All changes in long-term liabilities are reflected in the financing activities category of

the statement of cash flows.

a. True

b. False

Match the selected items from a classified balance sheet and multiple-step income state

ment to the section in which they would appear on the classified balance sheetor the inc

ome statement.

a. Current Assets (balance sheet)

b. Property, Plant, & Equipment (balance sheet)

c. Current Liabilities (balance sheet)

d. Long-term Liabilities (balance sheet)

e. Stockholders’ Equity (balance sheet)

f. Operating Revenue (income statement)

g. Operating Expenses (income statement)

h. Other Revenue & Expenses (income statement)

i. Income Taxes (income statement)

Service revenues

Use the following codes to indicate how the cash flow effect, if any, of each transaction

or event would be reported on a statement of cash flows if the operating activities

section is prepared using the indirect method.

a. Operating activity-add to net income

b. Operating activity-deduct from net income

c. Inflow from investing activity

d. Outflow from investing activity

e. Inflow from financing activity

f. Outflow from financing activity

g. Noncash investing and financing activity

h. Not reported on statement of cash flows

Purchased store equipment for cash.

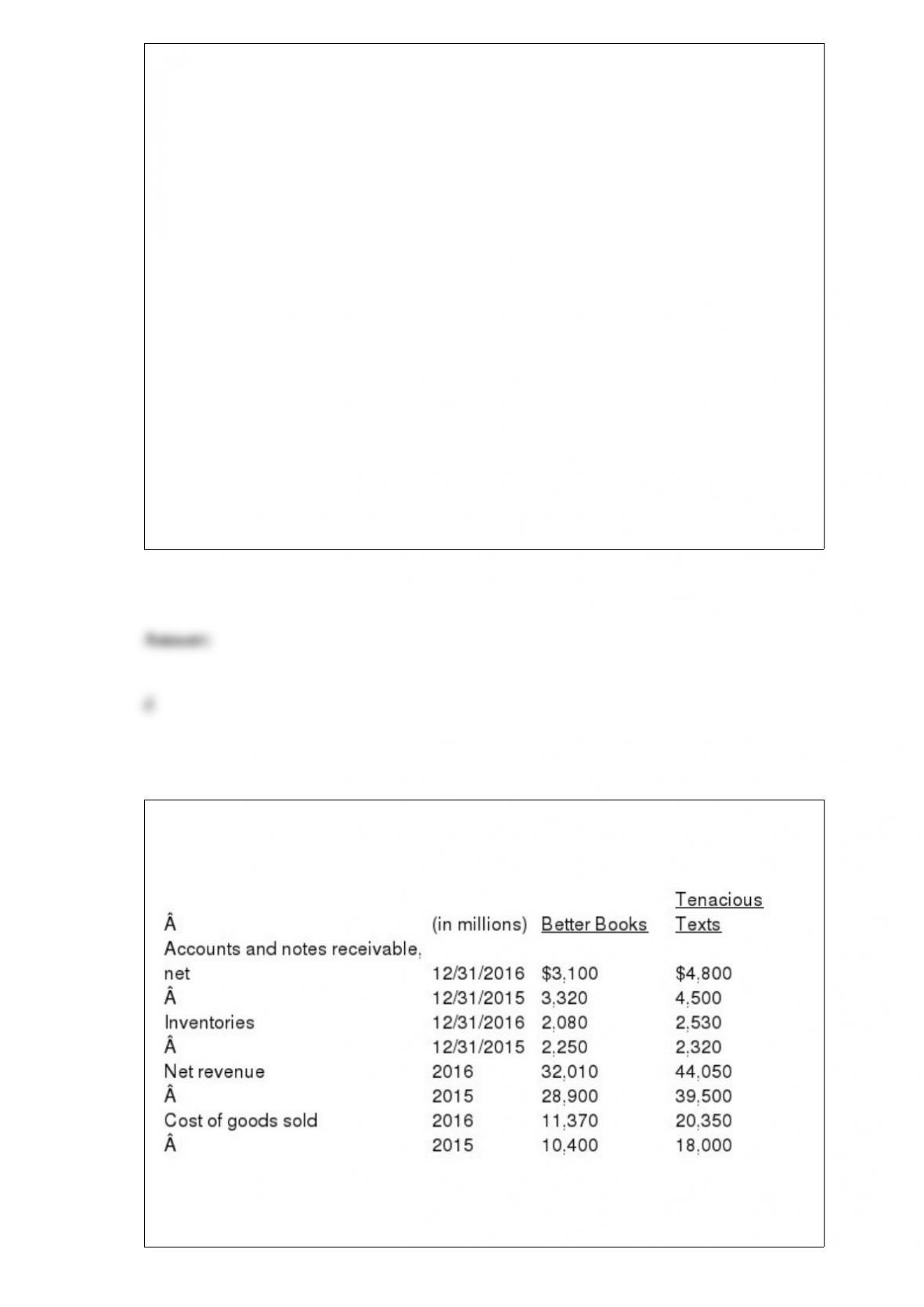

The following information was obtained from the 2016 and 2015 financial statements

Better Books and Tenacious Texts. Assume all sales are on credit for both companies.

REQUIRED: 1> Using the information provided, compute the following for each

company for 2016(rounded to two decimals):

a. Accounts receivable turnover ratio

b. Number of days’ sales in receivables

c. Inventory turnover ratio

d. Number of days’ sales in inventory

e. Cash-to-cash operating cycle

2> Comment briefly on the liquidity of each of these two companies.

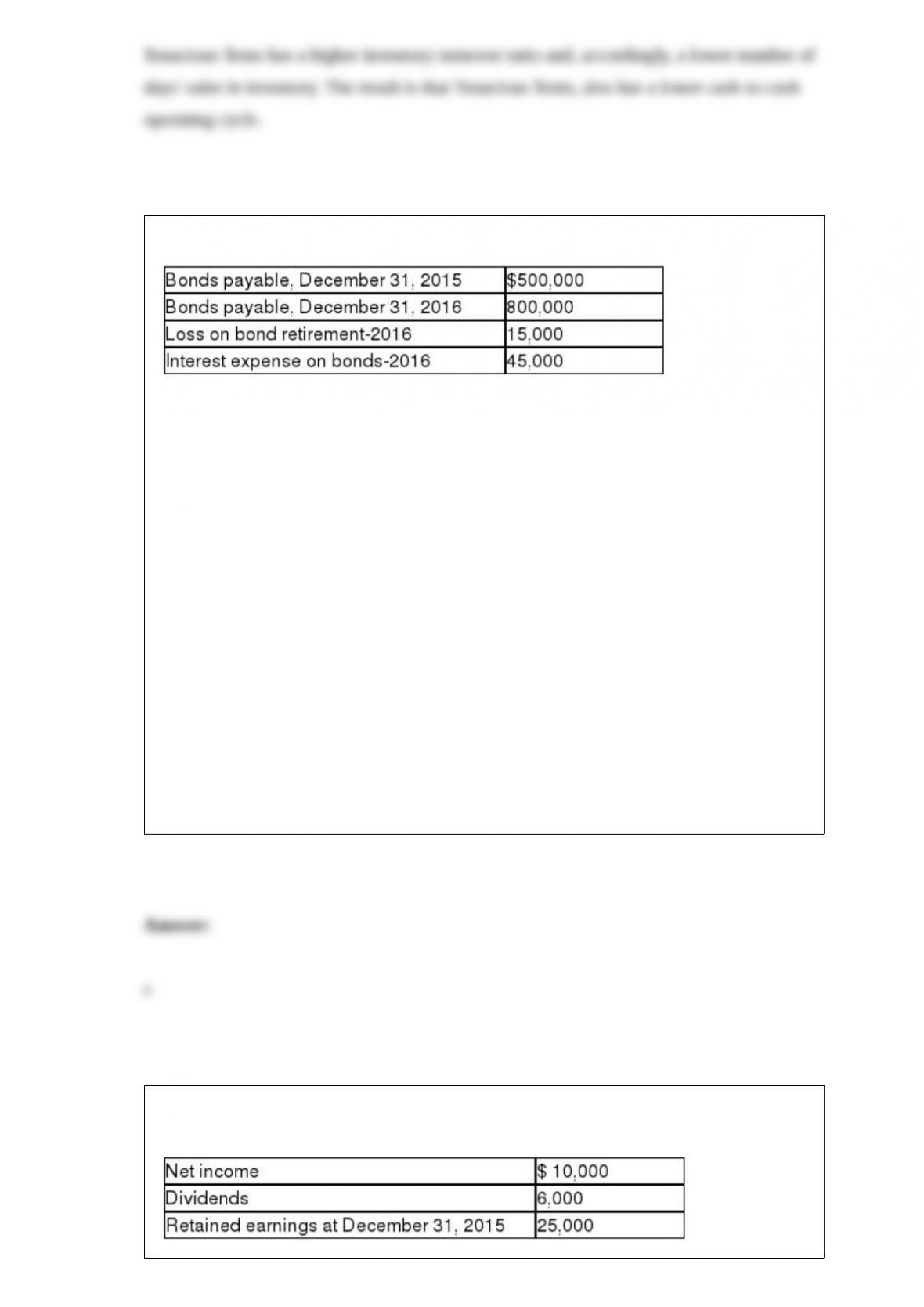

Below is information for Toronto Imports Corp. for 2015 and 2016:

At the end of 2016, Toronto issued bonds at par value for $800,000 cash. The proceeds

from these bonds were used to retire the $500,000 bond issue outstanding at the end of

2015 (before their maturity date). All interest expense was paid in cash during 2016.

The following statements describe how Toronto reported the cash flow effects of the

items described above on its 2016 statement of cash flows. The indirect method is used

to prepare the operating activities section. Which of the following has been reported

incorrectly by Toronto?

a. Proceeds of $800,000 from the issuance of bonds were reported as a cash inflow in

the financing activities section.

b. The loss on bond retirement of $15,000 was added to net income in the operating

activities section.

c. Payments of $560,000 were reported as a cash outflow in the investing activities

section.

d. Interest expense of $45,000 was not reported separately because it is included in net

income in the operating activities section.

Lewis Corporation reported the following information for the year ended December 31,

2015:

What was the economic effect of the payment of Lewis’ dividends?

a. The dividend reduced net income for 2015.

b. The dividend should be equal to net income if the company’s accounting equation is

in balance.

c. The dividends reduce total retained earnings for the year.

d. The dividends must be paid whenever Lewis Corp. reports net income.

Dividends declared and paid reduce a company’s retained earnings balance.

a. True

b. False

Match each of the following terms pertaining to liabilities to their definitions.

a. Current liability

b. Accounts payable

c. Notes payable

d. Discount on notes payable

e. Current maturities of long-term liabilities

f. Accrued liabilities

g. Contingent liability

h. Estimated liability

The portion of a long-term liability that will be paid within one year of the balance

sheet date.

Which one of the following best defines an internal event in terms of accounting?

a. Every type of transaction is an internal event.

b. An event recognized in a set of financial statements.

c. A happening of consequence to an entity.

d. An event occurring entirely within an entity.

The revenue recognition principle involves two factors: paid and incurred.

a. True

b. False

Failure to record dividends paid would result in which of the following?

a. Net income being understated

b. An increase in total liabilities

c. Stockholders’ equity being overstated

d. Total assets being understated

From the following list, identify each item as operating (O), investing (I), financing (F),

or not separately reported on the statement of cash flows (N).

a. Operating-O

b. Investing-I

c. Financing-F

d. Not separately reported-N

Issuance of common stock for cash

From the following list, select the proper section from the statement of cashflows in whi

ch it would beclassified.

a. Operating Activities

b. Investing Activities

c. Financing Activities

Received cash from the sale of a building

Three common categories of long-term assets are: 1) property, plant, and equipment, 2)

investments, and 3) intangibles.

a. True

b. False

The balance sheet is a statement that summarizes revenues and expenses for a period.

a. True

b. False

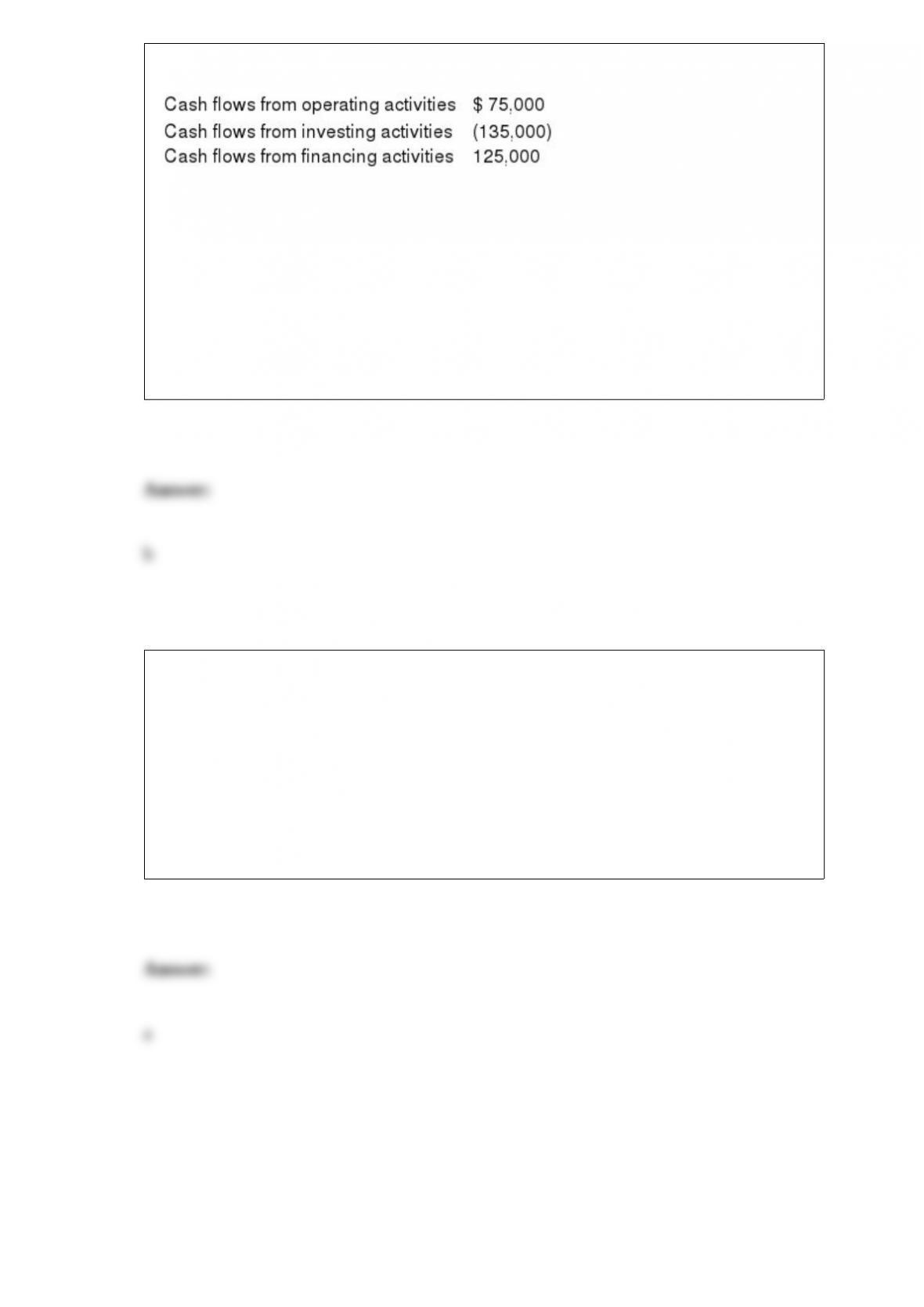

Upon review of Jerry’s Canoe Gallery statement of cash flows, the following was noted:

From this information, the most likely explanation is that Jerry is

a. using cash from operations and selling long-term assets to pay back debt.

b. using cash from operations and borrowing to purchase long-term assets.

c. using its profits to expand growth.

d. using cash from investors to provide for operations.

A decreasing long-term liability account is presented on the statement of cash flows as

a. a decrease in cash in the Financing Activities category.

b. a decrease in cash in the Investing Activities category.

c. an increase in cash in the Operating Activities category.

d. an increase in cash in the Financing Activities category.