Underapplied overhead occurs when the balance in the Manufacturing Overhead

Control account is:

A. greater than the balance in the Applied Manufacturing Overhead account.

B. equal to the balance in the Applied Manufacturing Overhead account.

C. less than the balance in the Applied Manufacturing Overhead account.

D. less than the balance in the Finished Goods Inventory account.

Answer:

Which of the following approaches allocates overhead by multiplying an actual

overhead rate xactual activity?

A. Actual costing

B. Normal costing

C. Regression costing

D. Standard costing

Answer:

The number of units required for production is equal to

A. budgeted sales plus units in the beginning inventory minus the units in the ending

inventory.

B. budgeted sales plus units in the ending inventory minus the units in the beginning

inventory.

C. budgeted sales plus the units in the ending inventory.

D. budgeted sales minus the units in the beginning inventory.

E. budgeted sales.

Answer:

In the computation of the manufacturing cost per equivalent unit, the weighted average

method of process costing considers

A. current costs only.

B. current costs plus cost of beginning Work-in-Process Inventory.

C. current costs plus cost of ending Work-in-Process Inventory.

D. current costs less cost of beginning Work-in-Process Inventory.

Answer:

An operating unit that is responsible for revenues and costs is commonly referred to as

a(n)

A. expense center.

B. revenue center.

C. profit center.

D. asset center.

Answer:

The basic cost flow model is:

A. EB + BB = TI + TO

B. BB + EB = TI + TO

C. EB – BB = TI – TO

D. EB – BB = TO – TI

E. BB -EB = TI

Answer:

One feature of a standard cost system is that it

A. makes the record keeping process more complex and difficult.

B. never requires updating if standard costs have been carefully determined.

C. reduces the amount of information available to a manager.

D. simplifies the record keeping process by allowing amounts to be carried at standard

cost rather than actual cost in the accounting records.

Answer:

A subjective performance measure is one where

A. different people will agree as to the appropriateness of a measure.

B. different people will agree as to the method to calculate the measure.

C. different managers will calculate a measure the same.

D. different managers will view the facts and come to different conclusion.

Answer:

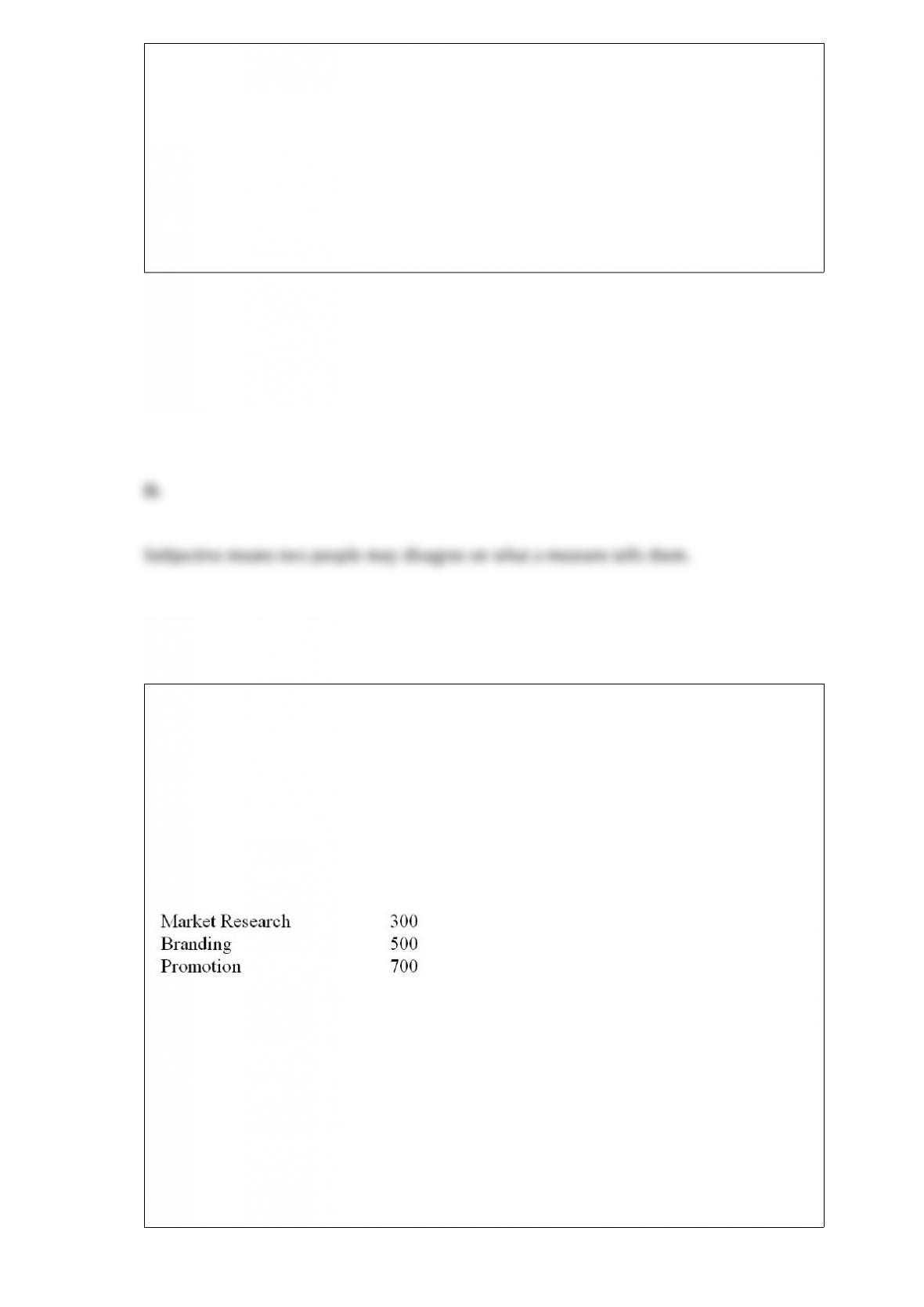

The Black Swan Company has three client-contact departments: Market Research,

Branding, and Promotion. Each department requires the services of the Legal

Department for the contracts that each undertakes. The size of the Legal Department

was based on long-run estimates of contracts. Information on the Legal Department’s

budgeted and actual costs is as follows:

The budget for the Legal Dept is $200,000 + $7.50/contract. The budgeted volume of

contracts is as follows:

The actual number of contracts for Market Research was 286, for Branding was 450,

and for Promotion was 675.

Required (use three decimal places in your calculations):

a) If a single charging rate based on budgeted usage is used, how much of the cost of

the Legal Department would be allocated to each of the producing departments?

b) If a dual charging rate is used, how much of the cost of the Legal Department would

be allocated to each of the producing departments

Answer:

The Super Supply Company manufactures cleaning spray for public schools. During

2010, the company spent $600,000 on prime costs and $800,000 on conversion costs.

Overhead is applied at a rate of 150% of direct labor costs. How much did the company

allocate for manufacturing overhead during 2010?

A. $480,000

B. $360,000

C. $320,000

D. $300,000

Answer:

Which of the following statements is (are) true?

(A) If variances are prorated at the end of the accounting period, an unfavorable direct

materials price variance will, when prorated, increase the value of the Finished Goods

Inventory.

(B) Insignificant variances are not generally prorated at the end of the accounting

period and are closed to the Cost of Goods Sold.

A. Only A is true.

B. Only B is true.

C. Both A and B are true.

D. Neither A nor B is true.

Answer:

Which of the following departments is not a service department in a typical

manufacturing company?

A. Assembly

B. Accounting

C. Human resources

D. Information processing

Answer:

The sales price variance is the difference between the actual sales revenues and the

A. budgeted selling price multiplied by the budgeted number of units sold.

B. budgeted selling price multiplied by the actual number of units sold.

C. actual selling price multiplied by the budgeted number of units sold.

D. actual selling price multiplied by the actual number of units sold.

Answer:

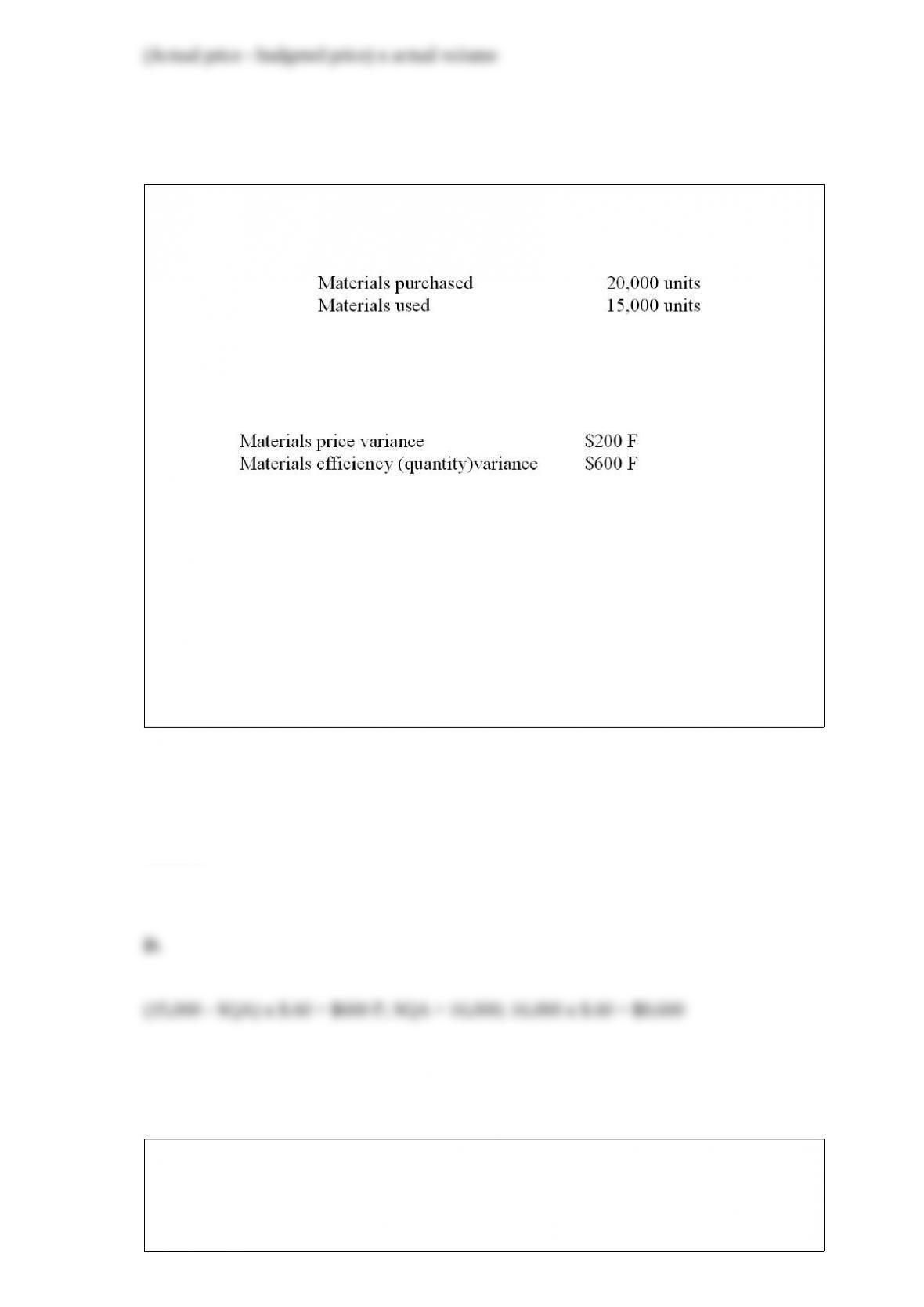

The Heavenly Gifts Company, a maker of Holiday novelties, needs your help

immediately. The company’s accountant resigned without leaving adequate records or

explanations for what she did. In reviewing the records, you find the following

information for May:

You find a copy of the budget which shows that materials were budgeted at $0.60/unit.

You know that the materials price variance is recorded at the time of purchase and you

find some handwritten notes among the accountant’s work papers, which indicate the

following:

What was the total standard cost of direct materials allowed during May?

A. $8,260

B. $8,400

C. $9,440

D. $9,600

Answer:

The Task Company is to begin operations in April. They have budgeted April sales of

$30,000. May sales of $34,000, June sales of $40,000, July sales of $42,000, and

August sales of $38,000. 10% of each month’s sales will represent cash sales; 75% of

the balance will be collected in the month following the sale, 17% the second month,

6% the third month and the balance is bad debts.

What is the amount of cash to be collected in the month of August?

A. $40,106

B. $40,340

C. $38,036

D. $44,140

Answer:

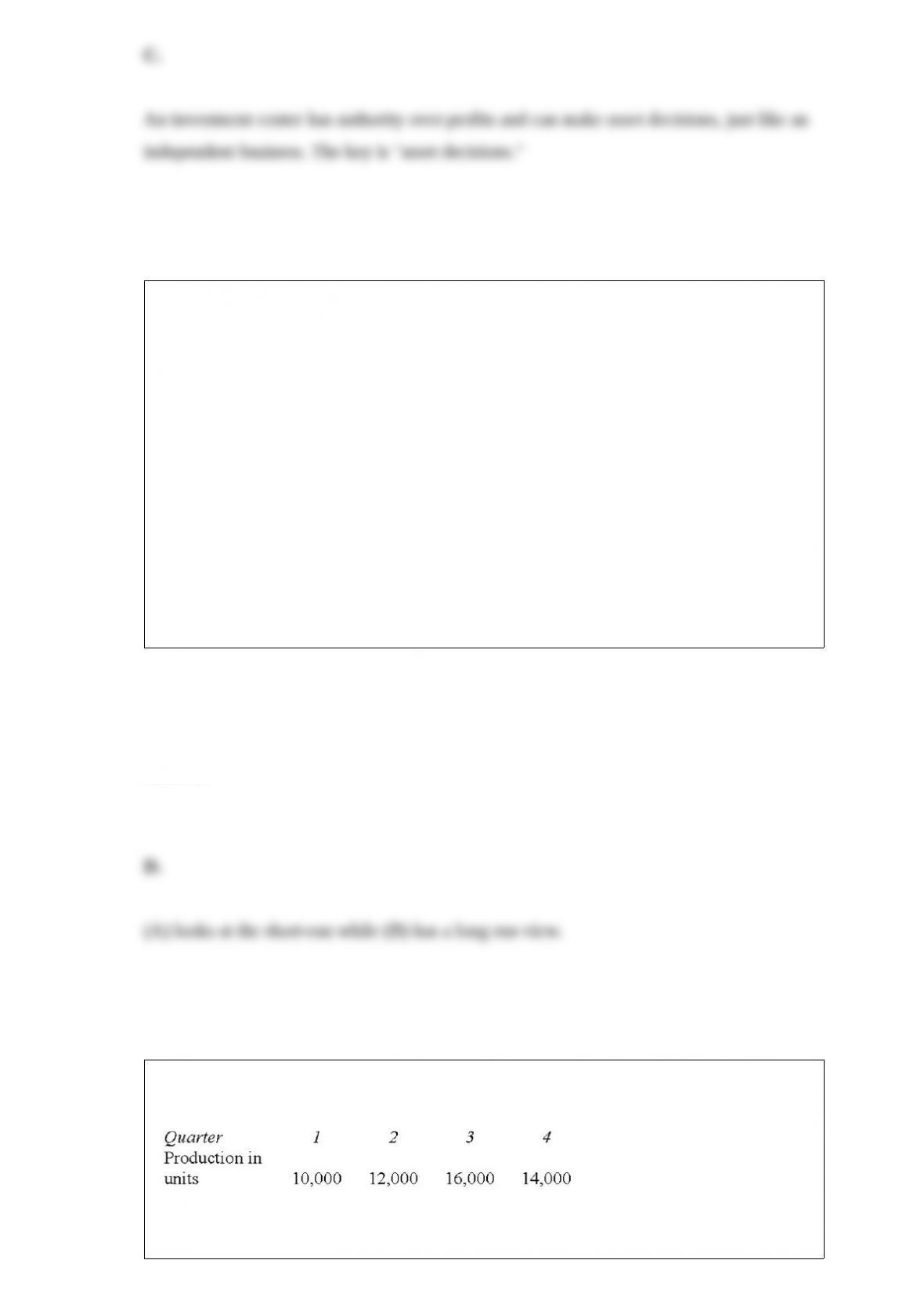

Decentralized organizations can delegate authority and still maintain control and

monitor managers’ performance by designing appropriate management control systems.

Which of the following responsibility centers would be evaluated similar to an

independent business?

A. profit center

B. revenue center

C. investment center

D. discretionary cost center

Answer:

Which of the following statements regarding special orders is (are) true?

(A) The primary decision for special orders is determining whether the differential

revenue is greater than the differential costs associated with the order.

(B) The differential analysis approach to pricing for special orders could lead to

underpricing in the long-run because fixed costs are not included in the analysis.

A. Only A.

B. Only B.

C. Neither A nor B is false.

D. Both A and B are true.

Answer:

The Tobler Company had budgeted production for the year as follows:

Four pounds of raw materials are required for each unit produced. Raw materials on

hand at the start of the year total 4,000 lbs. The raw materials inventory at the end of

each quarter should equal 10% of the next quarter’s production needs in materials.

Budgeted purchases of raw materials in the second quarter would be (in lbs.)

A. 48,000 lbs.

B. 46,400 lbs.

C. 49,600 lbs.

D. 54,400 lbs.

Answer:

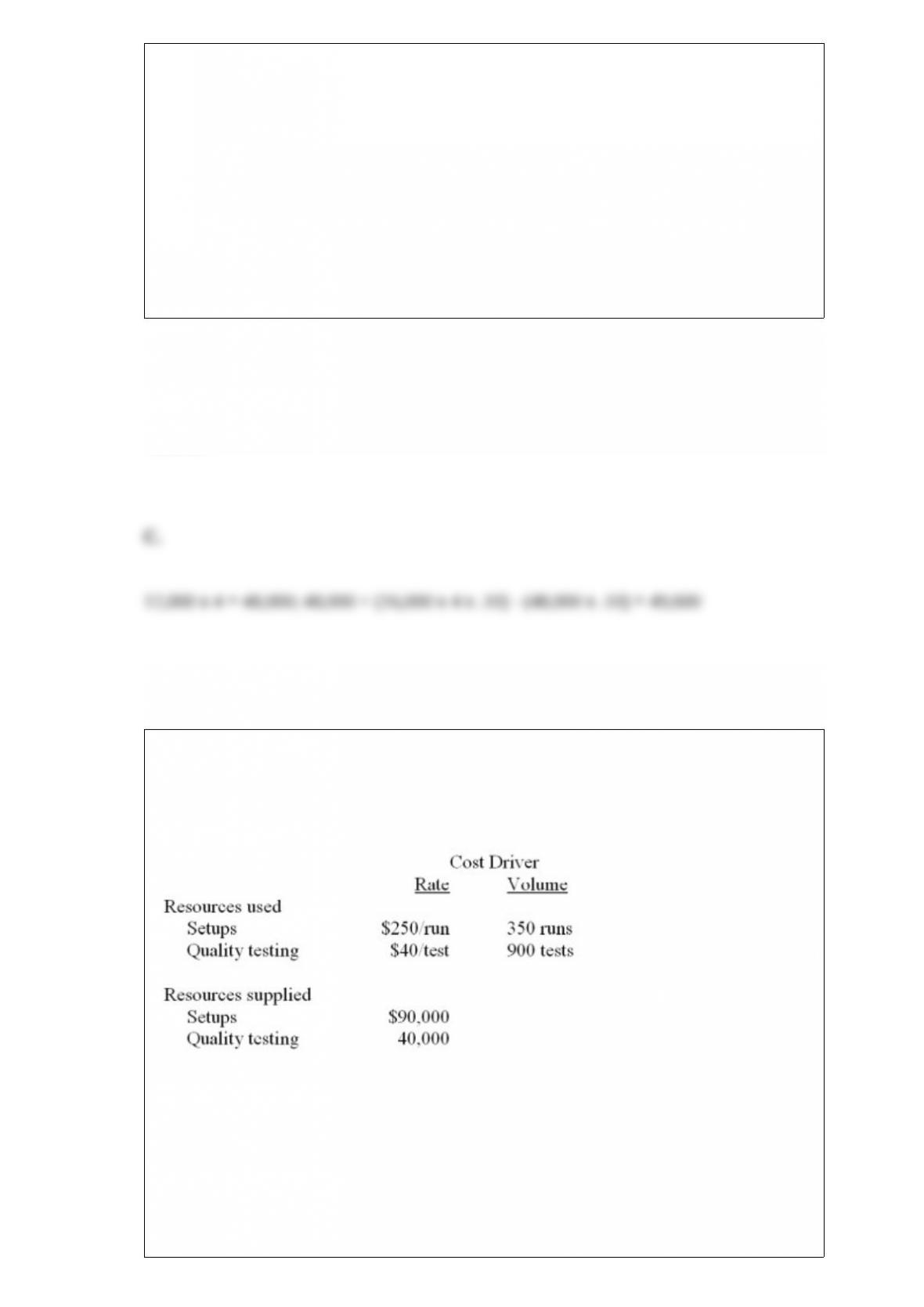

Demers Products reports the following information about resources. At the beginning

of the year, Demers estimated it would spend $84,000 for setups and $41,000 for

quality testing.

Compute unused resource capacity for setups for Demers Products.

A. $6,000

B. $2,500

C. $1,000

D. $3,500

Answer:

Which of the following approaches allocates overhead by multiplying a predetermined

overhead rate xactual activity?

A. Actual costing

B. Normal costing

C. Regression costing

D. Standard costing

Answer:

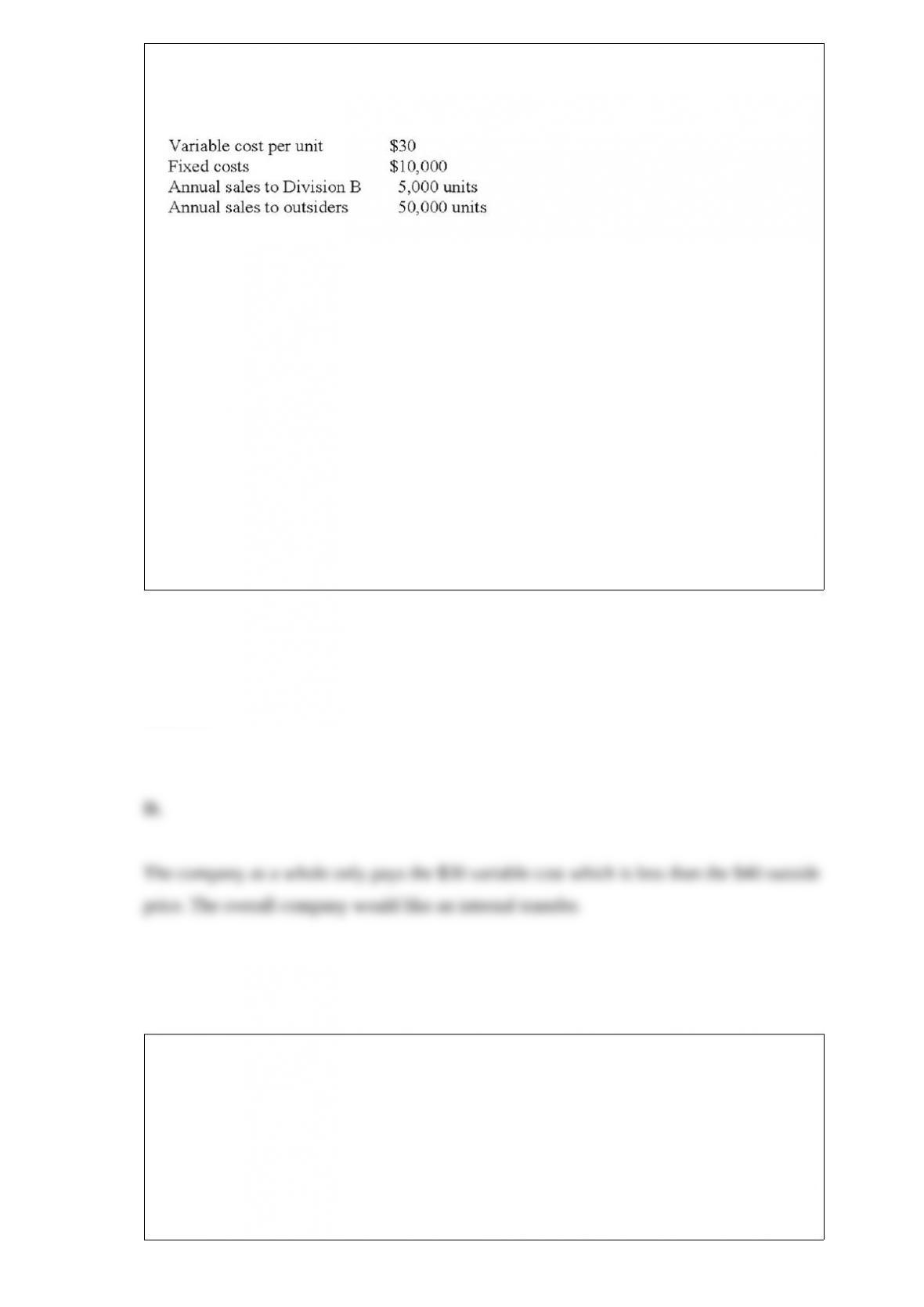

A company has two divisions, A and B, each operated as a profit center. Division A

charges Division B $35 per unit (for each unit transferred to Division B). Other data for

Division A are as follows:

Division A is planning to raise its transfer price to $50 per unit. Division B can purchase

units at $40 per unit from outsiders, but doing so would idle Division A’s facilities (now

committed to producing units for Division B), Division A cannot increase its sales to

outsiders. From the perspective of the company as a whole, from who should Division

B acquire the units, assuming Division B’s market is unaffected?

A. Outside vendors.

B. Division A, but only at the variable cost per unit.

C. Division A, but only until fixed costs are covered, then should purchase from outside

vendors.

D. Division A, in spite of the increased transfer price.

Answer:

Which one of the following variances is of least significance from a behavioral control

perspective? (CMA adapted)

A. Unfavorable materials quantity variance amounting to 20% of the quantity allowed

for the output attained.

B. Unfavorable labor efficiency variance amounting to 10% more than the budgeted

hours for the output attained.

C. Favorable materials price variance obtained by purchasing raw materials from a new

vendor.

D. Fixed factory overhead volume variance resulting from management’s decision

midway through the fiscal year to reduce its budgeted output by 20%.

Answer:

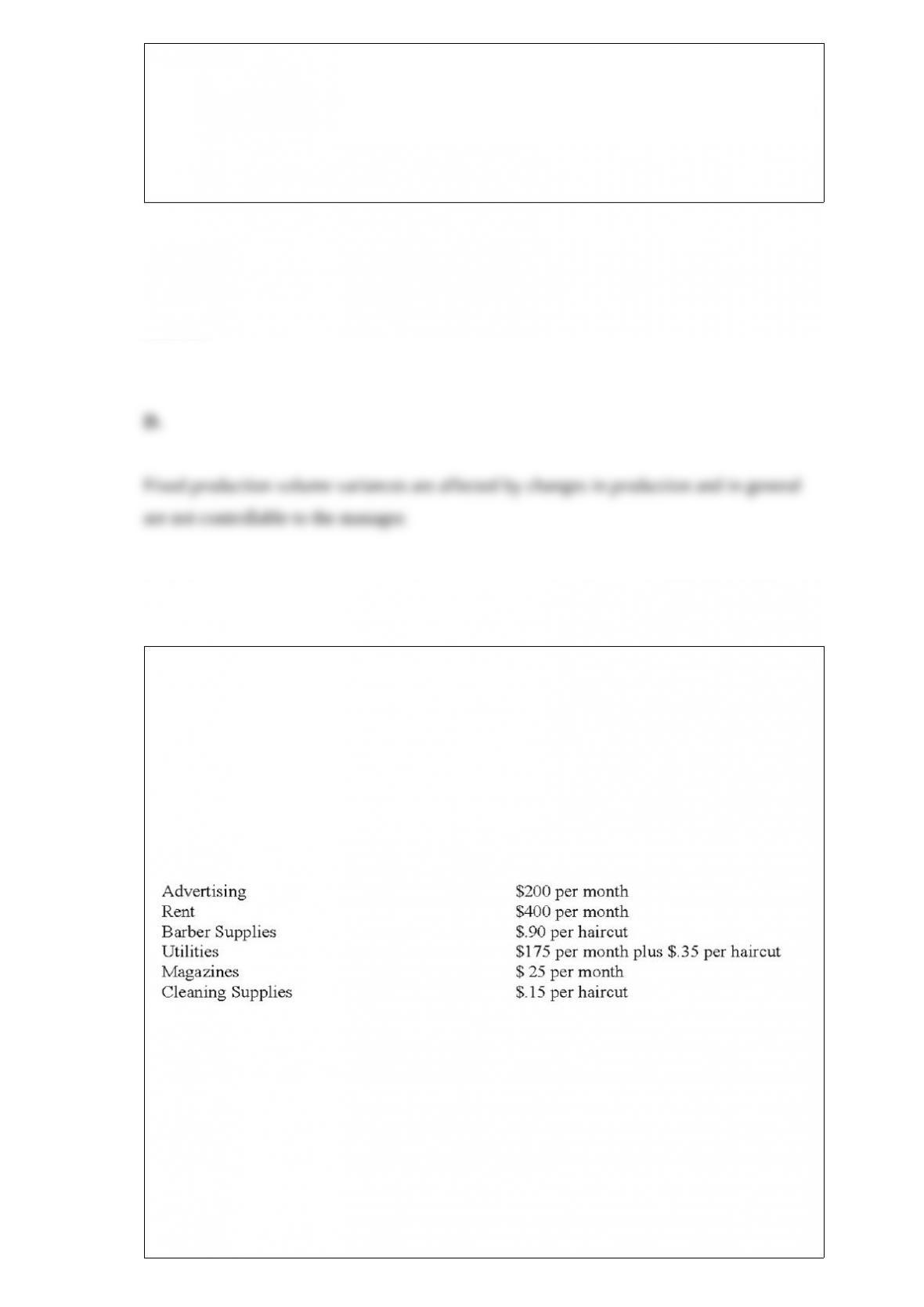

Stanley Clipper, now retired, owns the Campus Barber Shop. He employs five (5)

barbers and pays each a base rate of $500 per month. One of the barbers serves as the

manager and receives an extra $300 per month. In addition to the base rate, each barber

also receives a commission of $3 per haircut. A barber can do as many as 20 haircuts a

day, but the average is 14 haircuts per day. The Campus Barber Shop is open 24 days a

month. You can safely ignore income taxes.

Other costs are incurred as follows:

Stanley currently charges $8 per haircut.

Required:

(a) Compute the break-even point in (1) number of haircuts, (2) total sales dollars, and

(3) as a percentage of capacity.

(b) In March, 1,400 haircuts were given. Compute the operating profits for the month.

(c) Stanley wants a $2,160 operating profit in April. Compute the number of haircuts

that must be given in order to achieve this goal.

(d) If 1,500 haircuts are given in April, compute the selling price that would have to be

charged in order to have $2,160 in operating profits.

Answer:

Which of the following changes to a company’s contribution income statement will

always lower the break-even point (either in units or in dollars)?

A. Sales price increases by 10%.

B. Sales price decreases by 5%.

C. Variable costs increase by 10% and fixed costs decrease by 5%.

D. Variable costs decrease by 5% and fixed costs increase by 10%.

Answer:

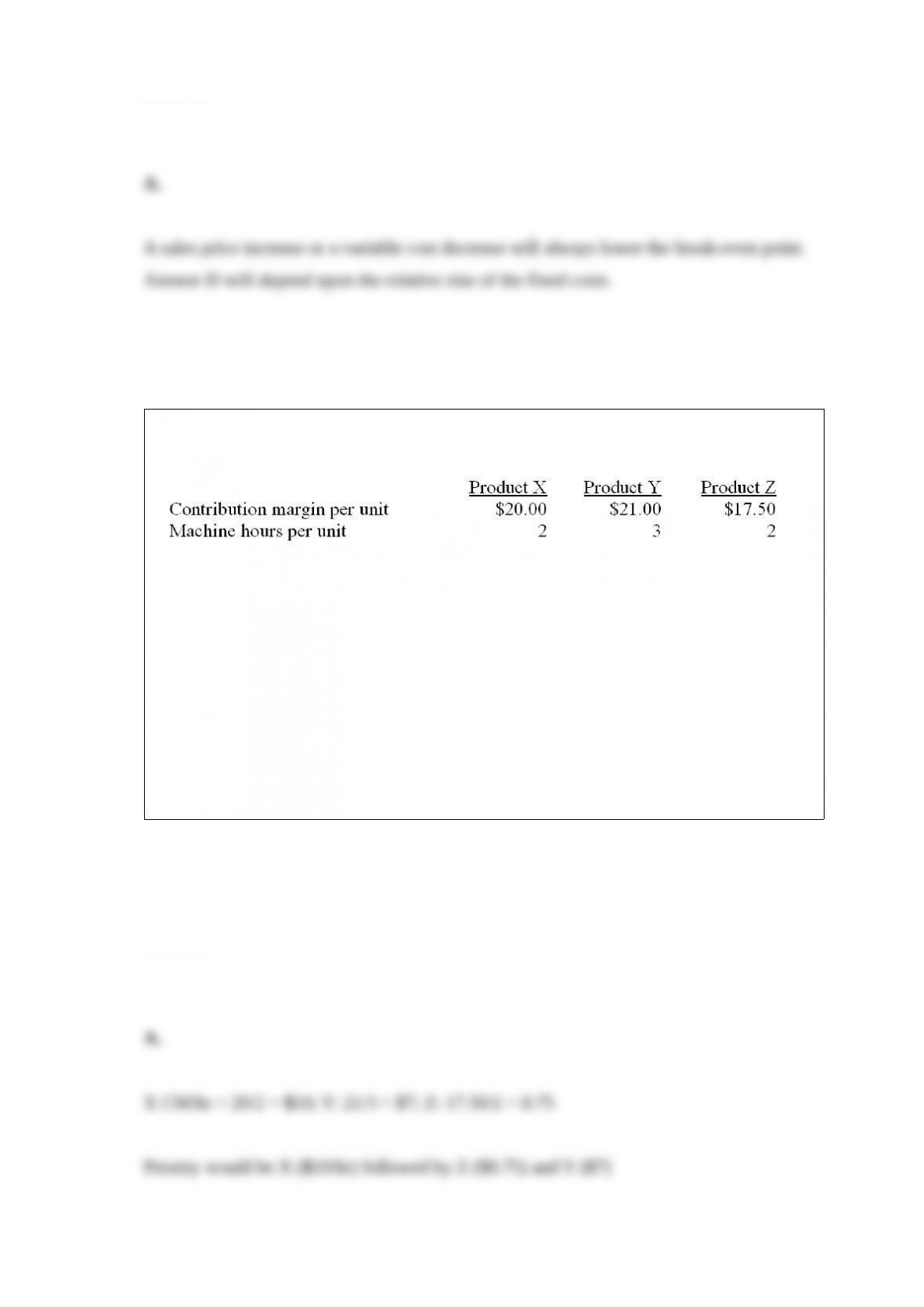

Lerner Inc has 6,600 machine hours available each month. The following information

on the company’s three products is available:

If market demand exceeds the available capacity, in what sequence should orders be

filled to maximize the company’s profits?

A. Product X first, product Z second, and product Y third

B. Product Y first, product Z second, and product X third

C. Product Y first, product X second, and product Z third

D. Product Z first, product X second, and product Y third

Answer:

Which of the following types of accounts would not be included on a budgeted balance

sheet?

A. cash

B. assets

C. liabilities

D. owners’ equity

E. revenues

Answer:

The Sledge Hammer Company manufactures a line of high quality tools. The company

sold 1,000,000 hammers at a price of $4 per unit last year. The company estimates that

this volume represents a 20% share of the current hammers market. The market is

expected to increase by 5%. Marketing specialists have determined that, as a result of a

new advertising campaign and packaging, the company will increase its share of this

larger market to 24%. Due to changes in prices, the new price for the hammer will be

$4.30 per unit. This new price is expected to be in line with the competition and have

no effect on the volume estimates. What are the estimated sales revenues in the coming

year?

A. $5,040,000.

B. $5,160,000.

C. $5,418,000.

D. $5,689,000.

Answer:

Expense A is a fixed cost expense, B is a variable cost. During the current year the

volume of output has decreased. In terms of cost per unit of output, we would expect

that

A. expense A has remained unchanged.

B. expense B has decreased.

C. expense A has decreased.

D. expense B has remained unchanged.

Answer:

Which of the following is not a partial productivity measure?

A. tons output/tons of material used

B. sales value/total cost

C. gallons output/direct labor hour

D. units produced/machine hour

Answer:

The cost accountant determined $1,700,000 of the server network’s costs were fixed

and should be allocated based on the number of connections. The remaining costs

should be allocated based on the time on the network. What is total server network costs

allocated to the Retail Division assuming the company uses dual-rates to allocate

common costs?

A. $741,667

B. $657,143

C. $425,000

D. $211,765

Answer:

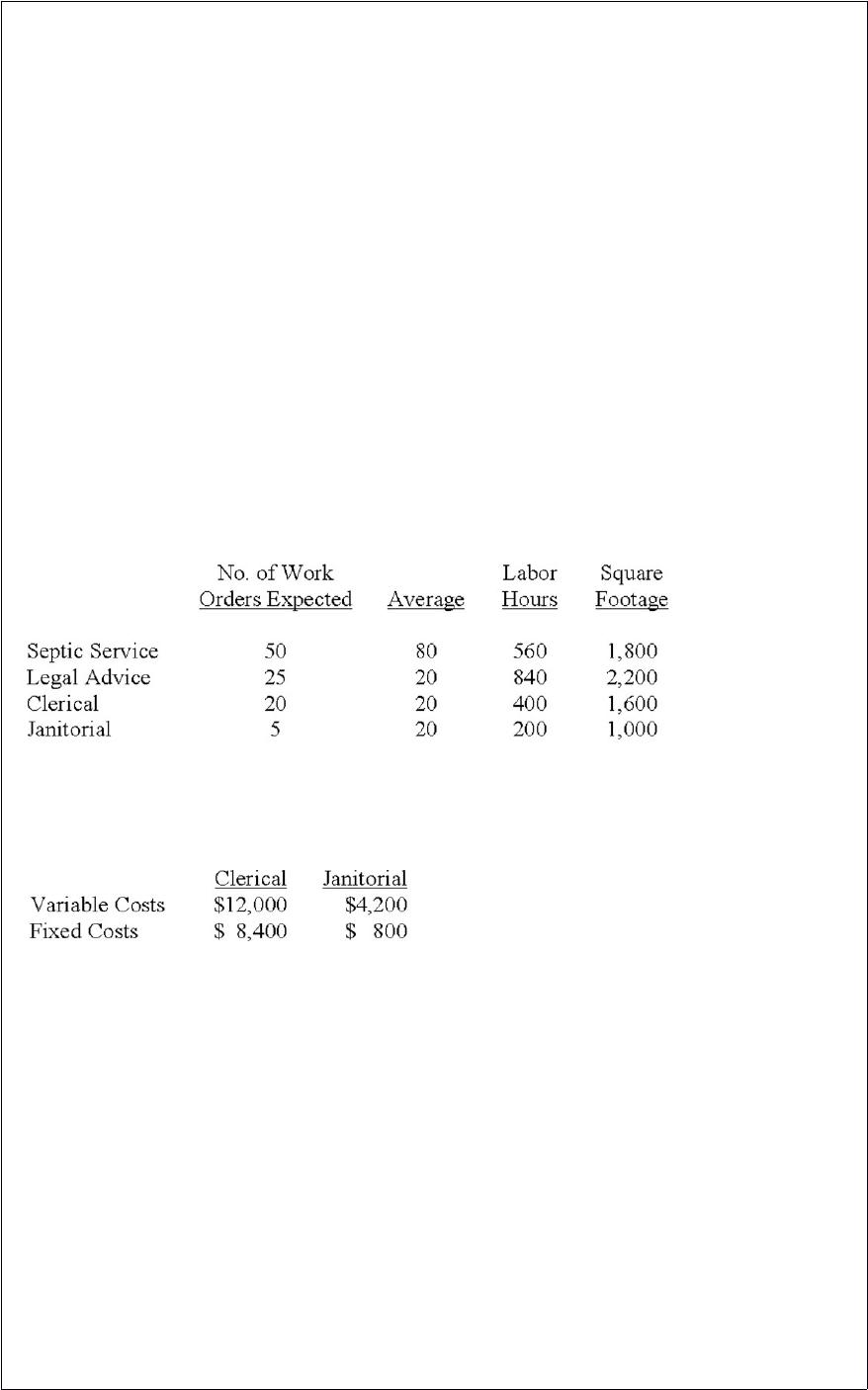

Harry Dishman owns and operates Harry’s Septic Service and Legal Advice. Harry’s

two revenue generating (production) operations are supported by two service

departments: Clerical and Janitorial. Costs in the service departments are allocated in

the following order using the designated allocation bases:

Clerical:

Variable cost: expected number of work orders processed

Fixed cost: long-run average number of work orders processed

Janitorial:

Variable cost: labor hours

Fixed cost: square footage of space occupied

Average and expected activity levels for next month (June) are as follows:

Expected costs in the service departments for June are as follows:

Under the direct method of allocation, what is the total amount of service cost allocated

to the Legal Advice operation for June? (Round all calculations to the nearest whole

dollar.)

A. $6,231

B. $7,720

C. $8,640

D. $9,330

E. $9,804

Answer:

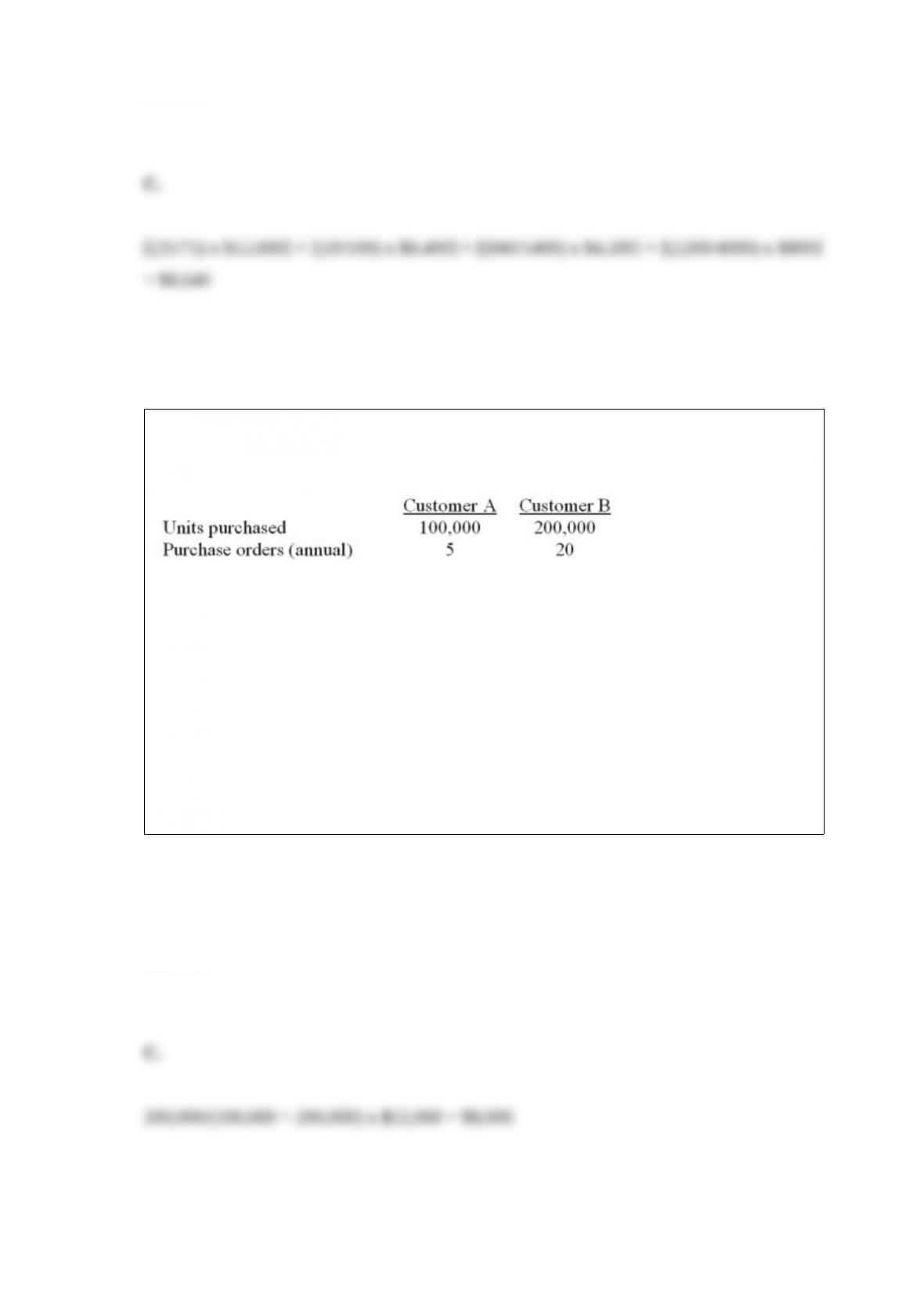

Beta Company is preparing its annual profit plan. As part of its analysis of the

profitability of its customers, management estimates that the $12,000 for sales support

should be assigned to the individual customers from the information given as follows:

What is the amount of the sales support costs that should be allocated to Customer B

assuming Beta uses units purchased to compute activity-based costs?

A. $2,400

B. $4,000

C. $8,000

D. $9,600

Answer:

The price based on customers’ perceived value for the product and the price that

competitors charge:

A. predatory price

B. target price

C. target cost

D. dumping price

Answer:

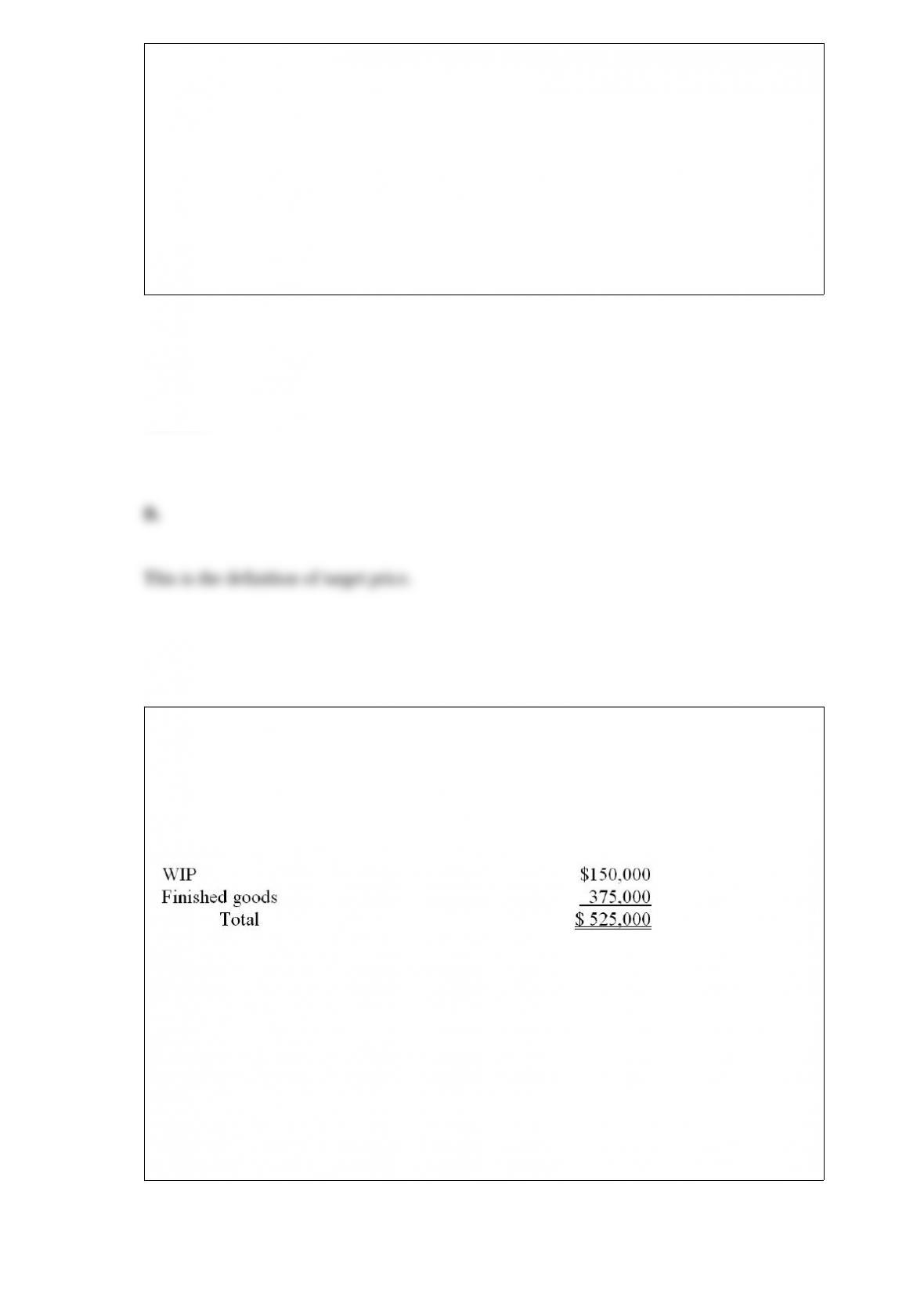

Bailey’s Corporation applies overhead based upon machine-hours. Budgeted factory

overhead was $325,000 and budgeted machine-hours were 13,000. Actual factory

overhead was $312,330 and actual machine-hours were 12,660. Before disposition of

over- or underapplied overhead, the cost of goods sold was $725,000 and ending

inventories were as follows:

Required:

a) Compute the amount of overhead applied to production.

b) Prepare the journal entry to dispose of the over/under-applied overhead using the

write-off to cost of goods sold approach.

c) Prepare the journal entry to dispose of the over/under-applied overhead using the

proration approach.

Answer: