1) Which balance-related audit objective cannot be assessed using monetary unit

sampling?

A) Accuracy

B) Completeness

C) Existence

D) All of the above can be assessed using monetary unit sampling.

2) The acquisition and payment cycle is highly controlled and not well-structured in

most companies.

A) True

B) False

3) The principal issue to be resolved in cases involving alleged negligence is usually:

A) the amount of the damages suffered by plaintiff

B) whether to impose punitive damages on defendant

C) the level of care exercised by the CPA

D) whether defendant was involved in fraud

4) For financial auditing, the audit report typically goes to many users of financial

statements, whereas operational audit reports are intended primarily for management.

A) True

B) False

5) Substantive tests of transactions and control tests are often conducted

simultaneously.

A) True

B) False

6) Which of the following is not a difference between operational auditing and financial

auditing?

A) Both must be CPAs

B) Operational audit reports are usually of a restricted distribution while financial audit

reports are widely distributed

C) Operational audits often cover non-financial issues while financial audits do not

D) None of the above is a difference

7) The net realizable value of accounts receivable is equal to:

A) gross accounts receivable less allowance for uncollectible accounts

B) gross accounts receivable less bad debt expense

C) gross accounts receivable less returns and allowances

D) gross accounts receivable less sales discounts

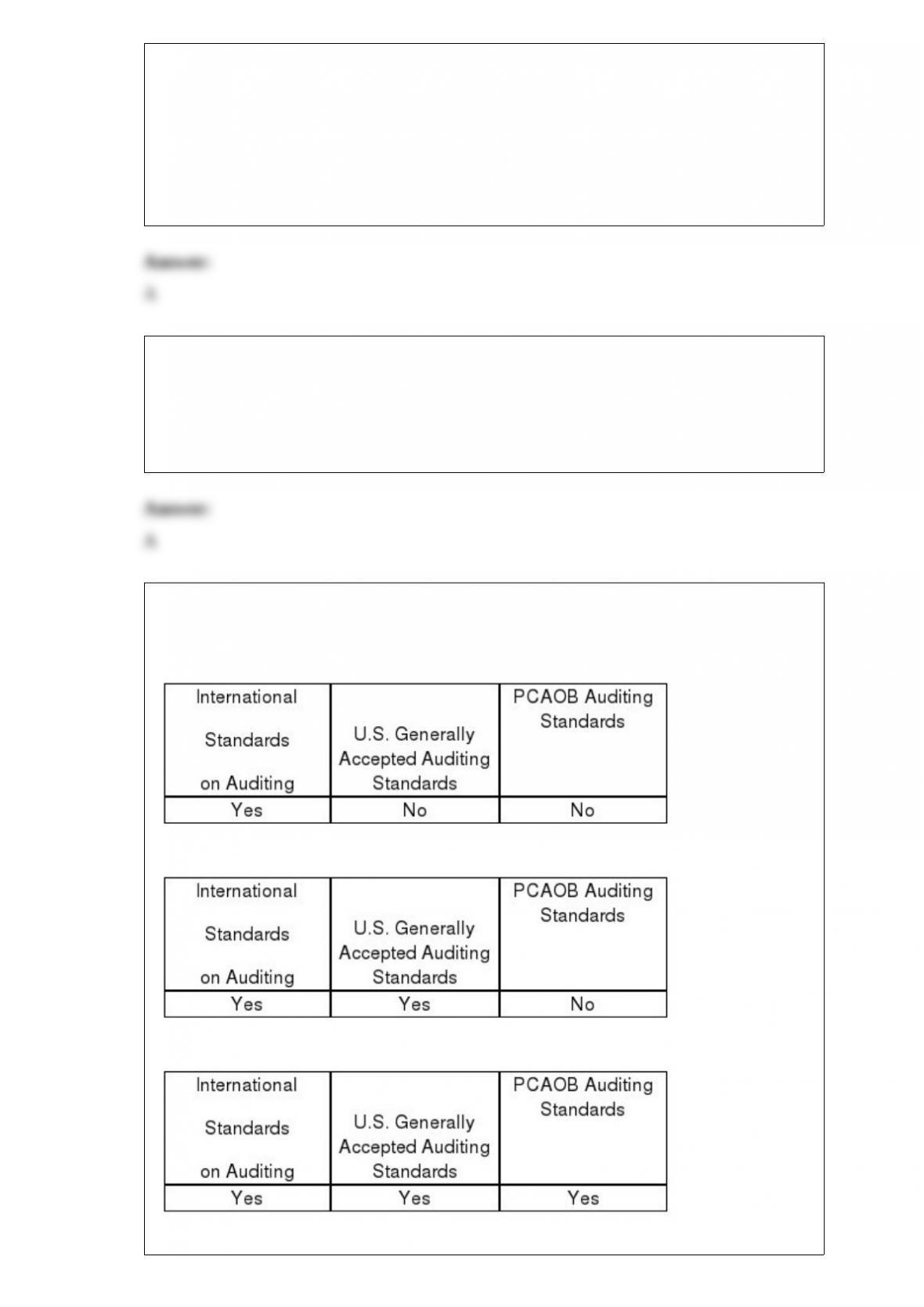

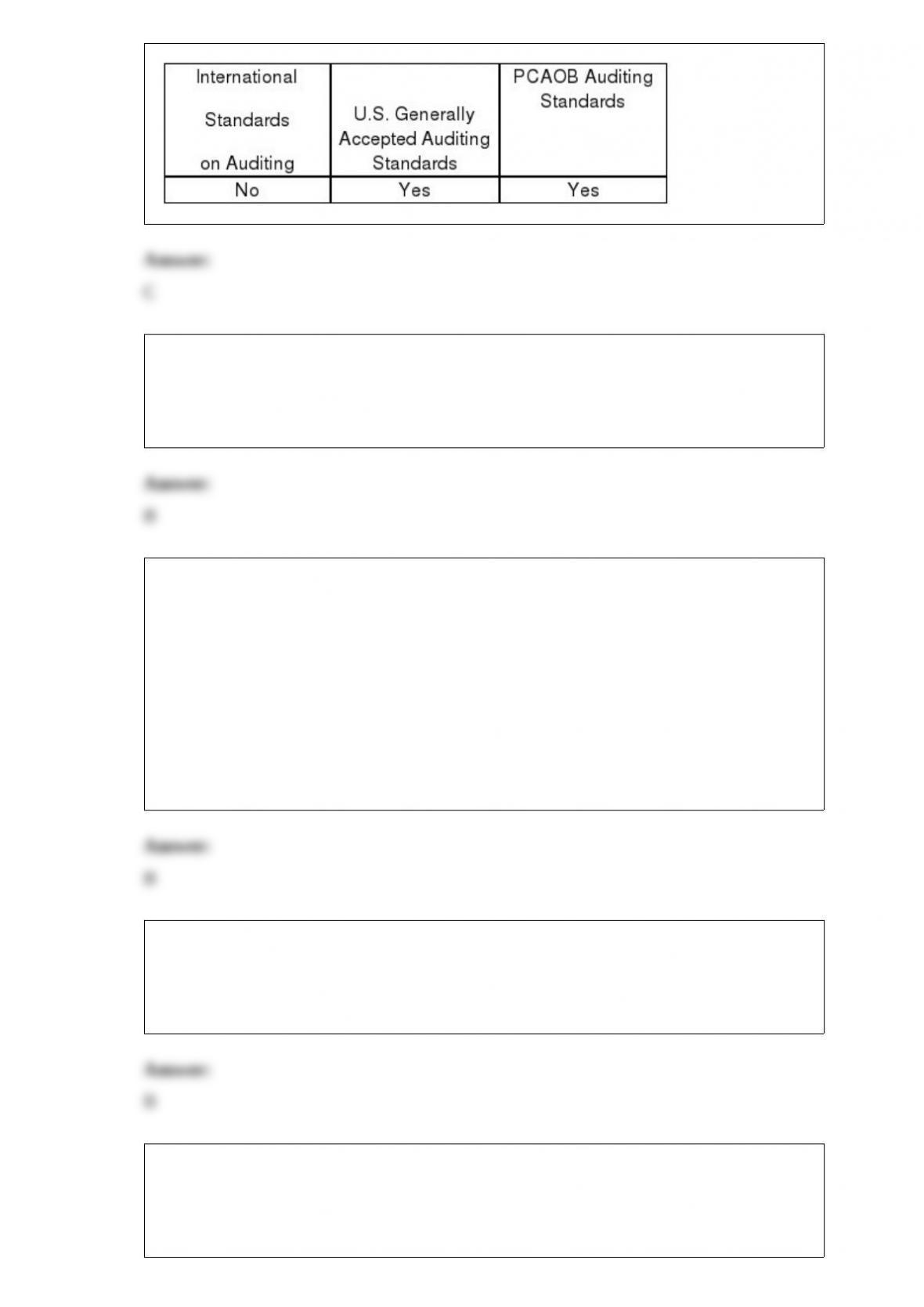

8) Which of the following are audit standards used in professional practice by audit

firms?

A)

B)

C)

D)

9) Two categories of audit-relevant information found in corporate code of ethics are

authorizations and discussions of matters affecting inherent risk.

A) True

B) False

10) Attestation services on information technology include WebTrust services and

SysTrust services. Which of the following statements most accurately describes

SysTrust services?

A) SysTrust services provide assurance on business processes, transaction integrity and

information processes

B) SysTrust services provide assurance on system reliability in critical areas such as

security and data integrity

C) SysTrust services provide assurance on internal control over financial reporting

D) SysTrust services provide assurance as to whether accounting personnel are

following procedures prescribed by the company controller

11) The Securities and Exchange Commission requires companies listed on exchanges

to employ stock transfer agents.

A) True

B) False

12) A CPA firm may practice public accounting only in a form of organization

permitted by federal law or regulation.

A) True

B) False

13) Which of the following statements is false?

A) The payroll cycle consists of one class of transactions

B) Balance sheet accounts related to payroll are generally more significant than related

transactions

C) Internal controls over payroll are effective for most companies

D) Small companies usually have effective controls over payroll

14) Practitioners who perform reviews and compilations are referred to in the SSARS

standards as:

A) bookkeepers

B) accountants

C) auditors

D) CPAs

15) Tests for kiting are performed using only a schedule of intrabank transfers.

A) True

B) False

16) Commitments include all but which of the following?

A) agreements to purchase raw materials

B) pension plans

C) agreements to lease facilities at set prices

D) Each of the above is a commitment.

17) Which of the following is an element of the CPA’s quality control system that

should be considered in establishing it’s quality control policies and procedures?

A) Considering audit risk and materiality

B) Using statistical sampling techniques

C) Assigning personnel to engagements

D) Complying with laws and regulations

18) A common way for a CPA firm to demonstrate its lack of duty to perform is by use

of a(n):

A) expert witness’ testimony

B) audit contract, or engagement letter

C) management representation letter

D) confirmation letter

19) When planning the audit, if the auditor has no reason to believe that illegal acts

exist, the auditor should:

A) include audit procedures which have a strong probability of detecting illegal acts

B) still include some audit procedures designed specifically to uncover illegalities

C) ignore the issue

D) make inquiries of management regarding their policies for detecting and preventing

illegal acts and regarding their knowledge of violations, and then rely on normal audit

procedures to detect errors, irregularities, and illegalities

20) A CPA firm can issue a compilation report:

A) only if the partners are independent

B) only if all the partners and the staff in the office performing the engagement are

independent

C) if the partners have no material or direct immaterial interest in client

D) even if it is not independent

21) Rule 101, Independence, applies to members of the

A) True

B) False

22) Smaller privately held companies may not maintain an accounts payable master file

by vendor. These companies pay on the basis of:

A) vendors’ monthly statements

B) individual vendors’ invoices

C) the accounts payable account in the general ledger

D) dunning letters

23) The standard letter of inquiry to the client’s legal counsel should be prepared on:

A) plain paper (no letterhead) and be unsigned

B) lawyer’s stationery and signed by the lawyer

C) auditor’s stationery and signed by an audit partner

D) client’s stationery and signed by a company official

24) Errors are usually more difficult for an auditor to detect than frauds.

A) True

B) False

25) Depreciation expense is normally verified as a part of tests of details of balances

rather than as part of tests of controls or substantive tests of transactions.

A) True

B) False

26) While performing a substantive test of details during an audit, the auditor

determined that the sample results supported the conclusion that the recorded account

balance was not materially misstated. It was, in fact, materially misstated. This situation

illustrates the risk of:

A) incorrect rejection

B) incorrect acceptance

C) assessing control risk too low

D) assessing control risk too high

27) Credit memos are normally issued for what purpose(s)?

A) To adjust the customers balance to the amount owed to the company

B) To assist in the aging of accounts receivable

C) To reduce customer frustration and sales losses

D) To inform the customer of the balance due

28) Confirmations are commonly used to verify additions of property, plant, and

equipment.

A) True

B) False

29) Management and the board of directors are responsible for setting the “tone at the

top.”

A) True

B) False

30) Evidence is generally considered appropriate when:

A) it has been obtained by random selection

B) there is enough of it to afford a reasonable basis for an opinion on financial

statements

C) it has the qualities of being relevant, objective, and free from known bias

D) it consists of written statements made by managers of the enterprise under audit

31) Johnson Co.’s physical count of inventories was lower than the inventory quantities

shown in its perpetual records. This situation could be the result of the failure to record:

A) sales

B) sales returns

C) purchases

D) purchase discounts

32) The Private Securities Litigation Reform Act of 1995 reduced potential damages in

securities-related litigation, but because the act applied only to federal courts, attorneys

began taking cases to state courts. Which of the following eliminated this loophole?

A) Private Securities Litigation Reform Amendment

B) Securities Litigation Uniform Standards Act of 1998

C) Racketeer Influenced and Corrupt Organization Act

D) U.S. Securities Claims Reform Act

33) The cutoff objective, “transactions near the balance sheet date are recorded in the

proper period,” is a balance-related audit objective.

A) True

B) False

34) Program audits are primarily focused on inefficient uses of federal funds in

sponsored programs.

A) True

B) False