LIFO periodic and LIFO perpetual always produce the same dollar amounts for ending

inventory.

Under the LIFO retail method, the current period cost-to-retail percentage includes both

net markdowns and net markups.

The income statement summarizes the operating activity of a firm at a particular point

in time.

When recognizing revenue over time on a long-term contract, amounts billed and the

cash actually received affect income recognition.

Net realizable value is selling price less costs of completion, disposal, and

transportation.

Cost of goods sold as reported in the income statement will be less than cash paid to

suppliers if:

a. The increase in accounts payable is greater than the increase in inventory during the

period.

b. The decrease in accounts payable is equal to the increase in inventory during the

period.

c. The decrease in accounts payable is less than the decrease in inventory during the

period.

d. The increase in accounts payable is equal to the decrease in inventory during the

period.

If the lessor retains title to leased property under the terms of the lease:

a. The amount to be recovered through periodic lease payments is reduced by the

present value of the residual amount.

b. The amount to be recovered through periodic lease payments is increased by the

present value of the residual amount.

c. The amount to be recovered will be the same as if there were no residual value.

d. The lessor will record a greater amount of depreciation due to the residual value.

Selected information from Large Corporation’s accounting records and financial

statements for 2016 is as follows ($ in millions):

Large prepares its financial statements in accordance with IFRS. In its statement of cash

flows, Large most likely reports net cash outflows from investing activities of:

a. $18 million.

b. $28 million.

c. $38 million.

d. $68 million.

Under the retail method, the denominator in the cost-to-retail percentage does not

include:

a. Purchases.

b. Purchase returns.

c. Abnormal shortages.

d. Freight-in.

Outstanding common stock is:

a. Stock that is performing well on the New York Stock Exchange.

b. Stock that has been authorized by the state for issue.

c. Stock held in the corporate treasury.

d. Stock in the hands of shareholders.

Pension gains related to plan assets occur when:

a. The return on plan assets is higher than expected.

b. The vested benefit obligation is less than expected.

c. Retiree benefits paid out are less than expected.

d. The accumulated benefit obligation is more than expected.

The attribution period for postretirement health care plans does not include:

a. The first five years of service.

b. The year of hire.

c. The employee probation period.

d. The years of service beyond the full eligibility date.

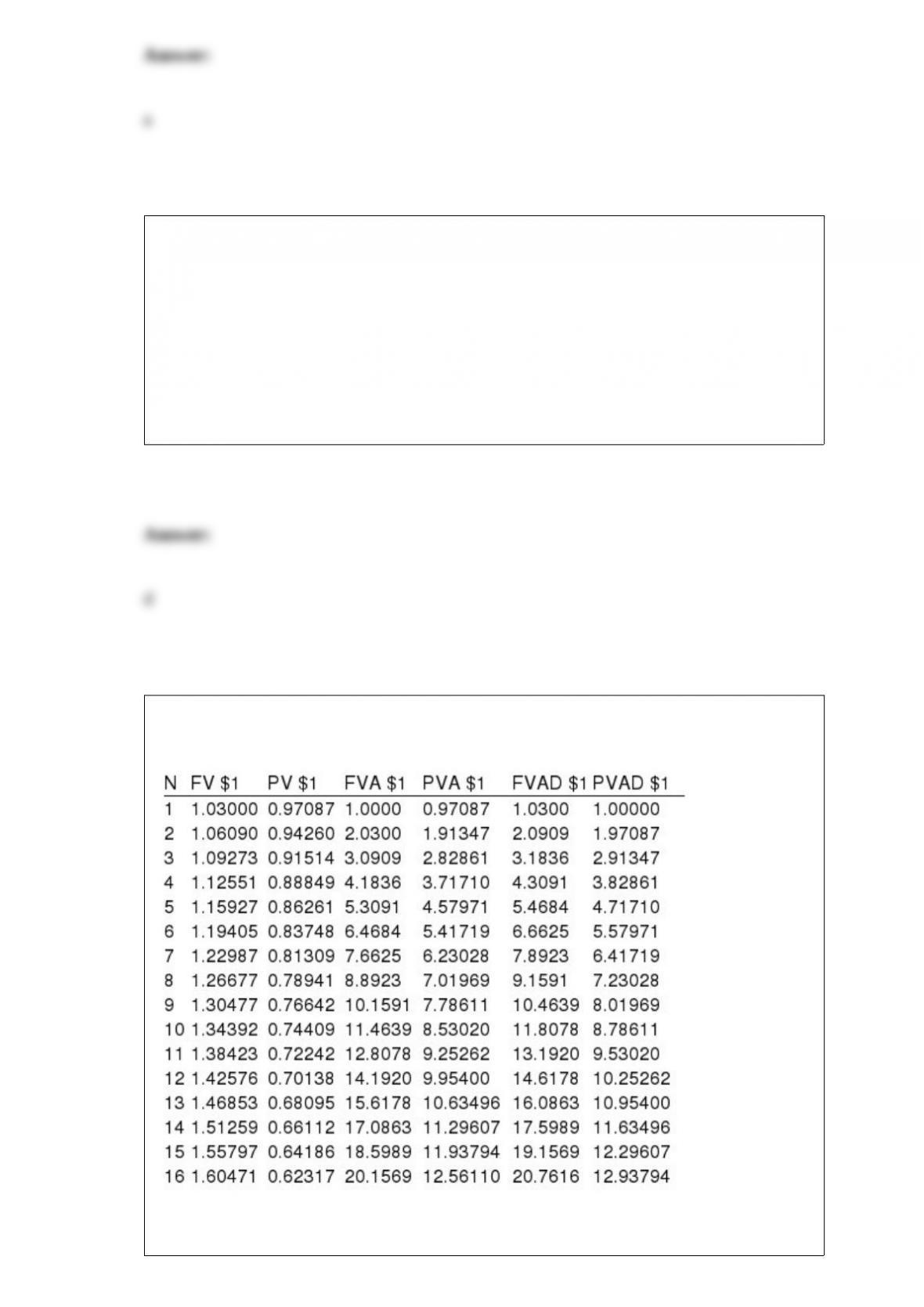

Present and future value tables of $1 at 3% are presented below:

Bill wants to give Maria a $500,000 gift in seven years. If money is worth 6%

compounded semiannually, what is Maria’s gift worth today?

a. $ 66,110.

b. $ 81,309.

c. $406,545.

d. $330,560.

The Ultimate Frisbee League (UFL) licenses its trademark to Tank-Skin Apparel. Under

the license arrangement, Tank-Skin pays the UFL a $1 million initial license fee plus a

bonus when annual sales of Tank-Skin merchandise reach a threshold. The license

agreement is for 4 years.

Refer to the information in the previous question. Assume that the UFL anticipates that,

in addition to receiving the $1 million license fee, it will receive a bonus of $2 million

in year 1 of the contract and a bonus of $3 million in years 2-4 of the contract based on

Tank-Skin’s sales. Also assume that the UFL is convinced that it is probable there will

not be a significant reversal of any revenue recognized with respect to the bonus in

subsequent periods. At the inception of the contract, what is the amount of transaction

price that the UFL would estimate with respect to this license arrangement?

a. $0

b. $1,000,000

c. $3,000,000

d. 12,000,000

Bloomfield Bakers accounts for its investment in Clor Confectionary under the equity

method. Bloomfield carried the Clor investment at $150,000 and $165,000 at December

31, 2015 and 2016, respectively. During 2016 Clor recognized $80,000 of net income

and paid dividends of $30,000. Assuming that Bloomfield owned the same percentage

of Clor throughout 2016, their percentage ownership must have been:

a. 15%.

b. 18.75%.

c. 30%.

d. 50%.

Which of the following may create employer liabilities in connection with their

payrolls?

a. Employee withholding taxes.

b. Employee voluntary deductions.

c. Employee fringe benefits.

d. All of these answer choices are correct.

Assets acquired under multi-year deferred payment contracts are:

a. Valued at their fair value on the date of the final payment.

b. Valued at the present value of the payments required by the contract.

c. Valued at the sum of the payments required by the contract.

d. None of these answer choices are correct.

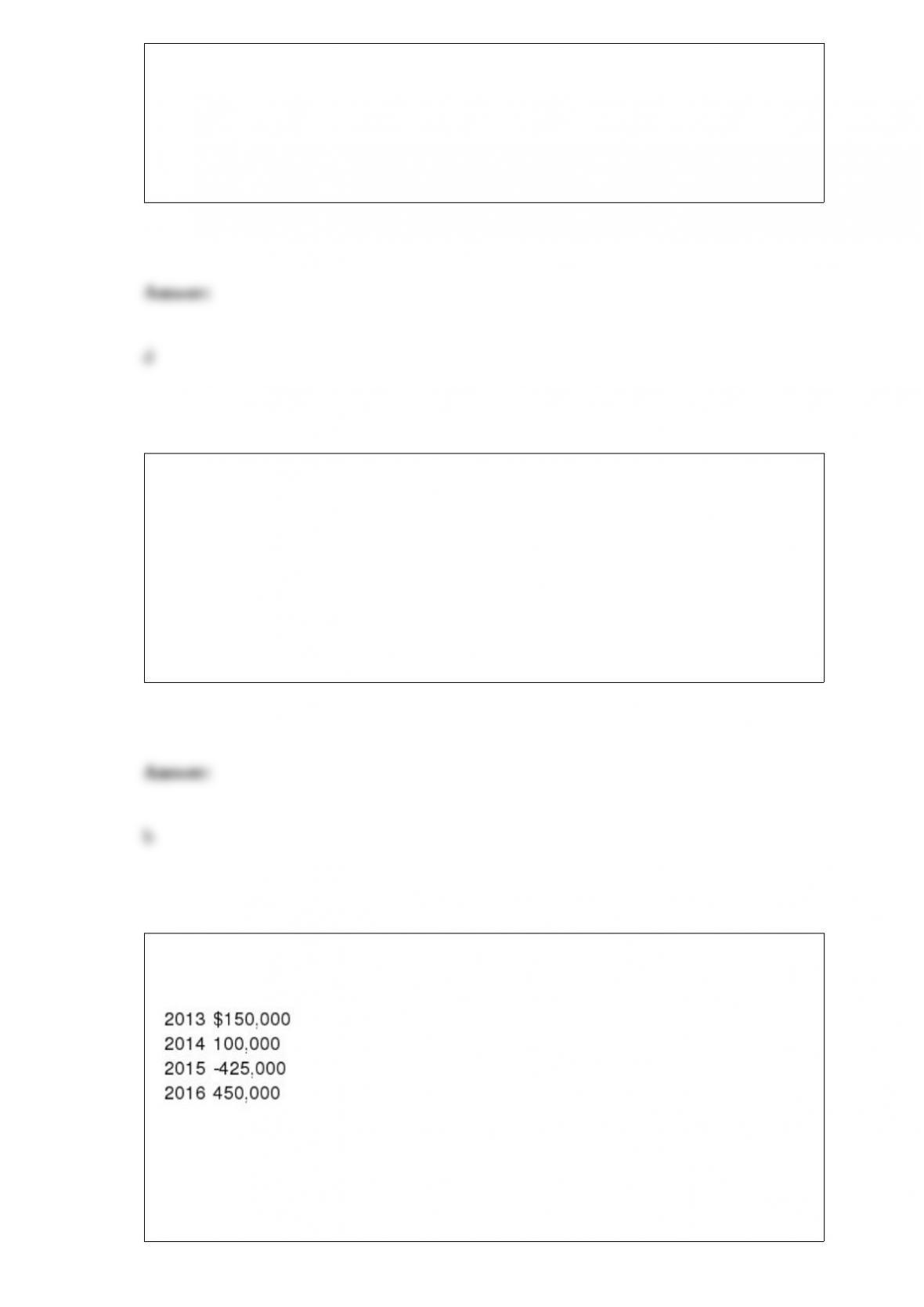

In its first four years of operations Peridot Jewelers reported the following operating

income (loss) amounts:

There were no other deferred income taxes in any year. In 2015, Peridot elected to carry

back its operating loss. The enacted income tax rate was 40%. In its 2016 income

statement, what amount should Peridot report as current income tax payable?

a. $ 80,000.

b. $110,000.

c. $170,000.

d. $180,000.

A customer of RoughEdge Sharpeners alleges that RoughEdge’s new razor sharpener

had a defect that resulted in serious injury to the customer. RoughEdge believes the

customer has a 51% chance of winning the case, and that if the customer wins the case,

there is a range of losses of between $1,000,000 and $3,000,000 in which any number is

equally likely to occur. Under U.S. GAAP, RoughEdge should accrue a liability in the

amount of:

a. $0.

b. $1,000,000.

c. $2,000,000.

d. $3,000,000.

Which of the following is not a reason to consider a decline in the fair value of a debt

investment to be “other than temporary”?

a. The investor determines that a credit loss exists on the investment.

b. The investor intends to sell the investment.

c. The investor believes it is “more likely than not” that the investor will be required to

sell the investment prior to recovering the amortized cost of the investment less any

credit losses arising in the current year.

. d. The investor intends to hold the investment to maturity.

The recognition of which of the following expenses exemplifies the application of

matching expenses with the revenues they produced?

a. President”s salary.

b. Research and development.

c. Cost of goods sold.

d. Advertising.

Distinguishing between operating and capital leases is due in large part to the

accounting concept of:

a. Conservatism.

b. Materiality.

c. Substance over form.

d. Historical cost.

What is the interest expense on the bonds in 2017?

a. $800,000.

b. $680,759.

c. $342,971.

d. $119,241.

Which of the following is not a requirement for a qualified pension plan?

a. It cannot discriminate in favor of highly paid employees.

b. It must cover at least 80% of the employees.

c. It must be funded in advance of retirement.

d. Benefits must vest after a specified period of service, commonly five years.

On December 31, 2016, the following pension-related data were available for CPS

Industries’ noncontributory, defined benefit pension plan:

Projected Benefit Obligation ($ in millions)

Balance, January 1, 2016 $960

Service cost 164

Interest cost, discount rate, 5% 48

Gain due to changes in actuarial assumptions in 2016 (20)

Pension benefits paid (80)

Balance, December 31, 2016 $1,072

Plan Assets

Balance, January 1, 2016 $1,000

Actual return on plan assets 80

(Expected return on plan assets, $90)

Cash contributions 140

Pension benefits paid (80)

Balance, December 31, 2016 $1,140

January 1, 2016, balances:

Prior service cost (amortization $16 per year) $ 96

Net gain (any amortization over 15 years) 160

Required:

1) Prepare the 2016 journal entry to record pension expense.

2) How will the statement of comprehensive income be affected by any 2016 gains and

losses?

What is comprehensive income and how does it differ from net income? Where is it

reported in the balance sheet?

In December of 2016, XL Computer’s internal auditors discovered that office equipment

costing $800,000 was charged to expense in 2014. The asset had an expected life of 10

years with no residual value. XL would have recorded a half year of depreciation in

2014.

Required:

Prepare the necessary correcting entry that would be made in 2016 (ignore income

taxes), and the entry to record depreciation for 2016.

Some inventory errors are described as ‘œself-correcting’ in that they have the opposite

financial statement effect in the period following the errors, thereby ‘œcorrecting’ the

original account balance errors.

Required:

Given this ‘œself-correcting’ feature, discuss why these errors should not be ignored and

describe the steps needed to correct these errors.

On September 1, 2016, Jacob Furniture Mart enters into a tentative agreement to sell

the assets of its office equipment division. This division qualifies as a component of the

entity according to GAAP regarding discontinued operations. The division’s

contribution to Jacob’s operating income for 2016 was a $3 million loss before taxes.

Jacob has an average tax rate of 30%. Required: Consider independently the

appropriate accounting by Jacob under the three scenarios below.

Scenario 3: Assume that Jacob had not yet sold the office furniture division by the end

of 2016. Further, assume that the fair value less costs to sell of the division’s assets at

December 31, 2016, was $12 million and was expected to remain the same when the

assets are sold in 2017. The book value of the division’s assets was $19 million at the

end of the year. Under these assumptions, what would Jacob report in its 2016 income

statement regarding the office equipment division? Explain where this information

would be presented.

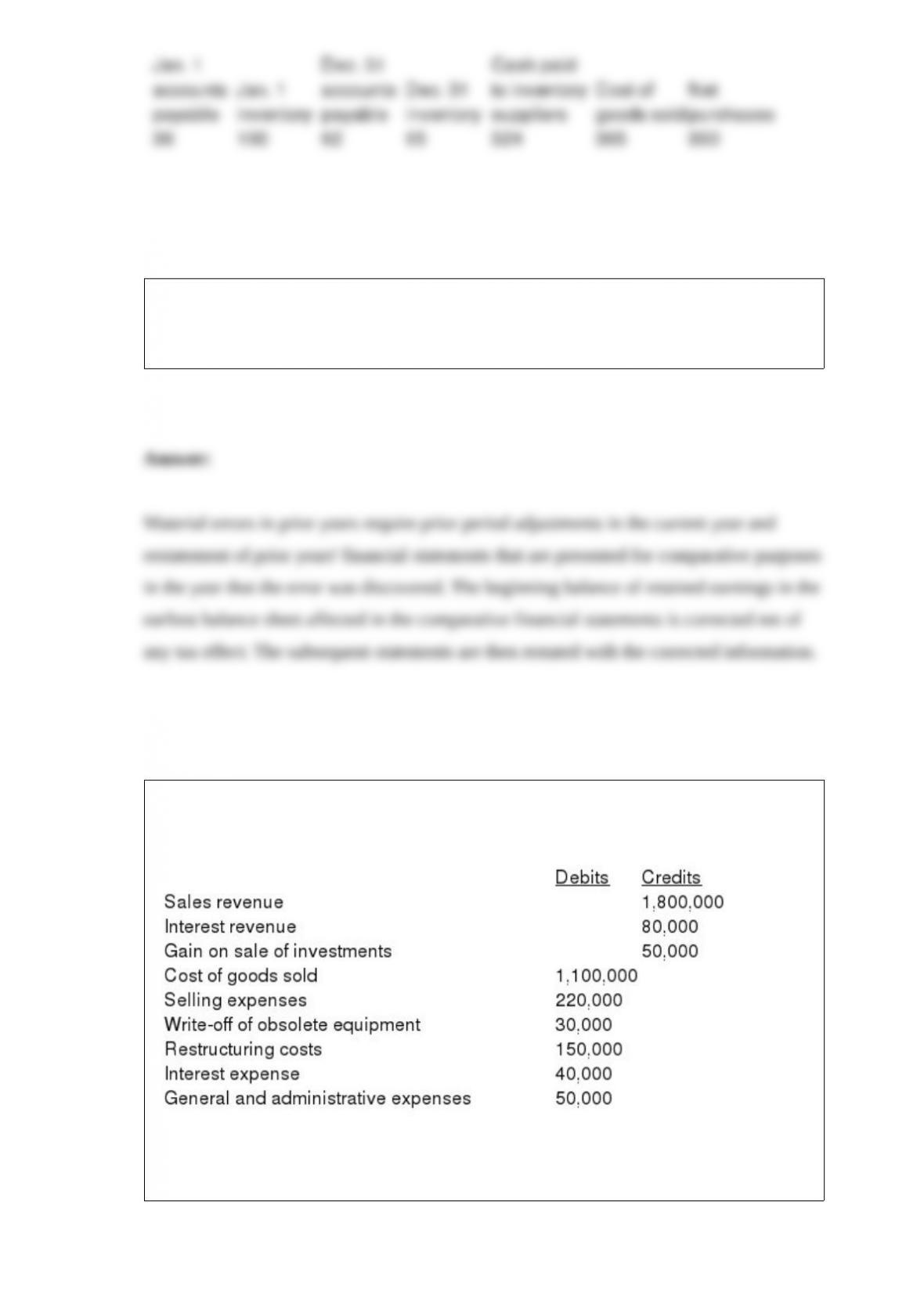

The following information is taken from the accounting records of Madeline Inc. for the

year 2016. Missing information has been left blank. Inventory is the only supply that

Madeline purchases on credit. Required: Compute the missing amounts.

Briefly explain the financial reporting required when material misstatements are found

in previous years’ financial statements that are included for comparative purposes in the

current year’s financial statements.

