Reliable Enterprises sells distressed merchandise on extended credit terms. Collections

on these sales are not reasonably assured, and bad debt losses cannot be reasonably

predicted. It is unlikely that repossessed merchandise is in condition to be re-sold.

Therefore, Reliable uses the cost recovery method. Merchandise costing $30,000 was

sold for $55,000 in 2015. Collections on this sale were $20,000 in 2015, $15,000 in

2016, and $20,000 in 2017.

In 2015, Reliable would recognize gross profit of:

a. $0.

b. $25,000.

c. $ 8,090.

d. $ 8,333.

Pickering Company’s prepaid insurance was $8,000 at December 31, 2015, and $10,000

at December 31, 2016. Pickering reported insurance expense of $15,000 on the 2016

income statement. What amount would be reported in the statement of cash flows as

insurance paid using the direct method?

a. $13,000.

b. $17,000.

c. $15,000.

d. $23,000.

On January 1, 2016, Gibson Corporation entered into a four-year operating lease. The

payments were as follows: $20,000 for 2016, $18,000 for 2017, $16,000 for 2018, and

$14,000 for 2019. What is the correct amount of lease expense for 2017?

a. $20,500.

b. $19,000.

c. $17,000.

d. $18,000.

An asset should be written down if there has been an impairment of value that is:

a. Relevant and objectively determined.

b. Material and market driven.

c. Unplanned and sudden.

d. Significant.

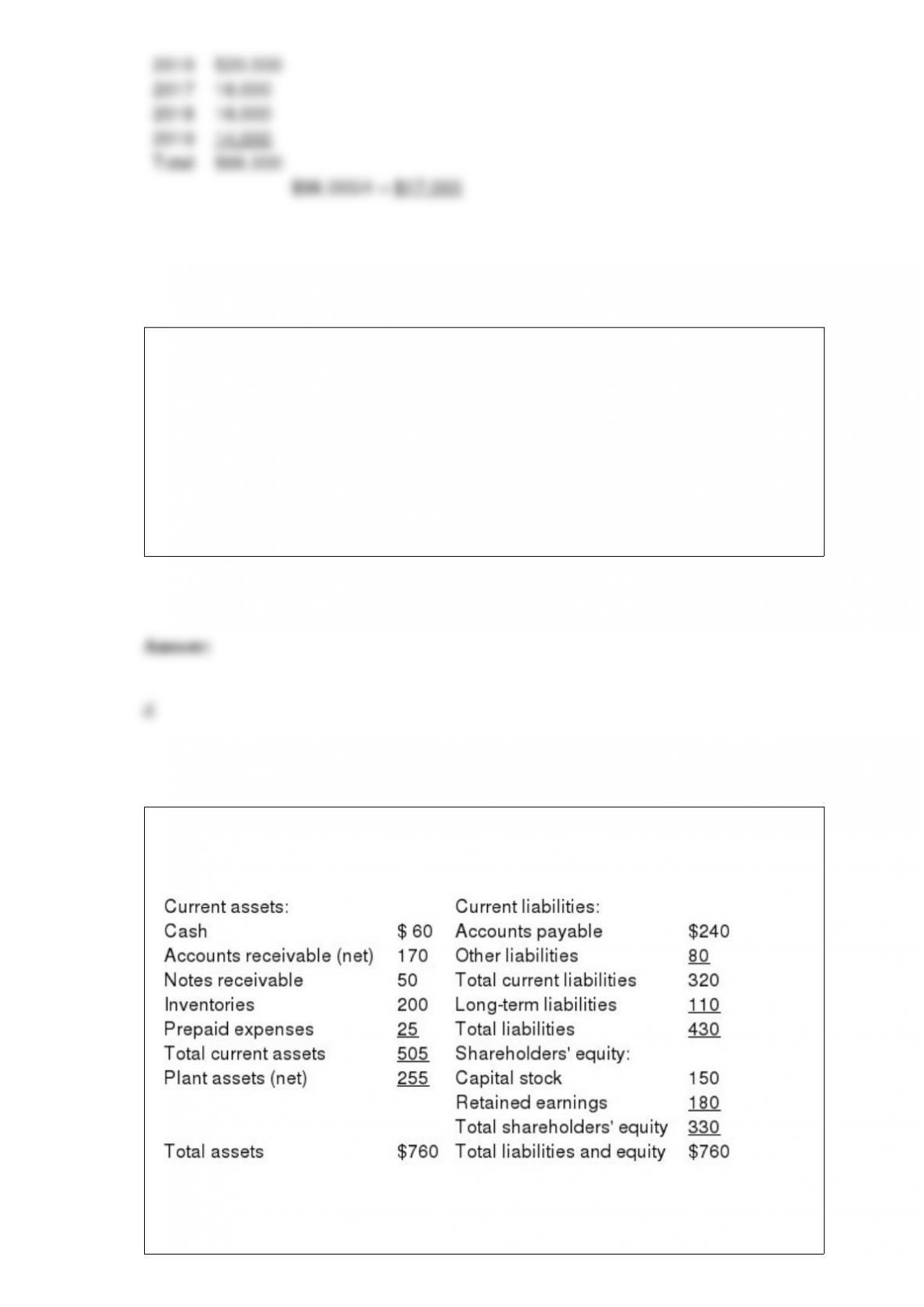

The following partial balance sheet ($ in thousands) for Paisano Seafood Inc. is shown

below.

Working capital is:

a. $505.

b. $265.

c. $185.

d. $75.

In 2016, management discovered that Dual Production had debited expense for the full

cost of an asset purchased on January 1, 2013, at a cost of $36 million with no expected

residual value. Its useful life was 5 years. Dual uses straight-line depreciation. The

correcting entry, assuming the error was discovered in 2016 before preparation of the

adjusting and closing entries, includes:

a. A debit to accumulated depreciation of $14.4 million

b. A credit to accumulated depreciation of $21.6 million.

c. A credit to an asset of $36 million.

d. A debit to retained earnings of $14.4 million.

The rate of interest that actually is incurred on a note payable is called the:

a. Face rate.

b. Contract rate.

c. Effective rate.

d. Stated rate.

Disclosure notes to a company’s financial statements:

a. Are relatively unimportant facts that don’t belong in the basic financial statements.

b. Document the source of financial statement facts, like literary footnotes.

c. Are an integral part of a company’s financial statements.

d. Are irrelevant facts that are immaterial in amount.

Accounting changes occur for which of the following reasons?

a. Management is being fair and consistent in financial reporting.

b. Management compensation is affected.

c. Debt agreements are impacted.

d. All of these answer choices are correct.

Pronouncements issued by the Committee on Accounting Procedures:

a. Dealt with specific accounting and reporting problems.

b. Were based on exposure drafts and public comment letters.

c. Originated from congressional studies and SEC directives.

d. Were the outcome of research studies and a theoretical framework.

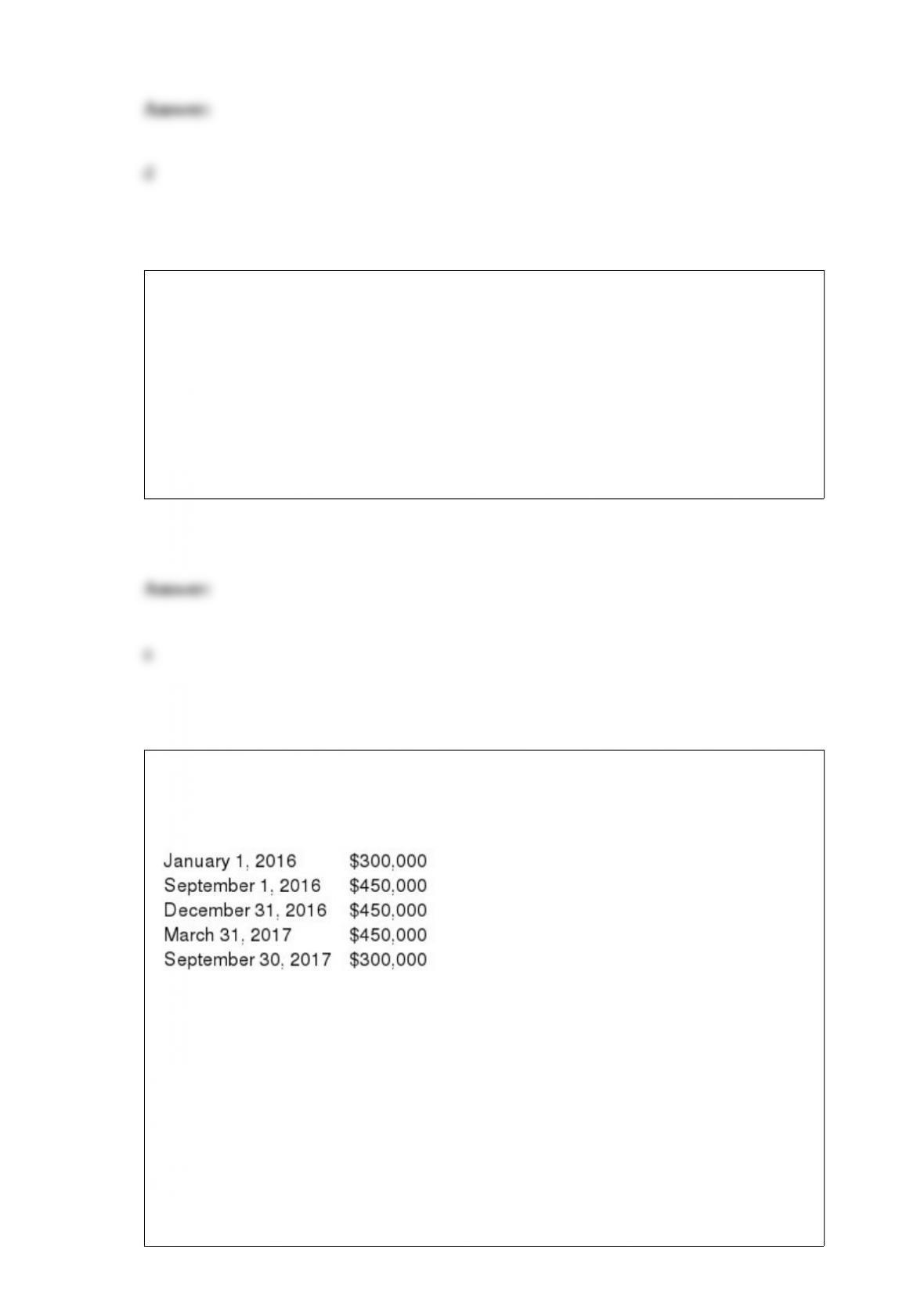

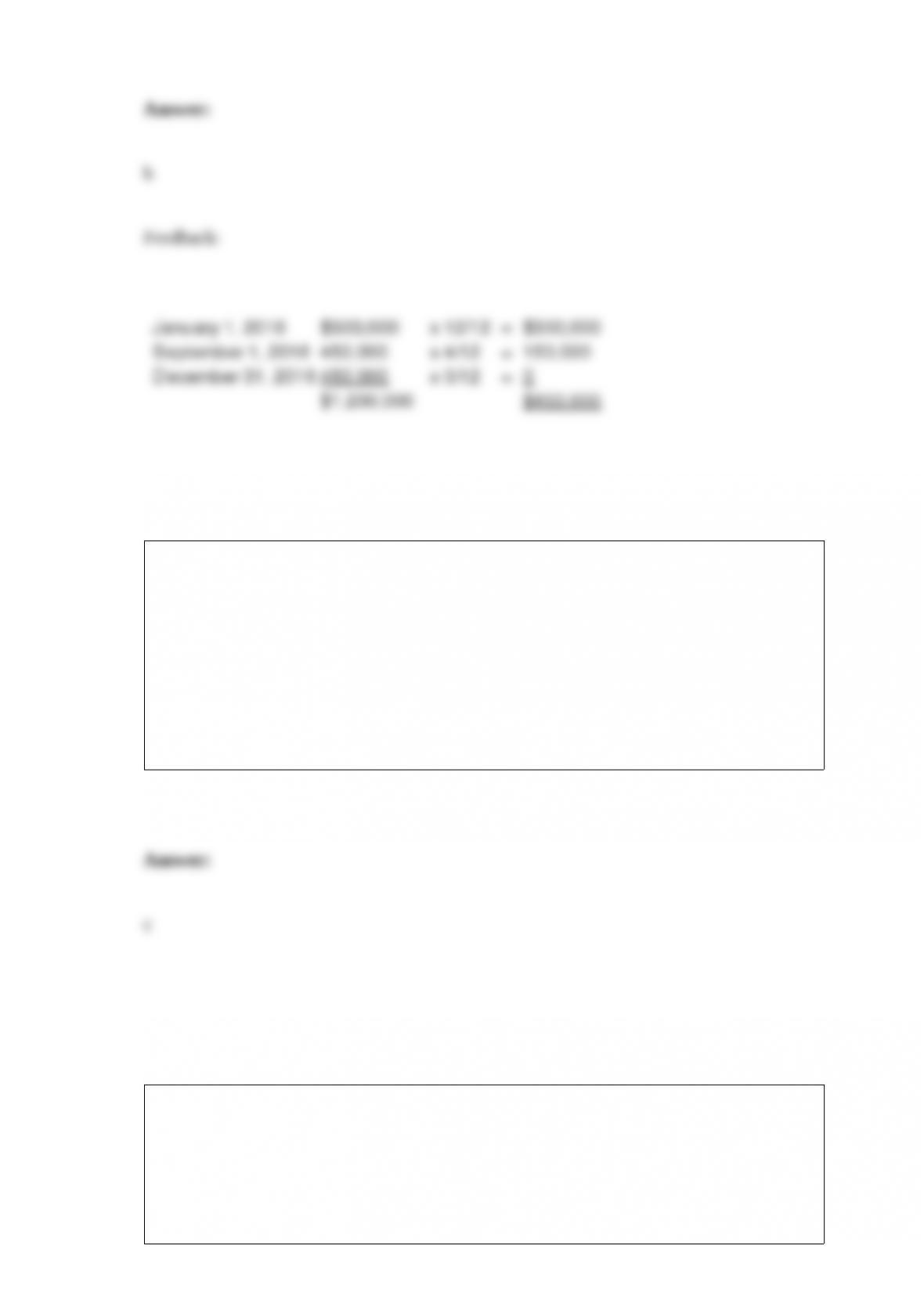

On January 1, 2016, Dreamworld Co. began construction of a new warehouse. The

building was finished and ready for use on September 30, 2017. Expenditures on the

project were as follows:

Dreamworld had $5,000,000 in 12% bonds outstanding through both years.

Dreamworld’s average accumulated expenditures for 2016 was:

a. $300,000.

b. $450,000.

c. $525,000.

d. $600,000.

Accumulated other comprehensive income is reported:

a. In the balance sheet as an asset.

b. In the balance sheet as a liability.

c. In the balance sheet as a component of shareholders’ ‘equity.

d. In the statement of comprehensive income.

Executive stock options should be reported as compensation expense:

a. Using the intrinsic value method.

b. Using the fair value method.

c. Using either the fair value method or the intrinsic value method.

d. Only on rare occasions.

Indicate the nature of each of the situations described below using the following

three-letter code.

CODE DESCRIPTION

CPR: Change in principle reported retrospectively

CPP: Change in principle reported prospectively

CES: Change in estimate

CRE: Change in reporting entity

PPA: Prior period adjustment required

____ Technological advance that renders worthless a patent with an unamortized cost of

$45,000.

____ Change from LIFO inventory costing to average inventory costing.

____ Including in the consolidated financial statements a subsidiary acquired several

years

earlier that was appropriately not included in previous years.

____ Change from FIFO inventory method to LIFO.

____ Pension plan assets for a defined benefit pension plan achieving a rate of return in

excess

of the amount anticipated.

____ Change from the pay-as-you-go method to estimating warranty expense in the

period the related product is sold.

____ Change from declining balance depreciation to straight-line.

____ Change from determining lower of cost or market for inventories by the individual

item

approach to the aggregate approach.

____ Settling a lawsuit for less than the amount accrued previously as a loss

contingency.

____ Change in the estimated useful life of office equipment.

Cartel Products Inc. offers a restricted stock award plan to its vice presidents. On

January 1, 2016, the corporation granted 12 million of its $1 par common shares,

subject to forfeiture if employment is terminated within two years. The common shares

have a market value of $6 per share on the date the award is granted.

Required:

(1) Assume that no shares are forfeited. Determine the total compensation cost

pertaining to the restricted shares.

(2) Prepare the appropriate journal entries related to the restricted stock through

December 31, 2017.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct number code for the term.

Bernard Corporation has an unfunded postretirement health care benefit plan. Life

insurance and medical care benefits are provided to employees who render 12 years of

service and attain age 55 while in service to the company. At the end of 2016, Teri Clark

is 35. She was hired by Bernard five years ago at age 30 and is expected to retire at the

age of 62. The expected postretirement benefit obligation for Teri is $50,000 at the end

of 2016 and $60,000 at the end of 2017.

Required:

Calculate the accumulated postretirement benefit obligation at the end of 2016 and

2017 and the service cost for 2016 and 2017 pertaining to Teri.

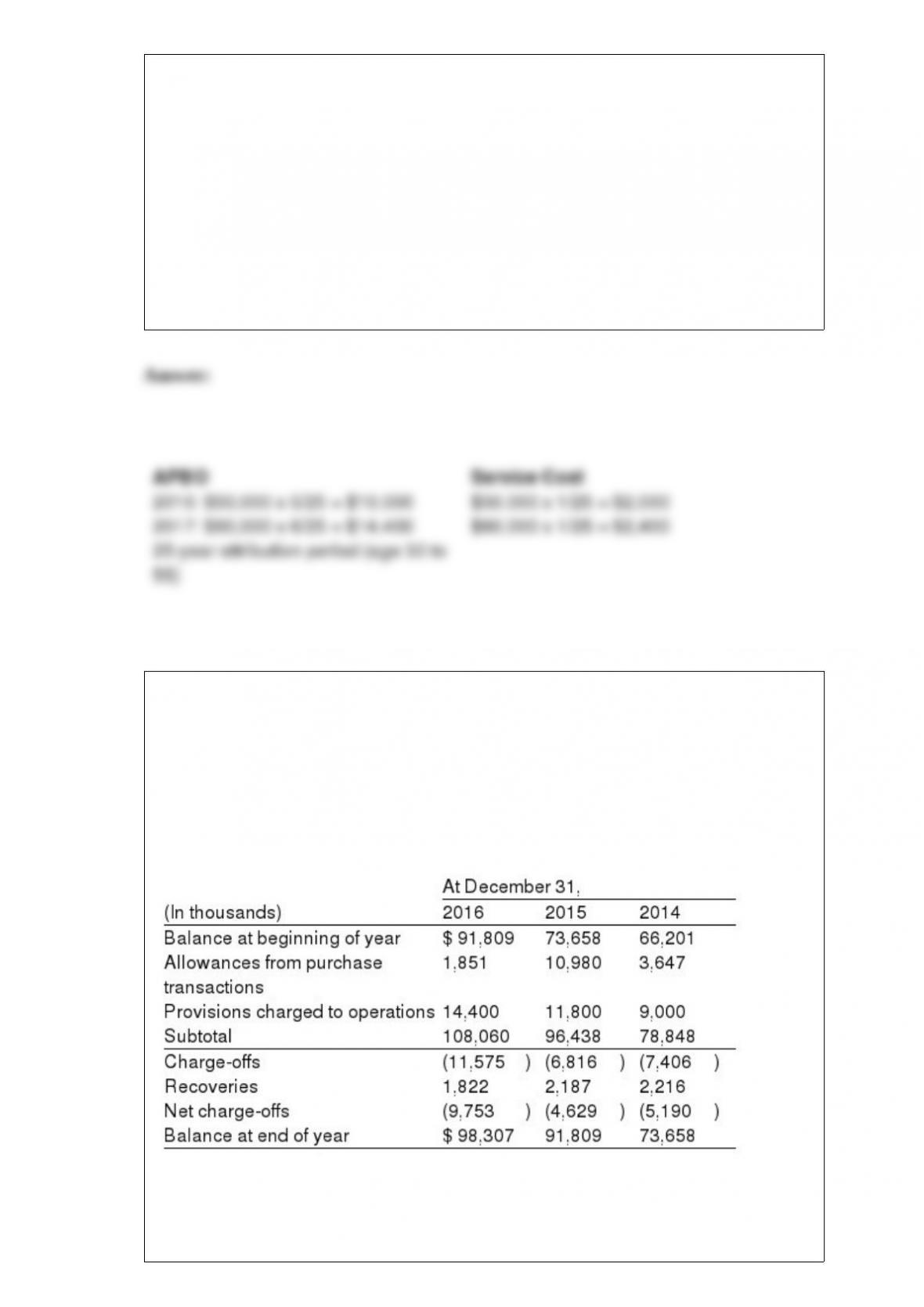

The following note disclosure is taken from the 2016 annual report to shareholders of

Winchester International Corporation. NOTE 5: ALLOWANCE FOR LOAN LOSSES

The allowance for loan loss is maintained at a level to absorb probable losses inherent

in the loan portfolio. This allowance is increased by provisions charged to operating

expense and by recoveries on loans previously charged off, and reduced by charge-offs

on loans. The following is a summary of the changes in the allowances for loan losses

for three years:

Winchester also reported (in thousands) in its comparative balance sheet that it held

Loans receivable, net, of $6,869,911 and $6,819,209 at December 31, 2016, and

December 31, 2015, respectively. Using a T-account for the Allowance for Loan Losses,

identify the changes in the account during 2016.

On February 1, 2016, Fox Corporation issued 9% bonds dated February 1, 2016, with a

face amount of $200,000. The bonds sold for $182,841 and mature in 20 years. The

effective interest rate for these bonds was 10%. Interest is paid semiannually on July 31

and January 31. Fox’s fiscal year is the calendar year. Fox uses the straight-line method

of amortization.

Required:

1> Prepare the journal entry to record the bond issuance on February 1, 2016.

2> Prepare the entry to record interest on July 31, 2016.

3> Prepare the necessary journal entry on December 31, 2016.

4> Prepare the necessary journal entry on January 31, 2017.

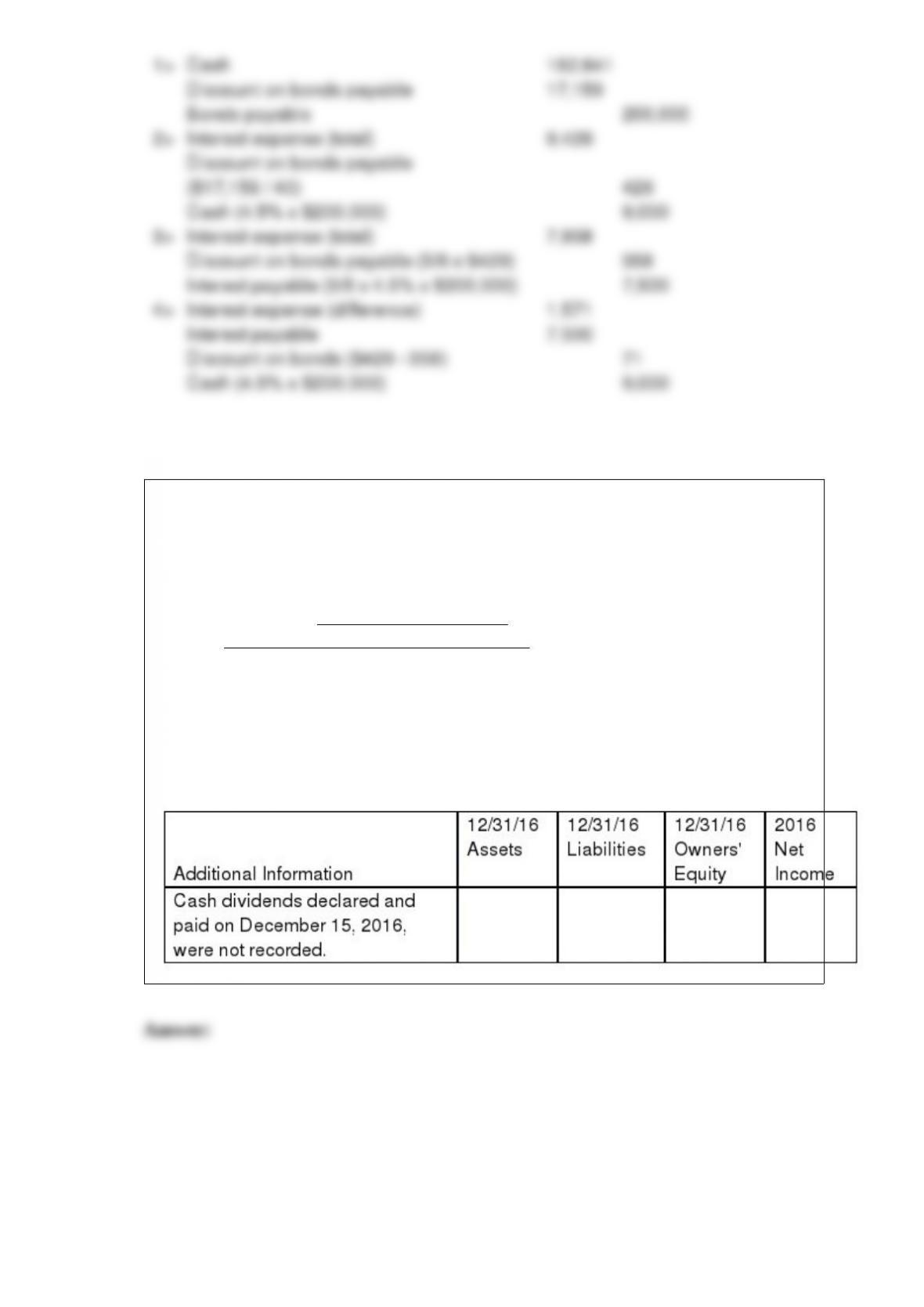

Use the following to answer questions 119-124: You are reviewing O’Brian Co.’s

adjusted trial balance for the year ended 12/31/16. You notice several omissions and

incorrect items during your review, some of which are noted below. For each one, you

are to determine what effect, if any, these items would have on the stated components of

O’Brian Co.’s 2016 Income Statement and 12/31/16 Balance Sheet if they are not

corrected or updated. Assume no income taxes. Use the following code for your

answers. You need not include any dollar amounts.

N = No Effect

O = Overstated

U = Understated