As a company uses supplies, an adjustment should be made to decrease an asset account

and increase an expense account.

Answer:

Which of the following statements regarding dividends in arrears isTRUE?

A. Dividends in arrears do not appear on the balance sheet or require a journal entry.

B. Dividends in arrears are not disclosed to stockholders.

C. Dividends in arrears applies to common stock.

D. Dividends in arrears are legal liabilities.

Answer:

A highly effective internal control should not be implemented if the cost is greater than

the benefit.

Answer:

Which of the following isTRUE?

A. Companies can choose to end their fiscal year on any date they feel is most relevant.

B. Companies must end their fiscal year on March 31, June 30, September 30, or

December 31.

C. Companies can select any date except a holiday to end their fiscal year.

D. Companies must end their fiscal year on December 31.

Answer:

An understatement of beginning inventory causes net income to be understated.

Answer:

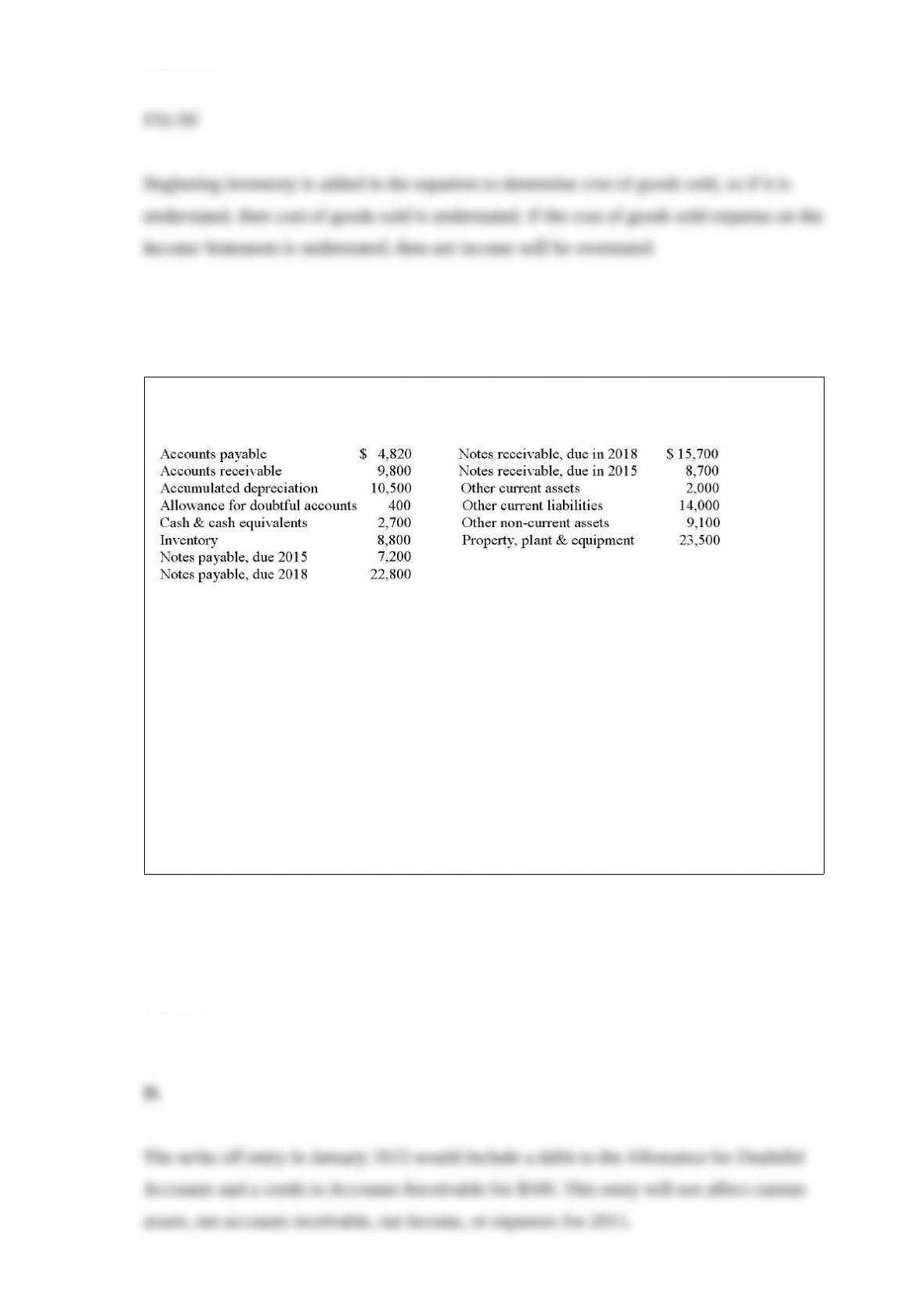

A company reported the following accounts and amounts in its December 31, 2014,

year-end financial statements:

Use the information above to answer the following question. In January 2015, the

company writes off a $500 account which it determines is uncollectible. If the company

uses the allowance method, which of the following isTRUE?

A. The write-off will decrease the current assets by $500.

B. The write-off will decrease net income for 2015 by $100.

C. The write-off will decrease net accounts receivable by $100.

D. The write-off will not increase the expenses for 2015.

Answer:

Which of the following isTRUE regarding a company’s fiscal year?

A. All companies have a December 31 year end.

B. It usually corresponds to a company’s slow period.

C. It always corresponds to the calendar year.

D. The Financial Accounting Standards Board assigns a year end to each company.

Answer:

Trend data can be measured in dollar amounts or percentages.

Answer:

In a perpetual inventory system, only one journal entry is required to record the sale of

merchandise.

Answer:

When companies switch from GAAP to IFRS, their financial ratios would not be

expected to change significantly.

Answer:

Which of the following is aTRUE statement?

A. Sales discounts is a contra-asset account.

B. Sales returns & allowances is a contra-revenue account.

C. Sales returns & allowances is a credit balance account.

D. Sales discounts is a contra-account to inventory.

Answer:

Which of the following is not aTRUE statement?

A. When making an adjustment to recognize supplies used in a period, total assets will

not change.

B. Accrued wages are wages owed but not yet paid to employees and will need to be

recorded with an adjusting entry that will increase expenses.

C. Deferrals are created by reflecting a transaction so that it delays or defers the

recognition of an expense or a revenue.

D. Depreciation is an example of a deferred expense.

Answer:

Credit card companies charge a fee to the seller that accepts the credit cards. This fee is

recorded by the seller as a non-operating expense on its income statement.

Answer:

Which of the following statements regarding the lower of cost or market rule is

notTRUE?

A. The lower of cost or market rule sometimes causes the book value of inventory to be

written down below cost, but will never cause the book value of inventory to be

increased above cost.

B. The amount of inventory write-down is an expense which most companies report as

cost of goods sold.

C. Lower of cost or market is an inventory cost method used to determine cost of goods

sold and ending inventory.

D. The lower of cost or market rule is based on the conservatism concept.

Answer:

Which of the following is aTRUE statement?

A. The SEC approves the rules used by the auditors in determining whether a public

company’s financial statements are in conformity with GAAP.

B. The PCAOB and the SEC were both created by the FASB.

C. The SEC was created by the PCAOB.

D. The PCAOB approves the rules used by auditors in determining whether a public

company’s financial statements are in conformity with GAAP.

Answer:

This month, a company recorded sales revenue of $50,000 from sales of goods to

customers who agreed to pay later. Next month, the company received payment from

customers of $45,000. Choose theTRUE statement.

A. Revenue for this month is $45,000.

B. Accounts receivable at the end of next month is $5,000.

C. Accounts Payable at the end of this month is $5,000.

D. Revenue for next month will be $45,000.

Answer:

If average net fixed assets decrease, then the fixed asset turnover ratio will increase,

assuming nothing else changes.

Answer:

Building a new warehouse is an operating activity.

Answer:

Which of the following is notTRUE about accrual basis accounting?

A. The revenue principle is applied.

B. The Expense Recognition (Matching) principle is applied.

C. It is required for external accounting reports.

D. It requires the timing of cash receipts be in the same period as revenues are

recognized.

Answer:

The fraud triangle identifies incentive, opportunity, and benchmarks as the requirements

for a fraud to occur.

Answer:

When an asset is sold and its book value exceeds its selling price, net income will

increase.

Answer:

A company receives $102,000 when it issues a bond with a face value of $100,000 and

a stated interest rate of 7%. Which of the following statements isTRUE?

A. The annual interest expense is $7,000.

B. The market interest rate is 7%.

C. A contra account to bonds payable is not needed.

D. The carrying value of the bonds will be $100,000 at maturity.

Answer:

Which of the following statements regarding timing issues associated with the closing

entries isTRUE?

A. Closing entries are recorded at the end of each reporting period which could be

monthly, quarterly or annually.

B. After closing entries are posted, the balances of the income statement accounts will

be zero.

C. Closing entries are made to zero out the balances of the permanent accounts on the

balance sheet.

D. After closing entries are posted, the only temporary account with a balance is the

Dividends Declared account.

Answer:

Extraordinary repairs, replacements, and additions are added to the appropriate asset

accounts rather than being recorded as expenses.

Answer:

In each accounting period, a manager can select the inventory costing method that

yields the highest net income.

Answer:

Which of the following statements isTRUE?

A. If revenues are less than expenses, the company has a net loss and retained earnings

decreases.

B. If revenues are greater than expenses, the company has net income and contributed

capital increases.

C. If revenues are less than expenses, the company has a net loss and contributed capital

increases to balance off the loss.

D. If revenues are greater than expenses, the company has net income and retained

earnings decreases.

Answer:

Bonds that are not backed by collateral are called debenture bonds.

Answer:

If a company produces the same number of units per period over an asset’s useful life,

straight-line depreciation expense per period will be the same as the depreciation

expense recorded using the units-of-production method.

Answer:

Stockholders are creditors of a company.

Answer:

The trial balance is a financial statement that reports the assets, liabilities, and equity of

a business at a point in time.

Answer:

Company X issues $40 million in new stock for cash. This does not affect stockholders’

equity because as new shares are sold the value of existing shares falls.

Answer:

When the amount of annual depreciation is revised because of a change in the estimated

useful life of an asset, prior years’ financial statements should be restated.

Answer:

Which of the following statements about dividends is notTRUE?

A. Dividends Declared has a debit balance.

B. Dividends reduce retained earnings.

C. Dividends Declared is an expense.

D. Dividends Declared is a balance sheet account.

Answer:

Journal entries show the effects of transactions on the elements of the accounting

equation, as well as the account balances.

Answer:

The primary difference between ordinary repairs and extraordinary repairs is:

A. ordinary repairs cost less.

B. ordinary repairs are expenditures for routine maintenance and upkeep, whereas

extraordinary repairs increase an assets economic usefulness in the future through

increased efficiency, capacity, or longer life.

C. extraordinary repairs only maintain the asset for a short time, whereas ordinary

repairs increase the usefulness of assets beyond their original condition.

D. extraordinary repairs are expenditures, not expenses.

Answer:

Which of the following accounts could have a non-zero balance on a post-closing trial

balance?

A. Dividends Declared

B. Premium on Bonds Payable

C. Income Tax Expense

D. Interest Expense

Answer:

Your company purchases $50,000 of inventory from a wholesaler who allows you 45

days to pay. In addition, the wholesaler offers a 3% discount if payment is made within

12 days. These payment terms would be expressed as:

A. .03/12, n/45.

B. n/45, 3/12.

C. n/45, .03/12.

D. 3/12, n/45.

Answer:

On March 20, 2014, E. Flynn Company acquired the following net assets from

M.Curtiz Company for $360,000.

How much Goodwill should E. Flynn Company record for this acquisition?

A. $66,000.

B. $63,000.

C. $44,000.

D. $0.

Answer:

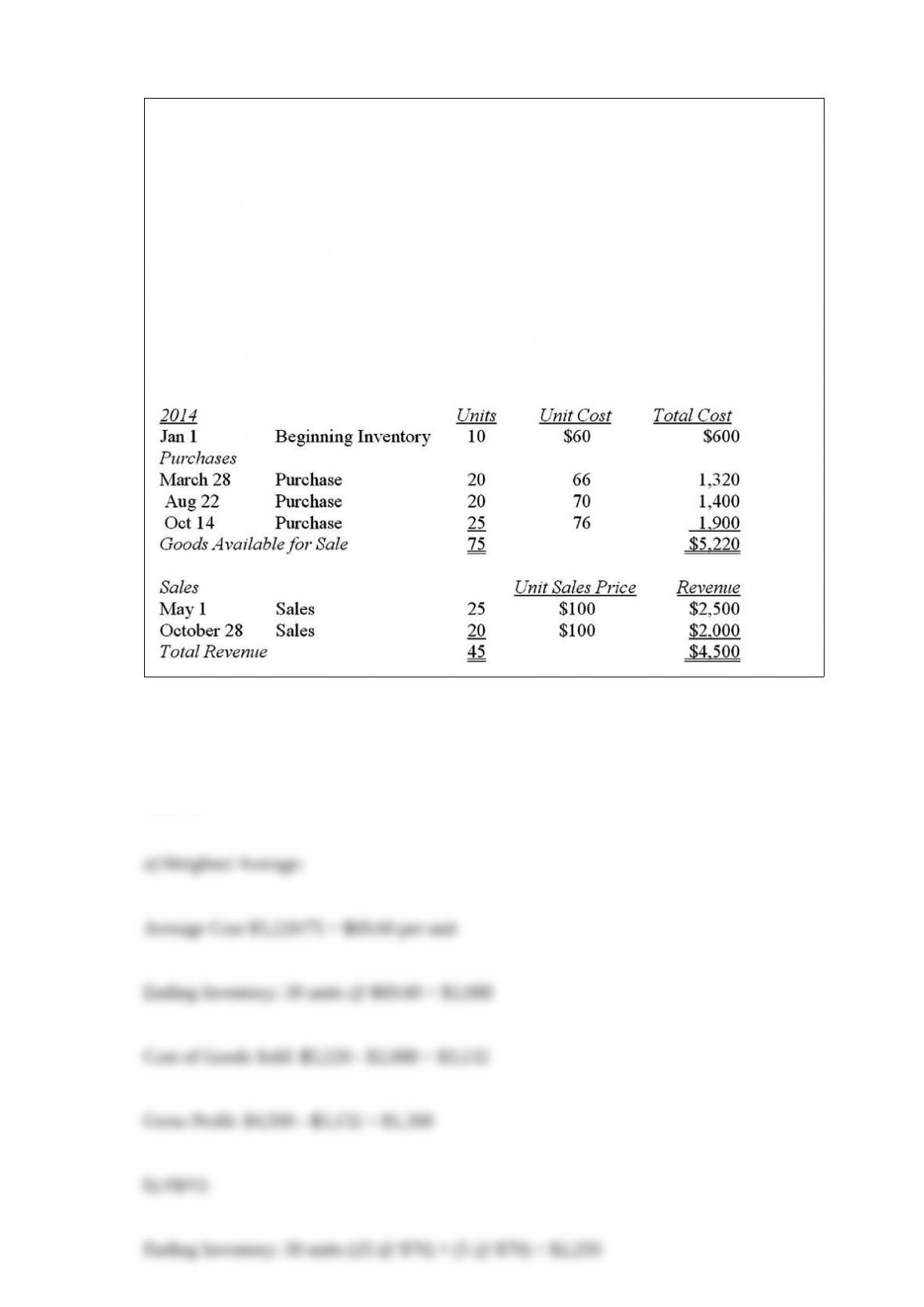

Given the following information for Maynor Company in 2014, calculate the company’s

ending inventory, cost of goods sold, and gross profit, using the following inventory

costing methods, assuming the company uses a periodic inventory system:

a) Weighted Average.

b) FIFO.

c) LIFO.

d) Specific Identification. (The ending inventory consisted of 15 @ $66; 10 @ $70; and

5 @ $76.)

Answer:

A debt to assets ratio of .50 indicates that the company has:

A. more liabilities than stockholders’ equity.

B. equal amounts of liabilities and stockholders’ equity.

C. more stockholders’ equity than liabilities.

D. no liabilities.

Answer:

BetterBuy purchases computers from companies like Hewlett Packard and IBM and

sells them to consumers. BetterBuy is a:

A. merchandising company at the retail level.

B. service company.

C. merchandising company at the wholesale level.

D. manufacturer.

Answer:

A company buys footwear and clothing from manufacturers, which it resells to discount

stores in a large urban area. This company is an example of a:

A. wholesale merchandising company.

B. service company.

C. retail merchandising company.

D. secondary service company.

Answer:

Your company orders and broadcasts a 30 second ad during the Super Bowl for $1.2

million. It is legally obligated to pay for the ad but has not yet done so.

A. This is an internal event and it does NOT affect the balance sheet.

B. This is an external event and it does NOT affect the balance sheet.

C. This is an internal event that affects the balance sheet.

D. This is an external event that affects the balance sheet.

Answer:

The Dubious Company operates in an industry where all sales are made on account.

Historically, Dubious has experienced a steady 1.0% of credit sales being uncollectible.

Presented below is the company’s forecast of sales and expenses over the next three

years.

Using this information:

a. Calculate bad debt expense and net income for each of the three years, assuming

uncollectible accounts are estimated as 1.0% of sales.

b. Describe the trend in net income changes from Year 1 to Year 2 and from Year 2 to

Year 3.

c. Suppose the company changes its estimate of uncollectible credit sales to 1.0% in

Year 1, 2.0% in Year 2 and 1.5% in Year 3. Calculate the bad debt expense and net

income for each of the three years under this alternative scenario.

d. Describe the trend in net income changes determined in requirement c from Year 1 to

Year 2 and Year 2 to Year 3.

e. Explain some of the factors that might cause the estimate of uncollectible accounts to

vary from year to year as in part c above.

Answer:

The retained earnings balance was $22,900 on January 1. Net income for the year was

$18,100. If retained earnings had a credit balance of $23,800 after closing entries were

made for the year, and if additional stock of $5,200 was issued during the year, what

was the amount of dividends declared during the year?

A. $17,200

B. $23,700

C. $23,300

D. $13,000

Answer:

In a T-account, debits appear in what manner?

A. They are on the left under assets but on the right under liabilities and stockholders’

equity.

B. They are always listed on the right.

C. They are always listed on the left.

D. They are on the right under assets but on the left under liabilities and stockholders’

equity.

Answer:

The fixed asset turnover ratio measures the:

A. useful life of long-lived assets.

B. the average difference between book value and disposal value of fixed assets.

C. useful life of intangible assets.

D. efficiency with which the investment in fixed assets produces revenue.

Answer:

The basic business model shows:

A. financing is used to generate revenue that is invested in assets that produce net

income.

B. financing is used to invest in assets that generate revenues that produce net income.

C. revenue is produced from net income that is invested in assets to repay financing.

D. assets are used to generate financing that produces revenue and net income.

Answer:

Flynn Company’s monthly bank statement showed the ending balance of cash of

$18,500. The bank reconciliation for the period showed an adjustment for a deposit in

transit of $1,500, outstanding checks of $2,000, a NSF check of $700, bank service

charges of $30 and the EFT from a customer in payment of the customer’s account of

$1,500.

Use the information above to answer the following question. What was the unadjusted

balance on the company’s books?

A. $18,000

B. $17,230

C. $19,000

D. $20,270

Answer:

The inventory costing method that smoothes out changes in costs is

A. FIFO.

B. LIFO.

C. Weighted average.

D. Specific identification.

Answer:

When the indirect method is used, details from which of the following balance sheet

accounts are used in calculating both operating and financing cash flows?

A. Bonds payable.

B. Taxes payable.

C. Retained earnings.

D. Contributed capital.

Answer:

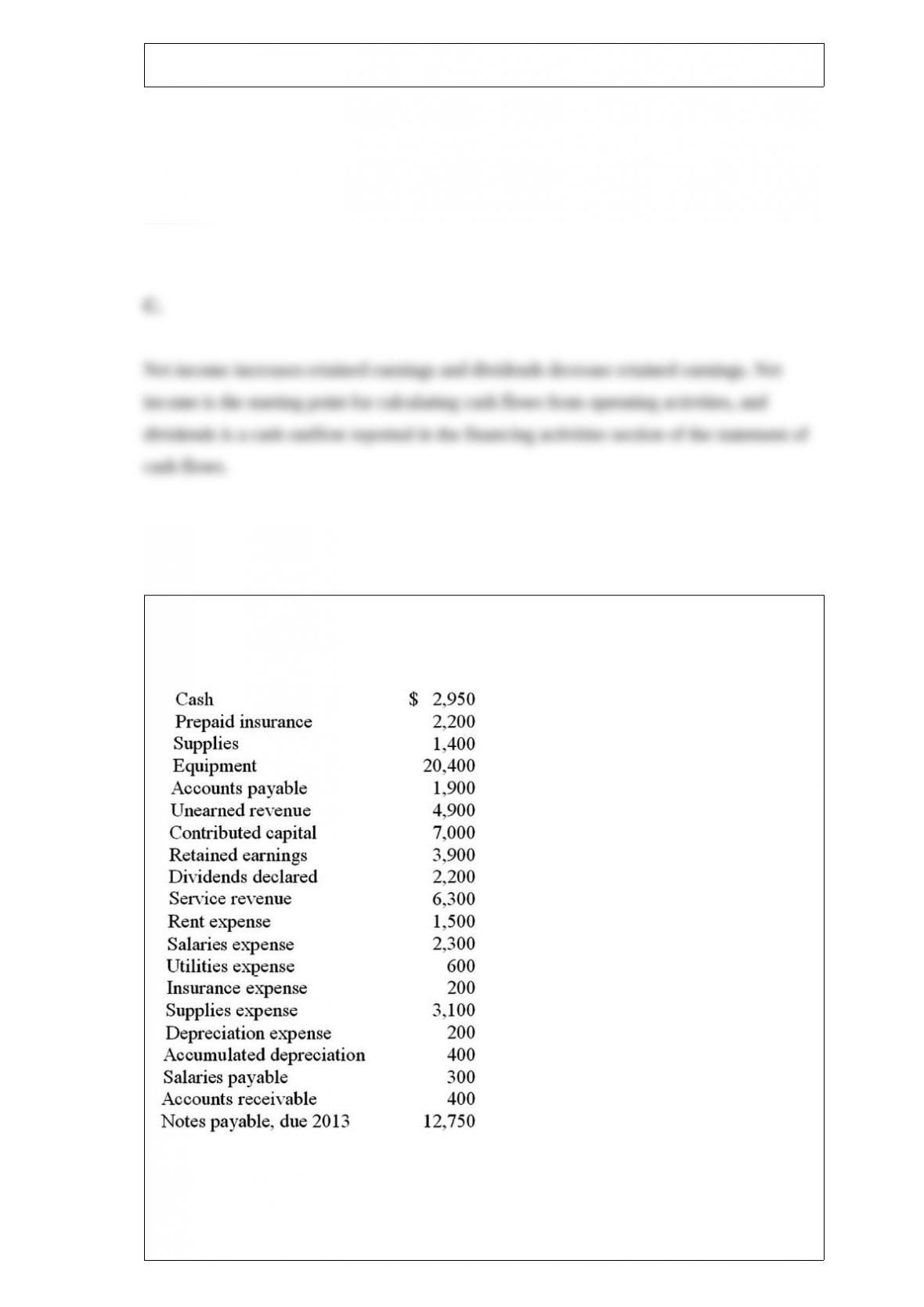

The following items are taken from the adjusted trial balance prepared as of December

31, 2013. All accounts have normal balances.

What is the amount of Retained Earnings on the Balance Sheet at December 31, 2013?

A. $100

B. $2,300

C. $3,900

D. $1,700

Answer:

On December 31, 2013, the balance in retained earnings is $20,000. On December 31,

2014, the balance in retained earnings is $19,100. During 2014, dividends of $4,000

were declared and paid. What is the amount of net income for 2014?

A. $4,900

B. $3,100

C. $900

D. $(900)

Answer:

Trudy’s Café paid employees $50,000 in September for work done that month. What

journal entry will Trudy’s record in September, assuming Trudy’s did not owe any

amounts to employees at the end of August?

A. Debit Cash, credit Wages Revenue.

B. Debit Cash, credit Wages Payable.

C. Debit Wages Revenue, credit Cash.

D. Debit Wages Expense, credit Cash.

Answer:

A check that was outstanding on last period’s bank reconciliation was not among the

cancelled checks returned by the bank this period. In preparing the bank reconciliation

for this period, the amount of this check should be

A. added to the bank balance of cash.

B. ignored in preparing this period’s bank reconciliation.

C. deducted from the bank balance of cash.

D. deducted from the company’s balance of cash.

Answer:

Current liabilities could include all of the following except:

A. accounts payable due in 30 days.

B. notes payable due in 9 months.

C. a bank loan due in 18 months.

D. any part of long-term debt due during the current period.

Answer:

Which of the following business organizations has only one owner?

A. A corporation.

B. A sole proprietorship.

C. A public company.

D. A partnership.

Answer:

During 2013, a company’s assets increase by $56,000 and its liabilities increase by

$38,000. If no dividend is paid and no further capital is contributed, net income for

2013 was:

A. $56,000.

B. $18,000.

C. $94,000.

D. $38,000.

Answer:

Transactions include which two types of events?

A. Direct events, indirect events.

B. Monetary events, production events.

C. External exchanges, internal events.

D. Past events, future events.

Answer:

Company X has net sales revenue of $1,250,000, cost of goods sold of $760,000, and

all other expenses of $290,000. The beginning balance of stockholders’ equity is

$400,000 and the beginning balance of fixed assets is $361,000. The ending balance of

stockholders’ equity is $600,000 and the ending balance of fixed assets is $389,000. The

return on equity (ROE) ratio is closest to:

A. 0.53.

B. 2.50.

C. 3.33.

D. 0.40.

Answer:

Which of the following would be in the work-in-process inventory of a company

making cheese?

A. Milk and cream used to make the cheese.

B. Cheese that has been made but is curing before being ready to sell.

C. Cured cheese that is waiting to be shipped to retailers.

D. Cured cheese that has been sold to retailers.

Answer:

At the end of the accounting period, which of the following accounts would not be

closed?

A. Sales Discounts

B. Cost of Goods Sold

C. Sales Returns & Allowances

D. Inventory

Answer:

Choose the letter to of the appropriate definition to match each term. Not all definitions

will be used.

Term

_____ 1/ Accelerated depreciation

_____ 2/ Goodwill

_____ 3/ Patent

_____ 4/ EBITDA

_____ 5/ Net book value

_____ 6/ Fixed assets

_____ 7/ Straight-line depreciation

_____ 8/ Residual value

_____ 9/ Trademark

Definition

A. Names or images that appear with a ® or TM.

B. A tax law dealing with how companies can depreciate their assets.

C. An intangible asset that represents the value of unidentifiable assets acquired.

D. Assets whose values do not change over time.

E. When a company expenses the cost of a long-lived asset by a constant annual

amount.

F. The acquisition cost of an asset minus its accumulated depreciation.

G. The estimated total use a company expects to receive from an asset.

H. Net income plus interest, taxes, depreciation and amortization expenses.

I. What a company expects to receive when an asset is disposed of at the end of its

useful life.

J. When a company expenses the entire cost of a long-lived asset in the first year of use.

K. Tangible long-lived assets.

L. When a company receives free publicity in return for charitable contributions.

M. When a company allocates the cost of a long-lived asset at a higher rate in the first

years of use.

N. The exclusive right to sell or use a product or process that is granted to encourage

innovation.

Answer:

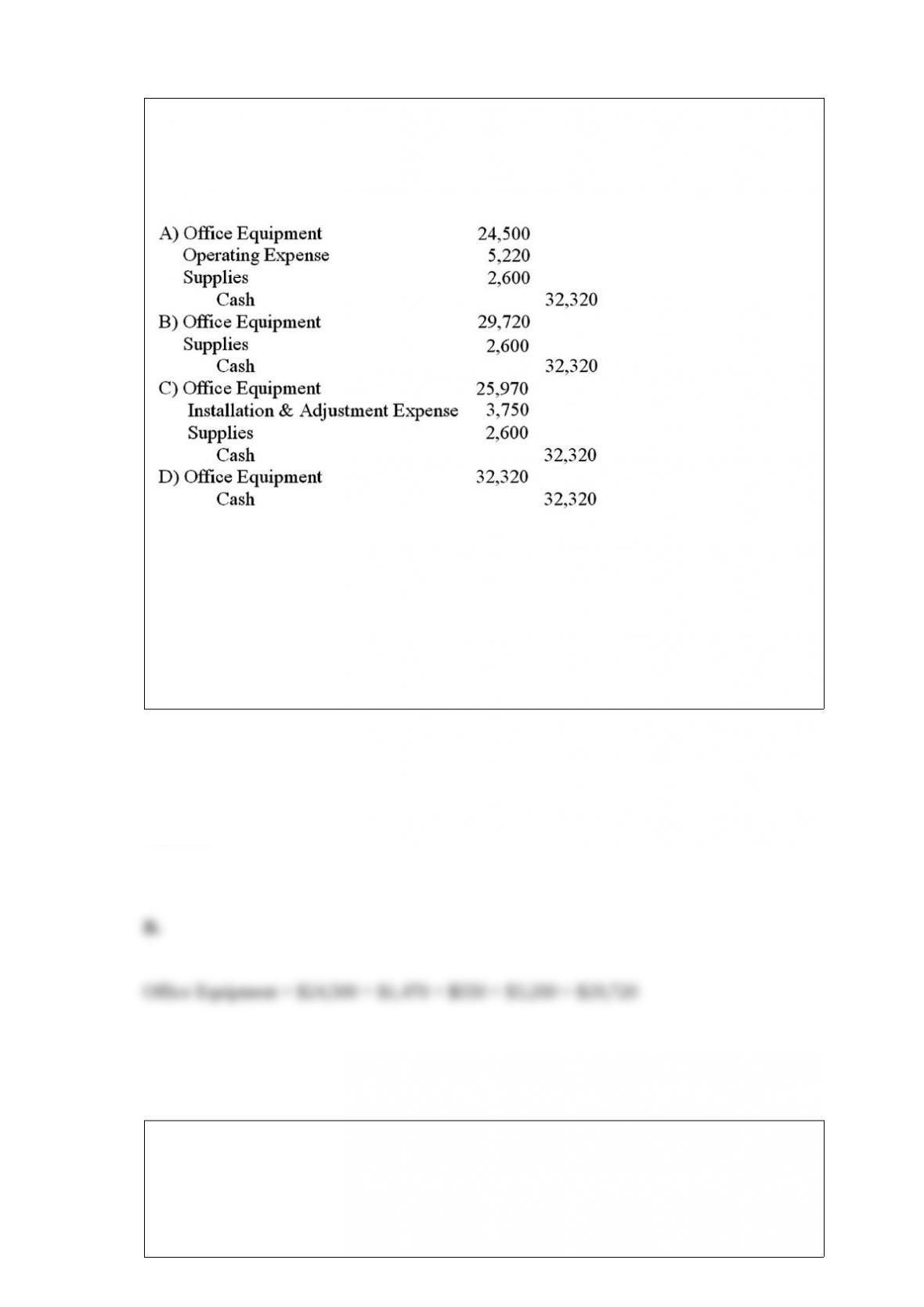

A company purchased office equipment for $24,500 and paid $1,470 in sales tax, $550

for installation, $3,200 for a needed adjustment to the equipment, and $2,600 for

supplies that will be used for periodic routine maintenance. What is the journal entry to

record this purchase?

A. Option A

B. Option B

C. Option C

D. Option D

Answer:

Your company rents out computers to local businesses and schools. You have 1,000

computers with a net book value of $160,000. As a result of changing technology, your

computers are more difficult to rent so you must severely reduce your rental price,

which causes a decrease in estimated future cash flows. The fair value of the computers

is estimated to be $125,000 because of their outdated technology. Your company should

report an asset impairment loss of:

A. $160,000.

B. $125,000.

C. $35,000.

D. $0

Answer:

A company has $72,500 of inventory at the beginning of the year and $65,500 at the

end of the year. Sales revenue is $986,400, cost of goods sold is $572,700, and net

income is $124,200 for the year. The inventory turnover ratio is closest to:

A. 1.8.

B. 8.3.

C. 6.0.

D. 14.3.

Answer:

A company loaned $1,000,000 with interest at 7% to another company. The interest

revenue from this loan would be reported on the statement of cash flows as

A. cash inflow from operating activities.

B. cash inflow from investing activities.

C. cash inflow from financing activities.

D. noncash transaction in a supplemental disclosure.

Answer:

Which of the following is not an operating activity?

A. Paying off a loan to the bank.

B. Receiving cash from customers for services rendered.

C. Paying employees for work completed.

D. Billing customers for services rendered but not yet paid for.

Answer:

A company began the year with Assets of $100,000, Liabilities of $20,000 and

Stockholders’ equity of $80,000. During the year Assets increased $55,000 and

stockholders’ equity increased $20,000. What was the change in Liabilities for the year?

A. Increase of $75,000

B. Increase of $35,000

C. Decrease of $75,000

D. Decrease of $35,000

Answer: