Which of the following is considered a sale of receivables?

a. Pledging receivables.

b. Assigning receivables.

c. Factoring receivables without recourse.

d. None of these answer choices are correct.

On June 1, 2016, Dirty Harry Co. borrowed cash by issuing a 6-month

noninterest-bearing note with a maturity value of $500,000 and a discount rate of 6%.

Assuming straight-line amortization of the discount, what is the carrying value of the

note as of September 30, 2016?

a. $525,000.

b. $300,000.

c. $495,000.

d. $475,000.

The common stock account in a company’s balance sheet is measured as:

a. The number of common shares outstanding multiplied by the stock’s par value per

share.

b. The number of common shares outstanding multiplied by the stock’s current market

value per share.

c. The number of common shares issued multiplied by the stock’s par value per share.

d. None of these answer choices is correct.

Retained earnings represent a company’s:

a. Undistributed net income.

b. Undistributed net assets.

c. Extra paid-in capital.

d. Undistributed cash.

Issued stock refers to the number of shares:

a. Outstanding plus treasury shares.

b. Shares issued for cash.

c. In the hands of shareholders.

d. That may be issued under state law.

An item that should be reported as a prior period adjustment is the:

a. Correction of an error in depreciation from last year.

b. Payment of taxes due to a tax audit of last year’s tax return.

c. Payment of a previously recorded warranty expense.

d. Receipt of the proceeds of a note receivable that was due last year.

Alliance Software began 2016 with accounts receivable of $115,000. All sales are made

on credit. Sales and cash collections from customers for the year were $780,000 and

$700,000, respectively. Cost of goods sold for the year was $450,000. What was

Alliance’s receivables turnover ratio (rounded) for 2016?

a. 4.00.

b. 5.03.

c. 2.90.

d. 6.78.

Crystal Corporation recorded a lease payment as follows:

Crystal must have a(n):

a. Operating lease.

b. Leveraged lease.

c. Capital lease.

d. Direct financing lease.

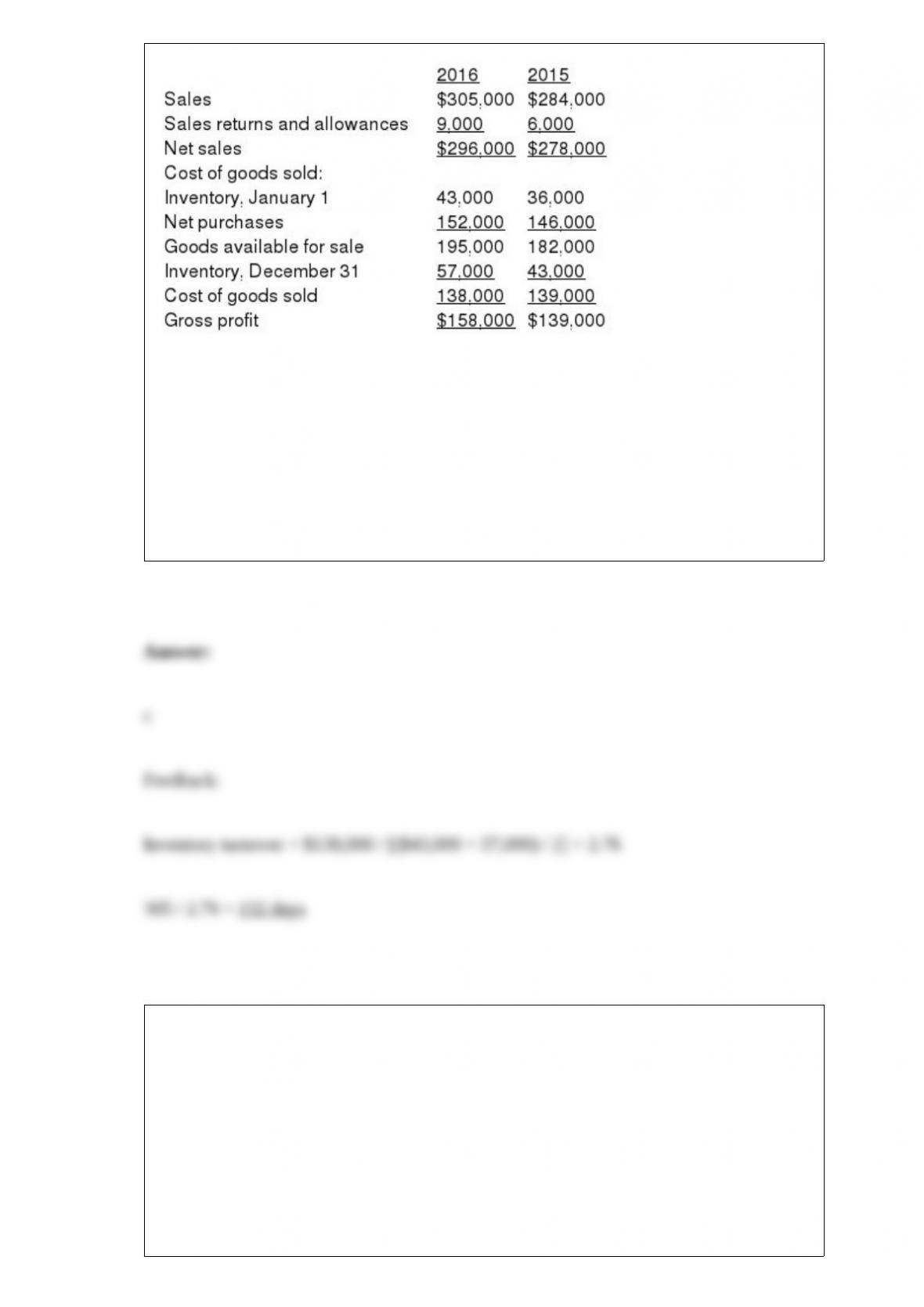

Anthony Thomas Candies (ATC) reported the following financial data for 2016 and

2015:

The average days inventory for ATC (rounded) for 2016 is:

a. Less than 100 days.

b. 114 days

c. 132 days.

d. 151 days.

When a business makes an end-of-period adjusting entry with a debit to supplies

expense, the usual credit entry is made to:

a. Accounts payable.

b. Supplies.

c. Cash.

d. Retained earnings.

Robertson Inc. prepares its financial statements according to International Financial

Reporting Standards (IFRS). At the end of its 2016 fiscal year, the company chooses to

revalue its equipment. The equipment cost $540,000, had accumulated depreciation of

$240,000 at the end of the year after recording annual depreciation, and had a fair value

of $330,000. After the revaluation, the accumulated depreciation account will have a

balance of:

a. $240,000.

b. $264,000.

c. $270,000.

d. None of these answer choices are correct.

Suppose that Laramie Company’s adjusted trial balance ignored the following

information. For each item of information, indicate what effects, if any, these omissions

would have on the stated components of Laramie Company’s 2016 Income Statement

and 12/31/16 Balance Sheet. Assume no income taxes. Use the following code for your

answers and be sure to include the dollar amounts of the effects next to the letter O or

U: N = No Effect

O = Overstated

U = Understated

In 2016, the internal auditors of KJI Manufacturing discovered the following material

errors made in prior years:

1> Equipment was purchased on June 30, 2014, for $100,000. The purchase was

incorrectly recorded as a debit to repair and maintenance expense. The equipment has a

useful life of five years and no residual value.

2> On March 31, 2015, $50,000 was paid to a contractor to landscape the area around a

manufacturing plant including the installation of a sprinkler system. The expenditure

was debited to the Land account. The landscaping is expected to have a 20-year useful

life and no residual value. KJI uses the straight-line method of depreciation for all

depreciable assets. Required:

1> Prepare the journal entries at December 31, 2016, to correct the errors (ignore

income taxes).

2> Prepare the journal entries to record 2016 depreciation for any assets recorded in

requirement 1.

The Santiago Corporation provides an executive stock option plan. Under the plan, the

company granted options on January 1, 2016, that permit executives to acquire 70

million of the company’s $1 par value common shares within the next eight years, but

not before December 31, 2019 (the vesting date). The exercise price is the market price

of the shares on the date of the grant, $27 per share. The fair value of the options,

estimated by an appropriate option pricing model, is $4 per option. No forfeitures are

anticipated. Ignore taxes.

Required:

1) Determine the total compensation cost pertaining to the options.

2) Prepare the appropriate journal entry (if any) to record the award of options on

January 1, 2016.

3) Prepare the appropriate journal entry (if any) to record compensation expense on

December 31, 2016.

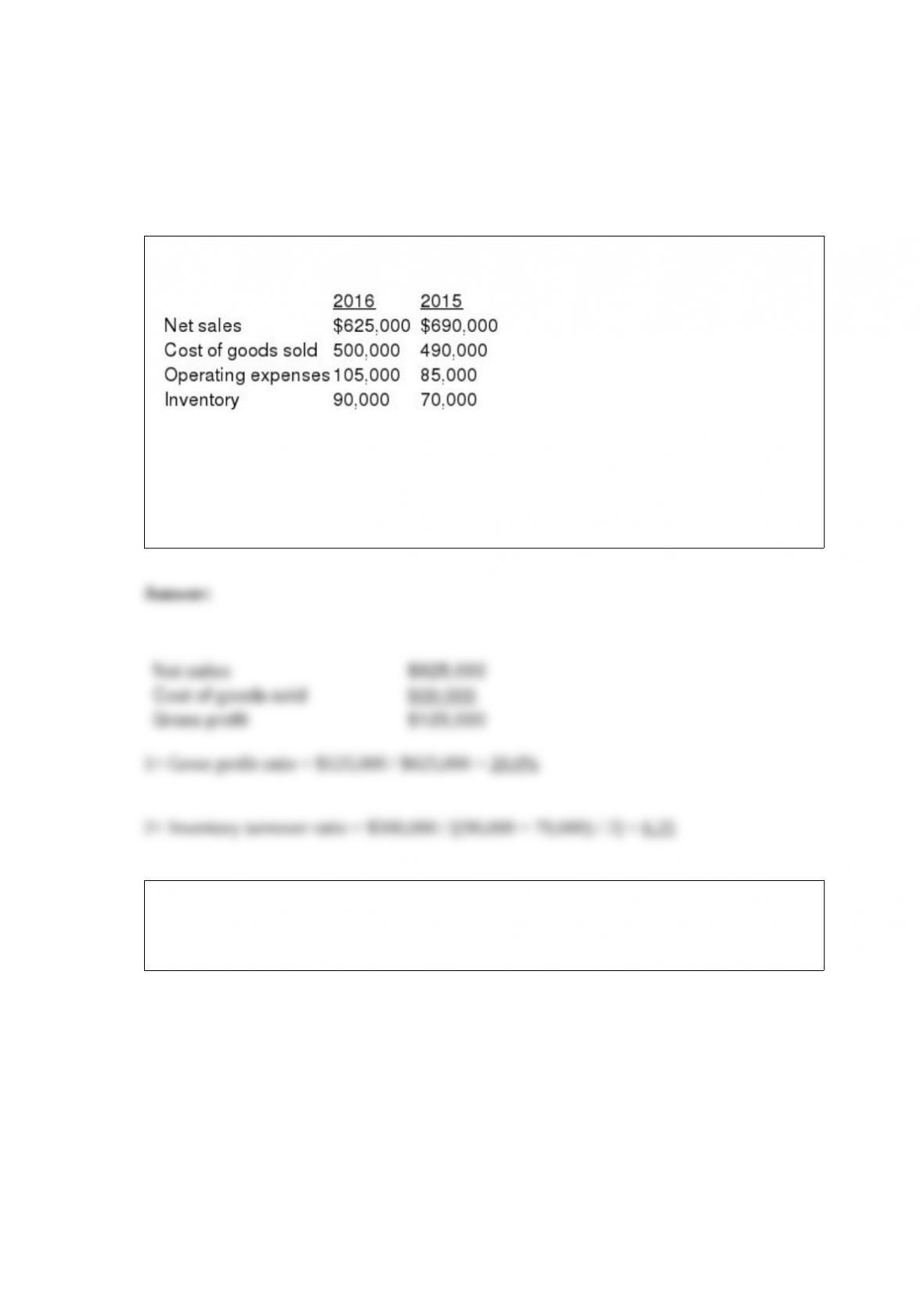

Selected financial statement data from Western Colorado Stores is shown below.

Required:

1> Compute the gross profit ratio for 2016.

2> Compute the inventory turnover ratio for 2016.

Indicate (by number) the way each of the items listed below should be reported in a

balance sheet at December 31, 2016. Match each phrase with the number for the correct

term.

Listed below are columns of time value of money tables for the 9% rate, followed by

labels for five of the columns. Match the columns with their appropriate labels by

placing the letter designating the column in the space provided by the label.

_____ Present value of an annuity due of $1

_____ Future value of an annuity due of $1

_____ Present value of $1

_____ Future value of $1

_____ Present value of an ordinary annuity of $1

Reporting actuarial gains and losses among OCI items in the statement of

comprehensive income also is required under IAS No. 19, referred to as remeasurement

gains and losses. Under IAS No. 19 they are not subsequently amortized to expense and

recycled or reclassified from other comprehensive income as is required under U.S.

GAAP (if the net gain or net loss exceeds the 10% threshold). So, the entry might be

identical to the one in question 2 except we call it a ‘œremeasurement’ loss and the

projected benefit obligation is called the defined benefit obligation (DBO):

($ in millions)

Loss-income statement (from change in assumption) 13

DBO 13