1) After the auditor has completed all audit procedures, it is necessary to combine the

information obtained to reach an overall conclusion as to whether the financial

statements are fairly presented. This is a highly subjective process that relies heavily on:

A) generally accepted auditing standards

B) the

C) generally accepted accounting principles

D) the auditor’s professional judgment

2) A credit memo is a document used internally that indicates authority to write-off an

account receivable as uncollectible.

A) True

B) False

3) When internal controls are highly effective in processing accounting transactions, the

extent of substantive tests should be reduced.

A) True

B) False

4) The emphasis in the audit of dividends is on the ending balance rather than the

transactions.

A) True

B) False

5) Rodgers CPA has requested permission to communicate with predecessor auditor in

order to review certain workpapers for high risk accounts for a new audit client. The

new audit clients refusal to allow this communication to occur would impact Rodgers

decision concerning:

A) the auditor’s ability to design audit tests

B) possible scope exception due to lack of access

C) integrity of management concerning possible accounting misstatements

D) violation of the GAAP rules concerning consistency and comparability of financial

information

6) When should auditors generally assess a client’s ability to continue as a going

concern?

A) upon completion of the audit

B) during the planning stages of the audit

C) throughout the entire audit process

D) during testing and completion phases of the audit

7) IT controls are classified as either input controls or output controls.

A) True

B) False

8) Tolerable misstatement is inversely related to sample size.

A) True

B) False

9) Procedures used to obtain an understanding of internal control are normally

performed on fewer transactions than procedures used to test controls.

A) True

B) False

10) The extent of a search for unrecorded liabilities largely depends on:

A) materiality and inherent risk

B) materiality and control risk

C) materiality only

D) inherent risk only

11) Hiring personnel initiates the payroll and personnel cycle.

A) True

B) False

12) Which of the following documents is not commonly associated with the “cash

receipts” class of transactions?

A) Remittance advice

B) Sales order

C) Prelisting of cash receipts

D) Cash receipts journal or listing

13) Operational audits are primarily geared towards improving a company’s operational

efficiency and effectiveness.

A) True

B) False

14) The term “audit failure” refers to the situation when the auditor has followed

auditing standards yet still fails to discover that the client’s financial statements are

materially misstated.

A) True

B) False

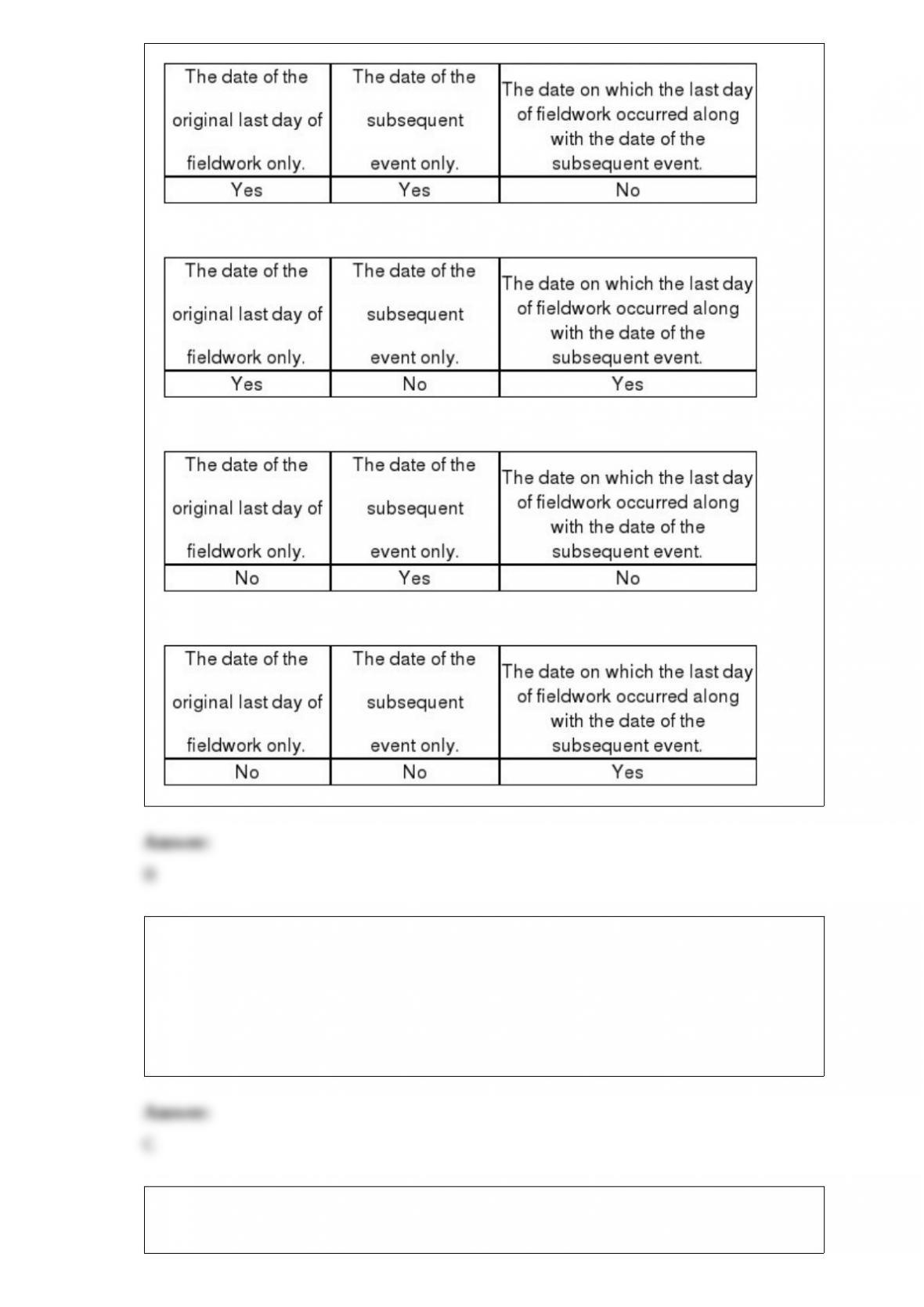

15) If the auditor determines that a subsequent event that affects the current period

financial statements occurred after fieldwork was completed but before the audit report

was issued, what date(s) may the auditor use on the report?

A)

B)

C)

D)

16) Which of the following is not a factor that relates to opportunities to commit

fraudulent financial reporting?

A) Lack of controls related to the calculation and approval of accounting estimates

B) Ineffective oversight of financial reporting by the board of directors

C) Management’s practice of making overly aggressive forecasts

D) High turnover of accounting, internal audit, and information technology staff

17) Auditors should issue a disclaimer of opinion when there is a highly material

client-imposed scope restriction.

A) True

B) False

18) During his examination of a January 19, 2008 cutoff bank statement, an auditor

noticed that the majority of checks listed as outstanding at December 31, 2007, had not

cleared the bank. This would indicate:

A) a high probability of kiting

B) a high probability of lapping

C) that the 2007 cash disbursements records had been closed prior to December 31,

2007

D) that the 2007 cash disbursements records had been held open past December 31,

2007

19) Auditors may decide to replace tests of details with analytical procedures when

possible because the:

A) analytical procedures are more reliable

B) analytical procedures are considerably less expensive

C) analytical procedures are more persuasive

D) tests of details are more difficult to interpret

20) In the auditing environment, failure to meet auditing standards is often:

A) an accepted practice

B) a suggestion of negligence

C) conclusive evidence of negligence

D) tantamount to criminal behavior

21) Which of the following can affect the independence of operational auditors?

A)

B)

C)

D)

22) Master files, worksheets, and reports that accumulate material, labor, and overhead

as the costs are incurred are:

A) accounting systems

B) storeroom documents

C) cost accounting records

D) finished goods inventory records

23) Controls which provide a means of ensuring that the physical counts are properly

summarized, priced at the same amount as the unit records, correctly extended and

totaled, and included in the general ledger at the proper amount are known as:

A) standard cost controls

B) pricing internal controls

C) compilation internal controls

D) count quantity internal controls

24) Which of the following audit procedures would be the most correct in determining

the audit objective of existence for the equipment account in the fixed asset master file?

A) Examine vendor invoices and receiving reports

B) Review transactions near the balance sheet date

C) Recalculate vendor invoices

D) Examine vendor invoices for correct accounting treatment

25) Examples of unqualified opinions which contain modified wording (without adding

an explanatory paragraph) include:

A) the use of other auditors

B) material uncertainties

C) substantial doubt about the audited company (or the entity) continuing as a going

concern

D) lack of consistent application of GAAP

26) The scope paragraph of the standard unqualified audit report states that the audit is

designed to:

A) discover all errors and/or irregularities

B) discover material errors and/or irregularities

C) conform to generally accepted accounting principles

D) obtain reasonable assurance whether the statements are free of material misstatement

27) When considering internal control, an auditor should be aware of the concept of

reasonable assurance, which recognizes that the:

A) segregation of incompatible functions is necessary to ascertain that internal control

is effective

B) employment of competent personnel provides assurance that the objectives of

internal control will be achieved

C) establishment and maintenance of internal control is an important responsibility of

the management and not of the auditor

D) concept allows for only a remote likelihood that material misstatements will not be

prevented or detected on a timely basis

28) Which of the following is not a disadvantage of monetary-unit-sampling?

A) It may be difficult to select samples from large population without computer

assistance

B) The total misstatement bounds resulting when misstatements are found may be too

low to be useful to the auditor

C) The total misstatement bounds resulting when misstatements are found may be too

high to be useful to the auditor

D) Each of the above is a disadvantage

29) Normally it may be unnecessary to examine supporting documentation for each

addition to property, plant, and equipment, but it would be customary to verify:

A) all large transactions

B) all unusual transactions

C) a representative sample of typical additions

D) all three of the above