1) An investor uses the cost method of accounting for its investment in common stock.

During the current year, the investor received $25,000 in dividends, an amount that

exceeded the investor’s share of the investee company’s undistributed income since the

investment was acquired. The investor should report dividend income of what amount?

A) $25,000

B) $25,000 less the amount in excess of its share of undistributed income since the

investment was acquired

C) $25,000 less the amount that is not in excess of its share of undistributed income

since the investment was acquired

D) None of the above is correct

2) Pew Corporation acquired 80% ownership of Sordid Incorporated, at a time when

Pew’s investment cost was equal to 80% of Sordid’s book value. At the time of

acquisition, the book values and fair values of Sordid’s assets and liabilities were equal.

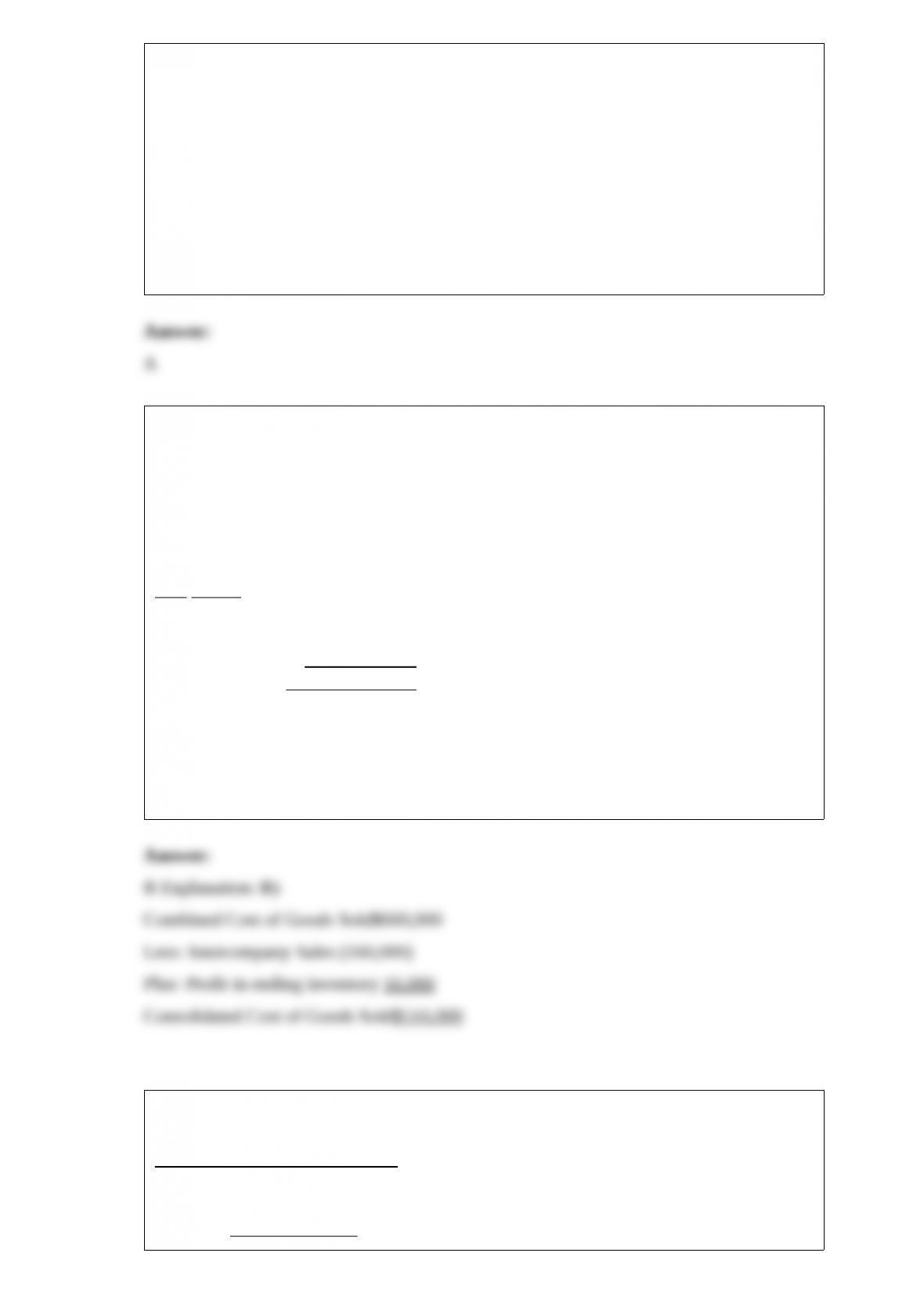

Pew uses the equity method. During 2011, Pew sold goods to Sordid for $160,000

making a gross profit percentage of 20%. Half of these goods remained unsold in

Sordid’s inventory at the end of the year. Income statement information for Pew and

Sordid for 2011 were as follows:

Pew Sordid

Sales Revenue$800,000 $300,000

Cost of Goods Sold500,000160,000

Operating Expenses200,00080,000

Separate incomes$100,000$60,000

The 2011 consolidated income statement showed cost of goods sold of

A) $500,000

B) $516,000

C) $532,000

D) $660,000

3) Pasfield Corporation acquired a 90% interest in Santini Corporation for $90,000 cash

on January 1, 2011 . The following information is available for Santini at that time.

Book ValueFair ValueDifference

Current assets$40,000$50,000$10,000

Plant assets60,00075,00015,000

Liabilities(50,000)(50,000)0

Net assets$50,000$75,000

Under the entity theory, a consolidated balance sheet prepared immediately after the

business combination will show goodwill of

A) $15,000

B) $22,500

C) $25,000

D) $32,500

4) In computing consolidated diluted EPS, the replacement calculation replaces the

parent’s equity in subsidiary earnings with the

A) parent’s share of basic EPS of the subsidiary

B) subsidiary’s share of basic EPS of the parent

C) parent’s share of diluted EPS of the subsidiary

D) subsidiary’s share of diluted EPS of the parent

5) Partnerships

A) are required to prepare annual reports

B) are required to file income tax returns but do not pay Federal income taxes

C) are required to file income tax returns and pay Federal income taxes

D) are not required to file income tax returns or pay Federal income taxes

6) Voluntary health and welfare organizations must report expenses classified by

A) restriction

B) function and natural classification

C) restriction and natural classification

D) restriction, function and natural classification

7) What is a significant difference for agency funds when compared to governmental

funds?

A) An agency fund has a separate ledger

B) An agency fund does not report revenues

C) Agency funds are not associated with any governmental unit

D) An agency fund will not balance because there is no fund balance account

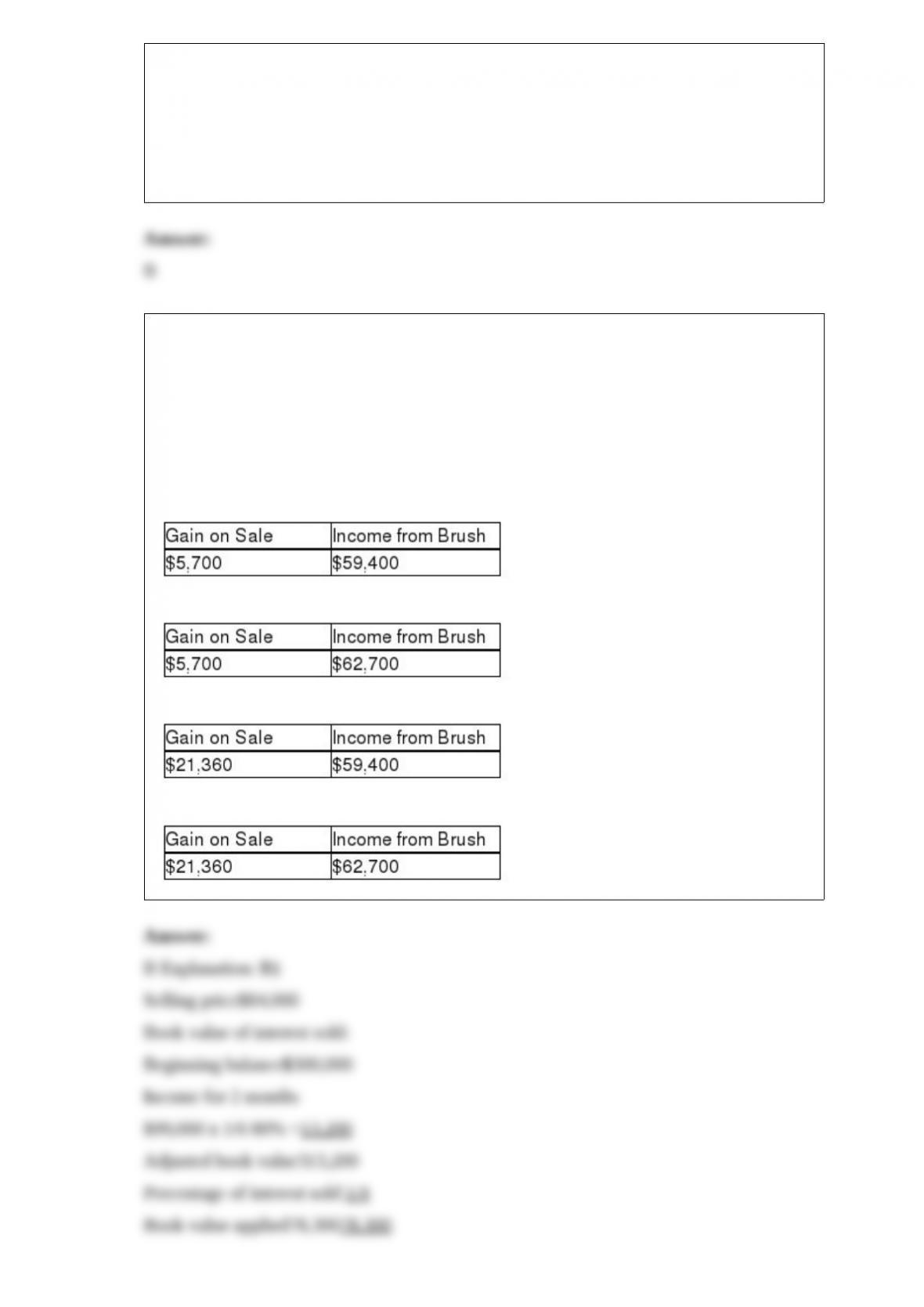

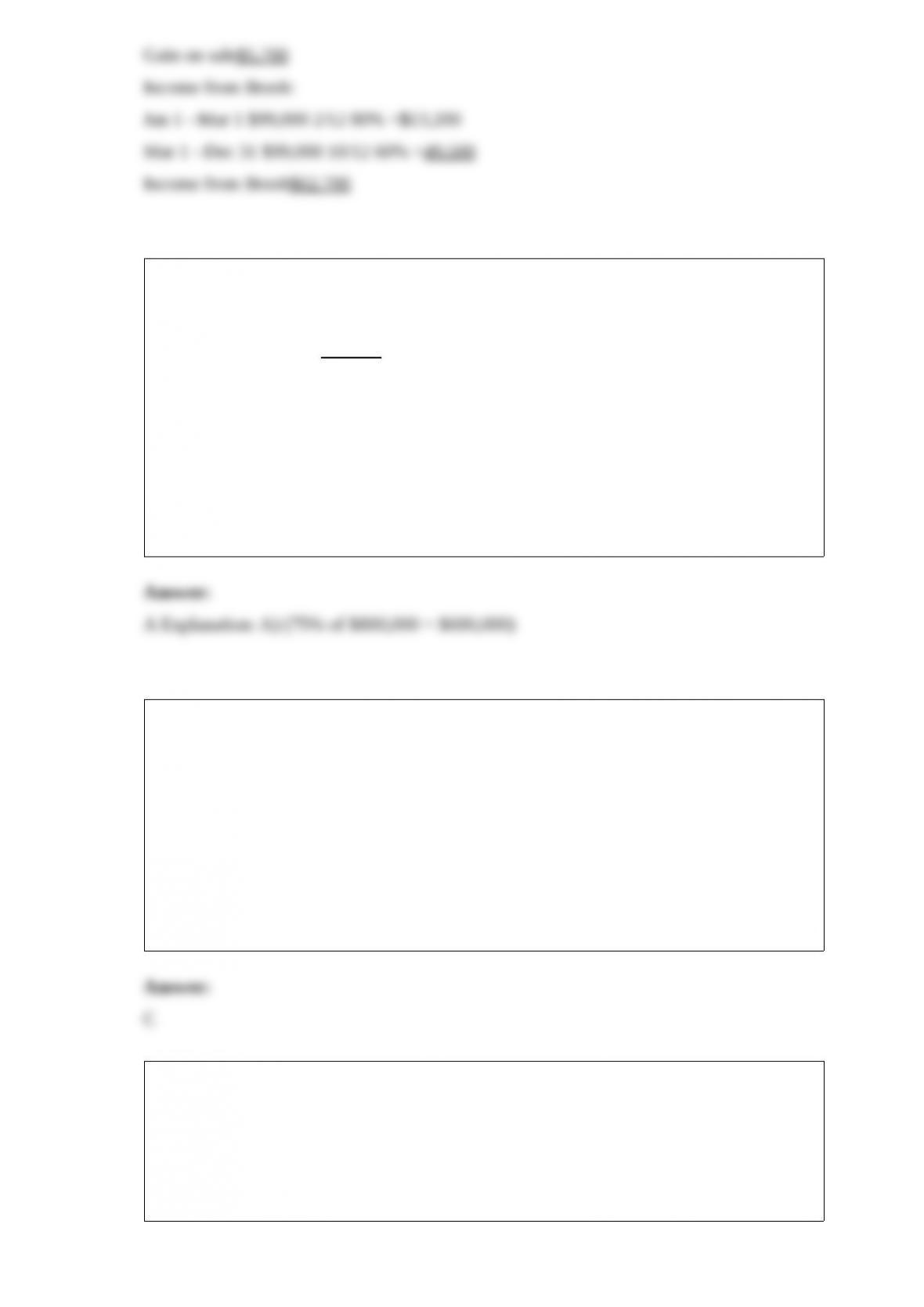

8) Bird Corporation purchased an 80% interest in Brush Corporation on July 1, 2010 at

its book value, and on January 1, 2011 its Investment in Brush account was $300,000,

equal to its book value. Brush’s net income for 2011 was $99,000 (earned uniformly);

no dividends were declared. On March 1, 2011, Bird reduced its interest in Brush by

selling a 20% interest, one-fourth of its investment, for $84,000.

If Bird uses the “actual-sale-date” sales assumption, its gain on the sale and income

from Brush for 2011 will be

A)

B)

C)

D)

9) Cole Company has the following 2011 financial data:

Consolidated revenue per income statement$800,000

Intersegment sales200,000

Intersegment transfers100,000

Combined revenues of all segments$1,100,000

Cole Company should add segments if

A) the sum of its segments’ external revenue does not exceed $600,000

B) the sum of its segments’ external revenue does not exceed $825,000

C) the sum of its segments’ revenue including intersegment revenue does not exceed

$600,000

D) the sum of its segments’ revenue including intersegment revenue does not exceed

$825,000

10) If the yield curve slope is flat for short maturities and then slopes steeply upward

for longer maturities, the liquidity premium theory (assuming a mild preference for

shorter-term bonds) indicates that the market is predicting

A) a rise in short-term interest rates in the near future and a decline further out in the

future

B) constant short-term interest rates in the near future and further out in the future

C) a decline in short-term interest rates in the near future and a rise further out in the

future

D) constant short-term interest rates in the near future and a decline further out in the

future

11) What is the purpose of interim reporting?

A) Provide shareholders with more timely information

B) Provide shareholders with more accurate information

C) Provide shareholders with more extensive detail about specific accounts and

