Which of the following statements about the need for adjustments is not correct?

A) Without adjustments, the financial statements present an incomplete and misleading

picture of the company.

B) Adjusting entries are intended to change the operating results to reflect

management’s objectives for operating performance.

C) Adjustments help the financial statements present the best picture of whether the

company’s activities were profitable for the period.

D) Adjustments help the financial statements present the economic resources that the

company owns and owes at the end of the period.

A company received a bill of $3,500 for utilities used in the current month. The journal

entry to record this event:

A) will include a debit to Accounts Receivable for $3,500.

B) will include a credit to Accounts Payable for $3,500.

C) will include a credit to Utilities Expense.

D) is not required; no journal entry should be prepared until the utilities bill is paid.

A company has net income of $5.6 million. Stockholders’ equity at the beginning of the

year is $32.55 million and, at the end of the year, it is $38.15 million. The only change

to stockholders’ equity came from net income. The return on equity ratio is

approximately:

A) 0.15.

B) 0.16.

C) 0.87.

D) 6.64.

Which of the following statements about bonds payable net of a discount or premium is

not correct?

A) If a company records a discount or premium with the bonds payable in a single

account called Bonds Payable, Net, it is using simplified effective-interest amortization.

B) When bonds payable are accounted for net of a discount, the initial amount recorded

in the Bonds Payable, Net account is the issue price of the bond.

C) When simplified effective-interest amortization is used, the balance in the Bonds

Payable, Net account will increase as the bond approaches the maturity date.

D) If a company issued bonds at their face value, the balance of Bonds Payable, Net

account will always be equal to the face value of the bonds as long as the bonds are

outstanding.

The amount of uncollectible accounts at the end of the year is estimated to be $25,000,

using the aging of accounts receivable method. The balance in the Allowance of

Doubtful Accounts account is an $8,000 credit before adjustment. What is the adjusted

balance of the Allowance for Doubtful Accounts at the end of the year?

A) $8,000

B) $17,000

C) $25,000

D) $33,000

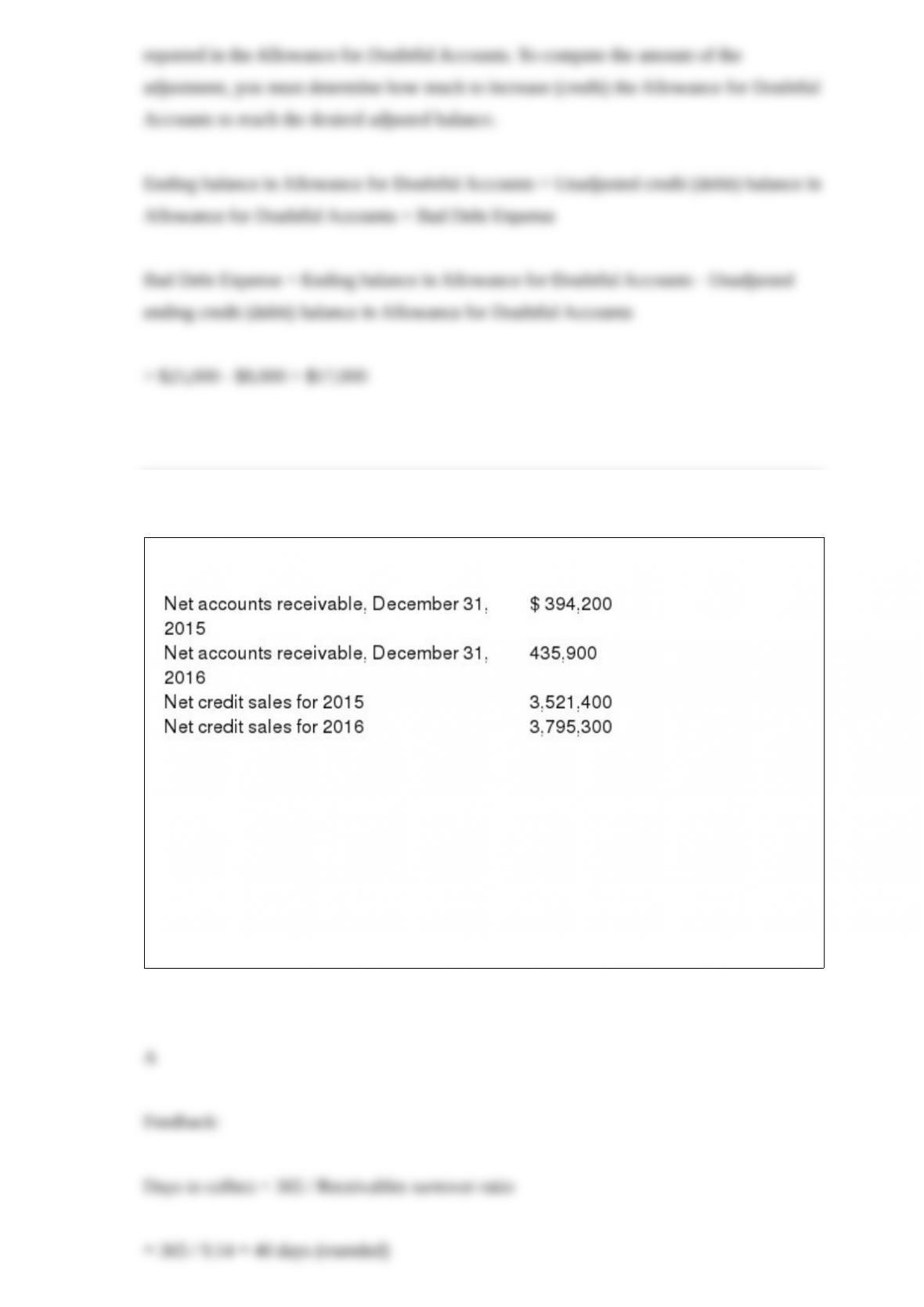

The following information is available:

The days to collect for 2016 is closest to:

A) 40 days.

B) 41 days.

C) 43 days.

D) 42 days.

Which of the following is not correct?

A) Assets = Liabilities + Stockholders’ Equity

B) Liabilities = Assets – Stockholders’ Equity

C) Stockholders’ Equity + Liabilities – Assets = 0

D) Assets = Liabilities – Stockholders’ Equity

Which of the following practices would not be considered ethical?

A) Failing to record an expense even though cash has been paid.

B) Recording 31 days of sales in April.

C) Using the cash basis of accounting.

D) Adjusting the accounts after a trial balance has been prepared.

Creditors look at the balance sheet to see whether the company:

A) is profitable.

B) owns enough assets to pay what it owes to creditors.

C) has had a positive cash flow from operations.

D) is paying sufficient dividends to stockholders.

Contra-revenue accounts:

A) are balance sheet accounts.

B) increase net income.

C) are increased with a debit.

D) increase net sales.

The principles of internal control include which of the following?

A) Use only computerized systems

B) Establish responsibility

C) Maintain perpetual inventory records

D) Eliminate fraud

Choose the appropriate letter to match the term and the definition. Not all definitions

will be used.

Term

1> _____ Full Disclosure Principle

2> _____ Ratio Analysis

3> _____ Liquidity

4> _____ Going-Concern Assumption

5> _____ Profitability

6> _____ Solvency

7> _____ Trend Analysis

8> _____ Vertical Analysis

Definition

A) The ability of a company to meet its short-run financial obligations.

B) A type of analysis that focuses on relationships within a single financial statement.

C) Also known as time-series analysis.

D) The standard that companies should present all relevant information needed to

interpret a company’s financial position and performance.

E) The standard that expenses should be recognized when incurred.

F) A measure of current earnings performance.

G) A result from comparing a company’s results to other companies in the industry.

H) A measure of long-run survivability.

I) The standard that revenue should be recorded when earned, provided payment is

reasonably expected.

J) Measures that relate financial variables reported in one or more of the financial

statements from the same year.

K) The characteristic that financial information needs to be valuable to decision makers.

L) The standard that takes for granted a company’s near term financial survival.

Suppose a company generally records revenues and expenses before receiving or

making cash payments. Which of the following statements is not correct?

A) If revenues are falling, a net loss could result even though the company reports a net

cash inflow from operating activities.

B) If revenues are rising, net income could result even though the company reports a

net cash outflow from operating activities.

C) Net income and net cash flows provided by operating activities will always agree.

D) The income statement doesn’t explain changes in cash because it focuses on just the

operating results of the business.

Which of the following statements about cash flows from investing activities is correct?

A) The proceeds from sales of investments are reported as cash inflows from investing

activities.

B) Cash flows from investing activities are calculated by making adjustments to net

income.

C) Cash paid to acquire long-lived assets is reported as a cash inflow from investing

activities.

D) Cash received from issuing a long-term payable is reported as a cash inflow from

investing activities.

Choose the appropriate letter to match the term and the definition. Not all definitions

will be used.

Term:

1> _____ Date of Declaration

2> _____ Issued Shares

3> _____ Seasoned New Issues

4> _____ Pro Rata Basis

5> _____ Date of Record

6> _____ Additional Paid-in Capital

7> _____ Outstanding Shares

8> _____ Stock Options

9> _____ Payment Date

Definition:

A. The date on which a company authorizes a dividend payment.

B. The total number of shares currently owned by stockholders.

C. When cash or stock dividends are issued according to the proportion of stock owned.

D. Dividends that have not had income tax withheld from them.

E. The date on which a company determines who receives a dividend.

F. When employees of a company have the opportunity to buy a company’s stock in the

future at a fixed price.

G. The accumulation of all the past dividends the company has not paid.

H. When a company sells issues of stock after its IPO.

I. The date on which a company debits dividends payable and credits cash.

J. When cash or stock dividends are issued in an equal dollar or share amount per

stockholder.

K. The date on which a liability is recorded for a dividend.

L. The total number of shares the company has sold, whether held by stockholders or by

the company.

M. When owners of the company contribute additional capital beyond what they paid

for their stock.

N. The amount above the par value of the stock that owners paid the issuer for the

stock.

A debt-to-assets ratio of 0.50 indicates that the company has:

A) more liabilities than stockholders’ equity.

B) equal amounts of liabilities and stockholders’ equity.

C) more stockholders’ equity than liabilities.

D) no liabilities.

Which of the following statements about financial statements is not correct?

A) Cash flows from financing activities would appear on the Statement of Cash Flows.

B) Dividends would appear on the Statement of Retained Earnings.

C) Assets would appear on the Income Statement.

D) Revenues would appear on the Income Statement.