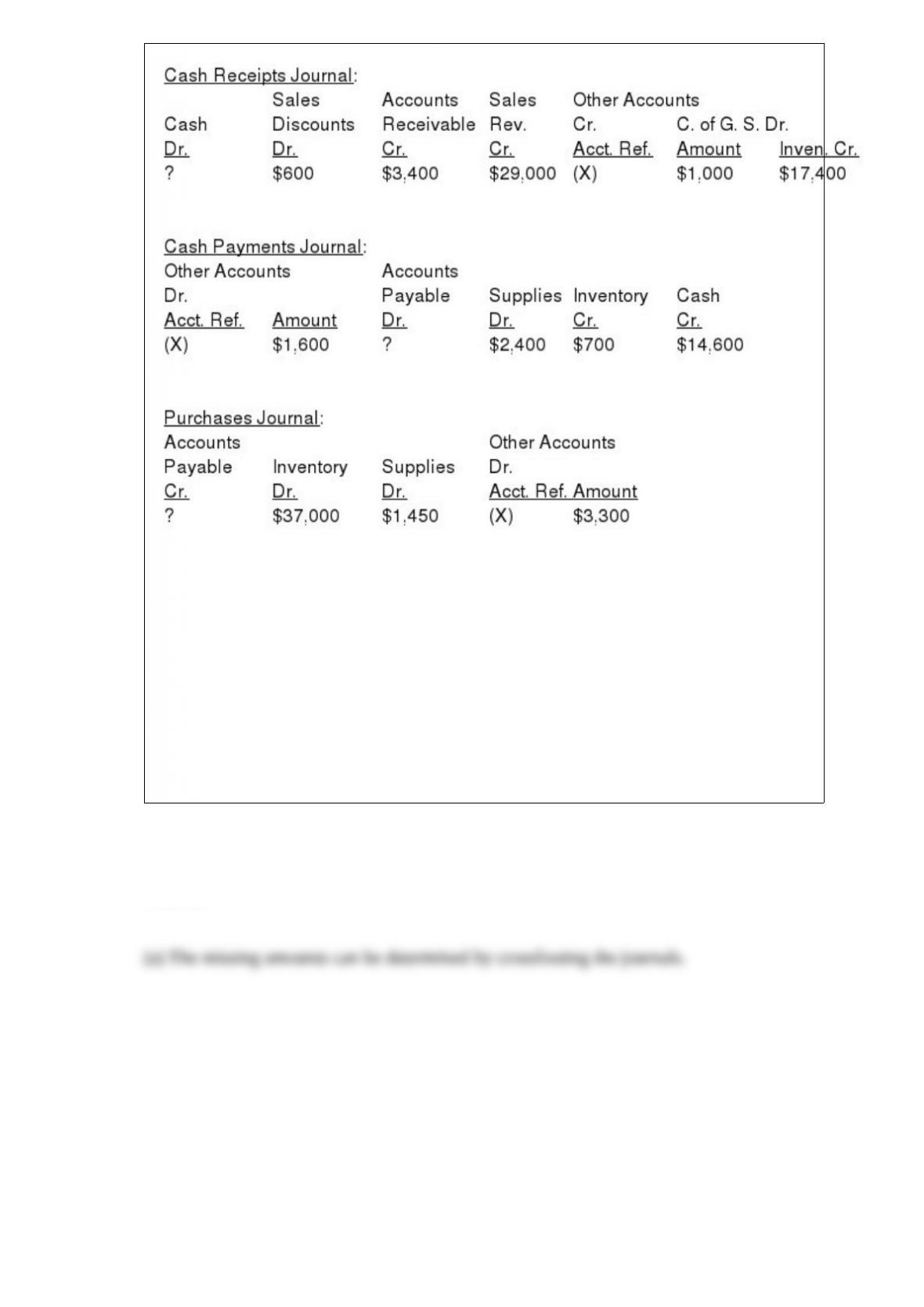

Horton Company uses four special journals, (cash receipts, cash payments, sales, and

purchases journal) in addition to a general journal. On November 1, 2015, the control

accounts in the general ledger had the following balances: Cash $12,000, Accounts

Receivable $200,000 and Accounts Payable $42,000. Selected information on the final

line of the special journals for the month of November is presented below:

Additional Data:

The Sales Journal total was $41,000. A customer returned merchandise for credit for

$360 and Norton Company returned store supplies to a supplier for credit for $400.

Instructions

(a) Determine the missing amounts in the special journals.

(b) Determine the balances in the general ledger accounts (Cash, Accounts Receivable,

and Accounts Payable) at the end of November.

Answer:

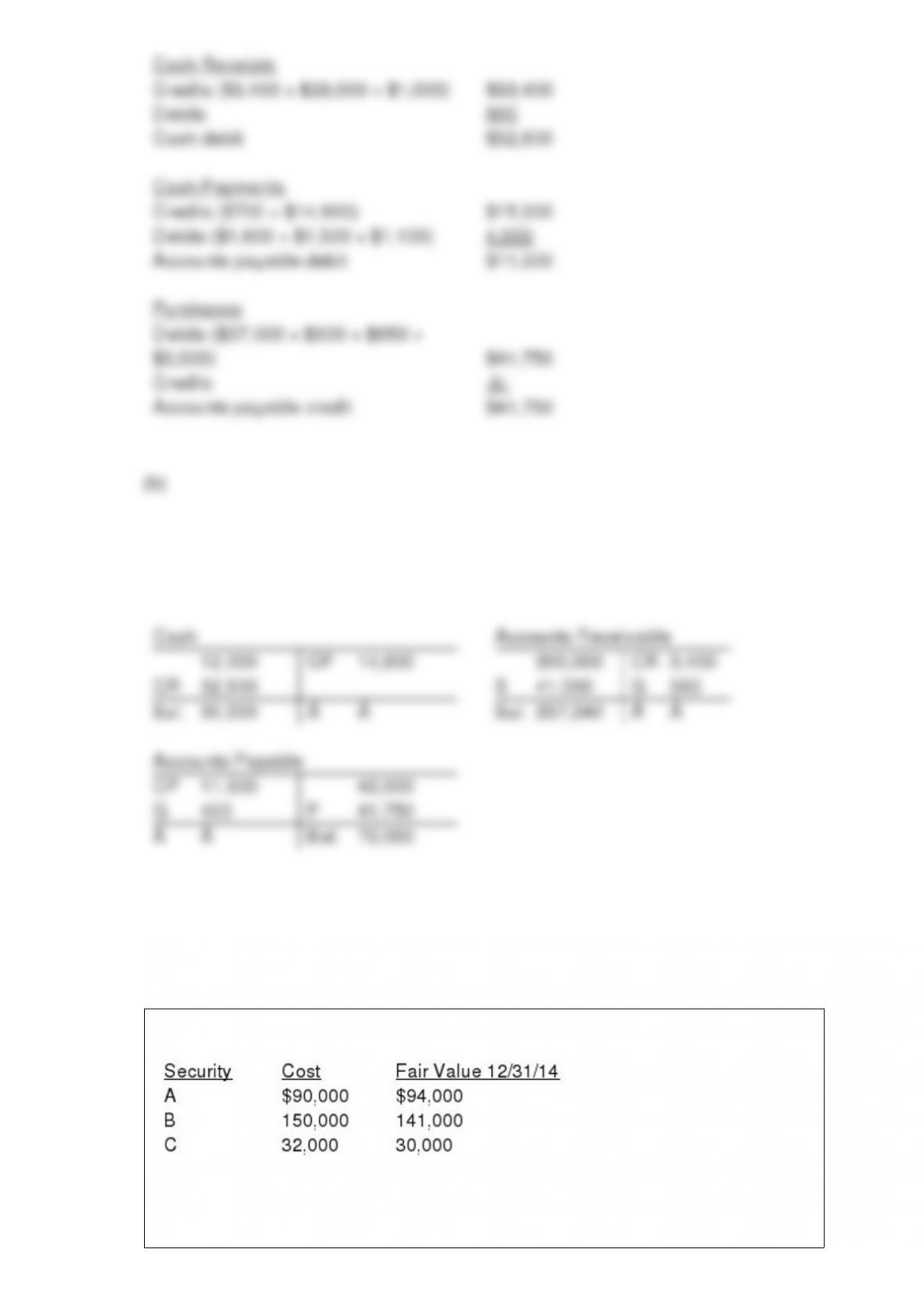

At December 31, 2014, the trading securities for Saddle, Inc. are as follows:

Saddle should report the following amount related to the securities in its 2014 income

statement:

a. $4,000 gain

b. $7,000 realized loss.

c. $7,000 unrealized loss.

d. $11,000 unrealized loss.

Answer:

The balance in the supplies account on June 1 was $5,200, supplies purchased during

June were $3,500, and the supplies on hand at June 30 were $3,000. The amount to be

used for the appropriate adjusting entry is

a. $3,500.

b. $5,700.

c. $6,500.

d. $11,700.

Answer:

A company purchased factory equipment on June 1, 2015, for $160,000. It is estimated

that the equipment will have a $10,000 salvage value at the end of its 10-year useful

life. Using the straight-line method of depreciation, the amount to be recorded as

depreciation expense at December 31, 2015, is

a. $15,000.

b. $8,750.

c. $7,500.

d. $6,250.

Answer:

Adjusting entries are prepared from

a. source documents.

b. the adjustments columns of the worksheet.

c. the general ledger.

d. last year’s worksheet.

Answer:

Depreciation is the process of

a. valuing an asset at its fair value.

b. increasing the value of an asset over its useful life in a rational and systematic

manner.

c. allocating the cost of an asset to expense over its useful life in a rational and

systematic manner.

d. writing down an asset to its real value each accounting period.

Answer:

The cost of an asset and its fair value are

a. never the same.

b. the same when the asset is sold.

c. irrelevant when the asset is used by the business in its operations.

d. the same on the date of acquisition.

Answer:

Dean Corporation reported net income $58,000, net sales $500,000, and average assets

$800,000 for 2015. The 2015 profit margin was:

a. 5.8%.

b. 11.6%.

c. 62.5%.

d. 160%.

Answer:

Match the principle of internal control to each of the following cases.

a) Establishment of responsibility

b) Segregation of duties

c) Accountability for assets

d) Documentation procedures

e) Physical controls

1> Cash is locked in a safe overnight.

2> Employees who receive shipments of goods do not have access to the accounting

records for merchandise.

3> Shipping documents are prenumbered.

4> The bookkeeper does not have physical custody of assets.

5> Only the treasurer of the company can sign checks.

Answer:

Intangible assets are

a. listed under current assets on the balance sheet.

b. not listed on the balance sheet because they do not have physical substance.

c. long-lived assets that are often very valuable.

d. listed as a long-term investment on the balance sheet.

Answer:

A corporation issued $600,000, 10%, 7-year bonds on January 1, 2015 for $648,666,

which reflects an effective-interest rate of 7%. Interest is paid semiannually on January

1 and July 1. If the corporation uses the effective-interest method of amortization of

bond premium, the amount of bond interest expense to be recognized on July 1, 2015, is

a. $30,000.

b. $21,000.

c. $32,434.

d. $22,703.

Answer:

On January 1, 2015, the stockholders’ equity section of Kingman Corporation shows:

common stock ($5 par value) $2,000,000; paid-in capital in excess of par value

$1,200,000; and retained earnings $1,500,000. During the year, the following treasury

stock transactions occurred.

Mar. 1 Purchased 60,000 shares for cash at $13 per share.

July 1 Sold 15,000 treasury shares for cash at $15 per share.

Sept. 1 Sold 10,000 treasury shares for cash at $11 per share.

Instructions

(a) Journalize the treasury stock transactions.

(b) Prepare the stockholders’ equity section after the entries in (a) are recorded.

(c) Prepare the entry for September 1, assuming the treasury shares were sold at $8 per

share.

Answer:

Which one of the following items would not be considered cash?

a. Coins

b. Money orders

c. Currency

d. Postdated checks

Answer:

A company uses a sales journal, cash receipts journal, purchases journal, cash payments

journal, and a general journal. A cash sales return would be recorded in the

a. sales journal.

b. cash receipts journal.

c. cash payments journal.

d. general journal.

Answer:

The equity method of accounting for an investment in the common stock of another

company should be used by the investor when the investment

a. is composed of common stock and it is the investor’s intent to vote the common

stock.

b. ensures a source of supply of raw materials for the investor.

c. enables the investor to exercise significant influence over the investee.

d. is obtained by an exchange of stock for stock.

Answer:

On July 7, 2015, Hidden Camera Enterprises performed cash services of $1,700. The

entry to record this transaction would include

a. a debit to Service Revenue of $1,700.

b. a credit to Accounts Receivable of $1,700.

c. a debit to Cash of $1,700.

d. a credit to Accounts Payable of $1,700.

Answer:

A post-closing trial balance contains

a. real and nominal accounts.

b. permanent and temporary accounts.

c. balance sheet or permanent accounts.

d. balance sheet and revenue accounts.

Answer:

On February 1, Barton Corporation issued 5,000 shares of its $20 par value preferred

stock for $28 per share.

Instructions

Journalize the transaction.

Answer:

Based on the following information, compute the (1) current ratio and (2) working

capital.

Answer:

In analyzing and interpreting financial statement information, three major

characteristics are generally evaluated: (1)____________, (2)_____________, and

(3)_____________.

Answer:

Selected transactions for Mountain Goats Tree Service are listed below.

1> Sold common stock for cash to start business.

2> Paid for monthly advertising.

3> Purchased supplies on account.

4> Billed customers for services performed.

5> Paid cash dividends.

6> Received cash from customers billed in (4).

7> Incurred utilities expense on account.

8> Purchased additional supplies for cash.

9> Received cash from customers when service was performed.

Instructions

List the numbers of the above transactions and describe the effect of each transaction on

assets,

liabilities, and stockholders’ equity. For example, the first answer is: (1) Increase in

assets and increase in stockholders’ equity.

Answer:

The declining-balance method is an accelerated method of depreciation. Briefly explain

what is meant by an accelerated method of depreciation and justify the choosing of an

accelerated method.

Answer:

Inigo Company prepared the following adjusting entries at year end on December 31,

2015:

In an effort to minimize errors in recording transactions, Inigo Company utilizes

reversing entries. Prepare reversing entries on January 1, 2016.

Answer:

The days in inventory is computed by multiplying inventory turnover by 365.

Answer:

Sales resulting from the use of Visa and MasterCard are considered ______________

by the retailer.

Answer:

A long-term note that pledges title to specific property as security for a loan is known as

a mortgage payable.

Answer:

Match the items below by entering the appropriate code letter in the space provided.

1> An incentive to encourage customers to pay their accounts early.

2> Expenses incurred in the process of earning sales revenue.

3> Freight terms that require the seller to pay the freight cost.

4> Sales revenue less sales returns and allowances and sales discounts.

5> A document that supports each credit purchase.

6> Net sales less cost of goods sold.

7> Freight cost to deliver goods to customers reported as a selling expense.

8> Requires a physical count of goods on hand to compute cost of goods sold.

9> Gross profit less total operating expenses.

10> Freight terms that require the buyer to pay the freight cost.

Answer: