1) Leasing assets may be a favorable alternative to purchasing assets if the asset has a

high risk of becoming obsolete.

2) Before a stock dividend can be declared or paid, there must be sufficient cash.

3) Under the direct write-off method, an attempt is made to match Bad Debt Expense to

sales revenues in the same accounting period.

4) Service department charges are similar to the expenses that would be incurred if the

profit center purchased the services from outside the company.

5) Variable costs are costs that vary in total in direct proportion to changes in the

activity level.

6) Controllable expenses are those that can be influenced by the decisions of the profit

center management.

7) On the income statement, sales discounts are normally deducted from sales to yield

the cost of merchandise sold.

8) A corporation has 10,000 shares of $100 par value stock outstanding that has a

current market value of $160. If the corporation issues a 4-for-1 stock split, the market

value of the stock will fall to approximately $32.

9) For a construction contractor, the wages of carpenters would be classified as direct

labor cost.

10) Bonds payable due in 2020 are reported on the balance sheet as long-term

liabilities.

11) Equality of the accounting equation means that no errors have occurred.

12) Creditors have preference to assets behind stockholders if a business fails.

13) Since transfer prices will affect a divisions financial performance, it is used by

decentralized segments of a business.

14) Cost behavior refers to the methods used to estimate costs for use in managerial

decision making.

15) A primary disadvantage of corporations is that the financial resources available to

them are limited.

16) Net income or loss may appear on the income statement of both a service business

and a merchandising business.

17) A cost that will not be affected by later decisions is termed an opportunity cost.

18) The basis for recording direct and indirect labor costs incurred is a summary of the

period’s:

A.job order cost sheets

B.time tickets

C.employees’ earnings records

D.clock cards

19) Espinosa Corporation had $220,000 invested in assets, sales of $242,000, income

from operations amounting to $48,400, and a desired minimum rate of return of 3%.

The rate of return on investment for Espinosa is:

A.20%

B.22%

C.3%

D.6.4%

20) Hudson, Inc. has estimated total factory overhead costs of $400,000 and 20,000

direct labor hours for the current fiscal year. If direct labor hours for the year totals

18,000 and actual factory overhead totals $350,000, what is the amount of overapplied

or underapplied overhead for the year?

A.$10,000 overapplied

B.$10,000 underapplied

C.$50,000 underapplied

D.$50,000 overapplied

21) For each of the following items indicate whether the transactions listed below

increased (+), decreased (–) or had no effect (o) by inserting the appropriate symbol.

NetIncome Assets Liab. Owners’Equity CashFlows

(a) Sold equipment for cash at a gain

(b) Recorded amortization expense on patents

(c) Paid cash for minor repairs to an asset

(d) Recorded a revenue expenditure incurred on account

(e) Paid cash to remove old building from land being prepared for use

22) A business received an offer from an exporter for 5,000 units of product at $10 per

unit. The acceptance of the offer will not affect normal production or domestic sales

prices. The following data are available:

Based on the above data, what is the differential cost from the acceptance of the offer?

A.$10,000

B.$40,000

C.$5,000

D.$45,000

23) Allowance for Doubtful Accounts has an unadjusted balance of $400 at the end of

the year, and uncollectible accounts expense is estimated at 1% of net sales. If net sales

are $300,000, compute the amount of the adjustment to record the provision for

doubtful accounts.

A.$400

B.$3,400

C.$3,000

D.$2,600

24) The charter of a corporation provides for the issuance of 100,000 shares of common

stock. Assume that 40,000 shares were originally issued and 5,000 were subsequently

reacquired. What is the number of shares outstanding?

A.5,000

B.35,000

C.45,000

D.55,000

25) Due to various fraudulent business practices and accounting coverups in the early

2000s, Congress enacted the Sarbanes-Oxley Act of 2002 . The act was responsible for

establishing a new oversight board for public accountants called the:

A.Generally Accepted Accounting Practices for Public Accountants Board

B.Public Company Accounting Oversight Board

C.Congressional Accounting Oversight Board

D.Financial Accounting Standards Board

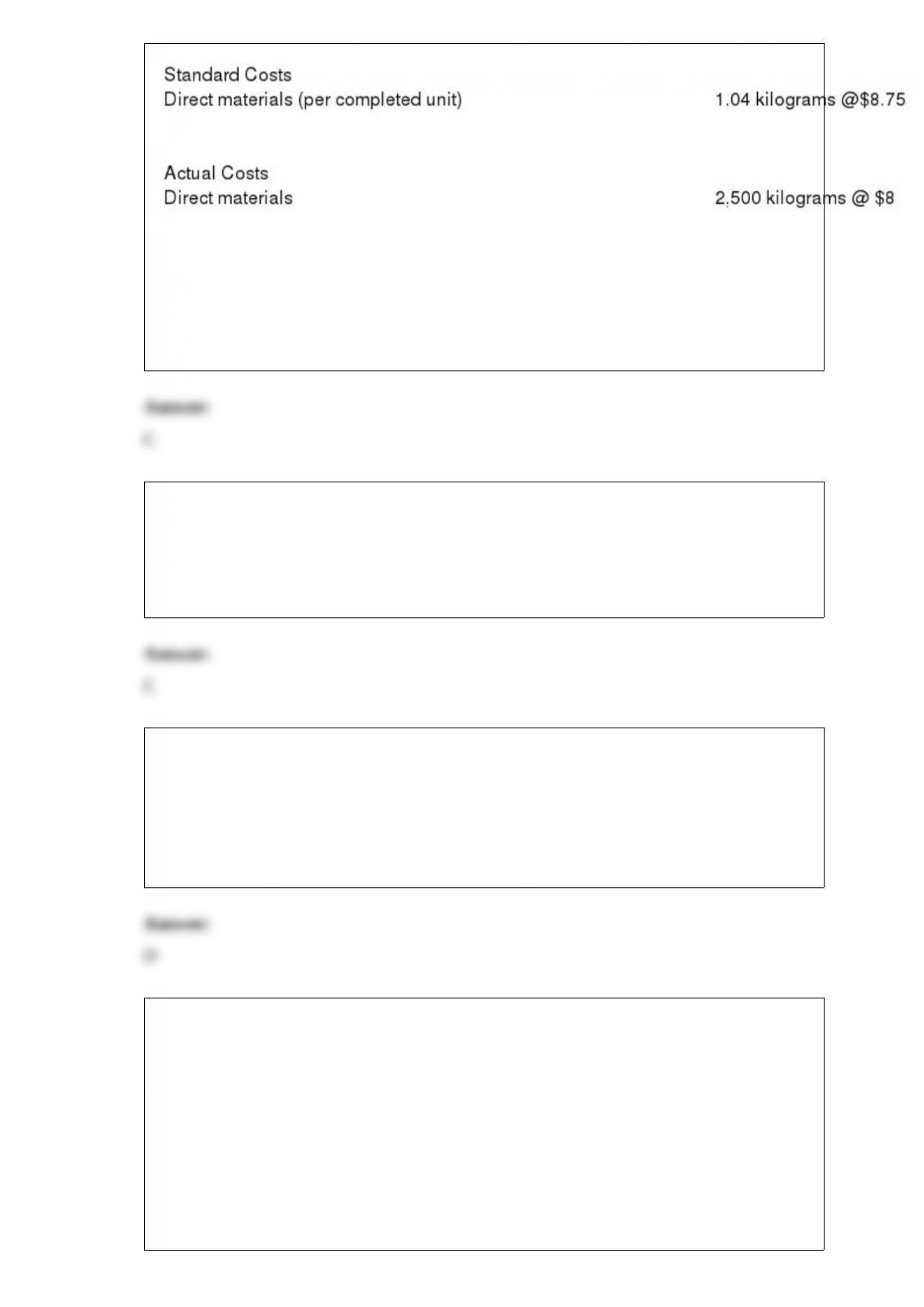

26) The standard costs and actual costs for direct materials for the manufacture of 2,500

actual units of product are as follows:

The amount of direct materials price variance is:

A.$1,875 unfavorable

B.$1,950 favorable

C.$1,875 favorable

D.$1,950 unfavorable

27) The first budget customarily prepared as part of an entity’s master budget is the:

A.production budget

B.cash budget

C.sales budget

D.direct materials purchases

28) The percentage change in long-term liabilities between two balance sheet dates is

an example of:

A.vertical analysis

B.solvency analysis

C.profitability analysis

D.horizontal analysis

29) Donald Duck Co.

Donald Duck Co. has a five-day workweek (Monday through Friday). Employees earn

$500 per day.

Refer to Donald Duck Co. If the month ends on Tuesday, and wages will not be paid

until Friday, how much wage expense should be accrued on Tuesday?

A.$500

B.$1,500

C.$2,500

D.$1,000

30) ABN Company sold goods, receiving $20,000 in cash and $25,000 on credit. How

much revenue should it record under the accrual basis of accounting?

A.$5,000

B.$25,000

C.$20,000

D.$45,000

31) Dinkins Inc. is considering disposing of a machine with a book value of $50,000

and an estimated remaining life of five years. The old machine can be sold for $15,000.

A new machine with a purchase price of $150,000 is being considered as a replacement.

It will have a useful life of five years and no residual value. It is estimated that variable

manufacturing costs will be reduced from $70,000 to $45,000 if the new machine is

purchased. The net differential increase or decrease in cost for the entire five years for

the new equipment is:

A.$10,000 increase

B.$25,000 decrease

C.$10,000 decrease

D.$25,000 increase

32) A note payable requires payment of the amount borrowed plus:

A.interest

B.tax

C.overhead

D.dividend

33) The financial statements are affected by which type(s) of adjustments?

A.Deferrals

B.Accruals

C.Both deferrals and accruals

D.Neither deferrals nor accruals

34) A company sold 200 shares of common stock with a par vale of $5 at a price of $12

per share. Which section of the statement of cash flows will contain this transaction?

A.Operating activities

B.Investing activities

C.Financing activities

D.Sale of stock will not appear on the statement of cash flows

35) Book value is computed as:

A.current market value less residual value

B.cost less residual value

C.current market value less accumulated depreciation

D.cost less accumulated depreciation

36) In evaluating the profit center manager, the income from operations should be

compared:

A.across profit centers

B.to historical performance or budget

C.to the competitor’s net income

D.to the total companys earnings per share

37) Which of the following doesnt result in an unfavorable fixed overhead volume

variance?

A.Sales orders at a low level

B.Machine breakdowns

C.Employee inexperience

D.Increase in utility costs

38) A _____ is an economic event that under generally accepted accounting principles

affects an element of the financial statements and must be recorded.

A.framework

B.control

C.set of rules

D.transaction

39) If the expected sales volume for the current period is 7,000 units, the desired ending

inventory is 400 units, and the beginning inventory is 300 units, the number of units set

forth in the production budget, representing total production for the current period, is:

A.6,900

B.7,000

C.7,200

D.7,100

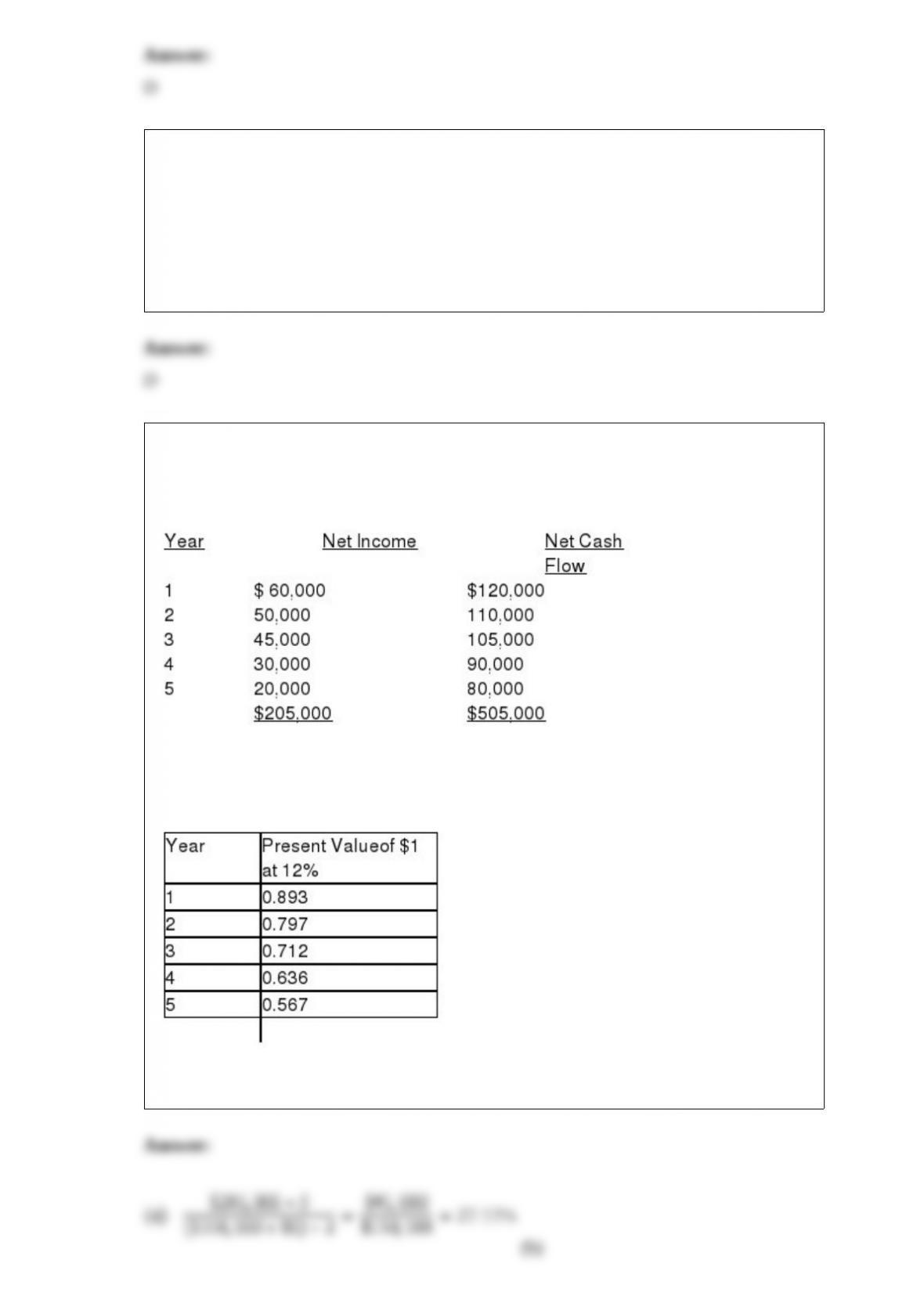

40) Sommers Company is evaluating a project requiring a capital expenditure of

$300,000. The project has an estimated life of 5 years and no salvage value. The

estimated net income and net cash flow from the project are as follows:

The company’s minimum desired rate of return for net present value analysis is 12%.

The present value of $1 at compound interest of 12% is shown in the table below:

Determine (a) the average rate of return on investment, giving effect to depreciation on

the investment, and (b) the net present value.

41) The amount of the estimated average income for a proposed investment of $60,000

in a fixed asset, giving effect to depreciation (straight-line method), with a useful life of

four years, no residual value, and an expected total income yield of $22,300, is:

A.$10,800

B.$5,575

C.$5,400

D.$15,000

42) A check drawn by a depositor for $810 in payment of a liability was recorded by the

depositor as $180. The $630 difference would be included on the bank reconciliation as

a(n):

A.addition to the cash balance per books

B.addition to the cash balance per bank

C.deduction from the cash balance per bank

D.deduction from the cash balance per books

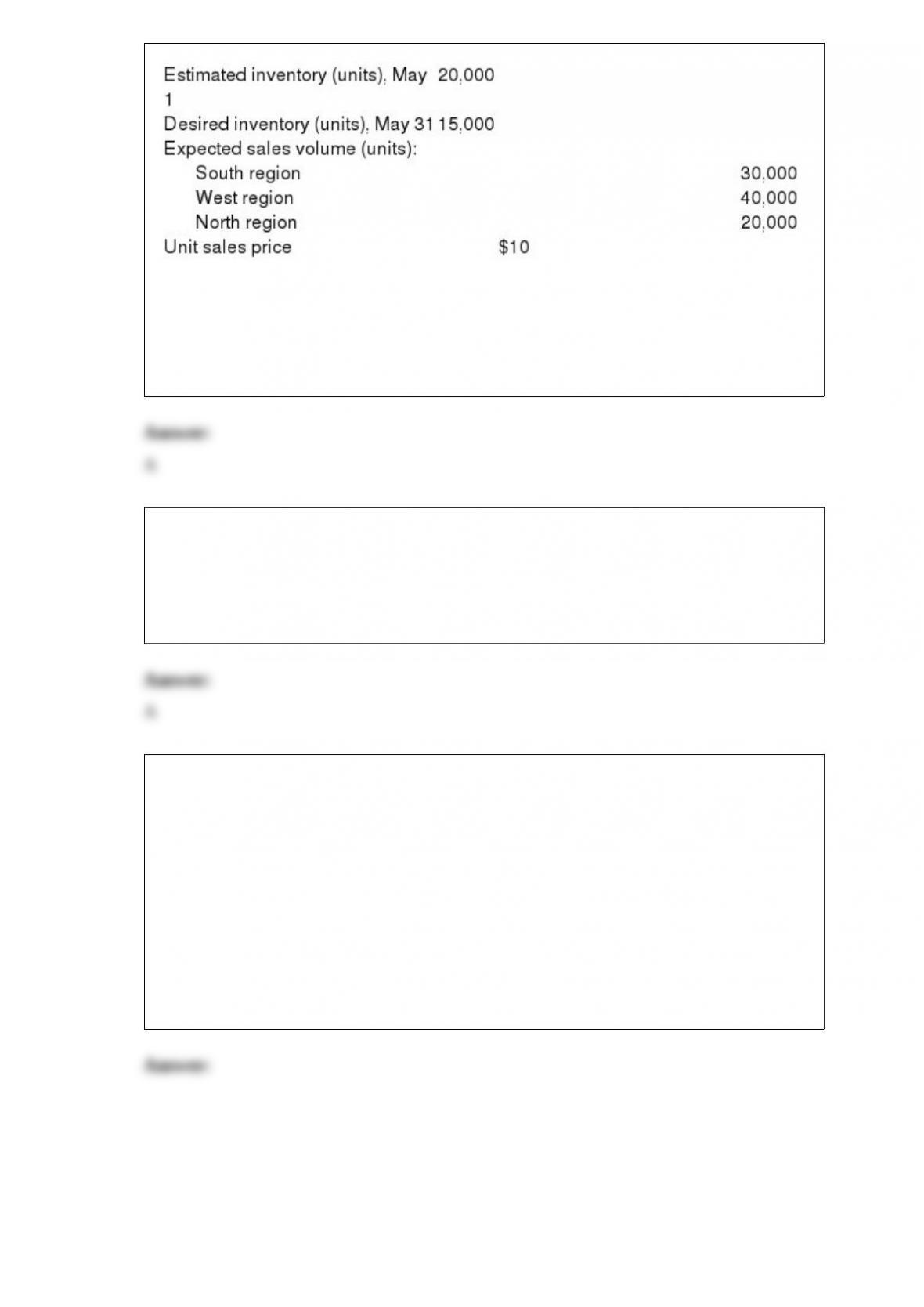

43) Based on the following production and sales estimates for May, determine the

number of units expected to be manufactured in May.

A.85,000 units

B.90,000 units

C.95,000 units

D.105,000 units

44) Which of the following is not a product cost?

A.CEO salary

B.Depreciation on factory equipment

C.Wages of an assembly worker

D.Silicon wafers for microcomputer chips

45) FDE Manufacturing Company has a normal plant capacity of 75,000 units per

month. Because of an extra large quantity of inventory on hand, it expects to produce

only 60,000 units in May. Monthly fixed costs and expenses are $150,000 ($2 per unit

at normal plant capacity), and variable costs and expenses are $13 per unit. The present

selling price is $25 per unit. The company has an opportunity to sell 5,000 additional

units at $14.30 per unit to an exporter who plans to market the product under its own

brand name in a foreign market. The additional business is therefore not expected to

affect the regular selling price or quantity of sales of FDE Manufacturing Company.

Prepare a differential analysis report, dated April 21 of the current year, on the proposal

to sell at the special price.

46) Define accounting and its role in business.

47) How do businesses make money? What strategies can they use to gain a

competitive advantage?

48) What is the purpose of the Sarbanes-Oxley Act of 2002, and why was it enacted?

49)

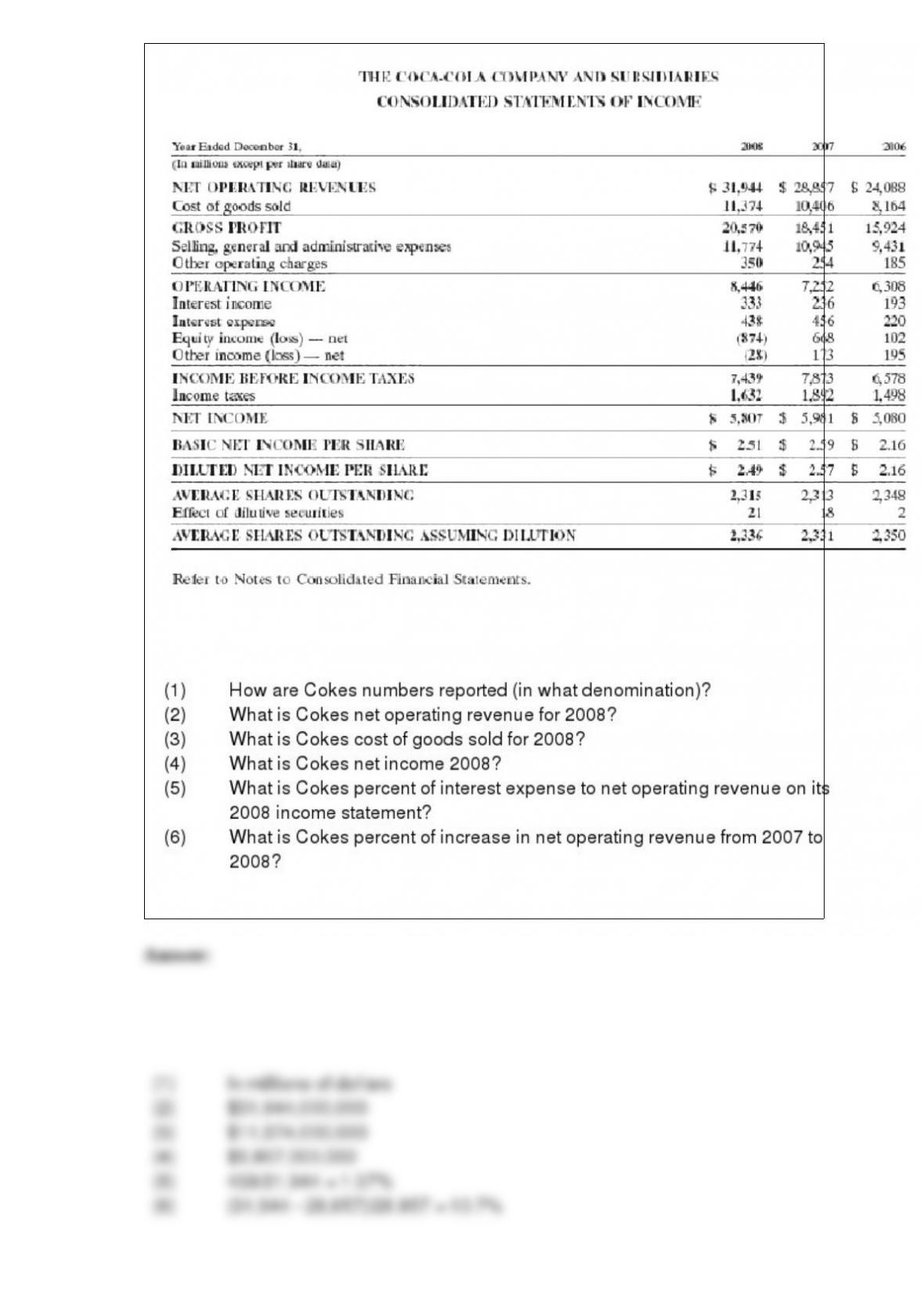

Review Coke-Colas financial statements and answer the following questions:

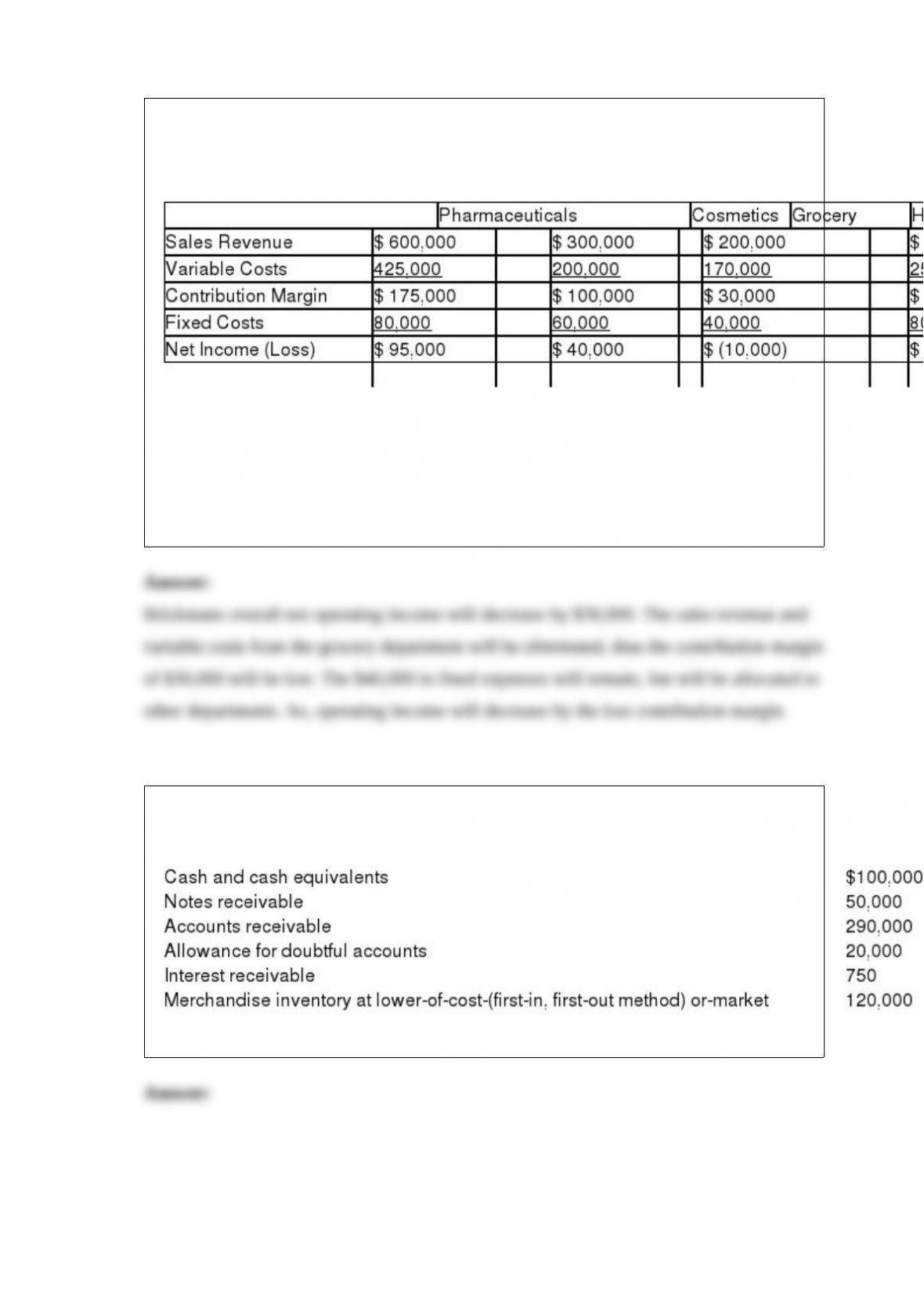

50) Brickmans Pharmacy sells a variety of products. The business is divided into four

segments or departments for reporting purposes. The departments and their operating

results are shown below:

The fixed costs consist of insurance, property taxes, interest, and other costs that will

not be eliminated if a department is discontinued.

Brickmans management is considering eliminating the grocery department. Assuming

sales in the other departments will not be affected by dropping the grocery department,

what will be the effect on the companys total operating income?

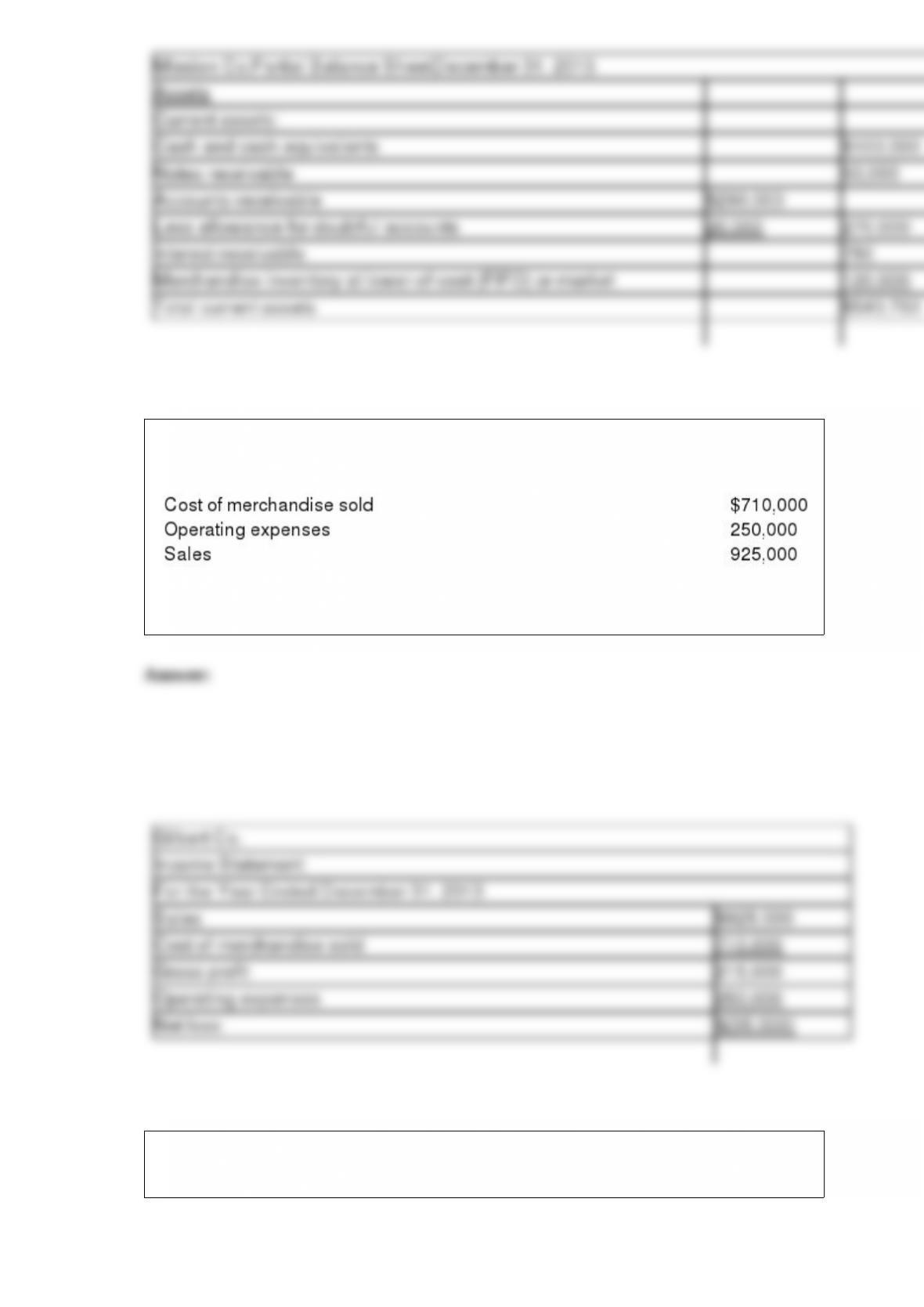

51) On the basis of the following data related to current assets for Mission Co. at

December 2013, prepare a partial balance sheet in good form.

52) The following data for the current year ended December 31, 2013, were extracted

from the accounting records of Gilbert Co.:

Prepare a multiple-step income statement for the year ended December 31, 2013 .

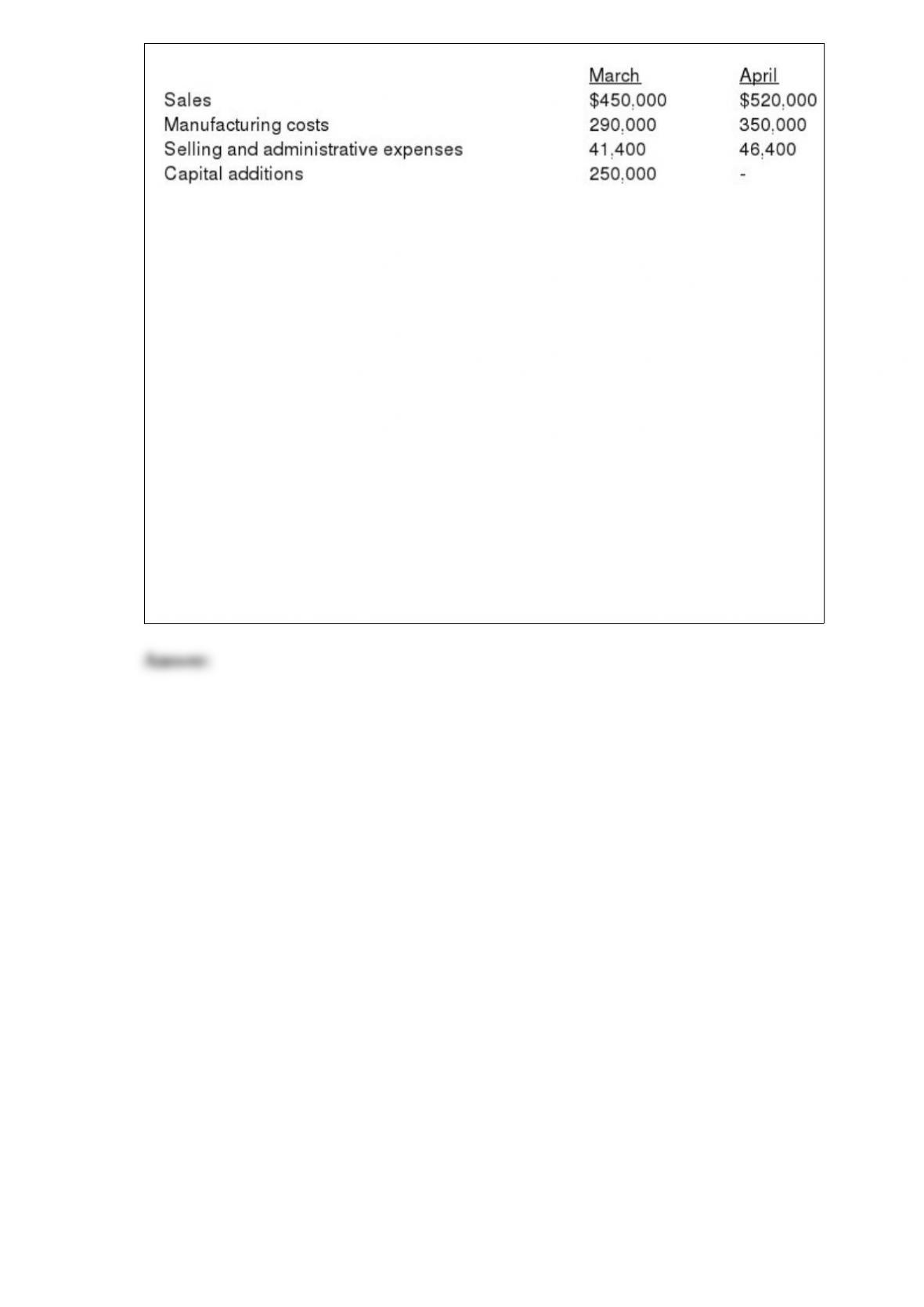

53) The treasurer of Unisyms Company has accumulated the following budget

information for the first two months of the coming year:

The company expects to sell about 35% of its merchandise for cash. Of sales on

account, 80% are expected to be collected in full in the month of the sale and the

remainder in the month following the sale. One-fourth of the manufacturing costs are

expected to be paid in the month in which they are incurred and the other three-fourths

in the following month. Depreciation, insurance, and property taxes represent $6,400 of

the probable monthly selling and administrative expenses. Insurance is paid in

February, and a $40,000 installment on income taxes is expected to be paid in April. Of

the remainder of the selling and administrative expenses, one-half are expected to be

paid in the month in which they are incurred, with the balance paid in the following

month. Capital additions of $250,000 are expected to be paid in March.

Current assets as of March 1 are composed of cash of $45,000 and accounts receivable

of $51,000. Current liabilities as of March 1 are composed of accounts payable of

$121,500 ($102,000 for materials purchases and $19,500 for operating expenses).

Management desires to maintain a minimum cash balance of $20,000.

Prepare a monthly cash budget for March and April.