The scope paragraph of the standard unqualified audit report in the auditor

responsibility section states that the audit is designed to

A) discover all errors and/or irregularities.

B) discover material errors and/or irregularities.

C) obtain reasonable assurance whether the statements are free of material

misstatement.

D) conform to a generally accepted financial reporting framework.

Which one of the following is a professional standard that must be followed by an

accountant when conducting a compilation engagement?

A) work being adequately planned and properly executed

B) having adequate technical training and proficiency in auditing

C) obtaining an adequate understanding of the business and its industry

D) documenting the processes used to compile and record transactions

The tests of details of balances procedure which requires the auditor to examine notes

paid after year-end to determine whether they were liabilities at the balance sheet date is

an attempt to satisfy the audit objective of

A) existence.

B) completeness.

C) accuracy.

D) classification.

Which of the following situations would indicate a susceptibility at the client to the

potential of fraud that pertains to theft of cash?

A) lack of segregation of duties between the handling of cash and the recording of cash

B) cash disbursements cheques requiring only one authorizing signature

C) payroll rates being approved by the corporate controller

D) customer master file changes being handled by the controller’s executive assistant

Who is responsible for developing financial statement audit and assurance standards in

Canada?

A) AASB (Auditing and Assurance Standards Board)

B) Standards staff at the CICA (Canadian Institute of Chartered Accountants)

C) National accounting bodies such as CGA Canada

D) The accounting firms who conduct financial statement audits

Which of the following is an example of auditing rather than accounting?

A) recording purchase amounts in the expense accounts

B) posting the daily sales totals to the general ledger

C) recording cash received in the customer account files

D) evaluating whether accounts receivable are collectible

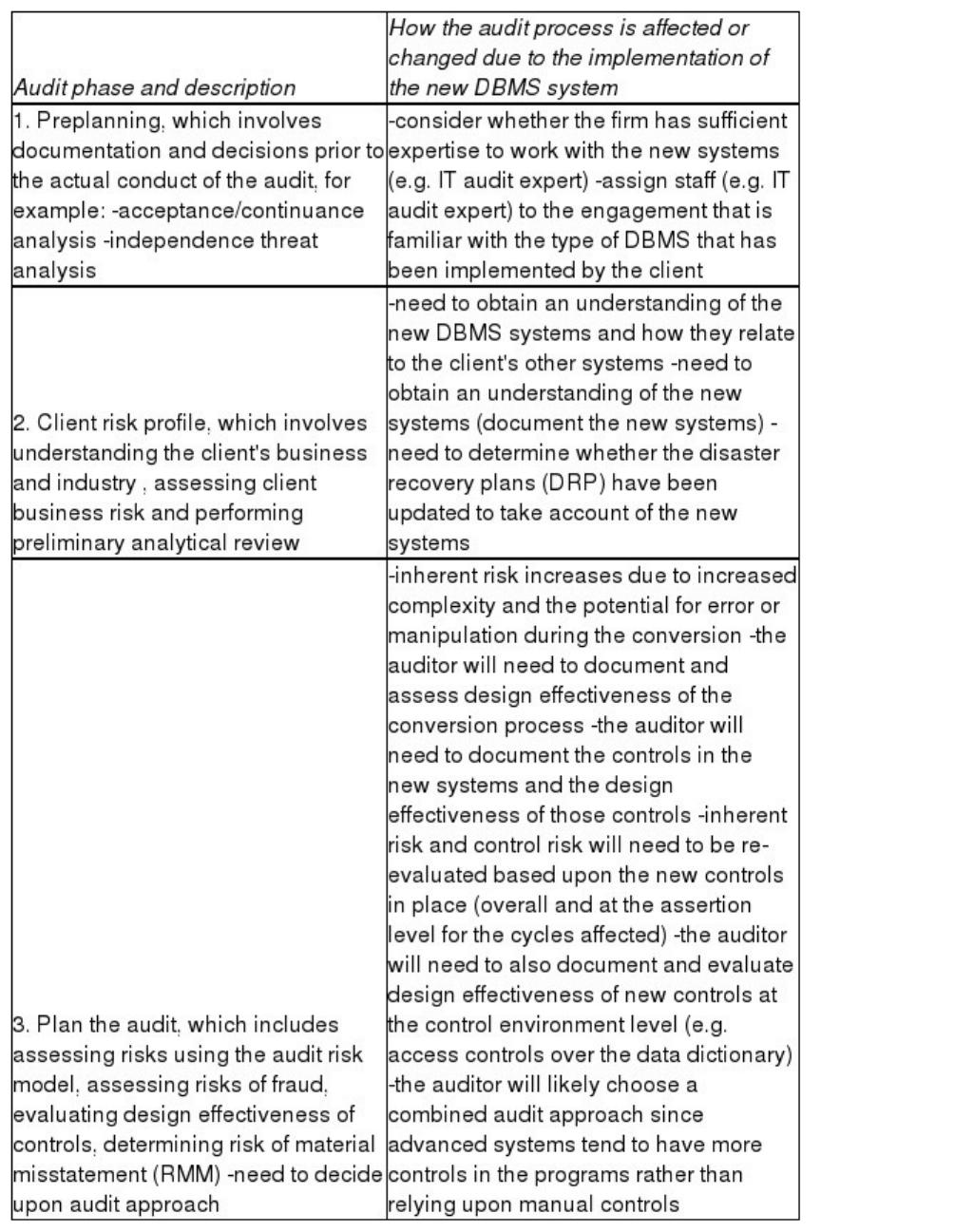

Restaurant Products Company (RPC) has been an audit client of your firm for many

years. RPC has a March 31 fiscal year end. The company is a successful distributor of

restaurant and food industry products, such as trays, weigh scales, dishes, cooking

implements. The company sells to businesses only (i.e. not to end consumers), with

clients ranging from small restaurants to large food service chains and hotels. The

company does have a perpetual inventory system, but the current inventory system

relies upon accurate data entry of receipts, shipments and inventory adjustments from

paper documents.

RPC is looking to improve inventory management and maintain costs in the face of

rising competition and growth. Accordingly, it is implementing RFID (radio frequency

identification) technology for its inventory in January 2012. RFID chips will be placed

on warehouse shelf locations, boxes of products, and on large cost individual products.

At the same time the company will implement a wireless mesh system throughout the

warehouse, with wireless tracking of product movement. Effective January 31, 2012 a

new inventory management system is being implemented to facilitate better decision

making and access to online realtime inventory data. The new inventory management

system will include a new database that will include internal records of inventory on

hand, receipts and shipments of inventory, purchase order details, and payment details.

Required:

A. For each phase of the financial statement audit process, describe the phase, and

explain how the audit process is affected or changed due to the implementation of the

new database management system.

B. What is the impact of the implementation of RFID on the financial statement audit

process?

[Note that these points must be different from those raised in Part A above.]

One of the purposes of developing a client risk profile is to assist the auditor in

A) developing the pertinent audit procedures for tests of internal controls.

B) assessing the client’s business risk.

C) locating related parties that need to be disclosed.

D) deciding whether fraud or illegal acts have taken place.

Canadian PAs are required to have controls in place to identify and track suspicious

transactions and comply with the reporting requirements of the Proceeds of Crime and

Terrorist Financing Act. This Act requires PAs to report to FINTRAC any

A) cash payment of $10,000 or more.

B) cash payment of $100,000 or more.

C) transaction of $1,000 or more from clients suspected of being terrorists.

D) cash payment to a related party.

The rules of accounting bodies in Canada require their members to behave in the best

interest of the profession and the public. Identify the situation where the accountant is

acting in the best interest of the profession. An accountant

A) reports a fellow accountant after noticing that the accountant helped a client with tax

evasion.

B) openly criticizes a fellow accountant’s competencies after having lost a bid for a new

client.

C) brags about his competence and professional title, and encourages clients to invest in

a new venture he is starting.

D) refuses to cooperate with the new auditor after having lost a client.

When a company uses purchased software packages for its accounting software, such

packages normally do not permit the company to change the software package’s

functionality. This means that the auditor will consider

A) access controls as being poor.

B) program change controls as poor.

C) program change controls as excellent.

D) access controls as being excellent.

Kumar is the internal auditor of Tarragon Inc. Kumar wants to put procedures in place

in order to prevent misstatements in owners’ equity and ensure proper record keeping.

Kumar suggested that management implements well-defined policies for preparing

stock certificates and recording capital stock transaction. What else should Kumar

recommend?

A) Independent internal verification of information in the records

B) Having all journal entries in the equity account reviewed by the controller

C) Perform a monthly reconciliation of shareholder’s equity

D) Reconcile the dividend payments with the bank statement

Which of the following statements best describes the position of cash on the balance

sheet at most organizations that utilize effective cash management practices? It is

usually

A) immaterial.

B) highly material.

C) dispersed among many different accounts.

D) affected by many different capital asset accounts.

Because of the lack of available evidence, it is usually difficult for an auditor to

discover if an employee records more time on his or her time card than actually worked.

One procedure is to reconcile the total hours

A) paid this period with a previous period.

B) paid according to the payroll records with an independent record of the total hours

worked, such as those maintained by production control.

C) worked this period with a previous period.

D) worked according to the summary payroll report with the total hours worked as

recorded on the time card for the period.

The auditor traces items from the source documents to the journals in order to satisfy

the

A) existence objective.

B) completeness objective.

C) accuracy objective.

D) classification objective.

PA recently finished the audit of a family-owned business. Now, she is working on a

large client with about 50 times the assets and 30 times total revenue. For the larger

client, PA will likely have

A) no effect on the audit risk model.

B) higher control risk.

C) higher audit risk.

D) lower audit risk.

Sample size in physical observation of inventory is

A) determined using attributes sampling.

B) determined using variables sampling.

C) determined using dollar-unit sampling.

D) difficult to specify because the emphasis is on observing client’s procedures.

Dimitri works at a large public accounting firm. Dimitri referred one of his friends for a

junior auditor position. Dimitri’s friend was hired despite the fact that he had a criminal

record dating from 3 years ago. The partner did not perform a background check on

Dimitri’s friend since he was recommended by an employee. Which element of quality

control is compromised?

A) General ethical requirements

B) Independence

C) General human resource policies

D) Engagement performance

Master file data is the semi-permanent data in an employee’s file. Changes to master file

changes

A) should be adequately supported.

B) should be checked by the originator.

C) would be entered only once per month.

D) would be implemented on an annual basis.

In which of the following circumstances would a public accountant be bound by ethics

to refrain from disclosing any confidential information obtained during the course of a

professional engagement?

A) The public accountant is issued a subpoena that orders the public accountant to

present confidential information.

B) A major shareholder of a client company seeks accounting information from the

public accountant after management declined to disclose the requested information.

C) Confidential client information is made available as part of a practice inspection of

the public accountant’s practice.

D) An inquiry by a disciplinary body of a provincial institute requests confidential

client information.

There are three main types of revenue manipulations. Which of the following revenue

manipulations affects the cutoff objective?

A) avoiding recording of returns and allowances for the year

B) recording subsequent period sales as current period sales

C) understatement of bad debts

D) creation of fictitious sales that are misclassified as revenue

A major benefit of computerized analytical procedures is the

A) ease of doing the calculations.

B) ease of updating the calculations.

C) ease of correcting math calculations.

D) ability to push the work down to lower levels of the audit staff to do the analysis.

When reading the corporate minutes, the auditor extracted the approved annual salary

for the President, the Chief Executive Officer and other senior executives. What audit

step would the auditor likely conduct with this information?

A) trace the payroll amount to each individual officer’s payroll record

B) check that the payroll has been recorded into the correct bank account

C) verify that payroll cheques have two signatures for all large amounts

D) ensure that all overtime is approved and adequately documented

When an auditor allocates materiality to segments, then the materiality amount for

different accounts under audit will

A) potentially differ from each other.

B) require the same level of unanticipated misstatements.

C) require the same amount of audit work.

D) be the same for each account audited.

There is a direct relationship between the interest and dividend accounts and debt and

equity. This means that in the audit of interest-bearing debt, it is desirable to

simultaneously verify

A) the related dividends declared and dividends payable.

B) the related interest expense and interest payable.

C) contracts and commitments that are long-term.

D) details provided in the Board of Directors’ minutes.

Management assertions are

A) directly related to auditing standards.

B) directly related to accounting standards.

C) indirectly related to auditing standards.

D) indirectly related to accounting standards.

A client acquired 25% of its outstanding capital stock after year-end and prior to

completion of the auditor’s fieldwork. The auditor should

A) advise management to adjust the balance sheet to reflect the acquisition.

B) issue pro forma financial statements giving effect to the acquisition as if it had

occurred at year-end.

C) advise management to disclose the acquisition in the notes to the financial

statements.

D) disclose the acquisition in the opinion paragraph of the auditor’s report.

Which of the following services results in the placement of an electronic seal affixed to

the web site?

A) review engagement

B) internal controls assessment

C) SysTrust

D) WebTrust

What is the best way to prevent potential alteration, deletion or addition of cancelled

cheques, duplicate deposit slips or other documents provided with the bank statement?

Have the

A) bank statements provided unopened to an independent reconciler.

B) person responsible for recording cash receipts does the bank reconciliation.

C) signing officer(s) review the bank reconciliation.

D) bank statements are provided to the accounts payable supervisor.

The most authoritative requirements for public accountants performing financial

statement audits in Canada are the

A) standards used by the client.

B) industry specific standards.

C) CICA handbook requirements.

D) assurance guidelines.