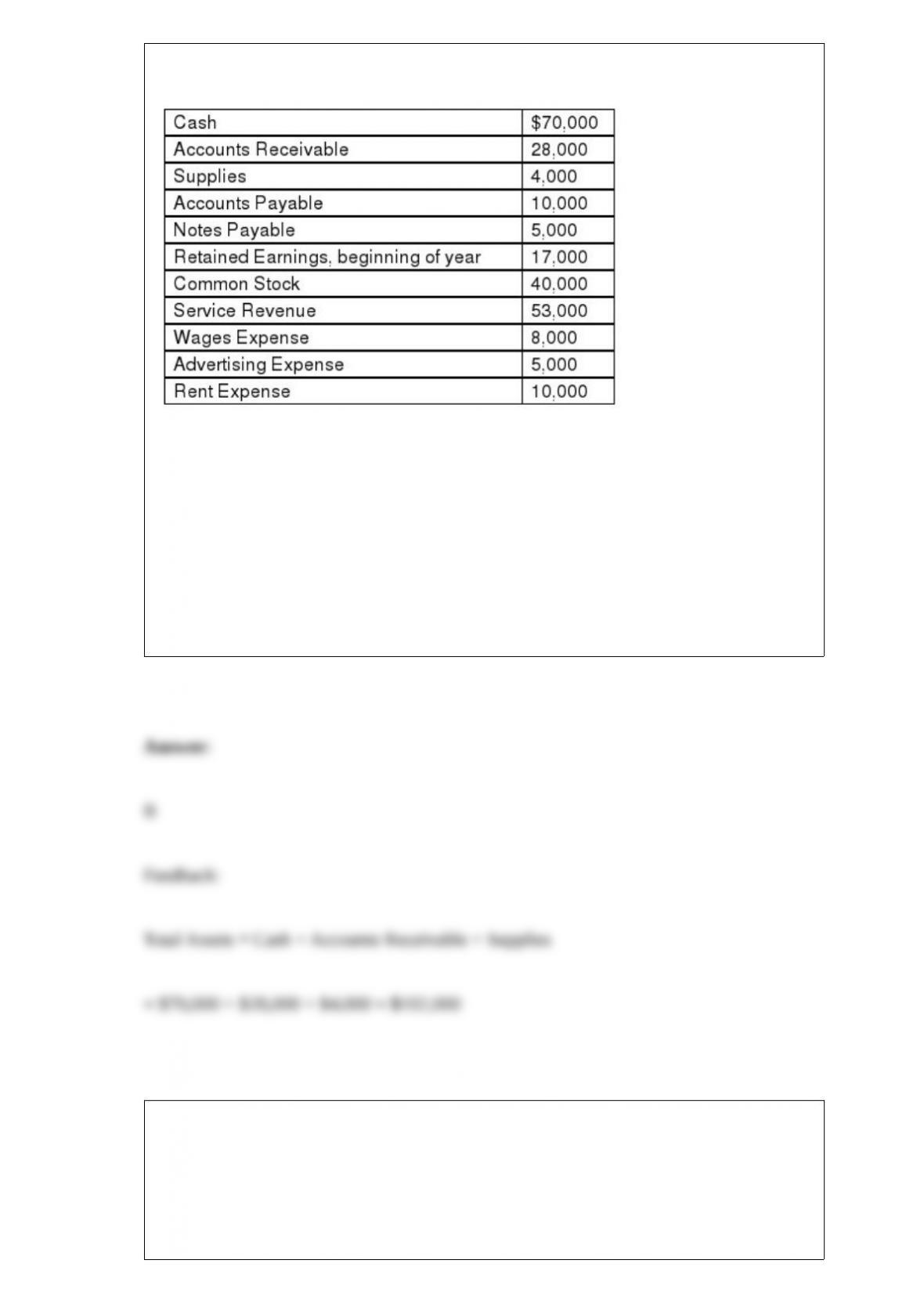

A company’s financial records at the end of the year including the following amounts:

Use the information above to answer the following question. What is the amount of

total assets to be reported on the balance sheet at the end of the year?

A) $112,000.

B) $102,000.

C) $119,000.

D) $155,000.

The carrying value of a long-lived asset is referred to as its:

A) residual value.

B) book value.

C) market value.

D) sales value.

Which of the following is an activity common to the operations of merchandising,

manufacturing, and service companies?

A) Producing the product

B) Incurring operating expenses

C) Buying goods or raw materials

D) Selling a physical product

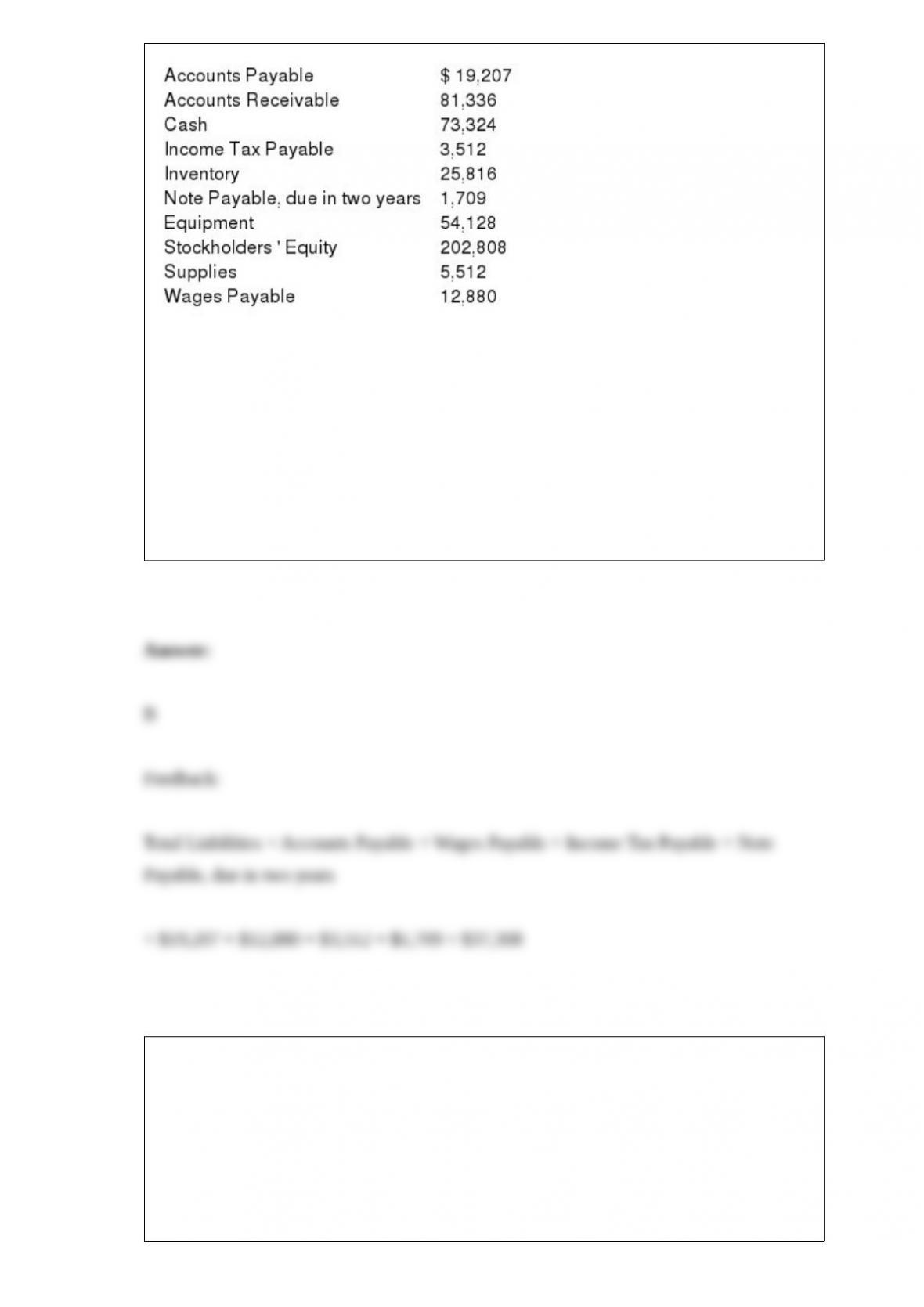

A company ‘s trial balance included the following account balances:

Use the information above to answer the following question. What is the amount of

Total Liabilities on the Balance Sheet?

A) $240,116.

B) $37,308.

C) $35,599.

D) $20,916.

The account entitled Premium on Bonds Payable:

A) increases when amortization entries are made.

B) appears on the balance sheet of the issuer as a deduction from bonds payable.

C) decreases when amortization entries are made and its balance is equal to zero at the

maturity date of the bond.

D) is a contra account with a normal debit balance.

McEnroe Inc. has outstanding 10 million shares of $2 par value common stock and 1

million shares of $4 par value preferred stock. The preferred stock has a 7% cumulative

dividend preference. The company declares total dividends amounting to $50,000,

$250,000, and $600,000 during 2015, 2016, and 2017, respectively.

Required:

Part a. Compute the amount of dividends to be distributed to preferred and common

shareholders during 2015.

Part b. Compute the amount of dividends to be distributed to preferred and common

shareholders during 2016.

Part c. Compute the amount of dividends to be distributed to preferred and common

shareholders during 2017.

Which one of the following statements about amortization of discounts and premiums is

not correct?

A) Under straight-line amortization, when a bond is sold at a premium, the annual

premium amortization is the total premium divided by the number of years until bond

maturity.

B) When a bond is sold at a discount, interest expense recorded using the

effective-interest method is less than the interest paid on the bond.

C) The effective-interest method of amortization is considered to be conceptually

superior to straight-line amortization.

D) When a bond discount is amortized using the effective-interest method, the promised

interest payment is less than the interest expense, so the bond liability will increase as a

result of the contra-liability account decreasing.

A one-time error in the application of the lower of cost or market (LCM) rule in the

current period distorts financial results for the current accounting period:

A) only.

B) and the period before.

C) and the period after.

D) and all periods after.

Cash flows from (used in) investing activities includes amounts:

A) received from a company’s stockholders for the sale of stock.

B) received from the sale of the company’s office building.

C) paid for dividends to the company’s stockholders.

D) paid for salaries of employees.

Cash flows from financing activities include all of the following except:

A) payment of long-term debt.

B) payment of interest.

C) proceeds from stock issuance.

D) cash dividends paid.

A corporation had 50,000 shares of $20 par value common stock outstanding. The

board of directors declared and issued a 50% stock dividend. The market value of the

stock was $27 per share. What is the journal entry to record this stock dividend?

A) Debit Retained Earnings and credit Common Stock for $675,000

B) Debit Retained Earnings and credit Common Stock for $500,000

C) Debit Retained Earnings and credit Cash for $675,000

D) No entry is made to record the stock dividend.

When the allowance method is used, the entry to record the write-off of specific

uncollectible accounts would decrease:

A) the Allowance for Doubtful Accounts account.

B) Net Income.

C) Accounts Receivable, Net.

D) Bad Debt Expense.

Which of the following statements about an adjusted trial balance is correct?

A) Debits should equal credits both before and after adjustments are made.

B) Debits will equal credits after adjustments are made but not necessarily before.

C) Debits will equal credits before adjustments are made but not necessarily after.

D) Debits do not have to equal credits in the adjusted trial balance but they must be

equal in the post-closing trial balance.

A company incurred $5,000 in wages for employees for the year. Of these wages,

$4,500 was paid by the end of the year. Which of the following statements is correct?

A) Salaries and Wages Payable on the income statement will be $4,500.

B) Salaries and Wages Expense on the income statement will be $500.

C) Salaries and Wages Expense on the balance sheet will be $5,000.

D) Salaries and Wages Payable on the balance sheet will be $500.

Plasma Inc. uses the percentage of credit sales method to estimate Bad Debt Expense.

The company reported net credit sales of $500,000 during the year. Plasma has

experienced bad debt losses of 2% of credit sales in prior periods. At the beginning of

the year, Plasma has a credit balance in its Allowance for Doubtful Accounts of $4,000.

No write-offs or recoveries were recorded during the year. What amount of Bad Debt

Expense should Plasma recognize for the year?

A) $4,000

B) $6,000

C) $10,000

D) $14,000

Amiable Inc. uses a perpetual inventory system. The following transactions took place

during the month of August:

If Amiable uses the LIFO method, what is the ending inventory at August 31?

A.$496.00

B.$486.00

C.$492.57

D.$300.00

E.$510.00

Which of the following statements about loan terminology is correct?

A) Loan covenants are the collateral provided by a borrower to a lender as security on a

loan.

B) A secured loan means that the borrower has a pre-approved line of credit backing the

debt.

C) Lenders can revise loan terms if a borrower violates a loan covenant.

D) All companies are able to establish lines of credit which will allow them to borrow

money as needed, up to a prearranged limit.

Special items reported as part of comprehensive income, but not included in net

income, might include:

A) gains or losses on foreign currency exchange.

B) interest expense.

C) extraordinary gains and losses.

D) income tax expense.