1) The ________ is a contract between a carrier (e.g., a trucking company) and the

seller of goods that dictates the details surrounding the shipment of goods.

A) bill of lading

B) sales invoice

C) picking ticket

D) remittance advice

2) The auditor’s objectives for the sales and cash collections activities when the client is

primarily an e-commerce business as compared to a “bricks and mortar” business are:

A) unchanged

B) expanded

C) mitigated

D) decreased

3) An auditor’s independence is considered impaired if the auditor has:

A) an immaterial, indirect financial interest in a client

B) an outstanding $8,000 balance on a credit card issued by a client

C) an automobile loan from a client bank, collateralized by the automobile

D) a joint, closely held business investment with the client that is material to the

auditor’s net worth

4) Which of the following audit procedures would most likely assist an auditor in

identifying conditions and events that may indicate there could be substantial doubt

about an entity’s ability to continue as a going concern?

A) review compliance with the terms of debt agreements

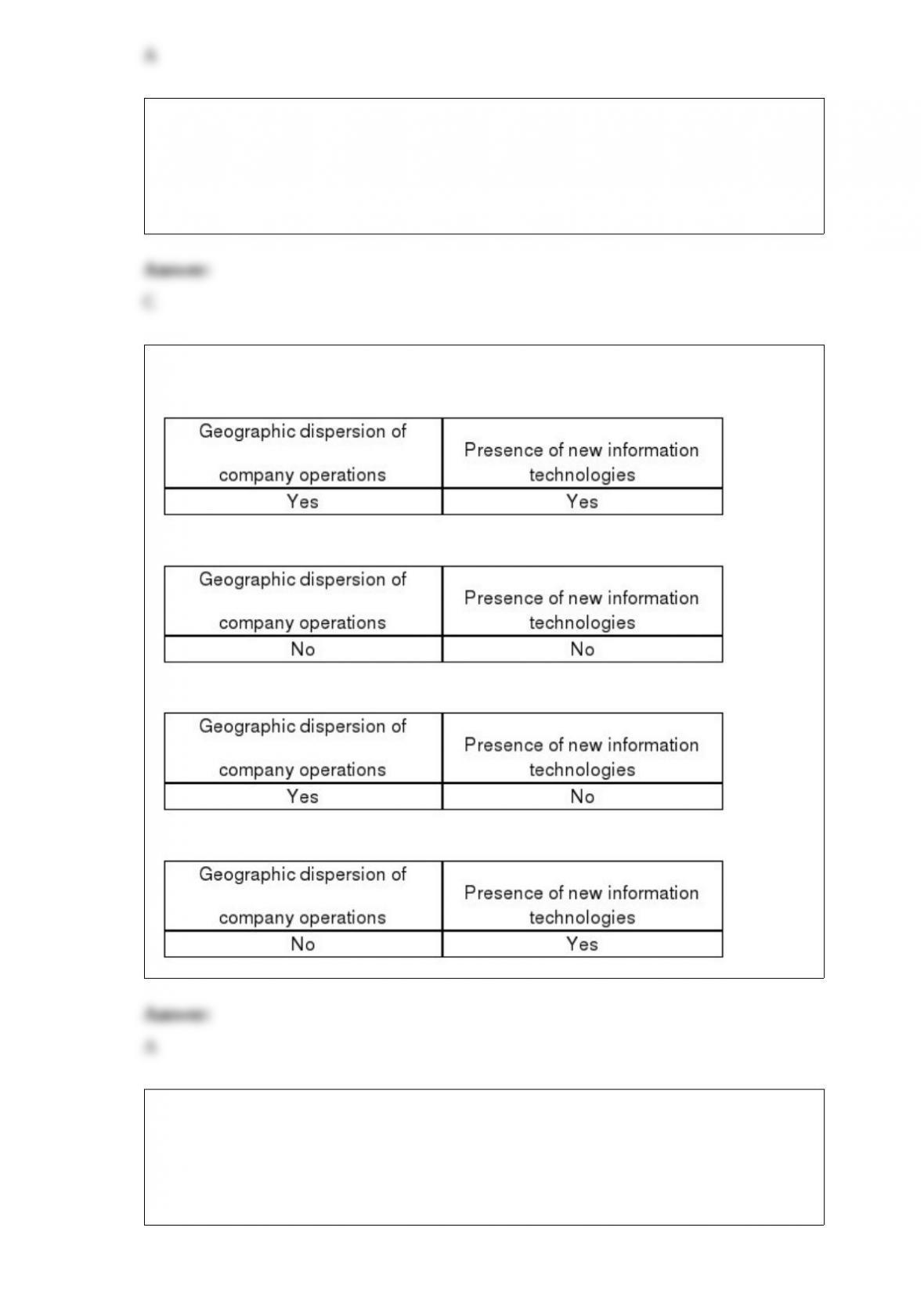

B) confirmation of accounts receivable from principal customers

C) reconciliation of interest expense with debt outstanding

D) confirmation of bank balances

5) The most important aspect of evaluating the client’s method of obtaining a reliable

cutoff is to:

A) perform extensive detailed testing of cutoff

B) evaluate the client’s control procedures around cutoff

C) confirm a sample of transactions near period end with customers

D) confirm transaction with customers

6) Audit reports issued for financial statements of a public company should refer to

generally accepted auditing standards in the scope paragraph.

A) True

B) False

7) Three common types of attestation services are:

A) audits, reviews, and attestations regarding internal controls

B) audits, verifications, and attestations regarding internal controls

C) reviews, verifications, and attestations regarding internal controls

D) audits, reviews, and verifications

8) There must be a periodic physical count by the client of the inventory items on hand:

A) only if the client uses the LIFO method

B) only if the client uses a lower-of-cost-or-market method

C) regardless of the client’s inventory valuation method

D) only if the client uses either the LIFO or FIFO method

9) When examining payroll transactions, an auditor is primarily concerned with the

possibility of:

A) incorrect summaries of employee time records

B) overpayments and unauthorized payments

C) under withholding of amounts required to be withheld

D) posting of gross payroll amounts to incorrect salary expense accounts

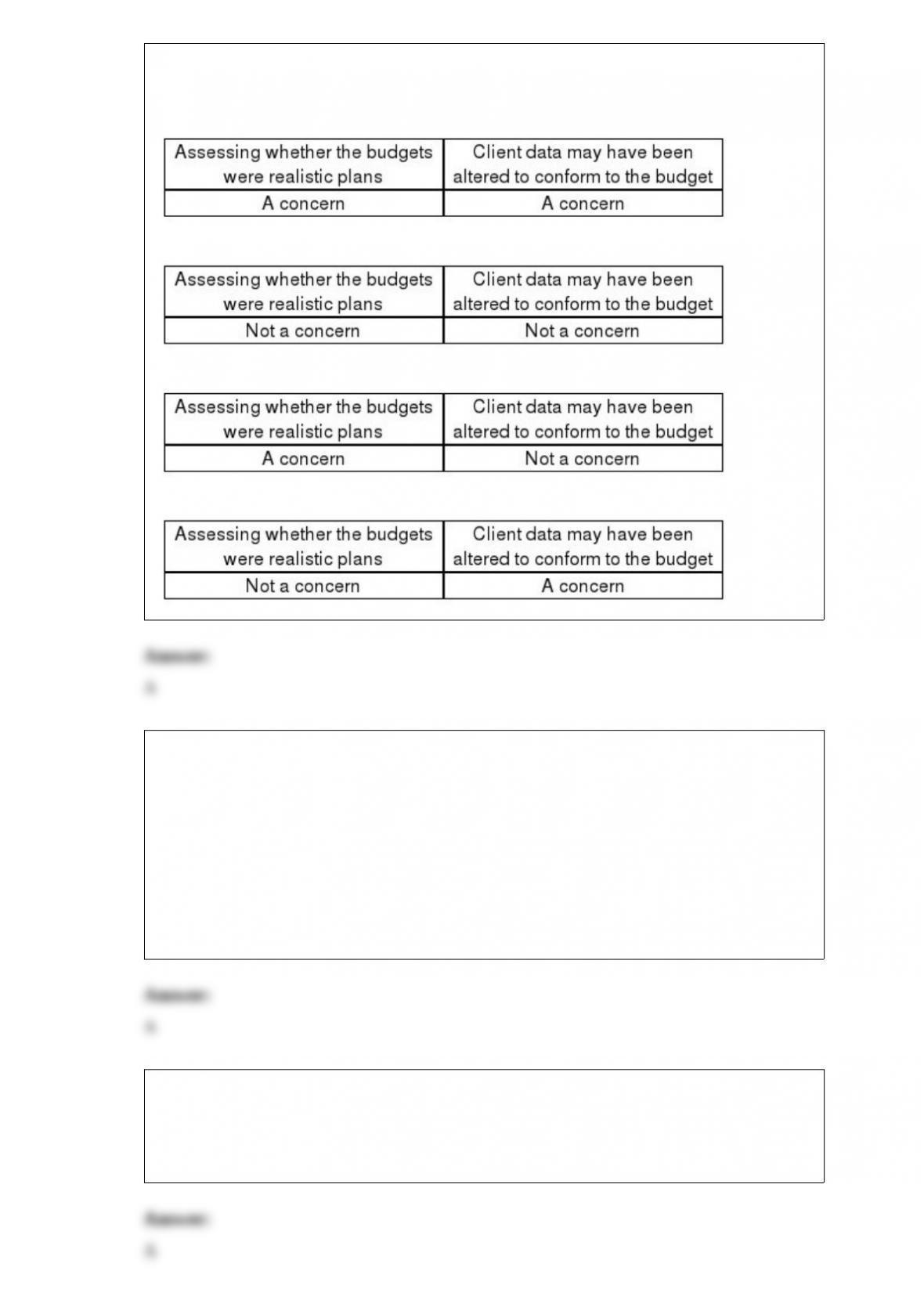

10) Whenever an auditor compares client data to client-prepared budgets, there are two

special concerns. Indicate if the two items below are concerns.

A)

B)

C)

D)

11) Proper separation of duties is useful to prevent various types of misstatements.

Which of the following is not an essential separation of duties?

A) Persons having access to cash should also be responsible for recording sales,

accounts receivable, and cash

B) Separate the credit-granting function from the sales function

C) Personnel doing internal comparisons should be independent of those entering the

original data

D) Anyone responsible for entering sales and cash receipts transactions information into

the computer should be denied access to cash

12) The extent and timing of an auditor’s physical examination of inventory is

significantly influenced by the adequacy of the client’s perpetual inventory records.

A) True

B) False

13) Auditors tests of the client’s bank reconciliation is done to verify whether the

client’s recorded bank balance is the same amount as the actual cash in the bank. Which

of the following would not explain a difference between the company’s cash balance

and the bank’s balance for the client?

A) Deposits in transit

B) Cash collected on a Note Receivable by the bank

C) Other reconciling items

D) Outstanding checks

14) In connection with the annual audit, which of the following is not a ‘subsequent

events” procedure?

A) Review available interim financial statements

B) Read available minutes of meetings of stockholders, directors, and committees and,

for meetings where minutes are not available, inquire about matters dealt with at such

meetings

C) Make inquiries with respect to the financial statements covered by the auditor’s

previously issued report if new information has become available during the current

examination that might affect that report

D) Discuss with officers the current status of items in the financial statements that were

accounted for on the basis of tentative, preliminary, or inconclusive data

15) In testing controls, an overreliance on internal controls that reduces substantive tests

and increases the likelihood of not detecting a material misstatement occurs because:

A) true deviation in the population was less than the sample

B) true deviation in the population was greater than the sample

C) auditor judgment was flawed

D) it is inherent in the audit risk model

16) The first step in verifying the valuation of purchased inventory is in determining the

valuation method used by the client. The 2nd step is:

A) determining that all inventory that is purchased is expensed through cost of goods

sold

B) determining which costs should be included in the valuation of an item of inventory

C) determining that all inventory on hand reconciles to the perpetual inventory records

D) determining that cut-off procedures have been adhered to prior to counting inventory

17) You are auditing Rodgers and Company. You are aware of a potential loss due to

non-compliance with environmental regulations. Management has assessed that there is

a 40% chance that a $10M payment could result from the non-compliance. The

appropriate financial statement treatment is to:

A) accrue a $4 million liability

B) disclose a liability and provide a range of outcomes

C) since there is less than a 50% chance of occurrence, ignore

D) since there is greater that a remote chance of occurrence, accrue the $10 million

18) Matching the supplier’s invoice, the purchase order, and the receiving report prior to

preparing the voucher would normally be the responsibility of the:

A) warehouse receiving function

B) purchasing function

C) general accounting function

D) treasury function

19) Contingent liability disclosure in the footnotes of the financial statements would

normally be made when:

A) the outcome of the accounting event is deemed probable, but a reasonable estimation

as to the amount cannot be made by the client or auditor

B) a reasonable estimation of the loss can be made, but the outcome is not probable

C) the outcome of the accounting event is deemed probable, and a reasonable

estimation as to the amount can be made

D) the outcome of the accounting event as well as a reasonable estimation of the loss

cannot be made

20) The test of details of balances procedure to “examine vendors’ invoices of closely

related accounts such as repairs to uncover items that should be property, plant, and

equipment” satisfies the audit objective of:

A) completeness

B) detail tie-in

C) cutoff

D) existence

21) Privity of contract exists between:

A) auditor and the federal government

B) auditor and third parties

C) auditor and client

D) auditor and client attorney

22) Which of the following factors may increase risks to an organization?

A)

B)

C)

D)

23) Which of the following would most likely be deemed a direct-effect illegal act?

A) violation of federal employment laws

B) violation of federal environmental regulations

C) violation of federal income tax laws

D) violation of civil rights laws

24) Which of the following would generally not need to be approved by the board of

directors?

A) Issuing capital stock

B) Repurchasing capital stock

C) Declaration of a Dividend

D) Payment of a Dividend

25) The auditor’s evaluation of the likelihood of material employee fraud is normally

done initially as a part of:

A) tests of controls

B) tests of transactions

C) understanding the entity’s internal control

D) the assessment of whether to accept the audit engagement

26) CPAs can issue a WebTrust opinion only on all five Trust Services principles.

A) True

B) False

27) In the context of the audit of sales, distinguish between the existence and

completeness transaction-related audit objectives. State the effect on the sales account

(overstatement or understatement) of a violation of each objective.

28) What are the six Ethical Principles stated in the Code of Professional Conduct?

Briefly discuss each principle. Are these principles enforceable?

29) Auditors frequently audit statements prepared on bases other than GAAP. Discuss

four commonly used bases other than GAAP.

30) State the three purposes of the client letter of representation.

31) Explain kiting, and discuss how it is performed.

32) Three approaches to the application of the foreseen users’ concept are (1) the Credit

Alliance approach, (2) the restatement of torts approach, and (3) the foreseeable user

approach. Summarize each of these three approaches.

33) Distinguish between constructive fraud and fraud.

34) Explain why it is necessary to allocate the preliminary judgment about materiality

to individual accounts (segments) in the financial statements. Also explain why

allocating to balance sheet accounts is more common than allocating to income

statement accounts.

35) The International Standards for the Professional Practice of Auditing list 7

performance standards. List three.

36) List four specific matters that should be included in a client representation letter.