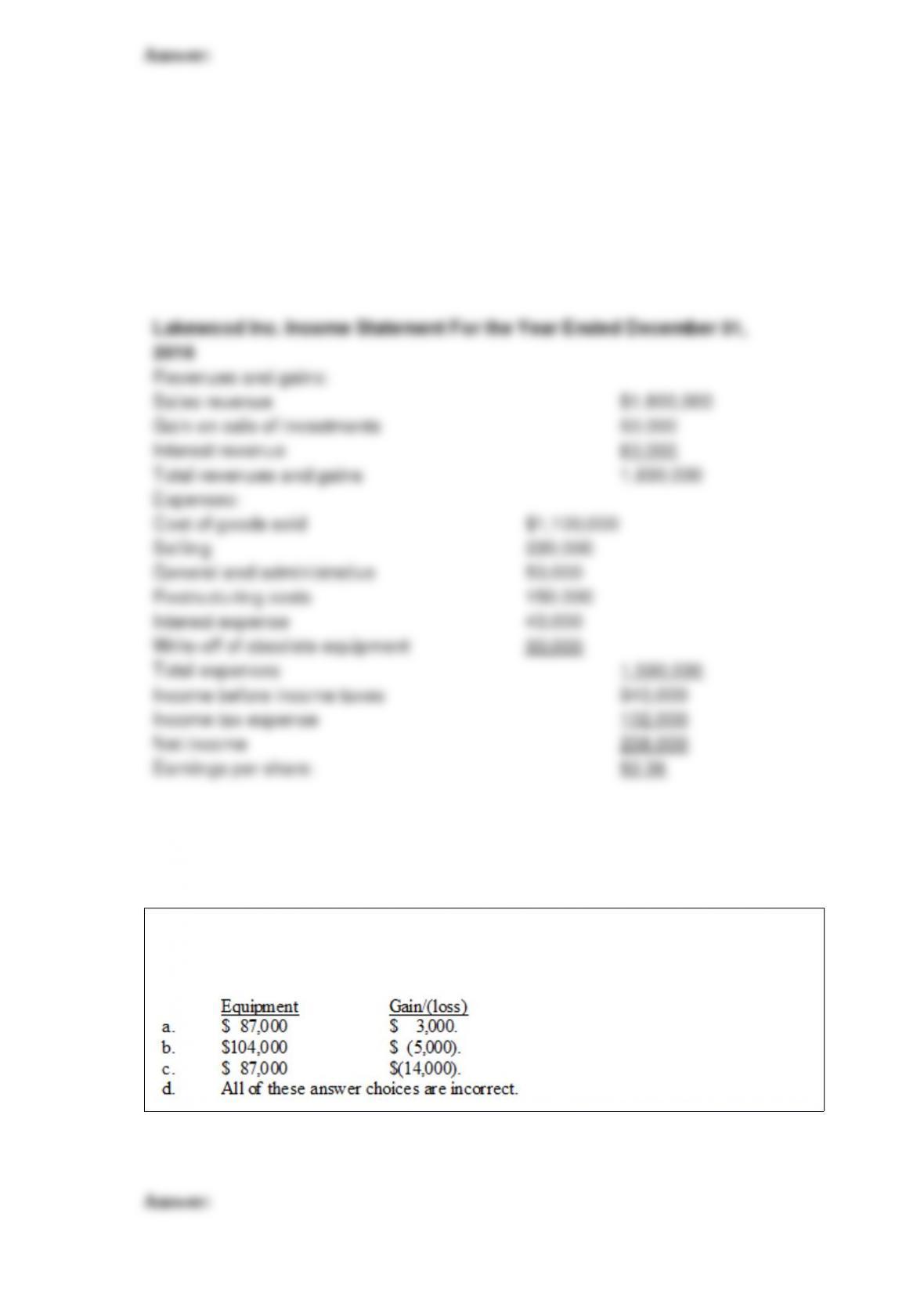

The trial balance of Lakewood Inc. included the following accounts as of December 31,

2016:

Lakewood Inc. had 100,000 shares of stock outstanding throughout the year. Income tax

expense has not yet been accrued. The effective tax rate is 30%.

Required: Prepare a single-step income statement with earnings per share disclosure.

Bloomington Inc. exchanged land for equipment and $3,000 in cash. The book value

and the fair value of the land were $104,000 and $90,000, respectively. Bloomington

would record equipment and a gain/(loss) of: