Anne Company has total cash register receipts of $39,690. This total includes a 5%

sales tax. The entry to record the receipts will include a

a. debit to Sales Tax Expense for $1,890.

b. credit to Sales Revenue for $36,690.

c. credit to Sales Taxes Payable for $1,986.

d. credit to Sales Taxes Payable for $1,890.

Answer:

If you are able to earn an 8% rate of return, what amount would you need to invest to

have $30,000 one year from now?

a. $27,747

b. $27,778

c. $27,273

d. $29,700

Answer:

GAAP defines market for lower-of-cost-or market essentially as

a. net realizable value.

b. estimated selling price in the ordinary course of business.

c. replacement cost.

d. replacement cost less costs of disposal.

Answer:

In reviewing the accounts receivable, the cash realizable value is $16,000 before the

write-off of a $1,500 account. What is the cash realizable value after the write-off?

a. $1,500

b. $14,500

c. $16,000

d. $17,500

Answer:

A periodic inventory system

a. allows for the determination of cost of goods sold after each sale.

b. traditionally has been used with low unit-value items.

c. requires that detailed inventory records be kept.

d. none of these answer choices are correct.

Answer:

Available-for-sale securities are classified as

a. short-term investments only.

b. long-term investments only.

c. either short-term or long-term investments.

d. current assets only.

Answer:

Stanley Company had inventory of $660,000 and $540,000 on December 31, 2014, and

December 31, 2015, respectively. Cost of goods sold for 2015 was $4,200,000. Average

days to sell the inventory is approximately

a. 52.1.

b. 6.4.

c. 46.9.

d. 57.4.

Answer:

Liabilities of a company are owed to

a. debtors.

b. benefactors.

c. creditors.

d. underwriters.

Answer:

On June 1, 2015 Ted Leo buys a copier machine for his business and finances this

purchase with cash and a note. When journalizing this transaction, he will

a. use two journal entries.

b. make a compound entry.

c. make a simple entry.

d. list the credit entries first, which is proper form for this type of transaction.

Answer:

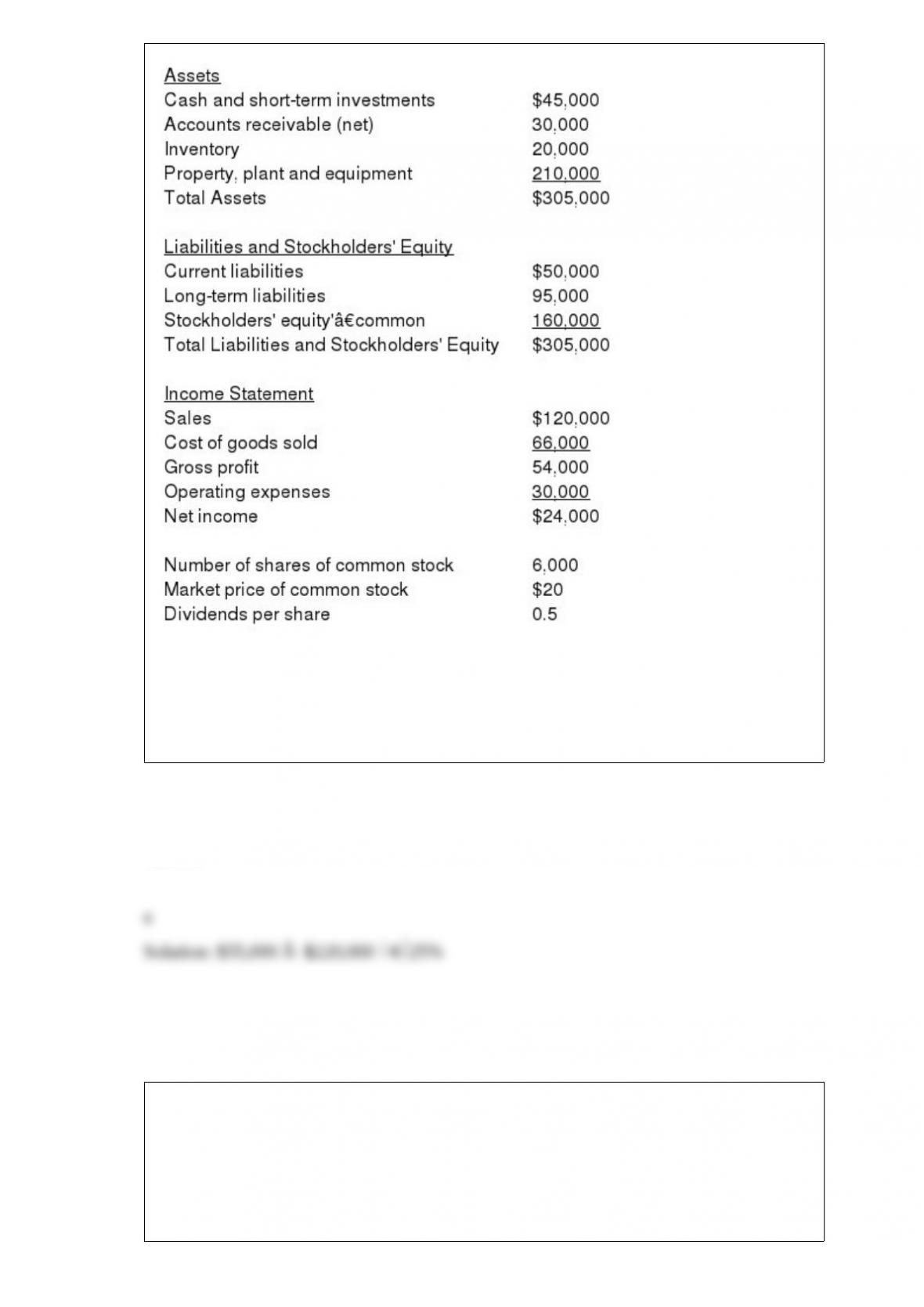

The following information pertains to Ortiz Company. Assume that all balance sheet

amounts represent both average and ending balance figures. Assume that all sales were

on credit.

What is the return on common stockholders’ equity for Ortiz?

a. 25%

b. 50%

c. 12.5%

d. 15.3%

Answer:

Which of the following statements is correct with respect to inventories?

a. The FIFO method assumes that the costs of the earliest goods acquired are the last to

be sold.

b. It is generally good business management to sell the most recently acquired goods

first.

c. Under FIFO, the ending inventory is based on the latest units purchased.

d. FIFO seldom coincides with the actual physical flow of inventory.

Answer:

Each of the following is an extraordinary item except the

a. effects of major casualties, if rare in the area.

b. effects of a newly enacted law or regulation.

c. expropriation of property by a foreign government.

d. losses attributable to labor strikes.

Answer:

Deborah Company’s account balances at December 31 for Accounts Receivable and

Allowance for Doubtful Accounts were $2,100,000 and $50,000 (Cr.), respectively. An

aging of accounts receivable indicated that $180,000 are expected to become

uncollectible. The amount of the adjusting entry for bad debts at December 31 is

a. $130,000.

b. $180,000.

c. $210,000.

d. $230,000.

Answer:

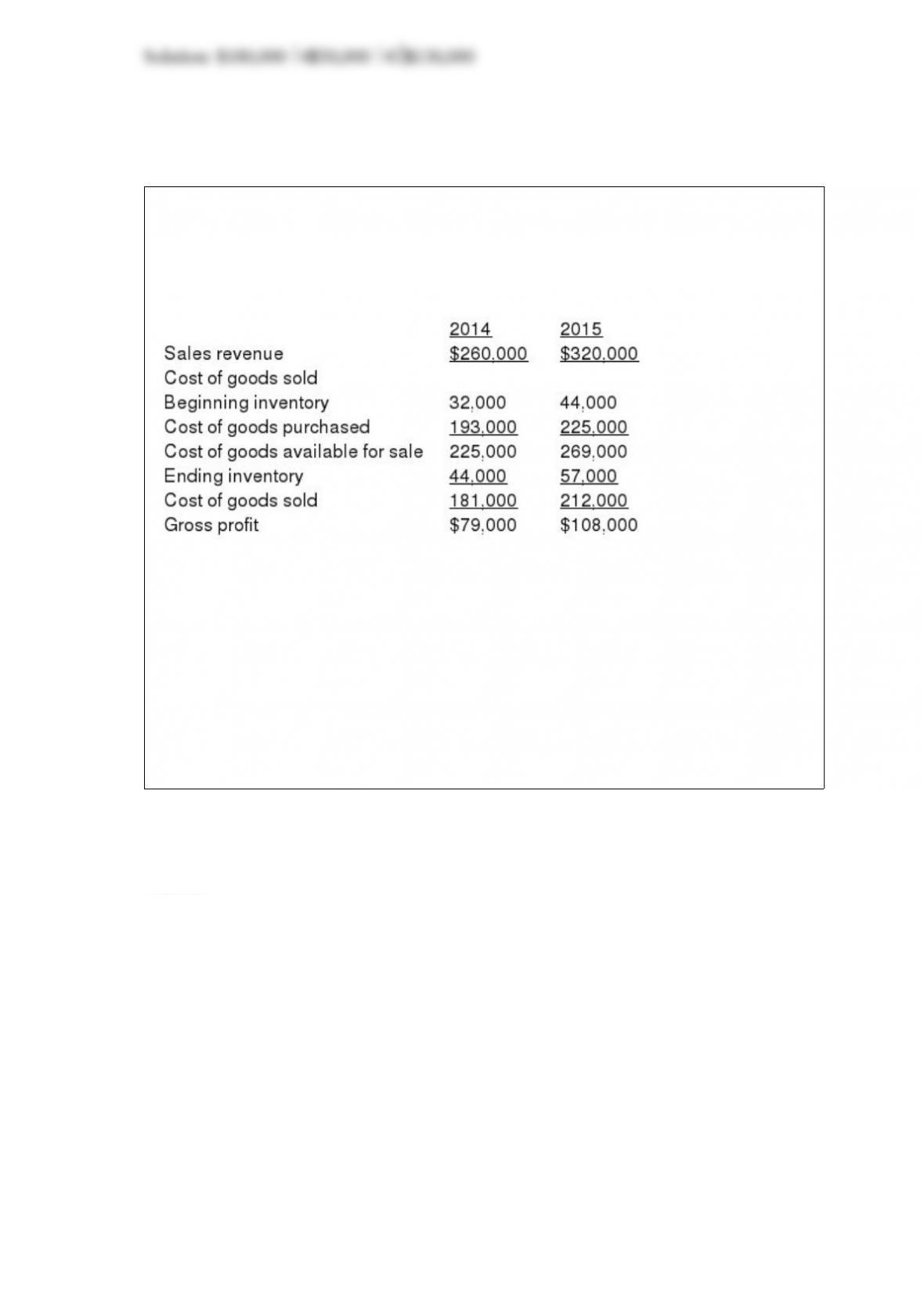

Morton Watch Company reported the following income statement data for a 2-year

period.

Morton uses a periodic inventory system. The inventories at January 1, 2014, and

December 31, 2015, are correct. However, the ending inventory at December 31, 2014,

was overstated $5,000.

Instructions

(a) Prepare correct income statement data for the 2 years.

(b) What is the cumulative effect of the inventory error on total gross profit for the 2

years?

Answer:

Instructions: Given the information provided below, prepare (a) a bank reconciliation

in proper format, and (b) the necessary journal entries for the month of September for

Tolan Company.

1> Balance per bank on September 30’”$24,070

2> Balance per books on September 30’”$19,500

3> Total outstanding checks at September 30’”$3,600

4> Debit memoranda:

a. NSF check from Lee Co.’”$540

b. Printing company checks’”$60

c. Payment to bank of $2,400 note owed bank by Tolan plus $200 interest.

5> Credit memorandum: Collection of note receivable for $7,500 plus $560 interest less

$60 collection fee.

6> Errors:

a. A check written this month to Nance Co. for office supplies cleared the bank at the

correct amount of $680, but was recorded by Tolan at $860.

b. The bank charged a $210 check of Thome Company against Tolan’s account this

month.

7> Deposit in transit on September 30’”$3,800.

(a) Bank Reconciliation

(b) Journal Entries (Note: Assume no interest has been accrued on the note.)

Answer:

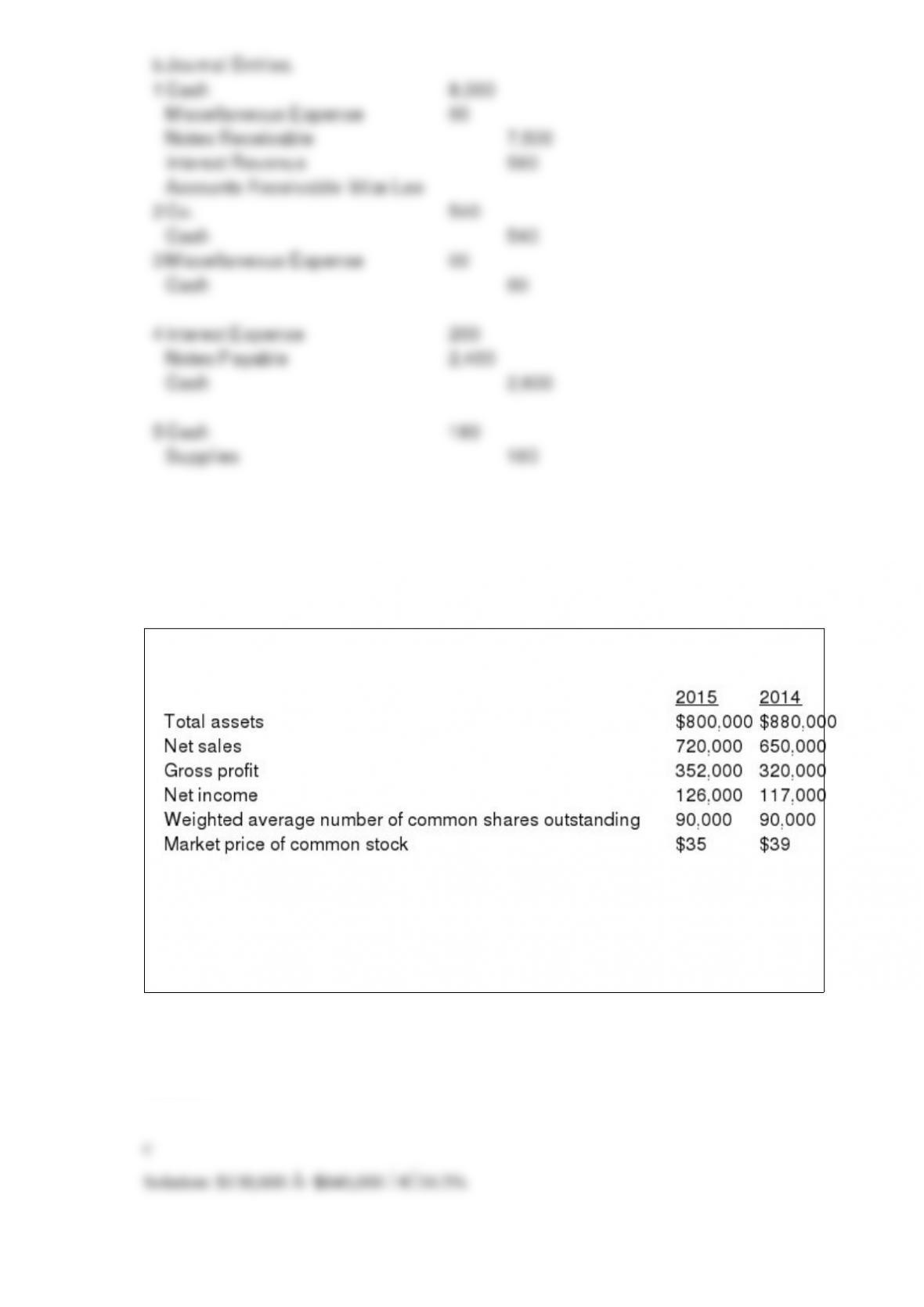

The following amounts were taken from the financial statements of Leaf Company:

The profit margin ratio for 2015 is

a. 15.4%.

b. 44.9%.

c. 16.5%.

d. 10.7%.

Answer:

Kreig Corporation has income before taxes of $900,000 and an extraordinary gain of

$300,000. If the income tax rate is 35% on all items, the income statement should show

income before irregular items and extraordinary items, respectively, of

a. $600,000 and $300,000.

b. $600,000 and $195,000.

c. $585,000 and $300,000.

d. $585,000 and $195,000.

Answer:

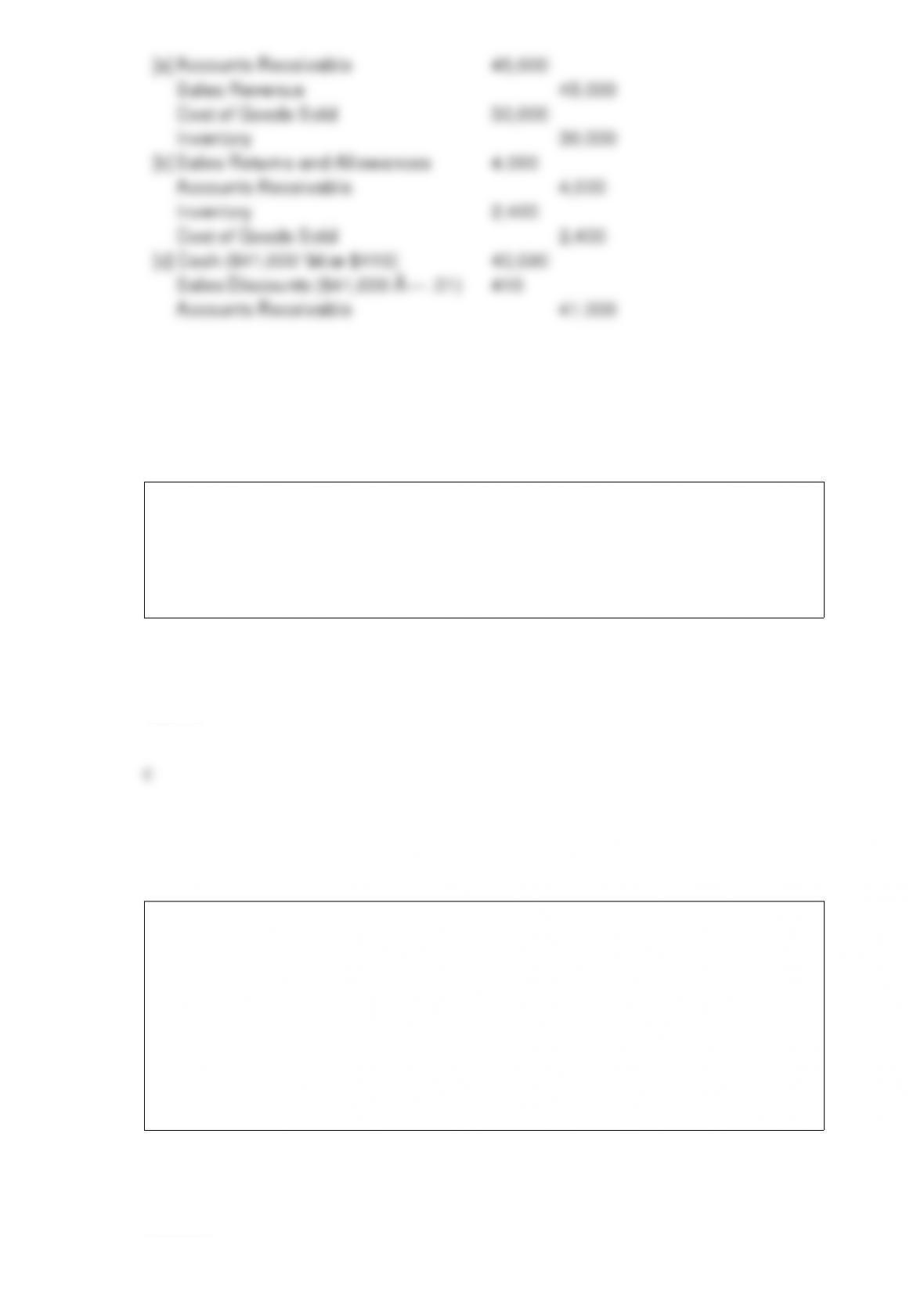

Prepare the necessary journal entries to record the following transactions, assuming

Eustace Company uses a perpetual inventory system.

(a) Eustace sells $45,000 of merchandise, terms 1/10, n/30. The merchandise cost

$30,000.

(b) The customer in (a) returned $4,000 of merchandise to Eustace. The merchandise

returned cost $2,400.

(c) Eustace received the balance due within the discount period.

Answer:

The explanation column of the general ledger

a. is completed without exception.

b. is nonexistent.

c. is used infrequently.

d. shows account titles.

Answer:

Understating beginning inventory will understate

a. assets.

b. cost of goods sold.

c. net income.

d. stockholder’s equity.

Answer:

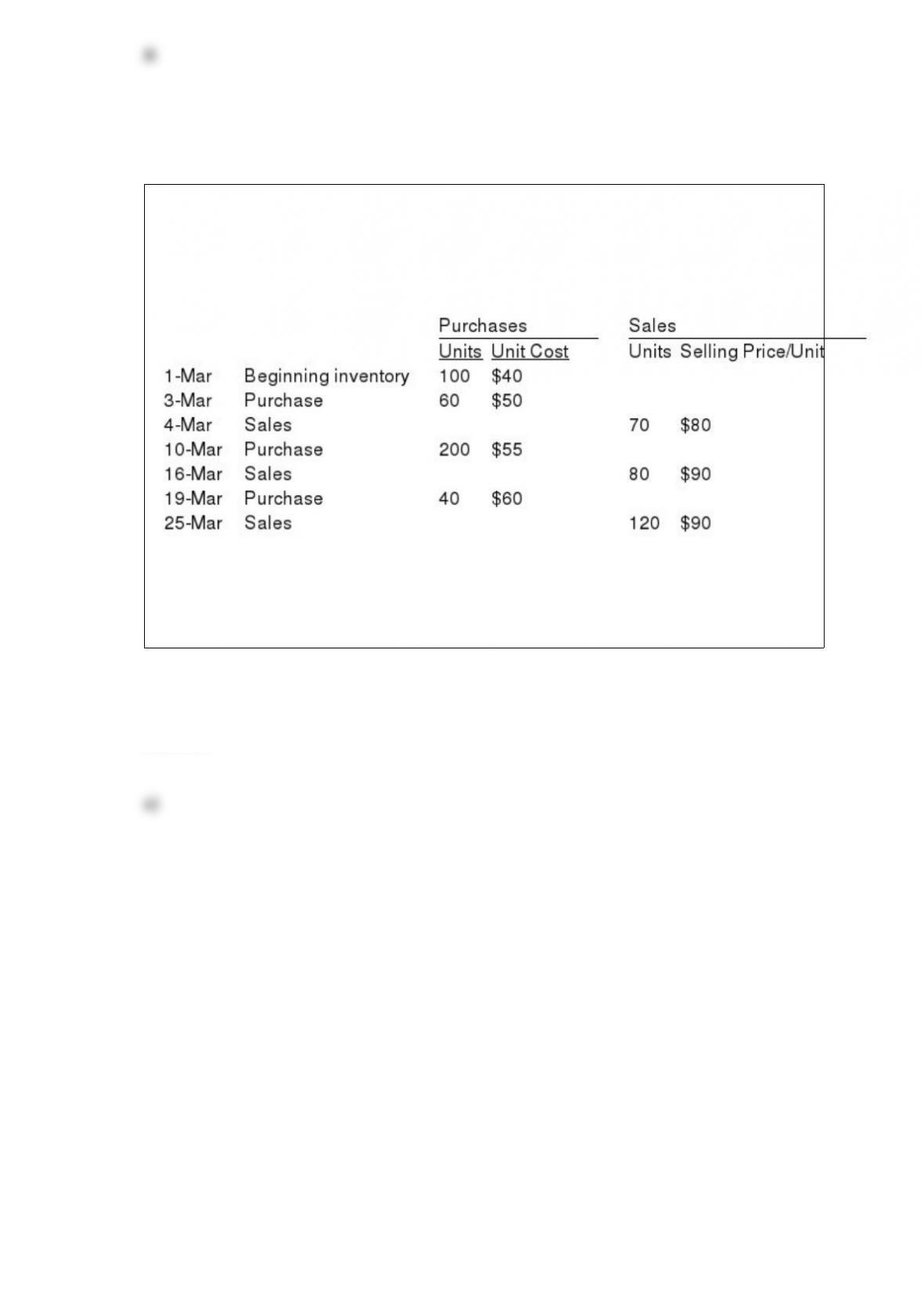

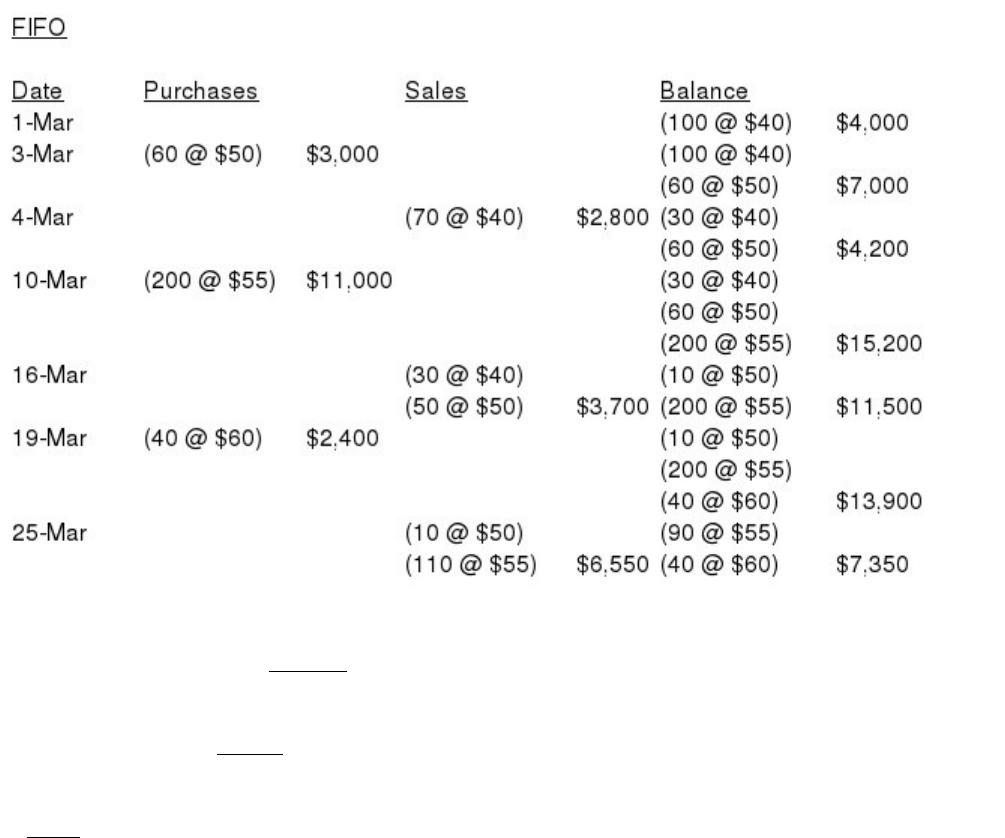

Norris Company uses the perpetual inventory system and had the following purchases

and sales during March.

Instructions

Using the inventory and sales data above, calculate the value assigned to cost of goods

sold in March and to the ending inventory at March 31 using (a) FIFO and (b) LIFO.

Answer:

The partnership form of business organization

a. is a separate legal entity.

b. is a common form of organization for service-type businesses.

c. enjoys an unlimited life.

d. has limited liability.

Answer:

The first item listed under current liabilities is usually

a. accounts payable.

b. notes payable.

c. salaries and wages payable.

d. taxes payable.

Answer:

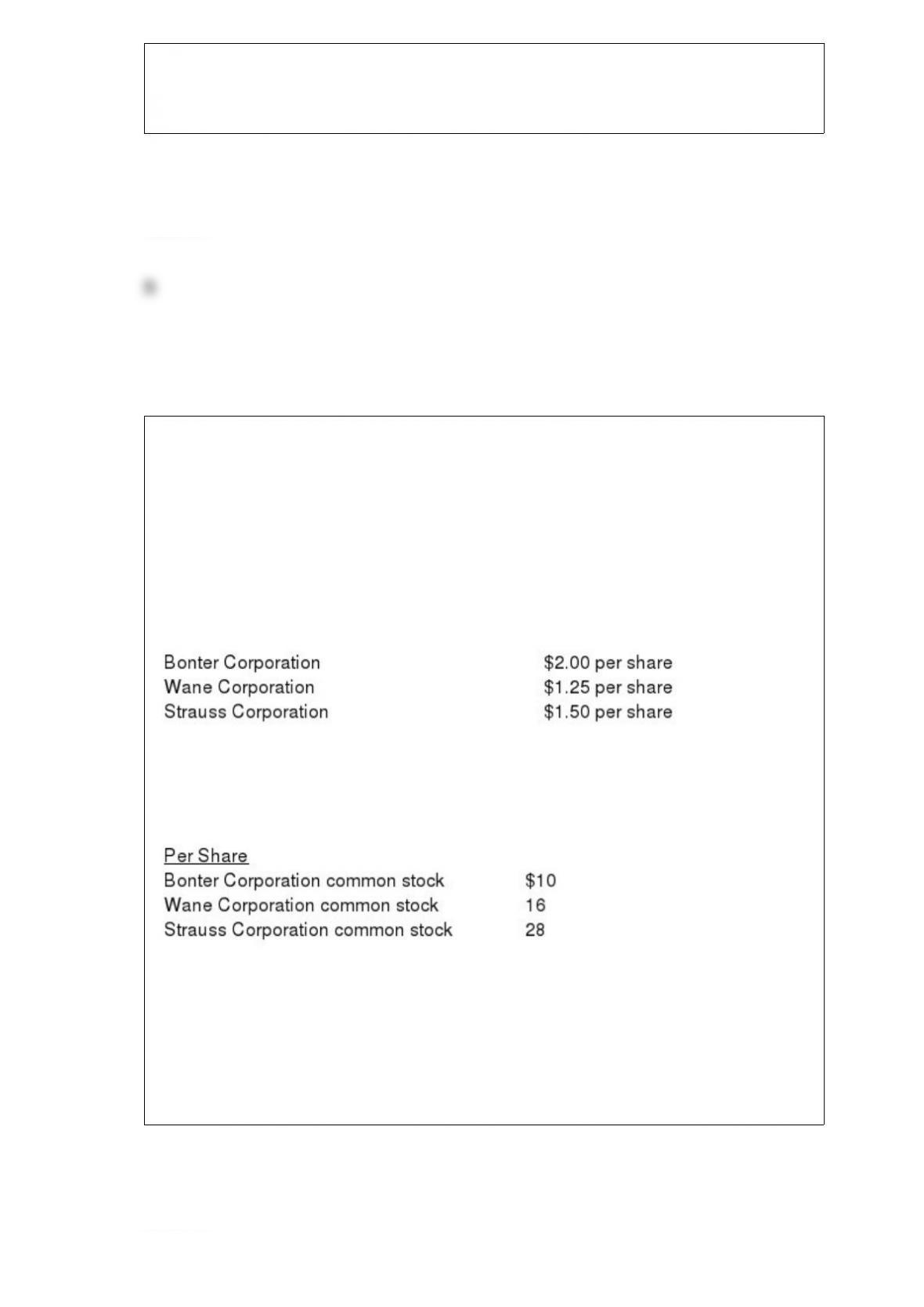

On January 5, 2014, Grouse Company purchased the following stock securities as a

long-term investment:

300 shares Bonter Corporation common stock for $4,500.

500 shares Wane Corporation common stock for $10,000.

800 shares Strauss Corporation common stock for $22,800.

Assume that Grouse Company cannot exercise significant influence over the activities

of the investee companies and that the cost method is used to account for the

investments.

On June 30, 2014, Grouse Company received the following cash dividends:

On November 15, 2014, Grouse Company sold 160 shares of Strauss Corporation

common stock for $7,200.

On December 31, 2014, the fair value of the securities held by Grouse Company is as

follows:

Instructions

Prepare the appropriate journal entries that Grouse Company should make on the

following dates:

January 5, 2014

June 30, 2014

November 15, 2014

December 31, 2014

Answer:

The retail inventory method requires a company to value its inventory on the balance

sheet at retail prices.

Answer:

The Financial Accounting Standards Board is a part of the Securities and Exchange

Commission.

Answer:

Net income of a corporation should be closed to retained earnings and net losses should

be closed to paid-in capital accounts.

Answer:

Prepare the necessary correcting entry for each of the following.

a> A collection on account of $350 from a customer was credited to Accounts

Receivable $530 and debited to Cash $530.

b> The purchase of supplies on account for $310 was recorded as a debit to Equipment

$310 and a credit to Accounts Payable $310.

Answer:

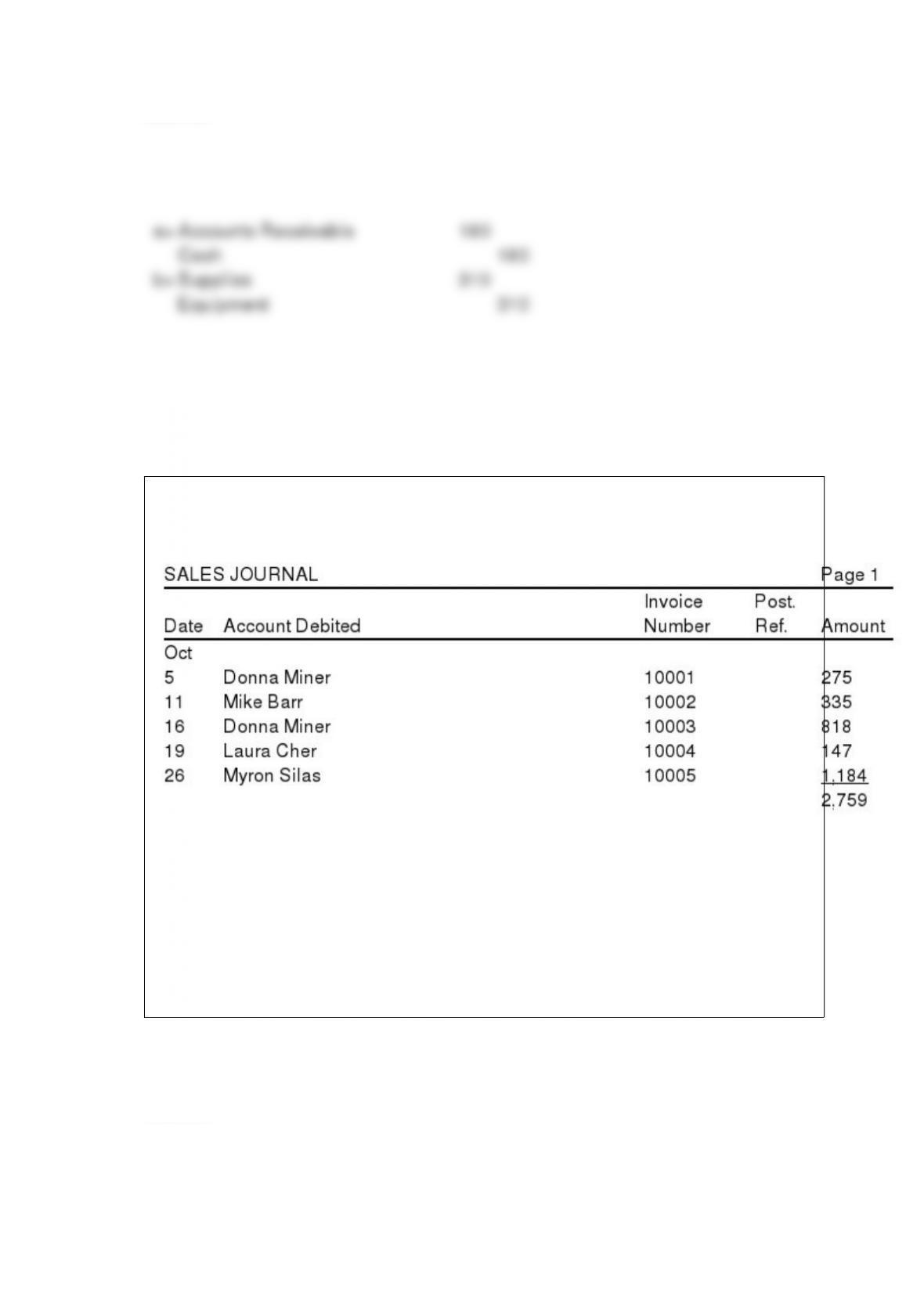

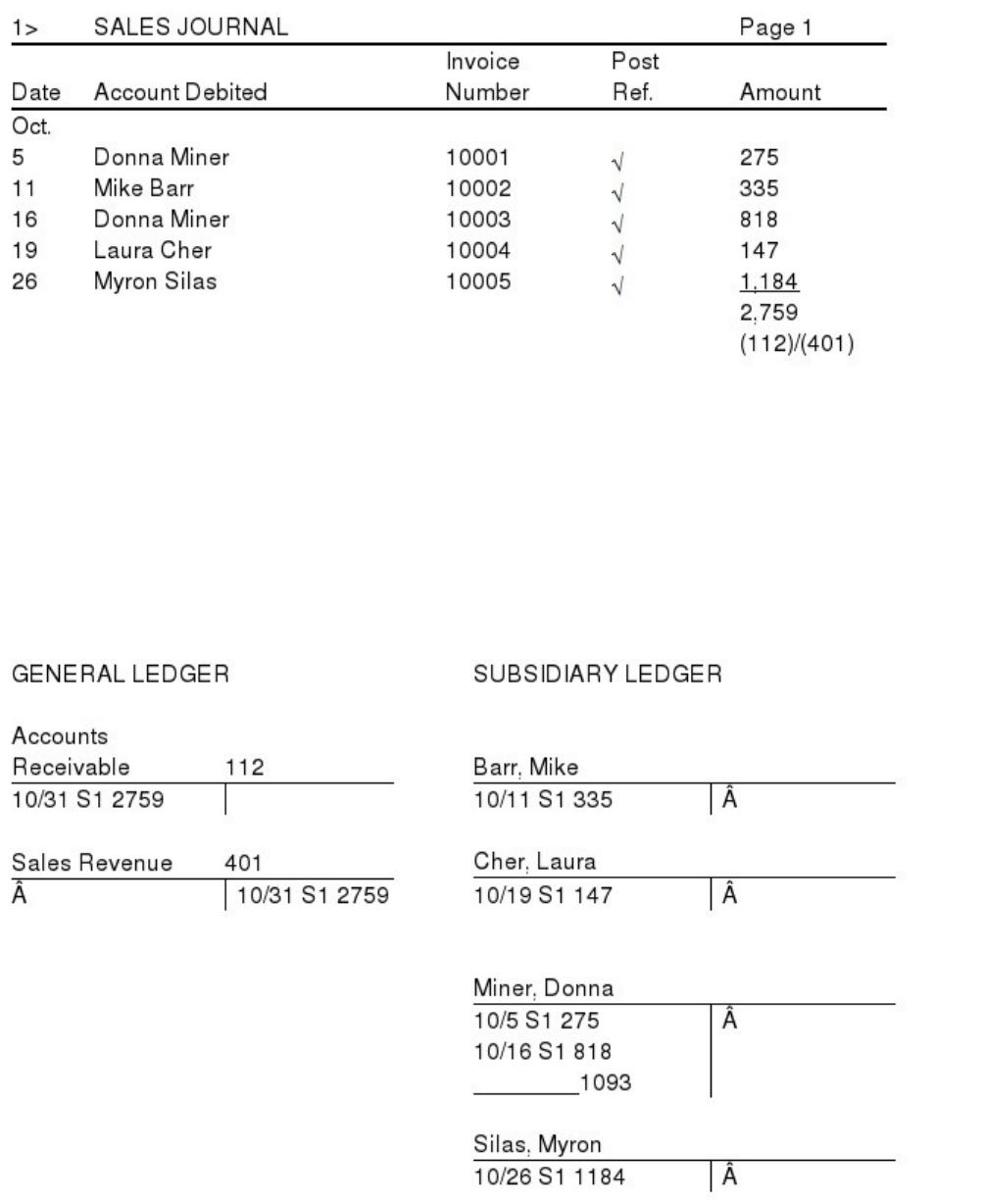

Easton Company began business on October The sales journal, as it appeared at the end

of the month, follows:

1> Open general ledger T-accounts for Accounts Receivable (No. 112) and Sales (No.

401) and an accounts receivable subsidiary T-account ledger with an account for each

customer. Make the appropriate postings from the sales journal. Fill in the appropriate

posting references in the sales journal above.

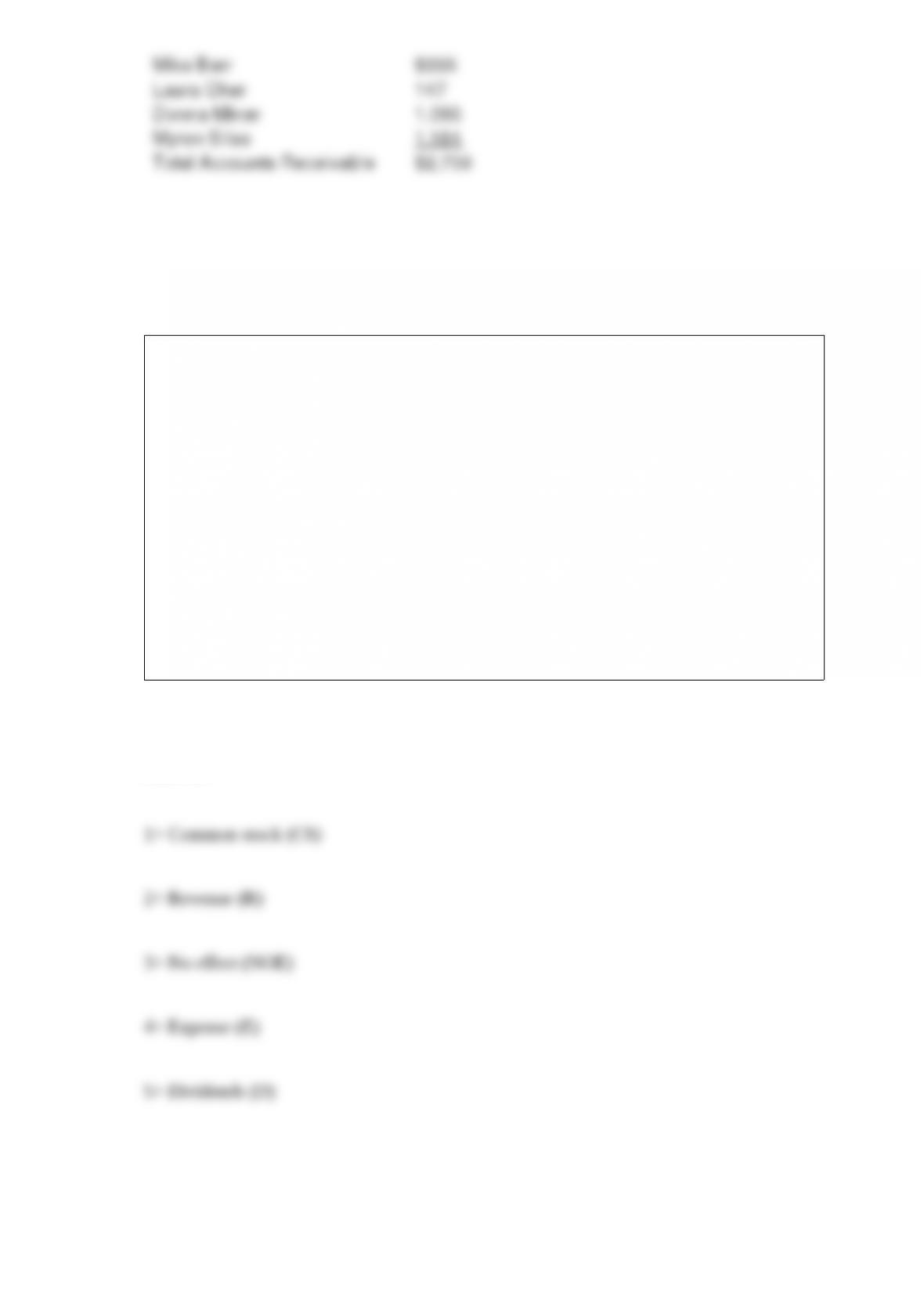

2> Prove the accounts receivable subsidiary ledger by preparing a schedule of accounts

receivable.

Answer:

For each of the following, indicate whether the transaction affects revenue (R), expense

(E), dividends (D), common stock (CS), or no effect on stockholders’ equity (NOE).

1> Made an investment to start the business.

2> Billed customers for services performed.

3> Purchased equipment on account.

4> Paid monthly rent.

5> Paid dividends.

Answer: