Which of the following creates a deferred tax liability?

a. An unrealized loss from recording inventory at lower of cost or market.

b. Accelerated depreciation in the tax return.

c. Estimated warranty expense.

d. Subscriptions collected in advance.

On June 1, 2016, Emmet Property Management entered into a 2-year contract to

oversee leasing and maintenance for an apartment building. The contract starts on July

1, 2016. Under the terms of the contract, Emmet will be paid a fixed fee of $50,000 per

year and will receive an additional 15% of the fixed fee at the end of each year provided

that building occupancy exceeds 90%. Emmet estimates a 30% chance it will exceed

the occupancy threshold, and concludes the revenue recognition over time is

appropriate for this contract.

Assume Emmet estimates variable consideration as the expected value. How much

revenue should Emmet recognize on this contract in 2016?

a. $25,000

b. $26,125

c. $28,750

d. $50,000

A deferred tax asset represents a:

a. Future income tax benefit.

b. Future cash collection.

c. Future tax refund.

d. Future amount of money to be paid out.

Canliss Mining uses the replacement method to determine depreciation on its office

equipment. During 2014, its first year of operations, office equipment was purchased at

a cost of $14,000. Useful life of the equipment averages four years and no salvage value

is anticipated. In 2016, equipment costing $5,000 was sold for $600 and replaced with

new equipment costing $6,000. Canliss would record 2016 depreciation of:

a. $3,500.

b. $4,400.

c. $5,400.

d. None of these answer choices are correct.

Listed below are 5 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the correct term. 1> Unqualified opinion a.

Independent and professional report about the fairness of the financial statements.

2> Disclaimer

3> Auditors’ report b. Given by an auditor when there is a limitation of audit

procedures or a departure from GAAP.

4> Qualified opinion

5> Adverse opinion c. Given by an auditor when financial statements are presented

fairly in conformity with GAAP.

d. Given by an auditor when there are substantial reporting errors and a qualified

opinion is not appropriate.

e. Given by an auditor when information is insufficient to express an opinion.

The most common type of liability is:

a. One that comes into existence due to a loss contingency.

b. One that must be estimated.

c. One that comes into existence due to a gain contingency.

d. One to be paid in cash and for which the amount and timing are known.

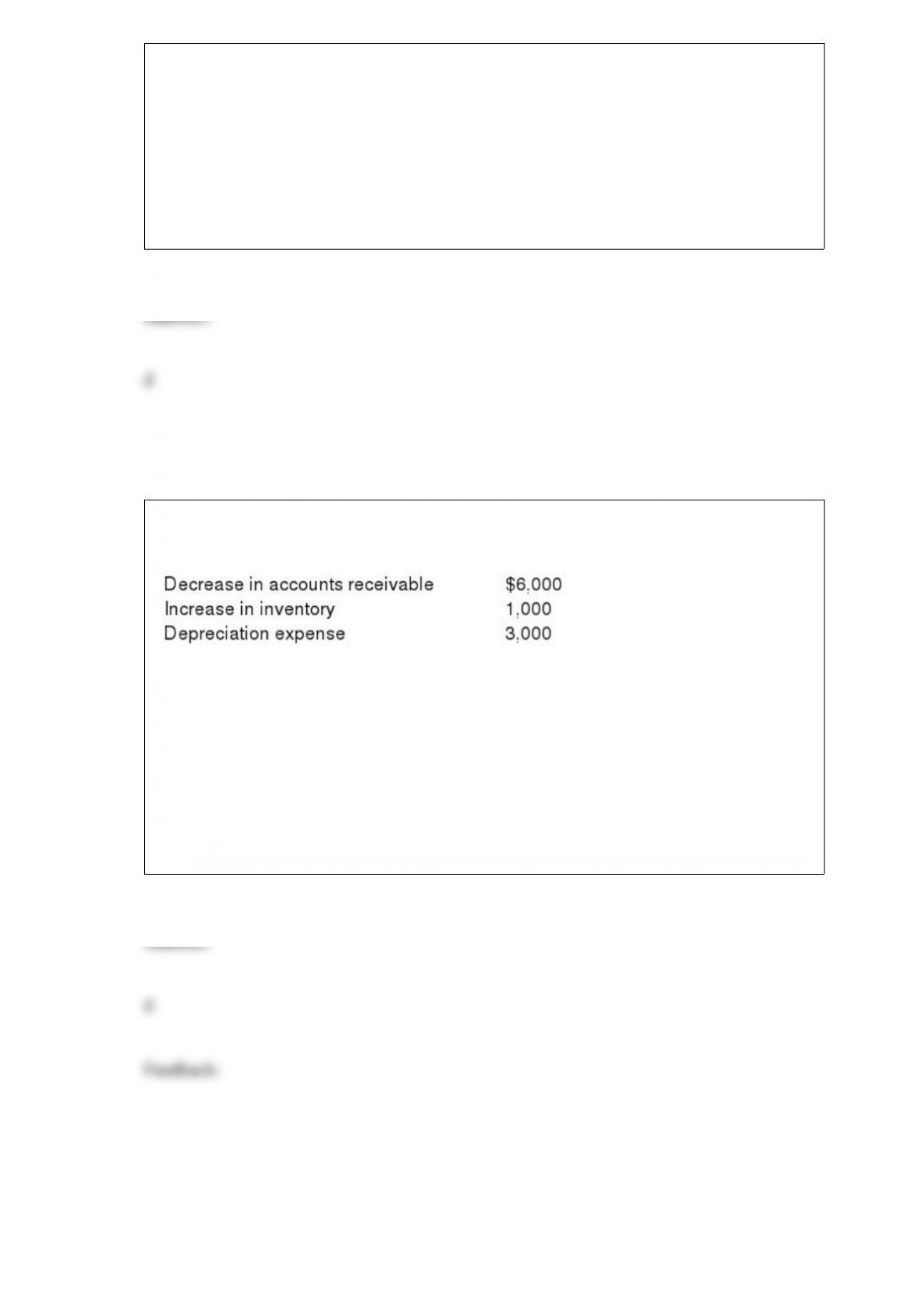

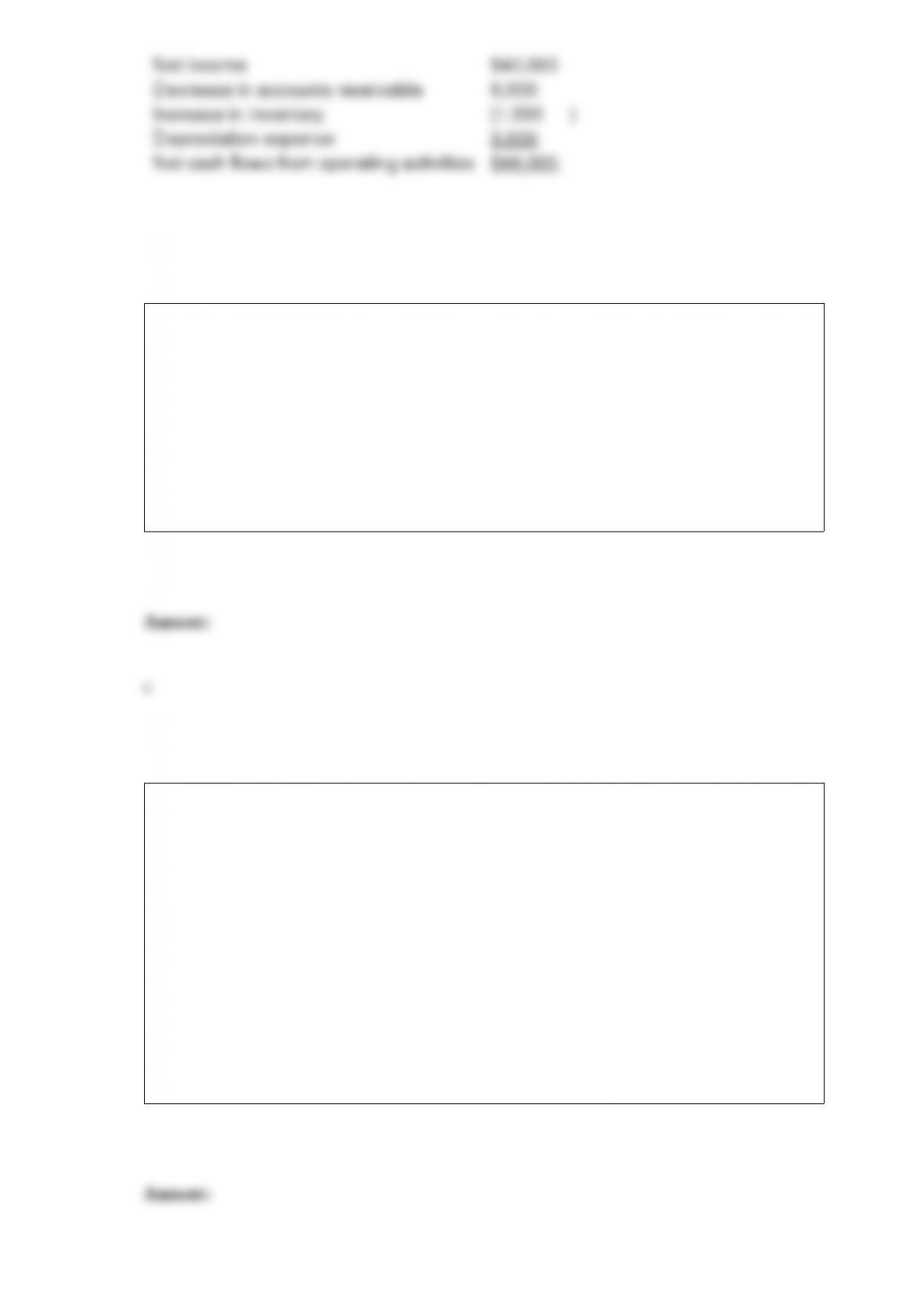

Hemmer Company reported net income for 2016 in the amount of $40,000. The

company’s financial statements also included the following:

What is net cash provided by operating activities?

a. $38,000.

b. $43,000.

c. $35,000.

d. $48,000.

Which of the following is not classified as an operating activity?

a. Interest paid on long-term debt.

b. Dividends received on common stock.

c. Dividends paid on common stock.

d. Payments on accounts payable.

During the year, L&M Leather Goods sold 1,000,000 reversible belts under a new sales

promotional program. Each belt carried one coupon, which entitles the customer to a

$4.00 cash rebate. L&M estimates that 70% of the coupons will be redeemed, even

though only 500,000 coupons had been processed during the year. At December 31,

L&M should report a liability for unredeemed coupons of:

a. $ 700,000.

b. $ 800,000.

c. $1,000,000.

d. $2,800,000.

Rusty Hardware makes only cash sales. It began 2016 with a credit balance of $32,000

in the refund liability account. Sales during 2016 were $600,000. Rusty estimates that

6% of all sales will be returned. During 2016, customers returned merchandise for

credit of $28,000 to their accounts.

Rusty’s 2016 income statement would report net sales of:

a. $600,000.

b. $564,000.

c. $568,000.

d. $604,000.

Grab Manufacturing Co. purchased a 10-ton draw press at a cost of $180,000 with

terms of 5/15, n/45. Payment was made within the discount period. Shipping costs were

$4,600, which included $200 for insurance in transit. Installation costs totaled $12,000,

which included $4,000 for taking out a section of a wall and rebuilding it because the

press was too large for the doorway. The capitalized cost of the 10-ton draw press is:

a. $171,000.

b. $183,600.

c. $187,600.

d. $185,760.

Sullivan Software sells packages of a software program and one year’s worth of

technical support for $500. Its packaging lists the $500 sales price as comprised of a

software program at a price of $450 and technical support with a price of $100, with a

$50 discount for the package deal. All of Sullivan’s sales are for cash, and there are no

returns. Sullivan sells the software program separately for $475 and offers a year of

technical support separately for $75.

Sullivan should recognize revenue for the two parts of the arrangement as follows:

a. Recognize the entire $500 when the customer pays cash to buy the package.

b. Recognize the portion of the $500 attributable to the software program when the

customer pays cash to buy the package; defer the portion attributable to technical

support and recognize over the support period.

c. Defer the entire $500 and recognize over the support period.

d. Recognize the entire $500 upon conclusion of the support period.

Boomerang Computer Company sells computers with an unconditional right to return

the computer if the customer is not satisfied. Boomerang has a long history selling these

computers under this returns policy and can provide precise estimates of the amount of

returns associated with each sale. Boomerang most likely should recognize revenue:

a. When Boomerang delivers a computer to a customer, ignoring potential returns.

b. When Boomerang delivers a computer to a customer, in an amount that is reduced by

the expected returns.

c. When Boomerang receives cash from the customer.

d. When a customer returns a computer.

Lake Power Sports sells jet skis and other powered recreational equipment. Customers

pay one-third of the sales price of a jet ski when they initially purchase the ski, and then

pay another one-third each year for the next two years. Because Lake has little

information about the ability to collect these receivables, it uses the installment sales

method for revenue recognition. In 2015, Lake began operations and sold jet skis with a

total price of $900,000 that cost Lake $450,000. Lake collected $300,000 in 2015,

$300,000 in 2016, and $300,000 in 2017 associated with those sales. In 2016, Lake sold

jet skis with a total price of $1,500,000 that cost Lake $900,000. Lake collected

$500,000 in 2016, $400,000 in 2017, and $400,000 in 2018 associated with those sales.

In 2018, Lake also repossessed $200,000 of jet skis that were sold in 2016. Those jet

skis had a fair value of $75,000 at the time they were repossessed.

In 2018, Lake would record a loss on repossession of:

a. $45,000.

b. $200,000.

c. $120,000.

d. $80,000

In the statement of cash flows, by using the indirect method for determining cash flows

from operating activities, a decrease in deferred tax liabilities is:

a. Added to net income.

b. Subtracted from net income.

c. Ignored.

d. Included under financing activities.

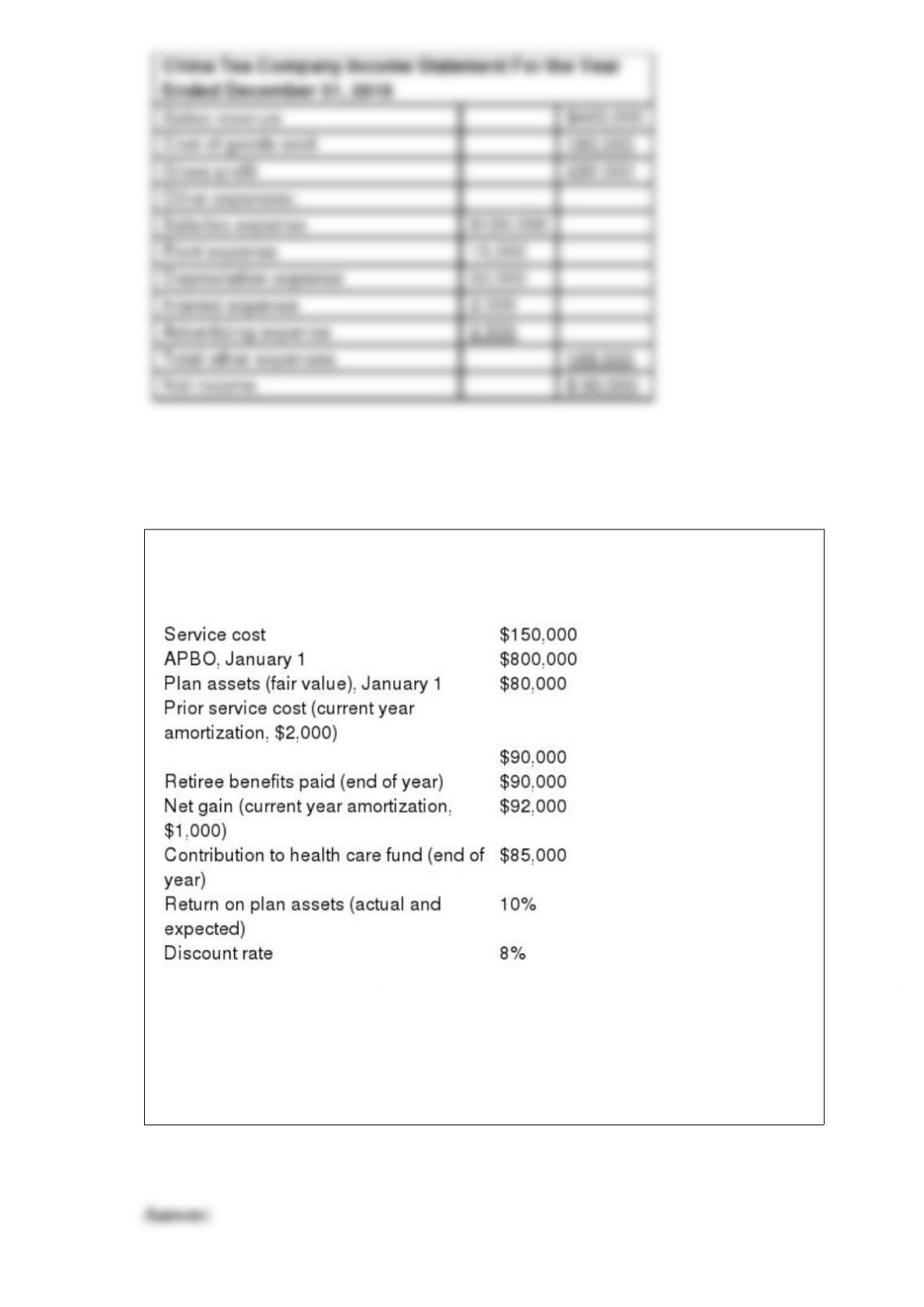

The following data are for Guava Company’s retiree health care plan for the current

calendar year.

What is the interest cost to be included in the current year’s postretirement benefit

expense?

a. $3,600.

b. $720.

c. $768.

d. $4,000.

Slick’s Used Cars sells pre-owned cars on the installment basis and carries its own notes

because its customers typically cannot qualify for a bank loan. Default rates tend to be

high or unpredictable. However, in the event of nonpayment, Slick’s can usually

repossess the cars without loss. The revenue method Slick would use is the:

a) Installment sales method.

b) Point of sales method.

c) Cost recovery method.

d) Installment sales method or cost recovery method.

Due to an error in computing depreciation expense, Prewitt Corporation overstated

accumulated depreciation by $20 million as of December 31, 2016. Prewitt has a tax

rate of 30%. Prewitt’s retained earnings as of December 31, 2016, would be:

a. Overstated by $14 million.

b. Understated by $14 million.

c. Overstated by $6 million.

d. Understated by $6 million.

Cash equivalents do not include:

a. Money market funds.

b. High grade marketable equity securities.

c. U.S. treasury bills.

d. Commercial paper.

What is the SEC and how is it involved with accounting standard-setting?

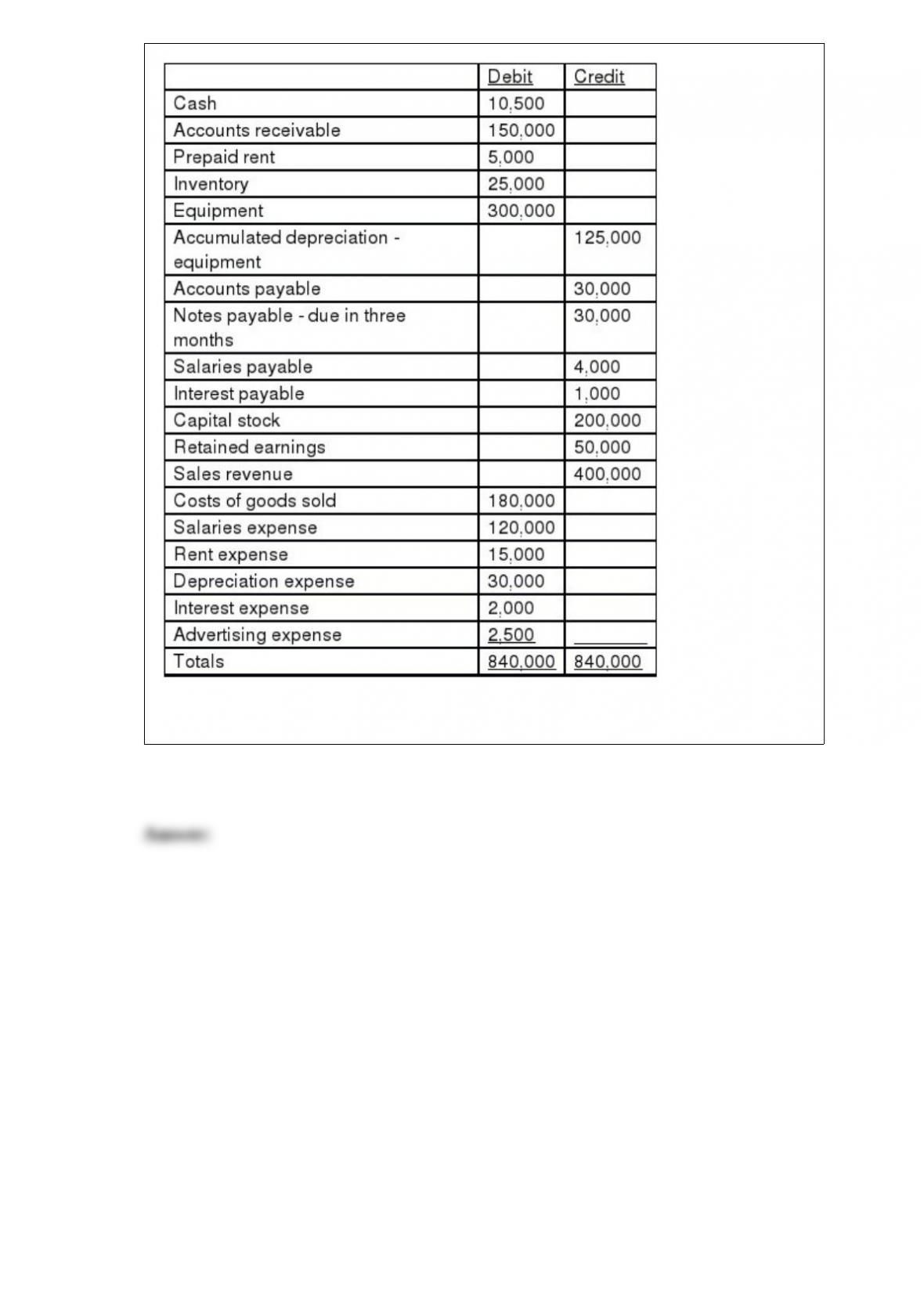

The adjusted trial balance for China Tea Company at December 31, 2016, is presented

below:

Prepare an income statement for China Tea Company for the year ended December 31,

2016.

Data pertaining to the postretirement health care benefit plan of Danielson Delivery

Service include the following for the current calendar year:

Required:

1) Determine Danielson’s postretirement benefit expense for the current year.

2) Prepare the journal entries to record the benefit expense and funding for the current

year.

Listed below are five terms followed by a list of phrases that describe or characterize

each of the terms. Match each phrase with the correct number code for the term.

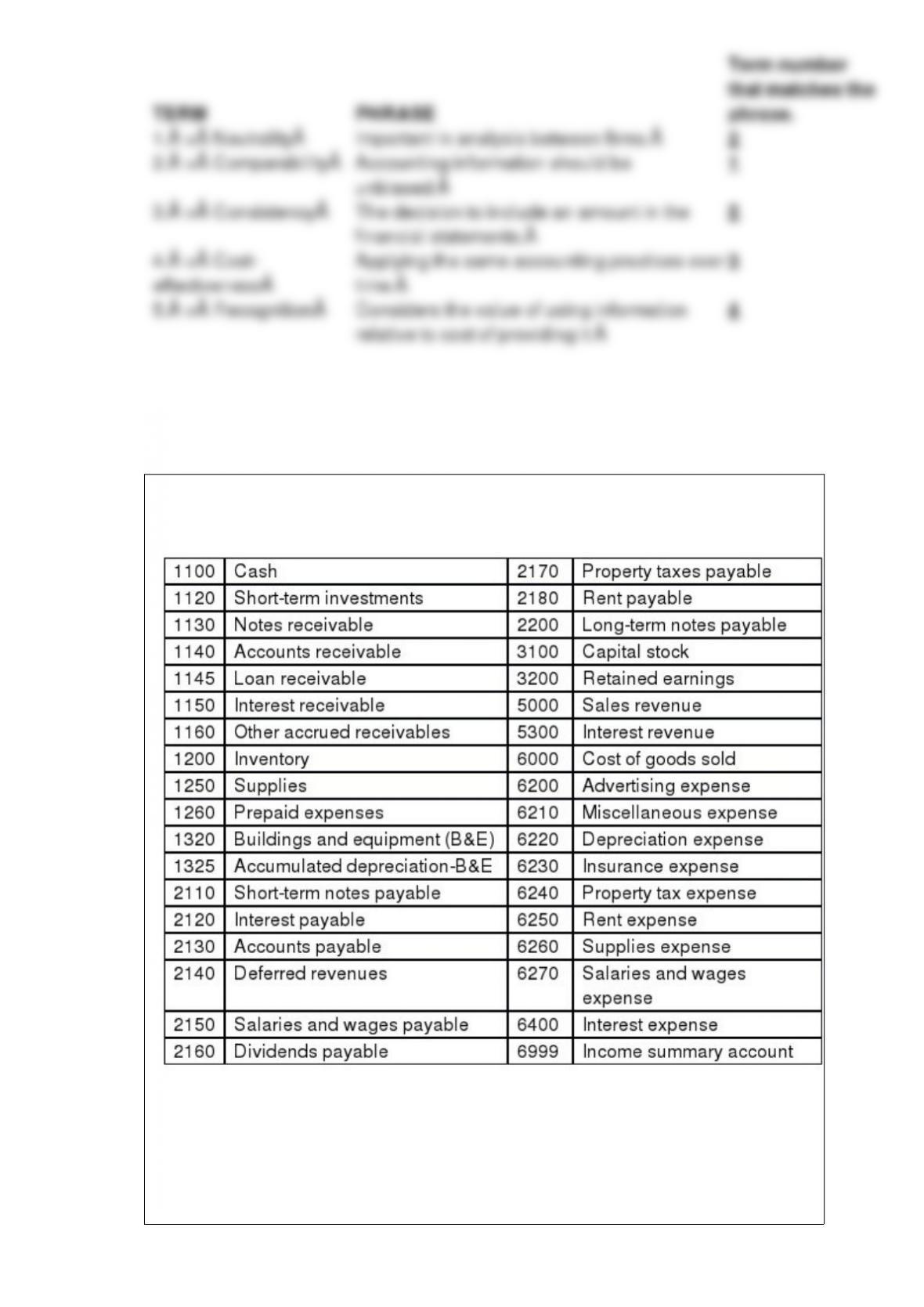

Using the chart of accounts provided, indicate by account number the account or

accounts that would be debited and credited in the following transactions and indicate

the type of transaction as: (1) an external transaction, (2) an internal transaction

recorded as an adjusting journal entry, or (3) a closing entry. The company uses a

perpetual inventory system. All prepayments are initially recorded in permanent

accounts.

Sold inventory on account.