Capital structure refers to a company’s long-run financial viability and its ability to

cover long-term obligations.

Planning is defining an organization’s ideas, goals, and actions.

On the date of the record the journal entry to record $10,000 in dividends is a debit to

Common Dividends Payable and a credit to Cash.

One difference between financial and managerial accounting is that the external users

that use financial information must plan a company’s future, but the internal users of

managerial accounting information generally must decide whether to invest in or lend

to a company.

A common rule of thumb is that a company’s acid-test ratio should be at least 2 or a

company may face near-term liquidity problems.

Asset accounts normally have credit balances and revenue accounts normally have debit

balances.

Basic bank services such as bank accounts, bank deposits, and checking contribute to

the control and safeguarding of cash.

An accelerated depreciation method yields smaller depreciation expense in the early

years of an asset’s life and larger depreciation expense in later years.

The three common forms of business ownership include sole proprietorship,

partnership, and non-profit.

The net method for recording purchases records the purchase invoice at its net amount

of any cash discount.

A contra account is an account linked with another account; it is added to that account

to show the proper amount for the item recorded in the associated account.

Since pledged accounts receivables only serve as collateral for a loan and are not sold,

it is not necessary to disclose the pledging.

The cost of developing, maintaining, or enhancing the value of a trademark is always

added to the value of the asset when incurred.

A company has current assets of $15,000 and current liabilities of $9,500. Its current

ratio is 1.6

A company has $595,000 in total stockholders’ equity. Preferred stock outstanding is

valued at $150,000, and 75,000 shares of common stock are outstanding. Its book value

per common share is $7.93.

The Sarbanes-Oxley Act (SOX) requires each issuer of securities to disclose whether is

has adopted a code of ethics for its senior financial officers and the contents of that

code.

Companies follow both the matching principle and the materiality constraint when

applying the direct write-off method.

Net assets always increase when revenue is recorded.

Companies promoting continuous improvement strive to achieve practical standards

rather than ideal standards.

Accounting is an information and measurement system that identifies, records, and

communicates relevant, reliable, and comparable formation about an organization’s

business activities.

The assignment of costs to the cost of goods sold and to ending inventory using FIFO is

the same for both the perpetual and periodic inventory systems.

The consistency concept prescribes that a company use the same accounting methods

period after period, so that financial statements are comparable across periods.

A special journal is used to record and post transactions of a similar type.

A company’s file of job cost sheets for finished but unsold jobs equals the balance in the

Finished Goods Inventory account.

An owner’s investment in a business always creates an asset (cash), a liability (note

payable), and owner’s equity (investment.)

Net income for a period will be overstated if accrued salaries are not recorded at the end

of the accounting period.

A process cost summary is an accounting report that describes the costs charged to a

department, the equivalent units of production by the department, and how the costs

were assigned to the output.

The cash flow on total assets ratio is defined as average total assets divided by

operating income.

Direct costs must be allocated across departments.

A perpetual inventory system requires updating of the inventory account only at the

beginning of an accounting period.

A joint cost of producing two products can be allocated between those products on the

basis of the relative physical quantities of each product produced.

The Factory Overhead account will have a credit balance at the end of a period if

overhead applied during the period is greater than the overhead incurred.

A company borrowed $10,000 by signing a 180-day promissory note at 11%. The total

interest due on the maturity date is.

A.$50

B.$275

C.$550

D.$825

E.$1,100

A machine originally had an estimated useful life of 5 years, but after 3 complete years,

it was decided that the original estimate of useful life should have been 10 years. At that

point the remaining cost to be depreciated should be allocated over the remaining:

A.2 years.

B.5 years.

C.7 years.

D.8 years.

E.10 years.

Internal controls that should be applied when a business takes a physical count of

inventory should include

A.Prenumbered inventory tickets.

B.Counters of inventory should not be those who are responsible for the inventory.

C.Counters must confirm the validity of inventory existence, amounts, and quality.

D.Second counts by a different counter.

E.All of these.

The Premium on Bonds Payable account is a(n):

A.Revenue account.

B.Adjunct or accretion liability account.

C.Contra revenue account.

D.Asset account.

E.Contra expense account.

A company’s flexible budget for 12,000 units of production showed sales, $48,000;

variable costs, $18,000; and fixed costs, $16,000. The operating income expected if the

company produces and sells 16,000 units is:

A.$ 2,667.

B.$14,000.

C.$18,667.

D.$24,000.

E.$35,000.

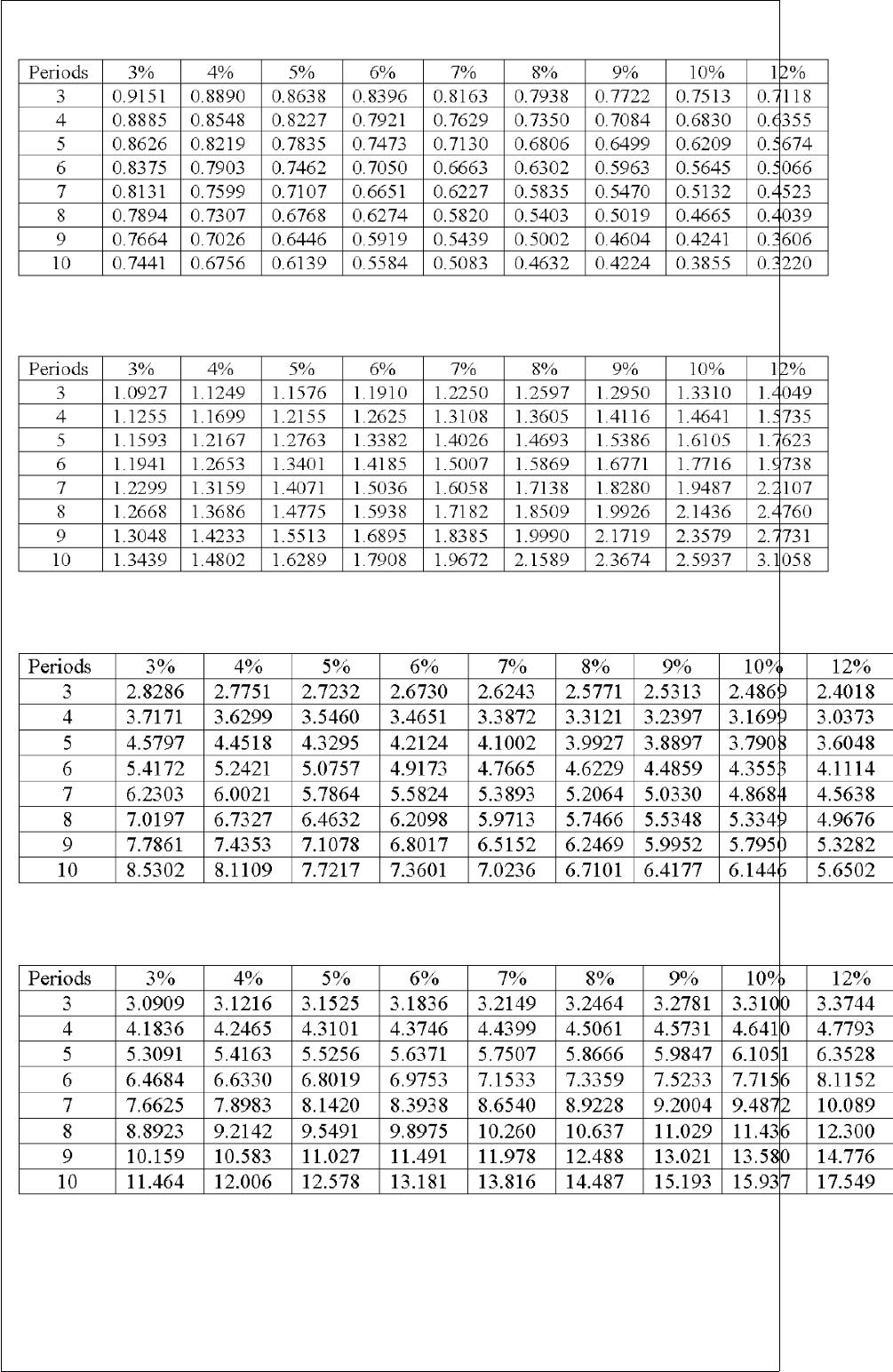

Present Value of 1

Future Value of 1

Present Value of an Annuity of 1

Future Value of an Annuity of 1

An individual is planning to set-up an education fund for her children. She plans to

invest $10,000 annually at the end of each year. She expects to withdraw money from

the fund at the end of 10 years and expects to earn an annual return of 8%. What will be

the total value of the fund at the end of 10 years?

A.$ 46,320.

B.$ 67,107.

C.$100,000.

D.$144,870.

E.$215,890.

Reebok had income of $150 million and average invested assets of $1,800 million. Its

return on assets is:

A.8.3%.

B.83.3%.

C.12%.

D.120%.

E.16.7%.

Endor Fishing Company exchanged an old boat for a new one. The old boat had a cost

of $260,000 and accumulated depreciation of $200,000. The new boat had an invoice

price of $400,000. Endor received a trade in allowance of $100,000 on the old boat,

which meant the company paid $300,000 in addition to the old boat to acquire the new

boat. If this transaction lacks commercial substance, what amount of gain or loss should

be recorded on this exchange?

A.$0 gain or loss.

B.$40,000 gain.

C.$40,000 loss.

D.$60,000 loss

E.$100,000 loss.

A financial statement analysis report usually includes:

A.An executive summary.

B.An analysis overview.

C.Evidential matter.

D.Assumptions.

E.All of these.

Another name for temporary accounts is:

A.Real accounts.

B.Contra accounts.

C.Accrued accounts.

D.Balance column accounts.

E.Nominal accounts.

Which of the following statements about budgeting is false?

A.Budgeting is an aid to planning and control.

B.Budgets create standards for performance evaluation.

C.Budgets help coordinate the activities of the entire organization.

D.Budgeting forces managers to think ahead and formalize long-range objectives.

E.The master budget should only be prepared by top management.

A company is considering purchasing a machine for $21,000. The machine will

generate an after-tax net income of $2,000 per year. Annual depreciation expense would

be $1,500. What is the payback period for the new machine?

A.4 years.

B.6 years.

C.10.5 years.

D.14 years.

E.42 years.

Cost of goods sold:

A.Is another term for merchandise sales.

B.Is the term used for the cost of buying and preparing merchandise for sale.

C.Is another term for revenue.

D.Is also called gross margin.

E.Is a term only used by service firms.

Contingent liabilities must be recorded if:

A.The future event is probable and the amount owed can be reasonably estimated.

B.The future event is remote.

C.The future event is reasonably possible.

D.The amount owed cannot be reasonably estimated.

E.All of these.

A method of estimating bad debts expense that involves a detailed examination of

outstanding accounts and their length of time past due is the:

A.Direct write-off method.

B.Aging of accounts receivable method.

C.Percentage of sales method.

D.Aging of investments method.

E.Percent of accounts receivable method.

The accounting principle that requires an accounting information system to report

useful, understandable, timely, and pertinent information for effective decision-making

is the:

A.Control principle.

B.Compatibility principle.

C.Relevance principle.

D.Flexibility principle.

E.Cost-Benefit principle.

A company is considering the purchase of a new machine for $48,000. Management

predicts that the machine can produce sales of $16,000 each year for the next 10 years.

Expenses are expected to include direct materials, direct labor, and factory overhead

totaling $8,000 per year plus depreciation of $4,000 per year. The company’s tax rate is

40%. What is the payback period for the new machine?

A.3.0 years.

B.6.0 years.

C.7.5 years.

D.12.0 years.

E.20.0 years.

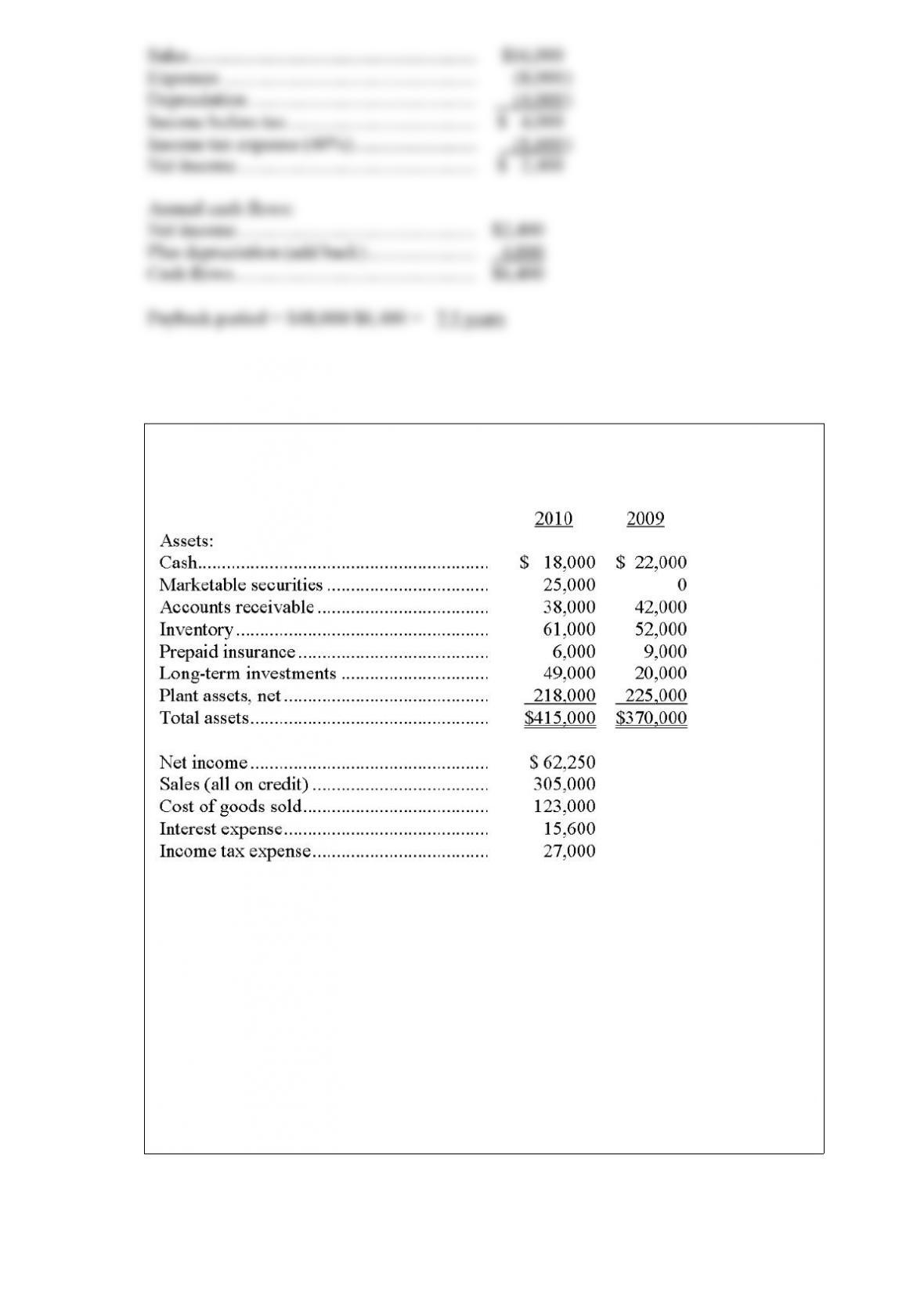

The following information is from Omega Corporation’s balance sheets as of December

31, 2009, and 2010 and its income statement for 2010:

From the above information, calculate the following ratios for 2010:

(a) Inventory turnover.

(b) Accounts receivable turnover.

(c) Return on total assets.

(d) Times interest earned.

(e) Total asset turnover.

A report that lists accounts and their balances, in which the total debit balances should

equal the total credit balances, is called a(n):

A.Account balance.

B.Trial balance.

C.Ledger.

D.Chart of accounts.

E.General Journal.

The costs that should be incurred under normal conditions to produce a specific product

or component or to perform a specific service are:

A.Variable costs.

B.Fixed costs.

C.Standard costs.

D.Product costs.

E.Period costs.

Credit card expense may be classified as:

A. A “discount” deducted from sales to get net sales.

B. A selling expense.

C. An administrative expense.

D. All of these.

E. Only A and B.

The statement of owner’s equity:

A.Reports how equity changes at a point in time.

B.Reports how equity changes over a period of time.

C.Reports on cash flows for operating, financing, and investing activities over a period

of time.

D.Reports on cash flows for operating, financing, and investing activities at a point in

time.

E.Reports on amounts for assets, liabilities, and equity at a point in time.

Labor costs that are clearly associated with specific units or batches of product because

the labor is used to convert raw materials into finished products called are:

A.Sunk labor.

B.Direct labor.

C.Indirect labor.

D.Finished labor.

E.All of these.

In cost-volume-profit analysis, the unit contribution margin is:

A.Sales price per unit less cost of goods sold per unit.

B.Sales price per unit less unit fixed cost per unit .

C.Sales price per unit less total variable cost per unit .

D.Sales price per unit less unit total cost per unit.

E.The same as the contribution margin ratio.

Match each of the following terms with the appropriate definitions.

1)Principal of a note

2)Full disclosure principle

3)Factor

4)Accounts receivable turnover

5)Materiality constraint

6)Allowance method

7)Maker of a note

8)Installment accounts receivable

9)Dishonoring a note

10)Direct write-off

A) A method of accounting for bad debts that matches the estimated loss from

uncollectible accounts receivable against the sales they helped to produce.

B)Amounts owed by customers from credit sales for which payment is required in

periodic payments over an extended period of time.

C) The amount that the signer of a note agrees to pay back when the note matures, not

including interest.

D) The accounting principle that requires the financial statements (including the notes)

to report all relevant information about operations and financial condition.

E)The accounting constraint that states that an amount can be ignored if its effect on the

financial statements is unimportant to their users.

F)A method of accounting for bad debts that records the loss from an uncollectible

account receivable when it is determined to be uncollectible.

G) Refers to a note maker’s inability or refusal to pay the note at maturity.

H)A measure of both the quality and liquidity of accounts receivable. It indicates how

often, on average, receivables are received and collected during the period.

I)A buyer of accounts receivable who charges the seller a fee and then receives cash

from the receivables as they come due.

J) One who signs a note and promises to pay it at maturity.

You are reviewing the accounting records of Cathy’s Antiques, owned by Cathy Miller.

You have uncovered the following situations. Compose a memo to Ms. Miller. Cite the

appropriate accounting principle and suggest an action for each separate item.

1) In August, a check for $500 was written to Wee Day Care Center. This amount

represents child care for her son Brandon.

2) Cathy plans a Going Out of Business Sale for May, since she will be closing her

business for a month-long vacation in June. She plans to reopen July 1 and will

continue operating Cathy’s Antiques indefinitely.

3) Cathy received a shipment of pine furniture from Quebec, Canada. The invoice was

stated in Canadian dollars.

4) Joseph Clark paid $1,500 for a dining table. The amount was recorded as revenue.

The table will be delivered to Mr. Clark in six weeks.

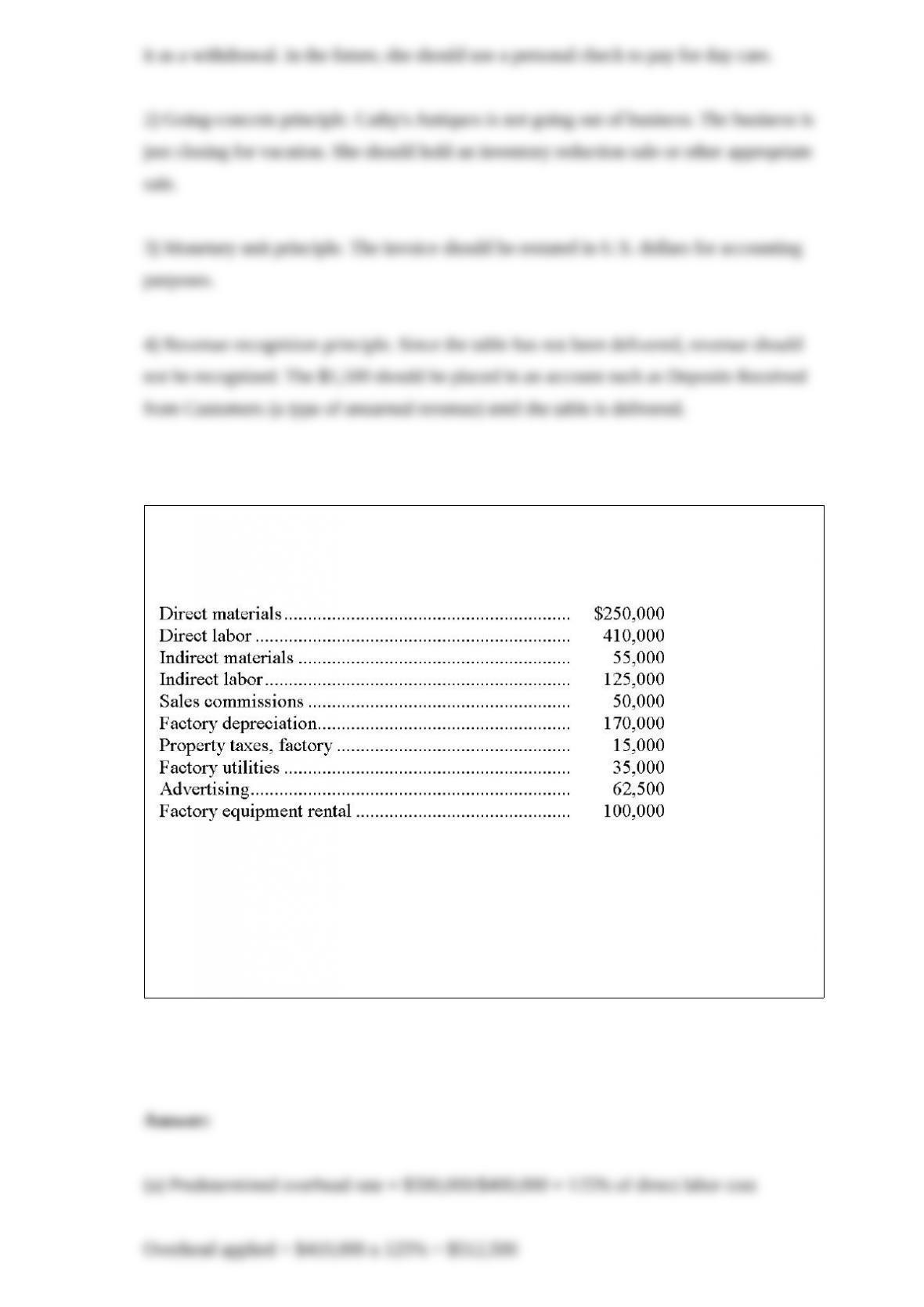

The predetermined overhead allocation rate for Forsythe, Inc., is based on estimated

direct labor costs of $400,000 and estimated factory overhead of $500,000. Actual costs

incurred were:

(a) Calculate the predetermined overhead rate and calculate the overhead applied during

the year.

(b) Determine the amount of over- or underapplied overhead and prepare the journal

entry to eliminate the over- or underapplied overhead assuming that it is not material in

amount.

The appropriate section in the statement of cash flows for reporting the purchase of

equipment for cash is:

A.Operating activities.

B.Financing activities.

C.Investing activities.

D.Schedule of noncash investing or financing activity.

E.None of these. This is not reported on the statement of cash flows.

Accounting for long-term investments in equity securities with controlling influence

uses the:

A.Controlling method.

B.Equity method with consolidation.

C.Investor method.

D.Investment method.

E.Consolidated method.

Revenues, expenses, withdrawals, and Income Summary are called

_________________ accounts because they are closed at the end of each accounting

period.

Companies with many employees often use a special ____________________ account

to pay employees.

The _____________________ principle requires that companies report the amount of

accumulated depreciation on plant assets as well as the depreciation methods used to

determine the annual depreciation expense.

_______________ refers to the expected proceeds from converting an asset into cash.

A partner can be admitted into a partnership by ________________________ or by

______________________________.

The _____________________ method of assigning costs to inventory and cost of

goods sold assumes that the inventory items are sold in the order acquired.

On January 1, a machine costing $260,000 with a 4-year life and an estimated $5,000

salvage value was purchased. It was also estimated that the machine would produce

500,000 units during its life. The actual units produced during its first year of operation

were 110,000. Determine the amount of depreciation expense for the first year under

each of the following assumptions:

1) The company uses the straight-line method of depreciation.

2) The company uses the units-of-production method of depreciation.

3) The company uses the double-declining-balance method of depreciation.

Pastimes Co. offers its employees a bonus equal to 2% of the company’s net income.

The estimated net income for the year is expected to be $850,000. Prepare the general

journal entry to record the employee bonus plan expense.

An internal control system refers to the policies and procedures managers use to

__________, ensure reliable accounting, promote efficient operations, and urge

adherence to company policies.

Policies and procedures used by management to monitor and control business activities

are known as ____________________________.

Explain the difference between a ledger and a chart of accounts.

Briefly describe the process by which budgets are developed and administered.