Auditors play an important role in the resource allocation process by adding credibility

to financial statements.

The cost-to-retail percentage used in the retail method to approximate average cost

incorporates both markdowns and markups.

Demolition costs to remove an old building from land purchased as a site for a new

building are considered part of the cost of the new building.

Premium on bonds payable is a contra liability account.

Routine transfers of debt and equity investments among the trading, available for sale,

and held to maturity portfolios need not be disclosed in the financial statements.

Revenue from the sale of computer software is always recognized at the point of sale.

Paid-in capital is increased when bonds payable are issued with detachable stock

purchase warrants.

There almost always is a balance sheet liability for plans of postretirement benefits

other than pensions since very few of these plans are funded.

A fee for recording a new customer in the seller’s information system should be treated

as a separate performance obligation and should be recognized upon payment.

When recognizing revenue over time on a long-term contract, the percent complete is

often estimated by comparing the cost incurred to date with the total estimated cost to

complete.

The transaction price should be allocated to the contract’s performance obligations in

proportion to the stand-alone selling prices of the performance obligations.

If an option to purchase an extended warranty at a special discount is included with a

product when the product is purchased, a portion of the contract price needs to be

allocated to the option.

The revenue/expense approach emphasizes:

a. Recognition of revenues.

b. Recognition of expenses.

c. The income statement.

d. All of the above are correct.

An asset that is generally not expected to be converted to cash or consumed within one

year or the operating cycle is:

a. Building.

b. Accounts receivable.

c. Inventory.

d. Supplies.

On June 30, 2016, Prego Equipment purchased a precision laser-guided steel punch that

has an expected capacity of 300,000 units and no residual value. The cost of the

machine was $450,000 and is to be depreciated using the units-of-production method.

During the six months of 2016, 24,000 units of product were produced. At the

beginning of 2017, engineers estimated that the machine can realistically be used to

produce only another 230,000 units. During 2017, 70,000 units were produced. Prego

would report depreciation in 2016 of:

a. $36,000.

b. $43,900.

c. $18,000.

d. $21,950.

Disclosure notes would not include:

a. Depreciation methods used and estimated useful life.

b. Definition of cash equivalents.

c. Details of pension plans.

d. Data to adjust the financial statements so that they are not misleading.

Which of the following is not a current liability?

a. Accounts payable.

b. A note payable due in two years.

c. Accrued interest payable.

d. Sales tax payable.

Reporting comprehensive income can be accomplished by each of the following

methods except:

a. In the statement of shareholders’ equity.

b. A single, continuous statement of comprehensive income.

c. In two separate, but consecutive statements.

d. All of the above are acceptable methods.

The retained earnings balance reported in the balance sheet typically is not affected by:

a. Net income.

b. A prior period adjustment.

c. Dividends paid.

d. Restrictions.

When preparing a statement of cash flows using the direct method, accrual of payroll

expense is:

a. Reported as an operating activity.

b. Reported as an investing activity.

c. Reported as a financing activity.

d. None of these answer choices is correct.

When computing diluted earnings per share, which of the following will not be

considered in the calculation?

a. Dividends paid on common stock.

b. The weighted average common shares.

c. The effect of stock splits.

d. The number of common shares represented by stock purchase warrants.

Estimate the stand-alone selling price of the software using the residual approach.

a. $50

b. $80

c. $90

d. $97.50

A change that uses the prospective approach is accounted for by:

a. Implementing it in the current year.

b. Reporting pro forma data.

c. Retrospective restatement of all prior financial statements in a comparative annual

report.

d. Giving current recognition of the past effect of the change.

In the balance sheet at the end of its first year of operations, Dinty Inc. reported an

allowance for uncollectible accounts of $82,000. During the year, Dinty wrote off

$32,000 of accounts receivable it had attempted to collect and failed. Credit sales for

the year were $2,200,000, and cash collections from credit customers totaled

$1,950,000.

What bad debt expense would Dinty report in its first-year income statement?

a. $ 50,000.

b. $ 82,000.

c. $114,000.

d. Can’t be determined from the given information

Accounting for postretirement health care benefits is similar, in most respects, to

accounting for:

a. Payroll taxes.

b. Health insurance costs for current employees.

c. Pension benefits.

d. Sick pay and vacation pay.

When a company’s only potential common shares are convertible bonds:

a. Diluted EPS will be greater if the bonds are actually converted than if they are not

converted.

b. Diluted EPS will be smaller if the bonds are actually converted than if the bonds are

not converted.

c. Diluted EPS will be the same whether or not the bonds are converted.

d. The effect of conversion on diluted EPS cannot be determined without additional

information.

Long-term solvency refers to:

a. The efficiency with which a company manages its resources.

b. The profitability of a company for a period of time.

c. The amount of current assets relative to long-term assets.

d. The riskiness of a company with regard to the amount of liabilities in its capital

structure.

Paid-in capital in excess of par is reported:

a. As a reduction of shareholders’ equity.

b. As a noncurrent asset.

c. As a noncurrent liability.

d. As an increase in shareholders’ equity.

When the equity method of accounting for investments is used by the investor, the

amortization of additional depreciation due to differences between book values and fair

values of investee assets on the date of acquisition:

a. Reduces the investment account and increases investment revenue.

b. Increases the investment account and increases investment revenue.

c. Reduces the investment account and reduces investment revenue.

d. Increases the investment account and reduces investment revenue.

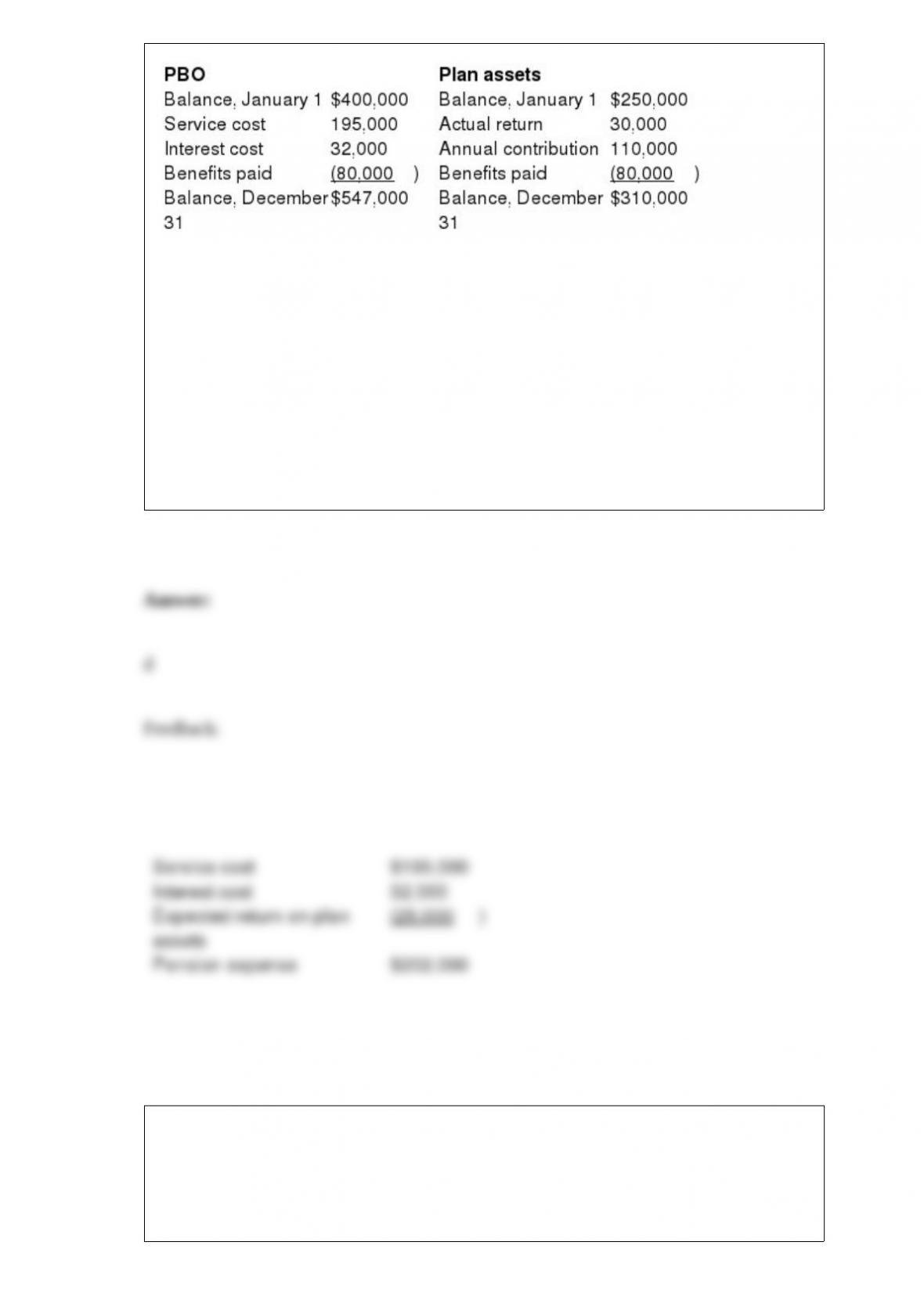

Scallion Company received the following reports of its defined benefit pension plan for

the current calendar year:

The long-term expected rate of return on plan assets is 10%. Assuming no other data are

relevant, what is the pension expense for the year?

a. $197,000.

b. $227,000.

c. $172,000.

d. $202,000.

Which of the following is a contingency that should be accrued?

a. The company is being sued and a loss is reasonably possible and reasonably

estimable.

b. The company deducts life insurance premiums from employees’ paychecks.

c. The company offers a two-year warranty and the expenses can be reasonably

estimated.

d. It is probable that the company will receive $100,000 in settlement of a lawsuit.

Below is a list of accounts in no particular order. Assume that all accounts have normal

balances. Required: In column A, indicate whether a debit will:

1> Increase the account balance, or

2> Decrease the account balance. In column B, classify each account according to the

following scheme. For contra accounts, indicate the classification of the account to

which it relates.

1>A current asset in the balance sheet.

2>A noncurrent asset in the balance sheet.

3>A current liability in the balance sheet.

4>A long-term liability in the balance sheet.

5>A permanent equity account in the balance sheet.

6>A revenue account in the income statement.

7>An expense account shown in the income statement.

8> Account does not appear in either the balance sheet or the income statement.

Capital stock

Listed below are 10 terms followed by a list of phrases that describe or characterize the

terms. Match each phrase with the number for the correct term.

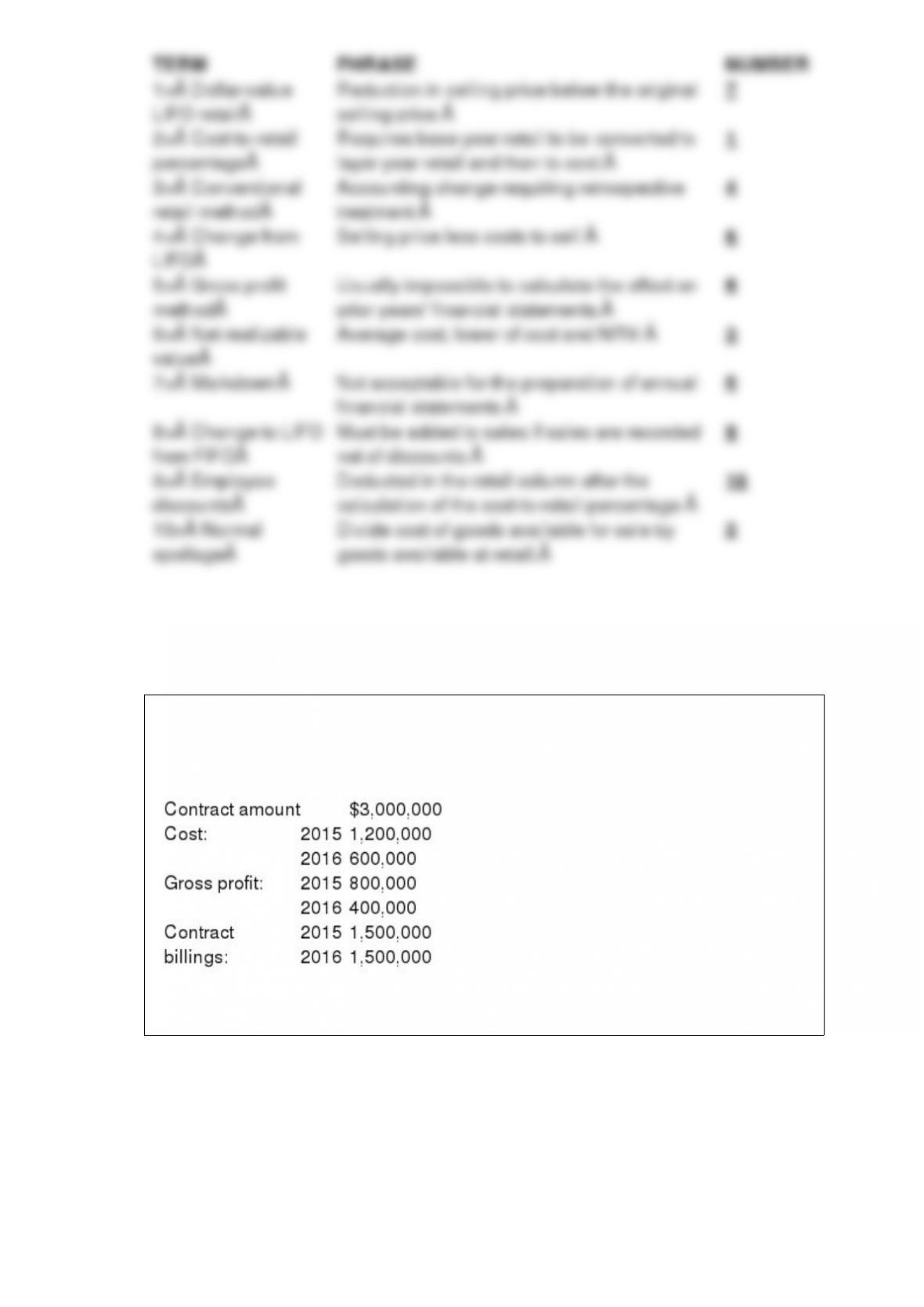

Sahara Desert Homes (SDH) reports under IFRS and constructed a new subdivision

during 2015 and 2016 under contract with Cactus Development Co. Relevant data are

summarized below:

SDH uses the cost recovery method under IFRS to recognize revenue. What is the

journal entry in 2015 to record revenue?

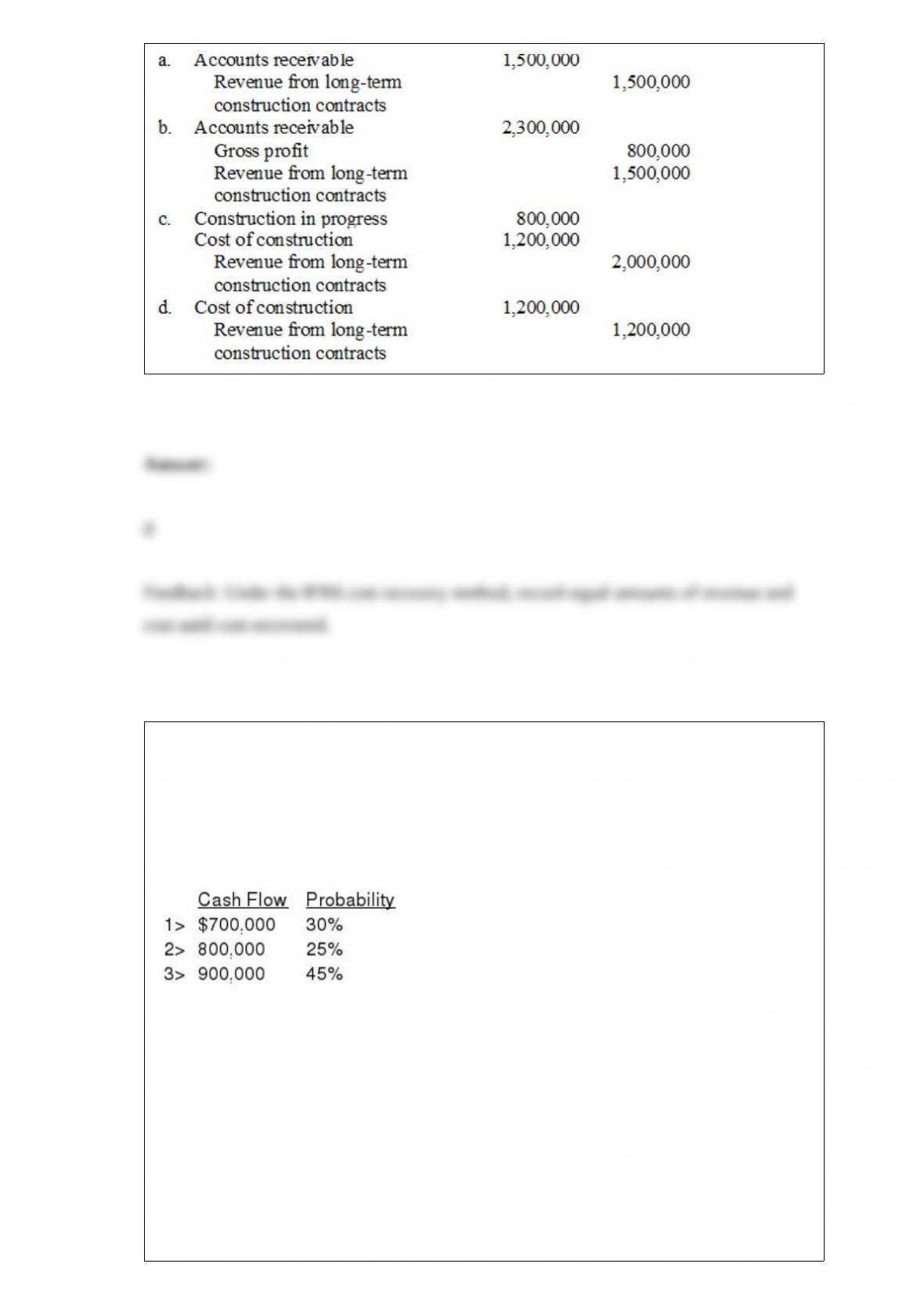

Schefter Mining operates a copper mine in Wyoming. Acquisition, exploration, and

development costs totaled $8.2 million. Extraction activities began on July 1, 2016.

After the copper is extracted in approximately six years, Schefter is obligated to restore

the land to its original condition, including constructing a park. The company’s

controller has provided the following three cash flow possibilities for the restoration

costs:

The company’s credit-adjusted, risk-free rate of interest is 5%, and its fiscal year ends

on December 31

Required:

1> What is the initial cost of the copper mine? (Round computations to nearest whole

dollar.)

2> How much accretion expense will Schefter report in its 2016 income statement?

3> What is the book value of the asset retirement obligation that Schefter will report in

its 2016 balance sheet?

4> Assume that actual restoration costs incurred in 2022 totaled $860,000. What

amount of gain or loss will Schefter recognize on retirement of the liability?

Watson Company purchased assets of Holmes Ltd. at auction for $1,300,000. An

independent appraisal of the fair value of the assets acquired is listed below:

Required:

Prepare the journal entry to record the purchase of the assets.

Describe the approaches of reporting changes in accounting principles.

Kramer Inc. had 95 million shares of common stock, 1 million shares of 6%, $100 par,

cumulative preferred stock, and 1 million shares of 8%, $100 par, noncumulative

preferred stock outstanding at the end of 2015 and 2016. No dividends were declared or

paid on common stock in either year. In 2016, a $3 million dividend was paid on the 6%

preferred stock and a $4 million dividend was paid on the 8% preferred stock. Net

income for 2016 was $300 million. The company’s tax rate is 30%.

Required:

Compute basic earnings per share (rounded to 2 decimal places) for the year ended

December 31, 2016.

Rite Shoes was involved in the transactions described below.

Required: Prepare the appropriate journal entry for each transaction. If an entry is not

required, state “No Entry.”

1> Purchased $8,200 of inventory on account.

2> Paid weekly salaries and wages, $920.

3> Recorded sales for the first week: Cash: $7,100; On account: $5,300.

4> Paid for inventory purchased in event (1).

5> Placed an order for $6,200 of inventory.

Bascomb Company purchased $420,000 in merchandise on account during the month

of April, and merchandise costing $350,000 was sold on account for $425,000.

Required:

1> Prepare journal entries to record the purchases and sales assuming Bascomb uses a

perpetual inventory system.

2> Prepare journal entries to record the purchases and sales assuming Bascomb uses a

periodic inventory system.