transactions

D) Provide shareholders with more current audited information

12) A plot of the interest rates on default-free government bonds with different terms to

maturity is called

A) a risk-structure curve

B) a default-free curve

C) a yield curve

D) an interest-rate curve

13) When the Treasury bond market becomes more liquid, other things equal, the

demand curve for corporate bonds shifts to the ________ and the demand curve for

Treasury bonds shifts to the ________

A) right; right

B) right; left

C) left; right

D) left; left

14) Papal Corporation acquired an 80% interest in Sandman Corporation at a cost equal

to 80% of the book value of Sandman’s net assets in 2010 . At the time of the

acquisition, the book values and fair values of Sandman’s assets and liabilities were

equal. During 2011, Papal recorded sales of $440,000 of merchandise to Sandman at a

gross profit rate of 30%. Sandman’s beginning and ending inventories for 2011 were

$60,000 and $80,000, respectively. Income statement information for both companies

for 2011 is as follows:

PapalSandman

Sales Revenue$1,660,000$580,000

Invest.income from Sandman 59,600

Cost of Goods Sold(1,060,000)(394,000)

Expenses(358,000)(104,000)

Net Income$301,600$82,000

Required:

Prepare a consolidated income statement for Papal Corporation and Subsidiary for 2011

.

15) On November 1, 2010, Stateside Company (a U.S. manufacturer) sold an airplane

for 1 million New Zealand dollars (NZ$) to New Zealand company Aukland

Corporation. Stateside will receive payment on January 30, 2011 in New Zealand

dollars. In order to hedge the accounts receivable position, Stateside entered into a

90-day forward contract to sell 1 million New Zealand dollars on January 30, 2011 . On

November 1, 2010, the 90-day forward rate is US$0.73 per New Zealand dollar. The

forward contract will be settled net. Account for the hedge as a fair value hedge. Ignore

the time value of money.

The relevant exchange rates per New Zealand dollar:

Spot Rate Forward Rate to 1/30/11

Nov. 1, 2010US$0.73US$0.73

Dec. 31, 2010US$0.75US$0.76

Jan. 30, 2011US$0.79US$0.79

Required:

Record the journal entries that Stateside would need to prepare at November 1, 2010,

December 31, 2010 and January 30, 2011 .

December 31, 2010 is the fiscal year end.

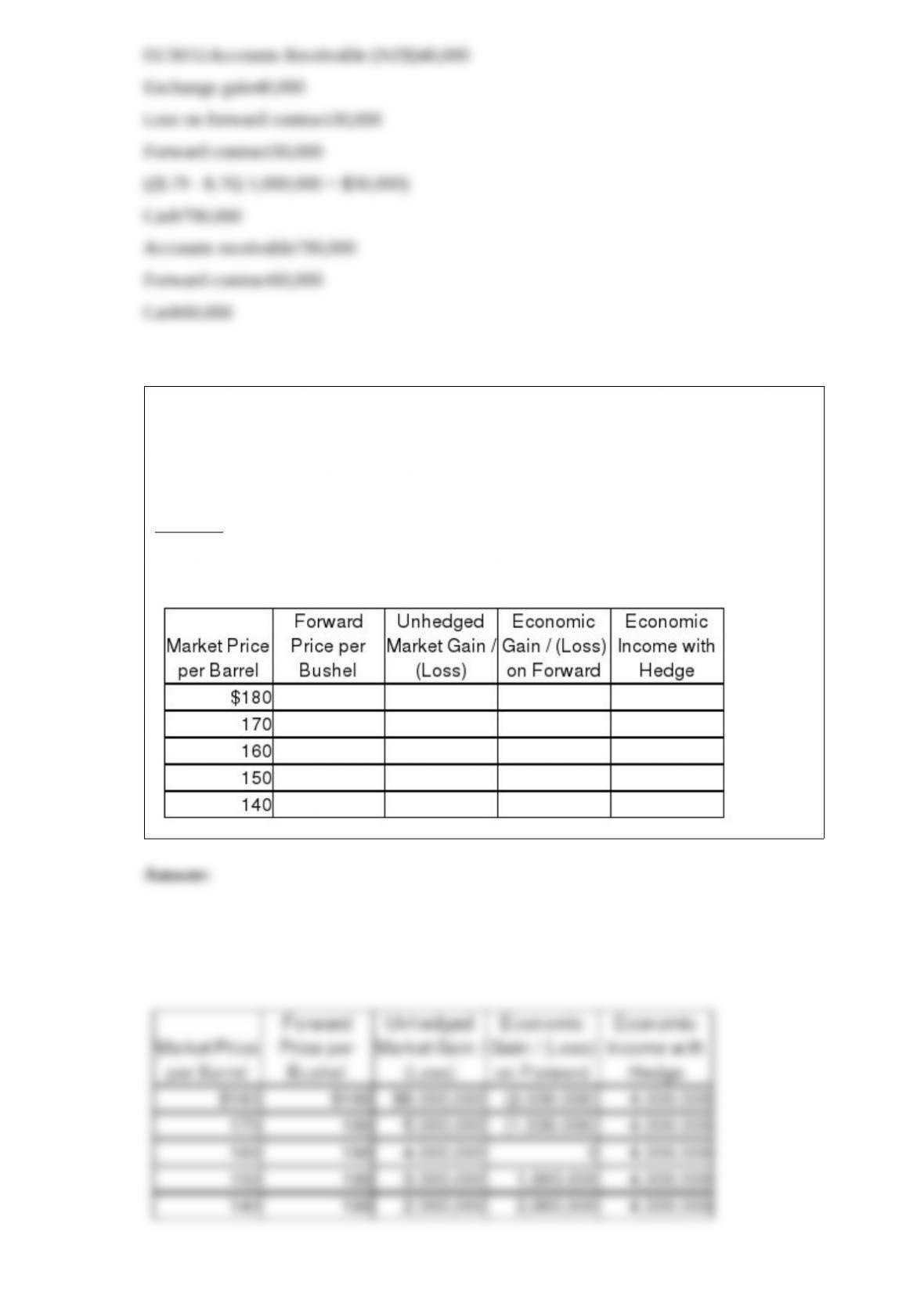

16) In September of 2011, Gunny Corporation anticipates that the price of heating oil

will increase soon, and wishes to lock in a firm price for the winter months. They enter

into a forward contract with Selton Industries to buy 100,000 barrels of oil at $160 per

barrel in December 2011 . Selton’s cost of production of the heating oil is $120 per

barrel.

Required:

Determine the economic impact of the transaction to Selton (the seller of the heating

oil) at the market price levels indicated in the table below, with and without the hedge.

17) For internal decision-making purposes, Calam Corporation’s operating segments

have been identified as follows:

Operating

ProfitIdentifiable

Operating SegmentRevenuesor LossAssets

Appliances$110,000$(15,000)$120,000

Clothing130,000(75,000)40,000

Lawn and Garden85,00015,00015,000

Auto Accessories100,00010,00020,000

Service Contracts65,000(5,000)10,000

Catalog Sales230,0005,00050,000

Home Furnishings280,00025,000100,000

Tools240,00030,00025,000

$1,240,000(10,000)$380,000

Required:

1>In applying the “operating profit or loss” test to identify reporting segments, what is

the test value for Calam Corporation?

2>Using the “reported profit or loss” test, which of Calam’s operating segments will

also be reporting segments?

18) A review of Ace Industries, a U.S. corporation, shows the following balances in

accounts receivable and accounts payable detail at September 30, 2011, their fiscal year

end.

ACCOUNTS RECEIVABLE

Receivables denominated in U.S. dollar$426,000

Receivable denominated in 40,000 Australian dollar43,000

Receivable denominated in 70,000 Canadian dollar71,750

$ 540,750

ACCOUNTS PAYABLE

Payables denominated in U.S. dollar$ 107,000

Payable denominated in 50,000 Canadian dollar51,250

Payable denominated in 200,000 Hong Kong dollar26,500

$ 184,750

As Ace prepared to close their books, they noted that the September 30 exchange rates

for the Australian dollar, Canadian dollar and Hong Kong dollar were $1.0366, $1.0301

and $0.1284, respectively.

Required:

Determine the exchange gain or loss to be included in the 2011 financial statements,

and the amount of Accounts Receivable and Accounts Payable that will be included on

the September 30, 2011 balance sheet.

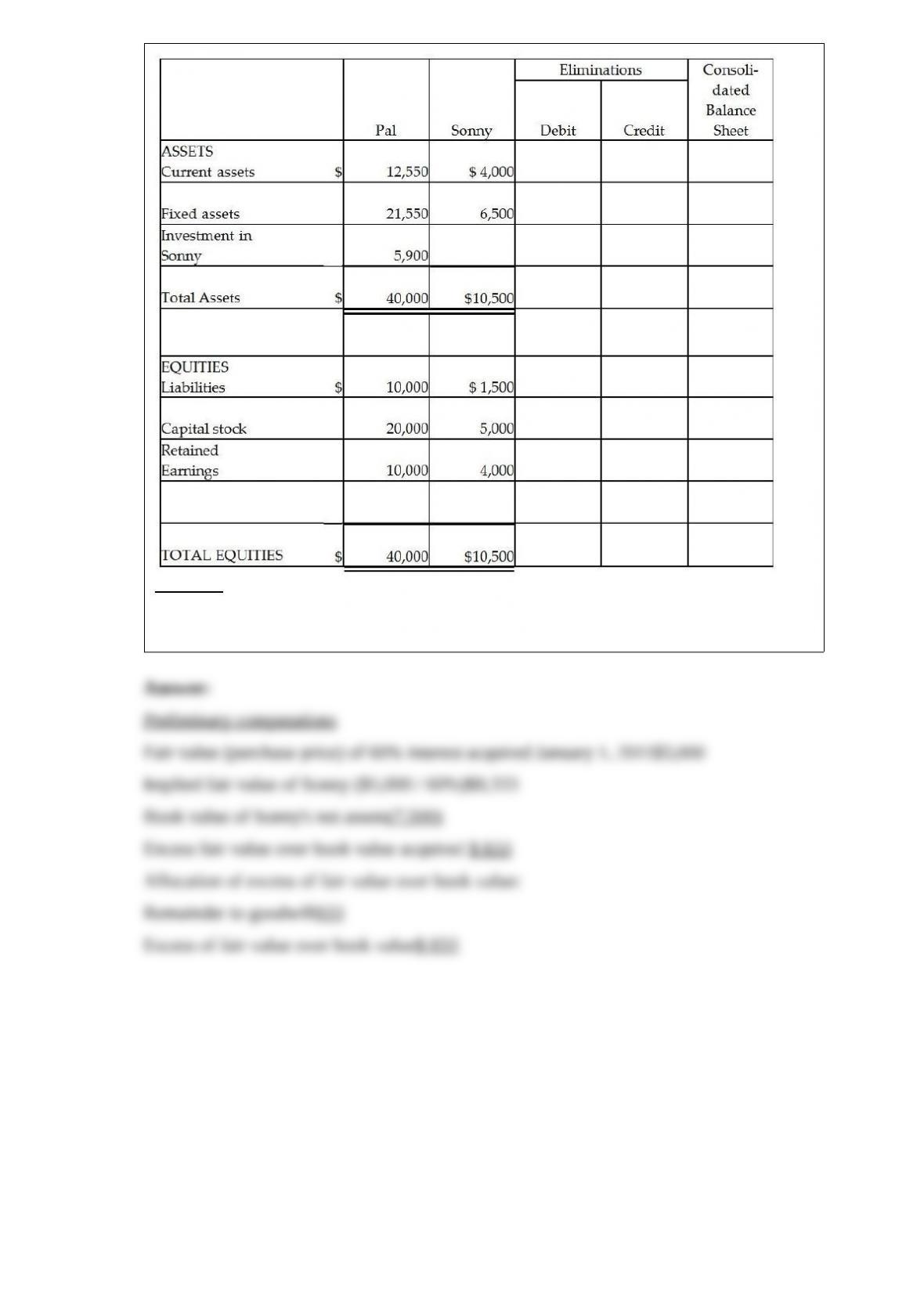

19) Pal Corporation paid $5,000 for a 60% interest in Sonny Inc. on January 1, 2011

when Sonny’s stockholders’ equity consisted of $5,000 Capital Stock and $2,500

Retained Earnings. The fair value and book value of Sonny’s assets and liabilities were

equal on this date. Two years later, on December 31, 2012, the balance sheets of Pal and

Sonny are summarized as follows:

Required:

Complete the consolidated balance sheet working papers for Pal Corporation and

Subsidiary at December 31, 2012 .

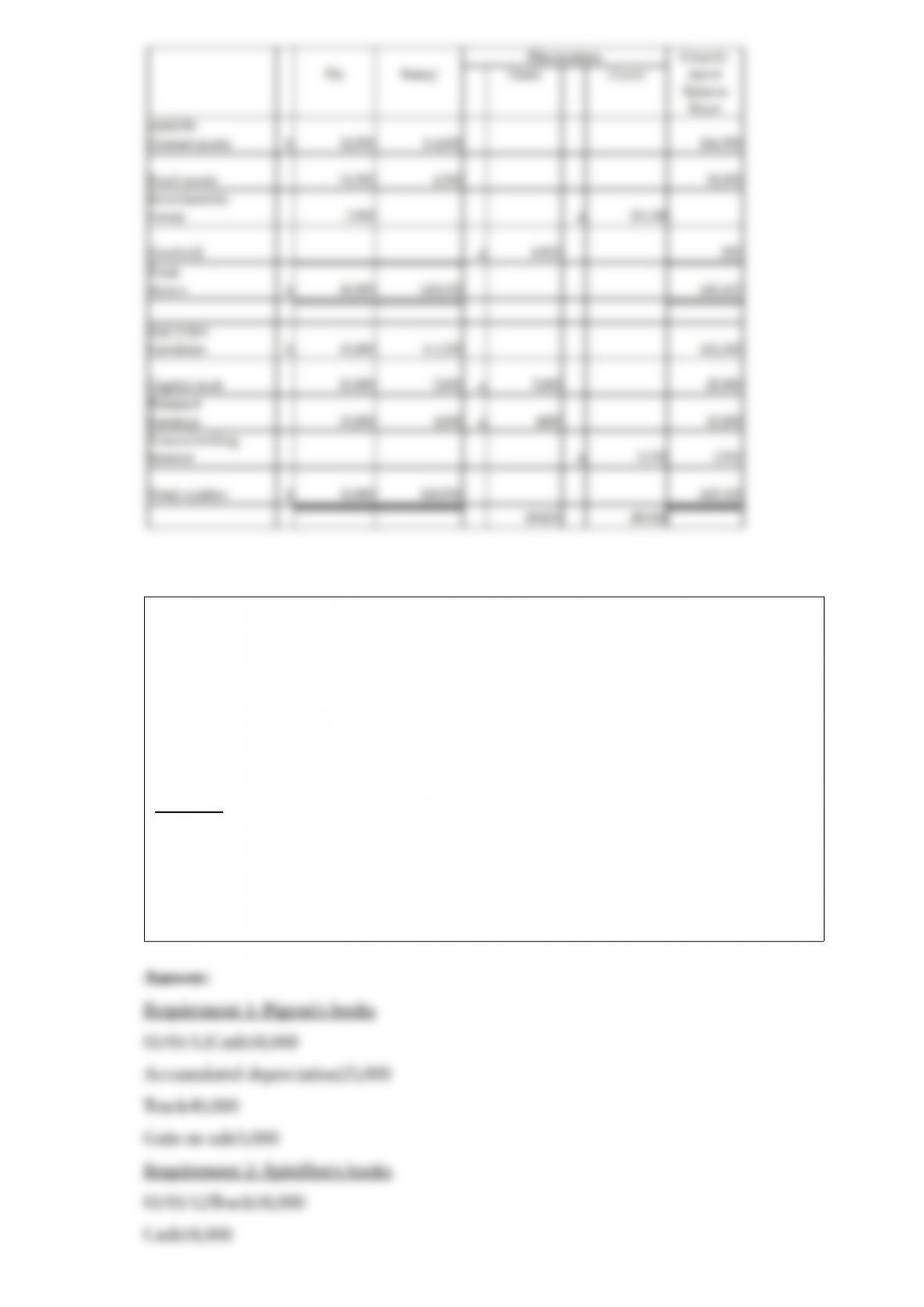

20) Pigeon Company owns 80% of the outstanding stock of Spiniflex Corporation,

which was purchased on January 1, 2006, when Spiniflex’s book values were equal to

its fair values. The amount paid by Pigeon included $16,000 for goodwill.

On January 1, 2007, Pigeon purchased a truck for $40,000 which had no salvage value

with a useful life of 8 years, depreciated on a straight-line basis. On January 1, 2012,

Pigeon sold the truck to Spiniflex Corporation for $18,000. The truck was estimated to

have a three-year remaining life on this date and no salvage value. All affiliates use the

straight-line depreciation method.

Required:

Prepare all relevant entries with respect to the truck.

1>Record the journal entries on Pigeon’s books for 2012 .

2>Record the journal entries on Spiniflex’s books for 2012 .

3>Prepare the consolidation entries required for Pigeon and subsidiary for 2012 as a

result of this transaction.

21) Stello Corporation’s stockholders’ equity on December 31, 2010 was as follows:

10% cumulative preferred stock, $100 par value,

callable at $110, with no dividends in arrears$100,000

Common stock, $1 par value300,000

Additional paid-in capital40,000

Retained earnings160,000

Total stockholders’ equity$600,000

On January 1, 2011, Kaprelian Corporation paid $300,000 for a 90% interest in Stello’s

common stock. On January 1, 2011, the book values of Stello’s assets and liabilities

were equal to fair values. On January 2, 2011, Kaprelian Corporation paid $100,000 for

a 90% interest in Stello’s preferred stock.

Required:

1> Determine the book value of the common stockholders’ equity for Stello Corporation

on January 1, 2011 .

2> Prepare the journal entry(ies) on January 1, 2011 for Kaprelian Corporation.

3> Prepare the journal entry(ies) on January 2, 2011 for Kaprelian Corporation.

4> For the year ending December 31, 2011, Stello Corporation reported net income of

$50,000. Stello Corporation declared and paid dividends of $10,000 to preferred

stockholders and $10,000 to common stockholders. Prepare the journal entries for

Kaprelian Corporation relating to this information.

22) On December 18, 2011, Wabbit Corporation (a U.S. Corporation) has a Forward

Contract recorded on their ledger as a debit balance of $17,500. The forward contract

was related to a purchase of electronic components purchased overseas, which were

going to be re-sold in the United States. On December 20, the forward contract was

settled with a payment of $20,000, and the related parts which cost $118,000 were sold

for $160,000 cash. The forward contract is set up to lock in the price for the electronic

components when they are sold. The forward contract was settled net. Assume this is a

cash flow hedge.

Required:

Prepare the journal entries required by Wabbit on December 20 .

23) On January 1, 2011, Paisley Incorporated paid $300,000 for 60% of Smarnia

Company’s outstanding capital stock. Smarnia reported common stock on that date of

$250,000 and retained earnings of $100,000. Plant assets, which had a five-year

remaining life, were undervalued in Smarnia’s financial records by $10,000. Smarnia

also had a patent that was not on the books, but had a market value of $60,000. The

patent has a remaining useful life of 10 years. Any remaining fair value/book value

differential is allocated to goodwill. Smarnia’s net income and dividends paid the first

three years that Paisley owned them are shown below.

Net Dividends

IncomePaid

201180,00030,000

201290,00010,000

201360,00020,000

Requirement 1: Calculate the noncontrolling interest share in Smarnia’s income for each

of the three years.

Requirement 2: Calculate the noncontrolling interest that should be reported on the

consolidated balance sheet at the end of each of the three years.

Requirement 3: Assuming that Paisley uses the equity method to record their

investment in Smarnia, calculate the ending balance in the Investment in Smarnia

account for each of the three years.