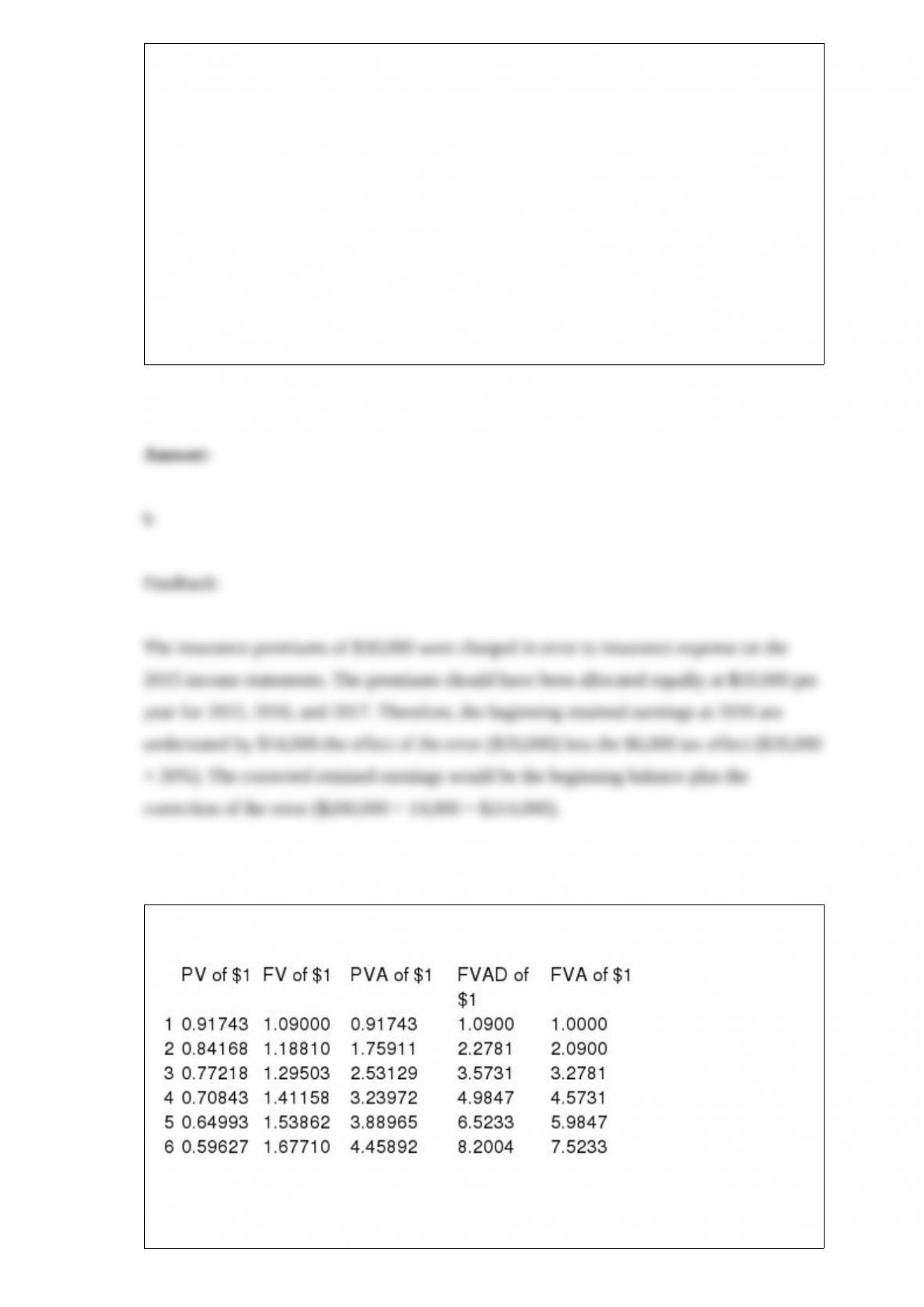

C Co. reported a retained earnings balance of $200,000 at December 31, 2015. In

September 2016, C determined that insurance premiums of $30,000 for the three-year

period beginning January 1, 2015, had been paid and fully expensed in 2015. C has a

30% income tax rate. What amount should C report as adjusted beginning retained

earnings in its 2016 statement of retained earnings?

a. $210,000.

b. $214,000.

c. $220,000.

d. $221,000.

Present and future value tables of 1 at 9% are presented below.

Claudine Corporation will deposit $5,000 into a money market sinking fund at the end

of each year for the next five years. How much will accumulate by the end of the fifth

and final payment if the sinking fund earns 9% interest?

a. $32,617.

b. $29,924.

c. $27,250.

d. $26,800.

If unexpected turnover in 2017 caused the company to estimate that 10% of the options

would be forfeited, what amount should M recognize as compensation expense for

2017?

On January 1, 2016, M Company granted 90,000 stock options to certain executives.

The options are exercisable no sooner than December 31, 2018, and expire on January

1, 2022. Each option can be exercised to acquire one share of $1 par common stock for

$12. An option-pricing model estimates the fair value of the options to be $5 on the date

of grant.

a. $ 30,000.

b. $ 60,000.

c. $120,000.

d. $150,000.

Which of the following causes a permanent difference between taxable income and

pretax accounting income?

a. The installment method used for sales of property.

b. MACRS depreciation method used for equipment.

c. Interest income on municipal bonds.

d. Percentage-of-completion method for long-term construction contracts.

Recording the expense for postretirement benefits will not:

a. Increase the APBO.

b. Increase the postretirement benefit assets.

c. Decrease the prior service cost.

d. Increase the net loss-AOCI.

Waldman Associates received a written, approved contract to deliver economic

consulting services, with service and payment commencing in one month. The contract

specifies the services that Waldman is to perform, and the payment terms. Waldman and

the customer both can cancel the contract without penalty prior to commencing service.

Does Waldman have a contract for purposes of revenue recognition on the day the

contract is received?

a. Yes, because Waldman has a written approved contract.

b. No, because Waldman and the customer can cancel without penalty, and neither has

performed an obligation under the contract.

c. Maybe, depending on whether Waldman can estimate collectability of the receivable.

d. There is insufficient data on which to base an answer.

Which of the following investment securities held by Zoogle Inc. may be classified as

held-to-maturity securities in its balance sheet?

a. Long-term debenture bonds.

b. Common stock.

c. Callable preferred stock.

d. All of these answer choices are correct.

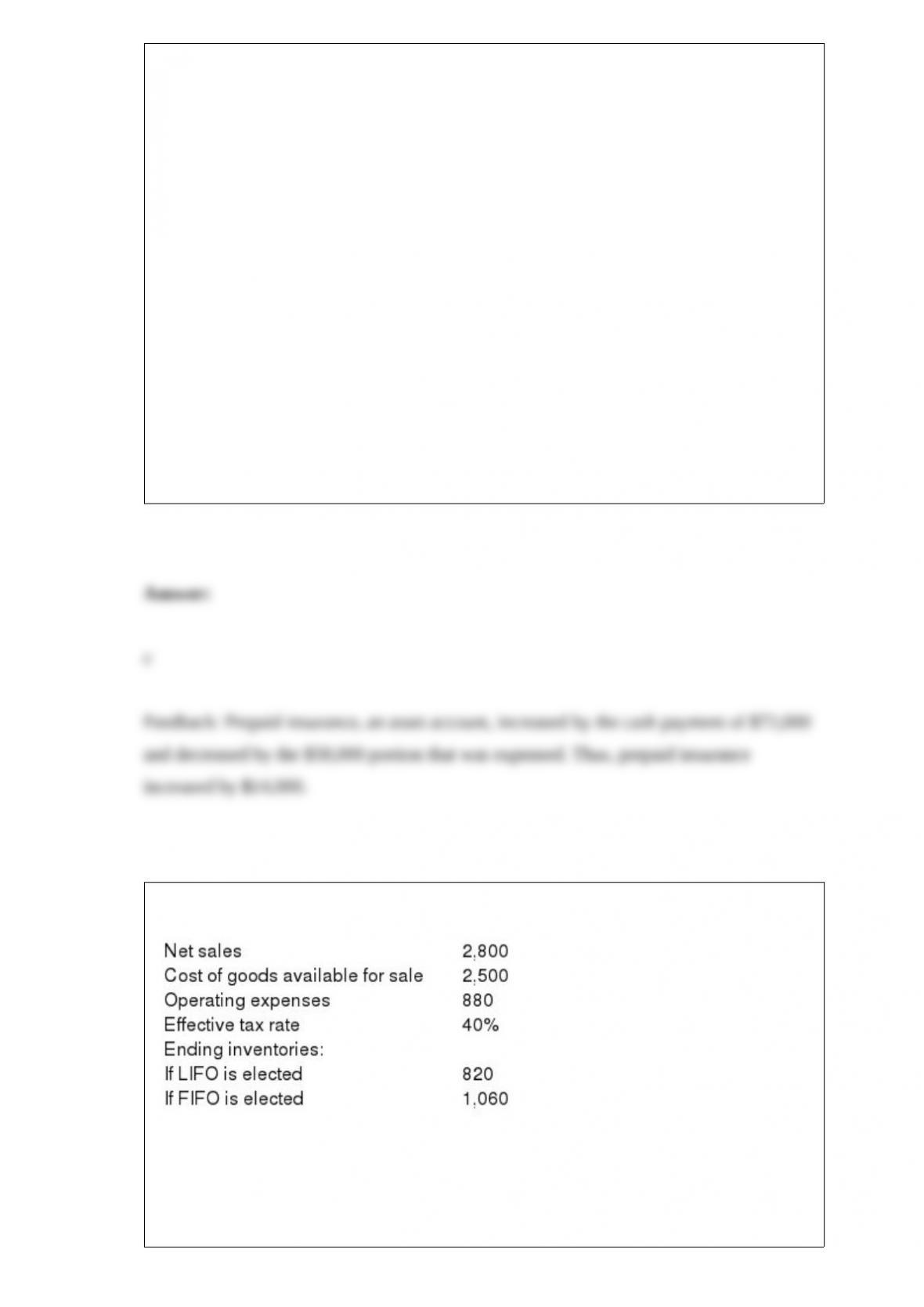

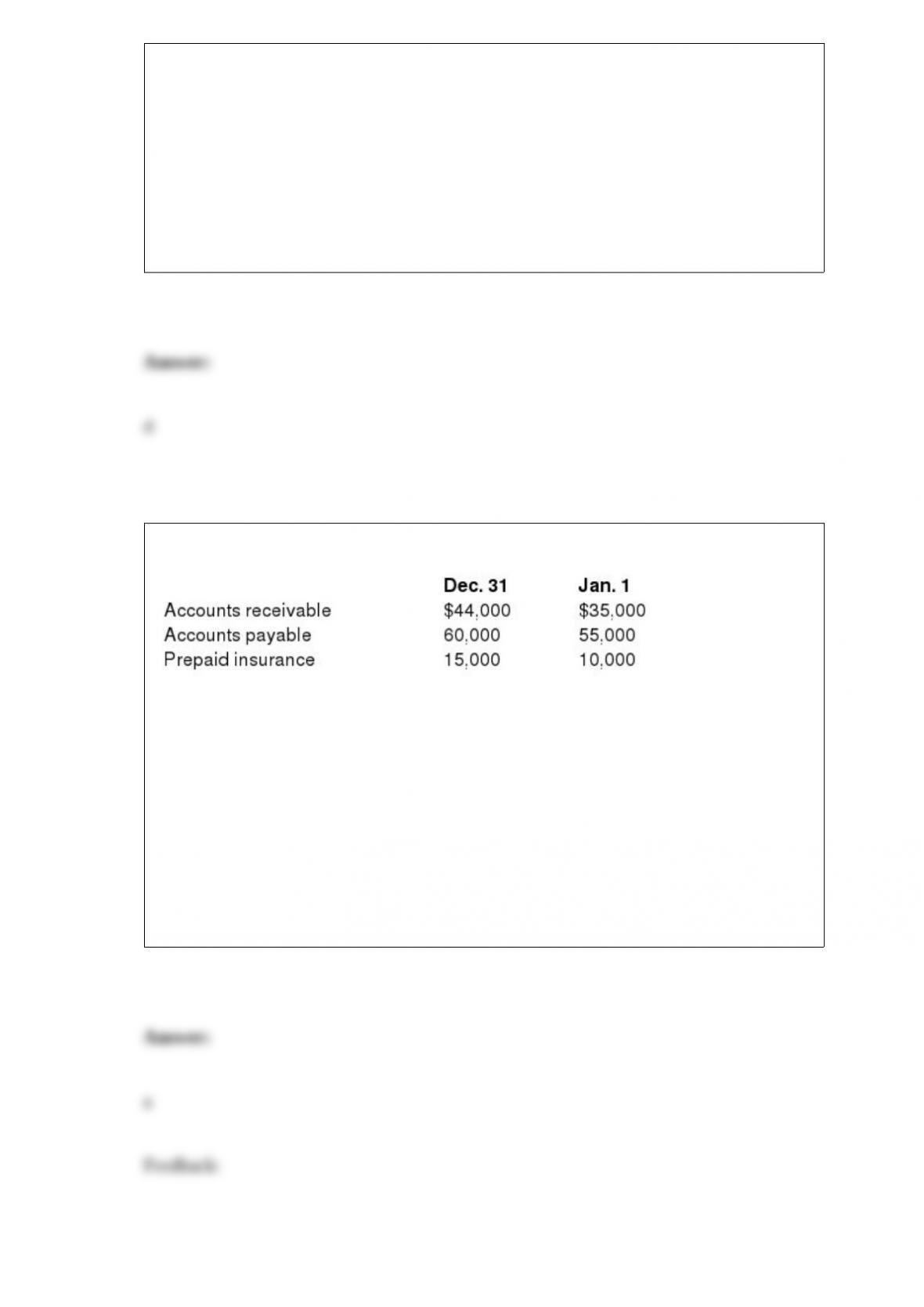

In its 2016 income statement, WME reported $58,000 for insurance expense. WME

paid $72,000 in insurance premiums during 2016. In its reconciliation schedule, WME

should:

Each year, White Mountain Enterprises (WME) prepares a reconciliation schedule that

compares its income statement with its statement of cash flows on both the direct and

indirect method bases.

a. Show a $14,000 positive adjustment to net income under the indirect method for the

increase in prepaid insurance.

b. Show a $14,000 negative adjustment to net income under the indirect method for the

decrease in prepaid insurance.

c. Show a $14,000 negative adjustment to net income under the indirect method for the

increase in prepaid insurance.

d. Show a $14,000 positive adjustment to net income under the indirect method for the

decrease in prepaid insurance.

Nu Company reported the following pretax data for its first year of operations.

What is Nu’s net income if it elects FIFO?

a. $ 480.

b. $ 288.

c. $1,360.

d. $ 144.

Stayman Associates has sold a good to a buyer and wants to recognize revenue. Which

of the following is an indicator that control of a good has passed from Stayman to the

buyer?

a. Buyer has scheduled delivery.

b. Buyer has a strong credit history, such that bad debts are reasonably estimable.

c. Buyer has not scheduled delivery.

d. Buyer has assumed the risk and rewards of ownership.

Gray Co. estimates it is probable that it will receive a $10,000 gain contingency and pay

a $4,000 loss contingency. After recording the appropriate journal entries to recognize

contingent amounts, Gray Co.’s net assets will:

a. Increase by $10,000.

b. Increase by $6,000.

c. Decrease by $4,000.

d. Not change.

According to International Financial Reporting Standards (IFRS), the level of testing

for goodwill impairment is the:

a. Reporting unit.

b. Subsidiary companies.

c. Cash-generating unit.

d. None of these answer choices are correct.

The rate of interest printed on the face of a note payable is called the:

a. Yield rate.

b. Effective rate.

c. Market rate.

d. Stated rate.

Hogan Company had the following account balances for 2016:

Hogan reported net income of $300,000 for 2016. Assuming no other changes in current

account balances, what is the amount of net cash provided by operating activities for

2016 reported in the statement of cash flows?

a. $291,000.

b. $290,000.

c. $281,000.

d. $301,000.

The shareholders’ ‘equity of HS Corporation includes $300,000 of $1 par common stock

and $600,000 par value of 6% cumulative preferred stock. The board of directors of HS

declared cash dividends of $70,000 in 2016 after paying $30,000 cash dividends in

2015 and $50,000 in 2014.

Required:

What is the amount of dividends common shareholders will receive in 2016?

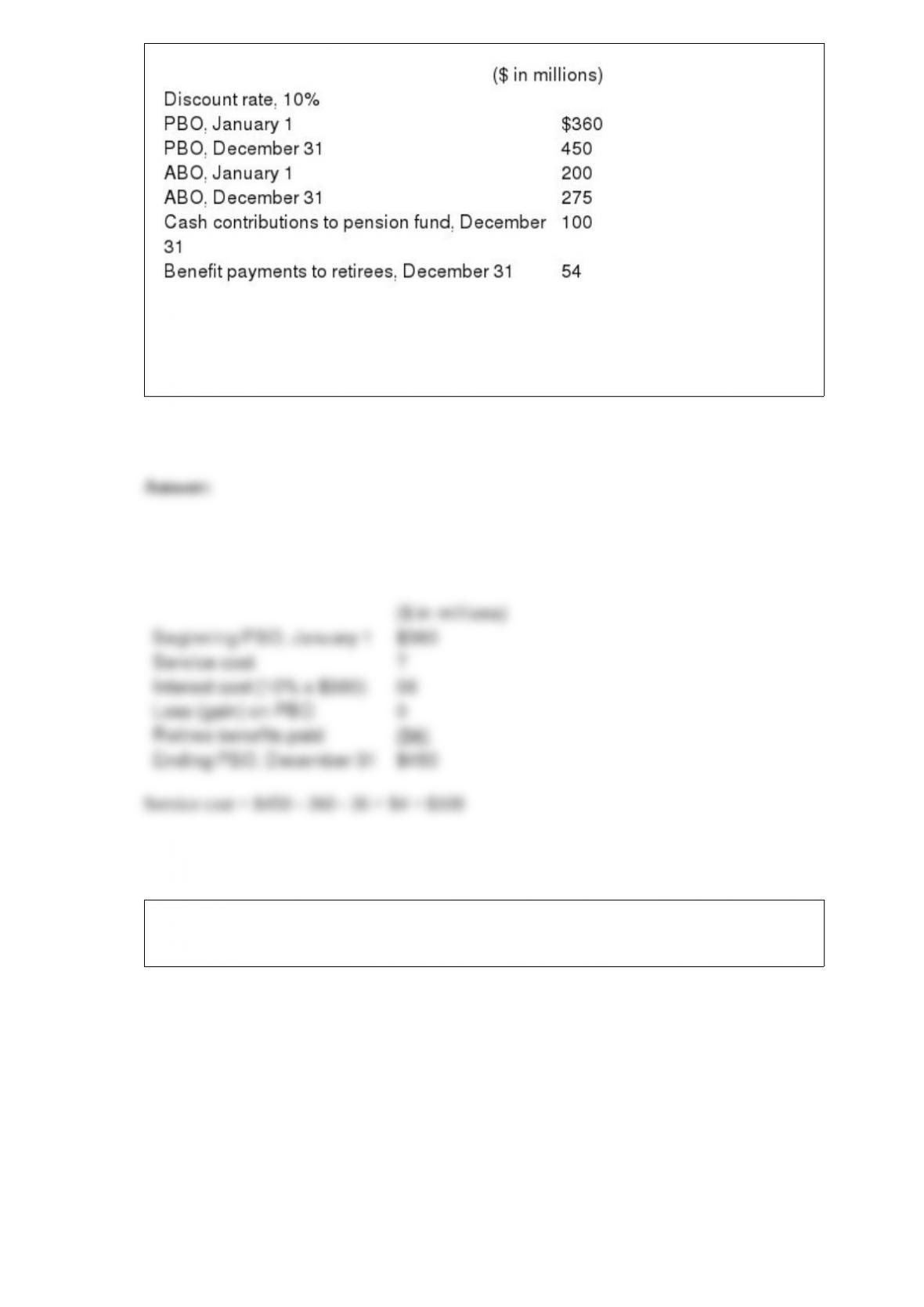

Pension data for Matta Corporation include the following for the current calendar year:

Required:

Assuming no change in actuarial assumptions and estimates, determine the service cost

component of pension expense for the current year.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the number for the most correct term.

What is the objective of disclosures about revenue recognition? Indicate at least two

common types of important revenue recognition disclosures.

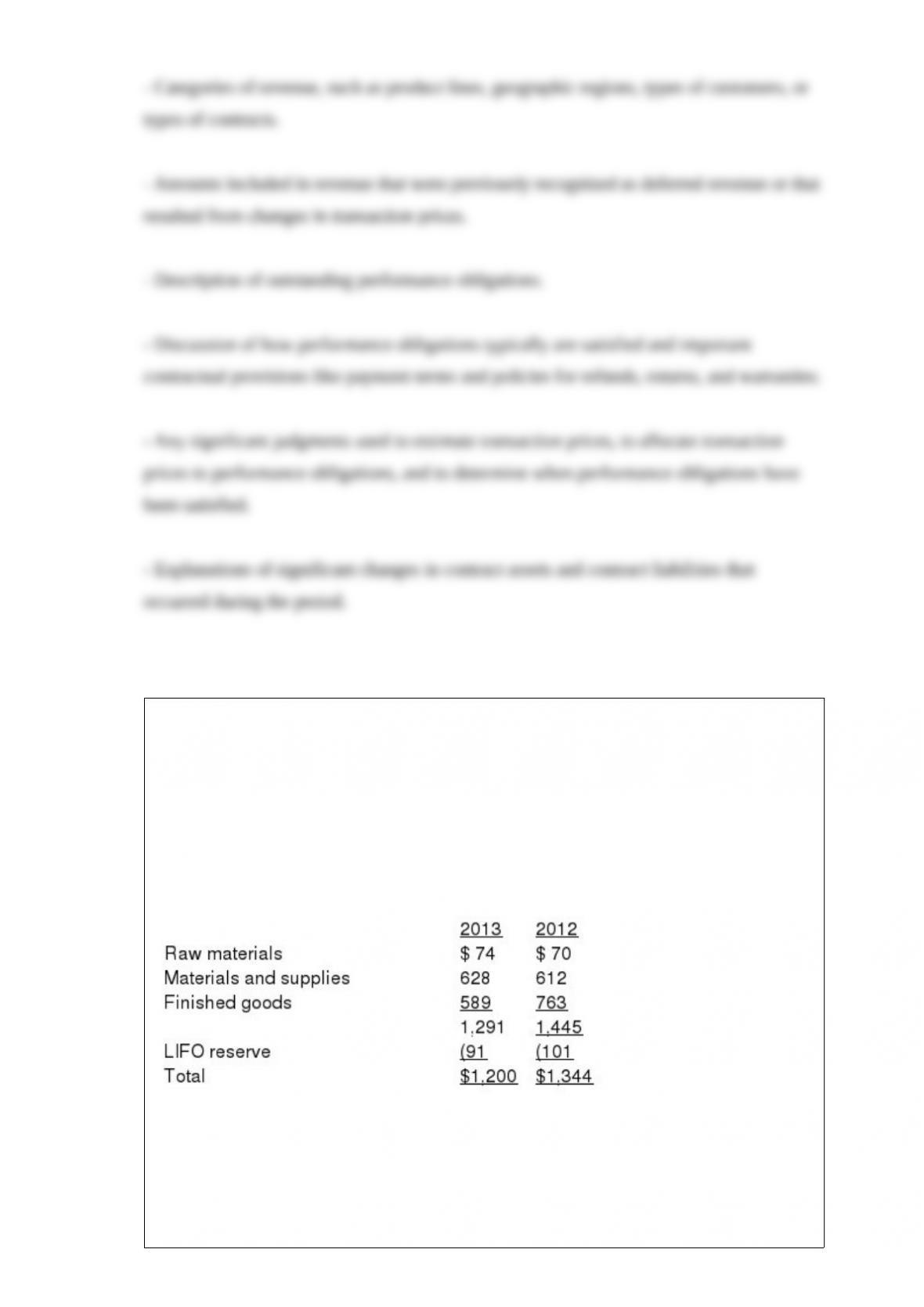

The following information comes from the 2013 Occidental Petroleum Corporation

annual report to shareholders:

NOTE 4 INVENTORIES

Net carrying values of inventories valued under the LIFO method were approximately

$205 million and $185 million at December 31, 2013 and 2012, respectively.

Inventories consisted of the following: ($ in millions)

The LIFO reserve indicates that inventories would have been $91 million and 101

million higher at the end of 2013 and 2012, respectively, if Occidental Petroleum had

used FIFO to value its entire inventory. Required:

If Occidental Petroleum had used FIFO to value its entire inventory how would its 2013

pre-tax income be affected?

Berry Farm produces organic tomatoes and strawberries. In June 2016, it transported

100 boxes of strawberries with a price of $20 per box to the Bay Farmers’ Market.

Berry Farm paid an upfront fee of $100 to present its products at the market for one

week, and the market earns a 25% profit margin on each item sold, but Berry Farm is

responsible for any items that remain unsold at the end of the week.

Required: The market was able to sell 65 boxes of strawberries to customers. How

much

revenue should Berry Farm recognize with respect to this transaction?

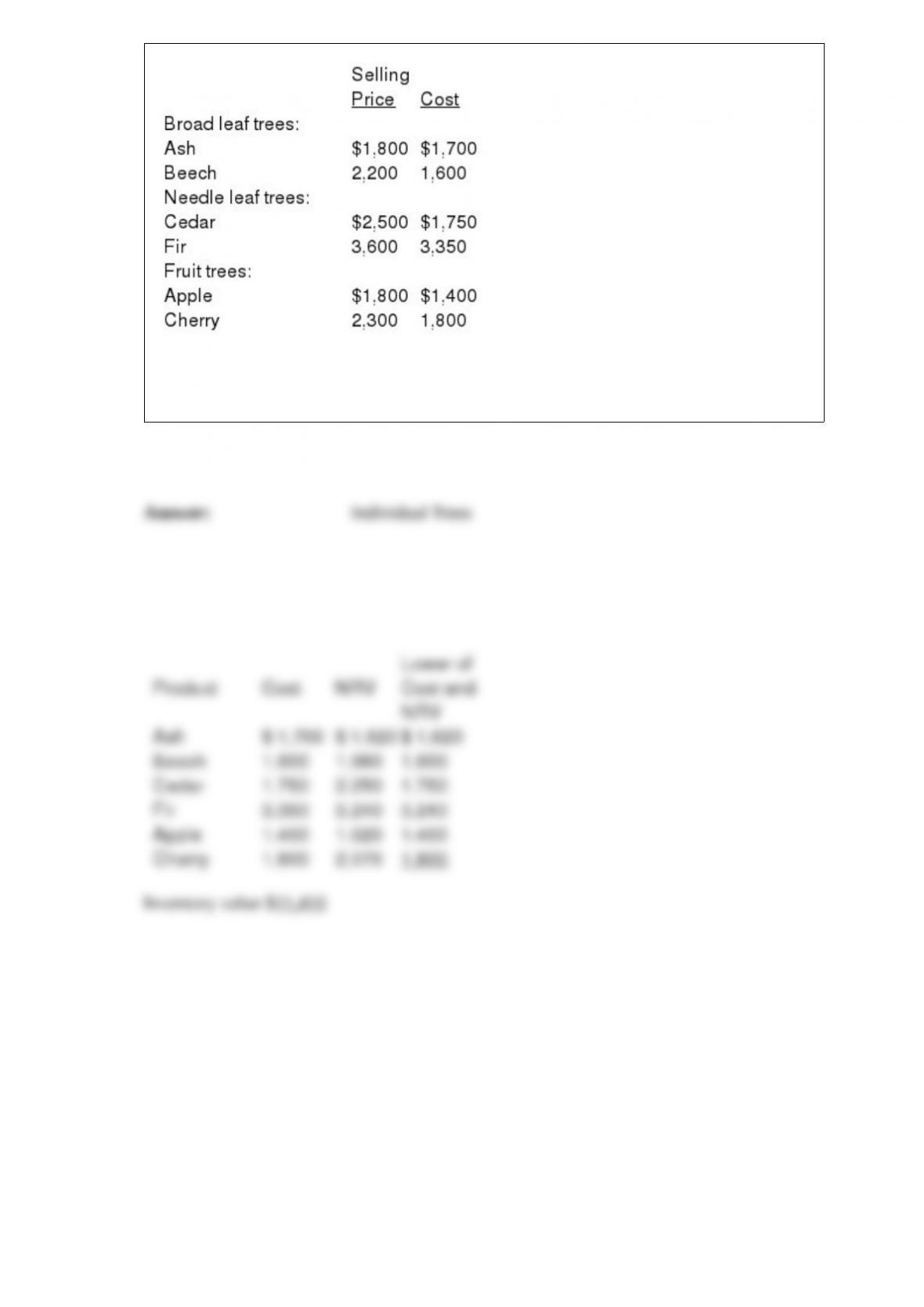

Novelli’s Nursery has developed the following data for lower of cost and net realizable

valuation for its products:

The costs to sell are 10% of selling price. Required: Determine the reported inventory

value assuming the lower of cost and net realizable value rule is applied to individual

trees.