Choose the appropriate letter to match the term and the definition. Not all definitions

will be used.

Term

1> _____ Operating Activities

2> _____ Indirect Method

3> _____ Working Capital

4> _____ Cash Equivalents

5> _____ Investing Activities

6> _____ Supplemental Disclosures

7> _____ Direct Method

8> _____ Financing Activities

Definition

A. Cash inflows and outflows related to components of net income.

B. Include assets that are very liquid and are purchased by the entity within three

months of maturity.

C. These activities include only purchases made with borrowed funds.

D. Reports the components of cash flows from operating activities as gross receipts and

gross payments.

E. This ratio uses net income instead of operating cash flow to analyze a company’s

ability to finance the cost of its debt.

F. Measures the ability of a company to finance its interest payments with its operating

cash flow before taxes and interest.

G. A measure of the amount by which current assets exceed current liabilities.

H. These activities include money lent by a company as well as money borrowed by a

company.

I. Must include cash paid for interest and income tax in a separate schedule.

J. Cash inflows and outflows related to the sale or purchase of investments and

long-lived assets.

K. Cash inflows and outflows related to financing sources external to the company

(owners and lenders).

L. Presents the operating activities section of the cash flow statement by adjusting net

income to compute cash flows from operating activities.

Match the term and its definition. There are more definitions than terms.

Terms

____ 1> Promissory Note

____ 2> Net Accounts Receivable

____ 3> Bad Debt Expense

____ 4> Maturity Date

____ 5> Days to Collect

____ 6> Accounts Receivable

____ 7> Allowance For Doubtful Accounts

____ 8> Receivables Turnover

Definitions

A. The time at which a loan must be repaid.

B. A financial statement that shows the calculation of Bad Debt Expense for a company.

C. Total money owed the company for sales made on credit.

D. Net credit sales revenue divided by the net income.

E. An agreement by a borrower to repay the lending company with interest during a

specified time period.

F. The time at which a borrower must make annual interest payments.

G. A contra-asset account.

H. The days of the year divided by the receivables turnover ratio.

I. The portion of Accounts Receivable that the company expects to collect.

J. An account that is debited for the amount of credit sales estimated as uncollectible.

K. Net credit sales revenue divided by the average net receivables.

L. The days of the year divided by the net sales revenue.

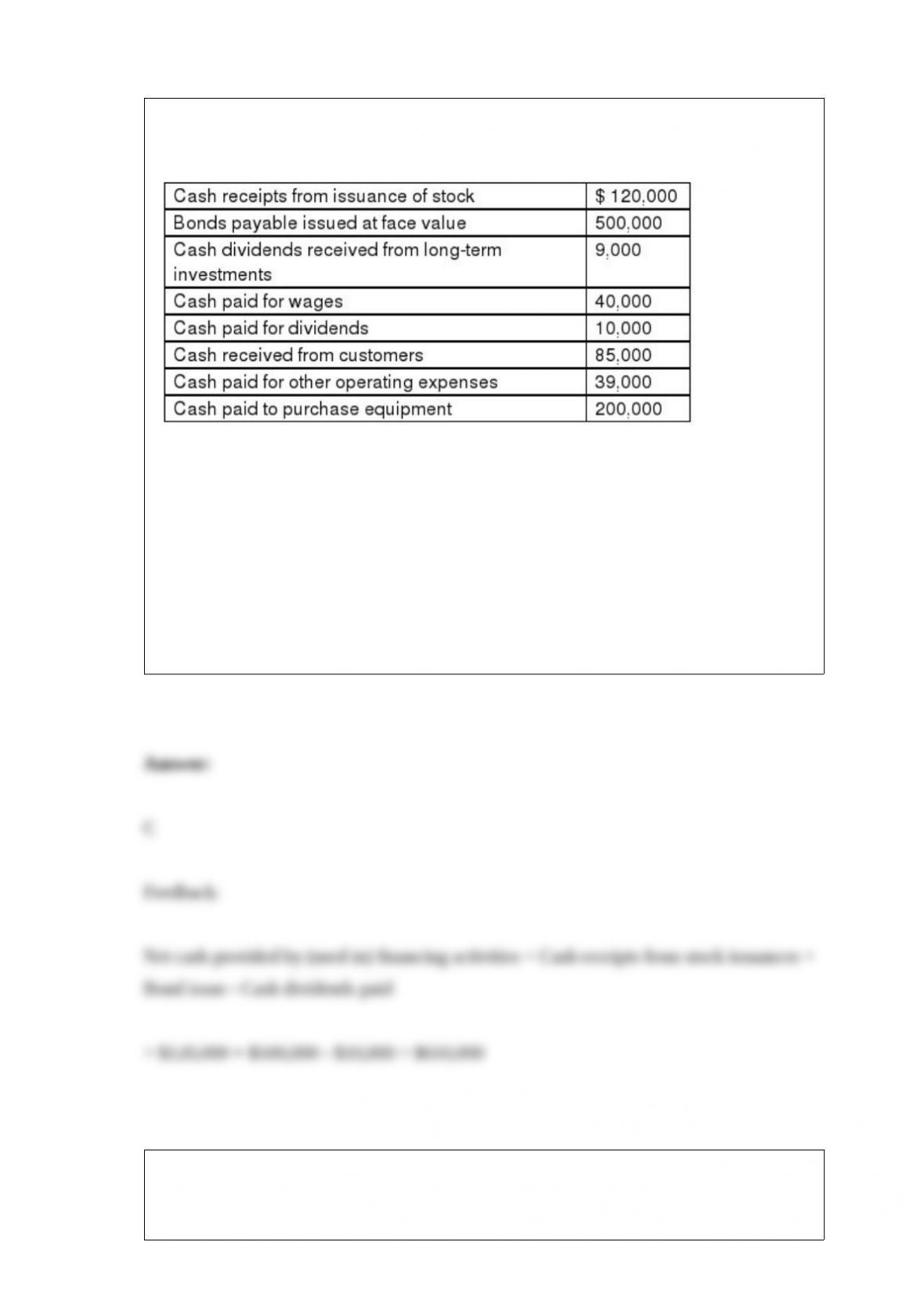

Flynn Corporation had the following cash flows for the current year. The company uses

the direct method in preparing the statement of cash flows.

Use the information above to answer the following question. What is the net cash flows

provided by (used in) financing activities?

A) $620,000

B) $410,000

C) $610,000

D) $490,000

The Treasure Chest Corporation had Retained Earnings at the end of December 31,

2015 of $450,000. During 2016, the company had net income of $170,000 and declared

dividends of $20,000. The amount of Retained Earnings reported on the balance sheet

as of December 31, 2016 will be:

A) $430,000.

B) $600,000.

C) $620,000.

D) $640,000.

Travis County Bank agrees to lend Brickyard Corporation $200,000 on January 1.

Brickyard signs a $200,000, 4%, 9-month note. Interest is due at maturity on September

30. The company’s fiscal year ends June 30 and adjusting entries are recorded at that

time only.

Use the information above to answer the following question. What journal entry will

Brickyard make when paying the note at maturity?

A) Debit Cash and credit Notes Payable for $200,000

B) Debit Cash and credit Notes Payable for $206,000

C) Debit Notes Payable and credit Cash for $206,000

D) Debit Notes Payable and credit Cash for $200,000

Pearly Gates Inc. has a debt-to-assets ratio of 0.55. This means that:

A) stockholders’ equity is 55% of total assets.

B) stockholders’ equity is 45% of total assets.

C) investors provide 55% of the company’s financing.

D) liabilities are 55% of equity.

A company purchased a computer system on January 2, 2015 for $1,600,000. The

company used the straight-line depreciation method with an estimated useful life of 6

years and a residual value of $130,000. The company prepares financial statements at

December 31.

Use the information above to answer the following question. Which of the following is

correct about the depreciation recorded?

A) Accumulated Depreciation will be debited for $266,667.

B) The book value of the computer system at December 31, 2015 will be $1,225,000.

C) Depreciation expense will be debited for $245,000.

D) The depreciable cost of the computer system is $1,600,000.

The total amount of interest that will be paid on a four-month, $6,500, 9% note payable

equals:

A) $585

B) $292

C) $146

D) $195

Darin Company purchased land at a cost of $15,000 and planned to use it to construct a

new storage facility on the property. A short time later, the company changed its plans

and sold the property to Dee Company for $15,000. Dee Company signed a note for

$15,000 that is due in 60 days. The journal entry prepared by Darin Company to record

the sale of the property would include which of the following?

A) Credit to Note Receivable

B) Debit to Cash

C) Credit to Land

D) Debit to Accounts Payable

During the current year, a company paid $4,500 which it owed from its prior year

income tax liability and $30,000 for its current year tax liability. The company still

owes $6,000 at the end of the current year. How much should the company report as

cash paid for income taxes on its statement of cash flows for the current year?

A) $34,500

B) $40,500

C) $30,000

D) $3,500

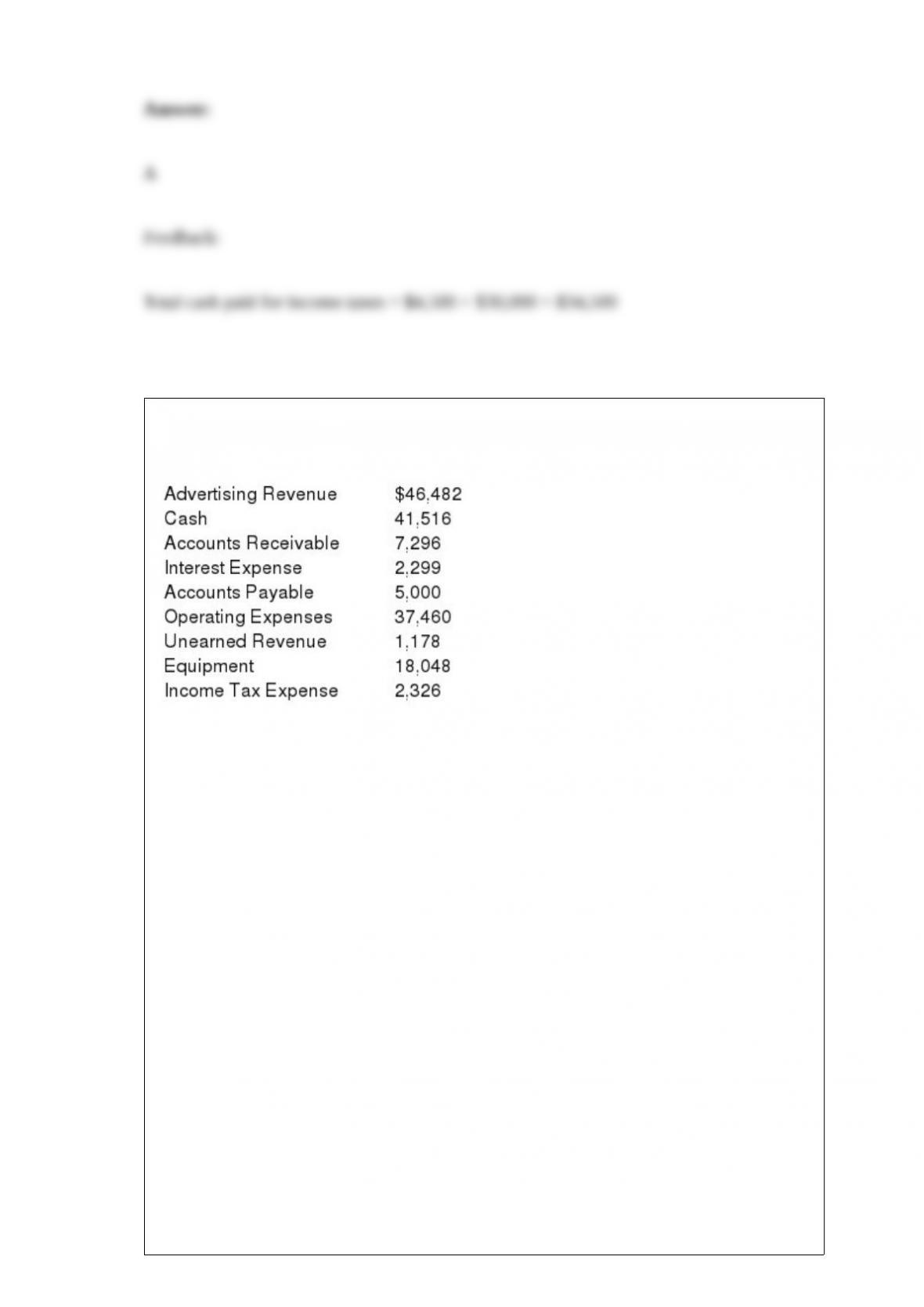

The following account balances are taken from the December 31, 2015, financial

statements of ABZ Advertising Company. The company uses accrual basis accounting.

The following activities occurred in 2016:

1> Performed advertising services on account, $55,000.

2> Received cash payments on account, $10,400.

3> Received deposits from customers for advertising services to be performed in 2017,

$2,500.

4> Made payments to suppliers on account, $5,000.

5> Incurred $45,000 of operating expenses; $39,000 was paid in cash and $6,000 was

on account and unpaid as of the end of the year.

Use the information above to answer the following question. What is the balance of

Accounts Receivable at December 31, 2016?

A) $51,896.

B) $55,000.

C) $44,600.

D) $54,396.

The MegaHit Film Studio has a licensing right (or agreement) to distribute films

produced by the Artsy Film Company. How would the MegaHit Company classify this

licensing right?

A) Tangible asset

B) Research and development

C) Intangible asset

D) Fixed asset

Employee fraud includes all of the following categories except:

A) asset misappropriation.

B) corruption.

C) deception.

D) financial statement fraud.

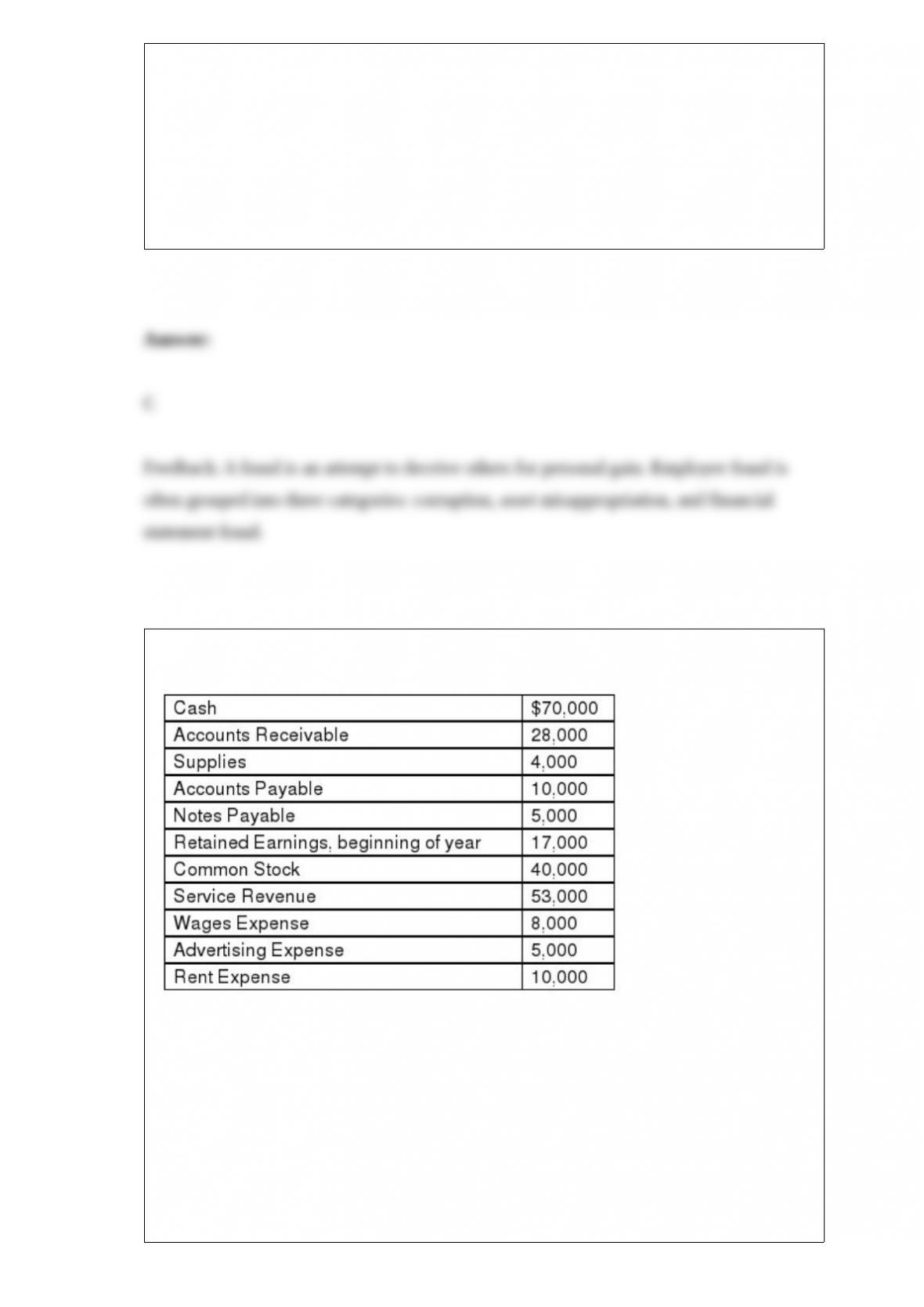

A company’s financial records at the end of the year including the following amounts:

Use the information above to answer the following question. What is the amount of net

income on the income statement for the year?

A) $30,000.

B) $38,000.

C) $88,000.

D) $47,000.

Which of the following statements about revenue and expense accounts is correct?

A) Revenue accounts are a subset of assets, and expense accounts are subcategories of

liabilities.

B) Both revenue accounts and expense accounts are subcategories of assets.

C) Both revenue accounts and expense accounts are subcategories of Retained

Earnings.

D) Revenue accounts are a subcategory of Cash and expense accounts are a subcategory

of Accounts Payable.

Which transaction would be reported on the income statement for the current year?

A) The revenue earned from selling sold goods in the current year to customers who

have not yet paid for those goods (that is, they have promised to pay for those goods

next year).

B) The amount of cash received from customers this year as payment for goods that

were sold to those customers last year.

C) The proceeds from a borrowing from the bank that was to be used to finance

business activities during the current year.

D) The proceeds from the issuance of common stock to owners that was to be used to

finance business activities during the current year.

On December 1, 2015, a company converted an existing account receivable in the

amount of $6,000 to a note receivable to allow an extended payment period. The note is

due in three months and includes an annual interest rate of 9%, The company prepares

year-end financial statements on December 31 and recorded adjusting entries at that

time. What entry should the company make on March 1, 2016, when the interest is paid

at maturity?

A) Debit Cash and credit Notes Receivable for $6,135

B) Debit Cash for $6,135, credit Notes Receivable for $6,000, and credit Interest

Revenue for $135

C) Debit Cash for $135, credit Interest Receivable for $45, and credit Interest revenue

for $90

D) Debit Cash for $135, credit Interest Receivable for $45, and credit Interest Revenue

for $90