1) If the company bases its predetermined overhead rate on capacity, the predetermined

overhead rate is closest to:

The management of Wray Corporation would like to investigate the possibility of

basing its predetermined overhead rate on activity at capacity. The company’s controller

has provided an example to illustrate how this new system would work. In this

example, the allocation base is machine-hours and the estimated amount of the

allocation base for the upcoming year is 68,000 machine-hours. In addition, capacity is

79,000 machine-hours and the actual level of activity for the year is 63,500

machine-hours. All of the manufacturing overhead is fixed and is $3,384,360 per year.

For simplicity, it is assumed that this is the estimated manufacturing overhead for the

year as well as the manufacturing overhead at capacity. It is further assumed that this is

also the actual amount of manufacturing overhead for the year.

A.$53.30

B.$49.77

C.$42.84

D.$47.27

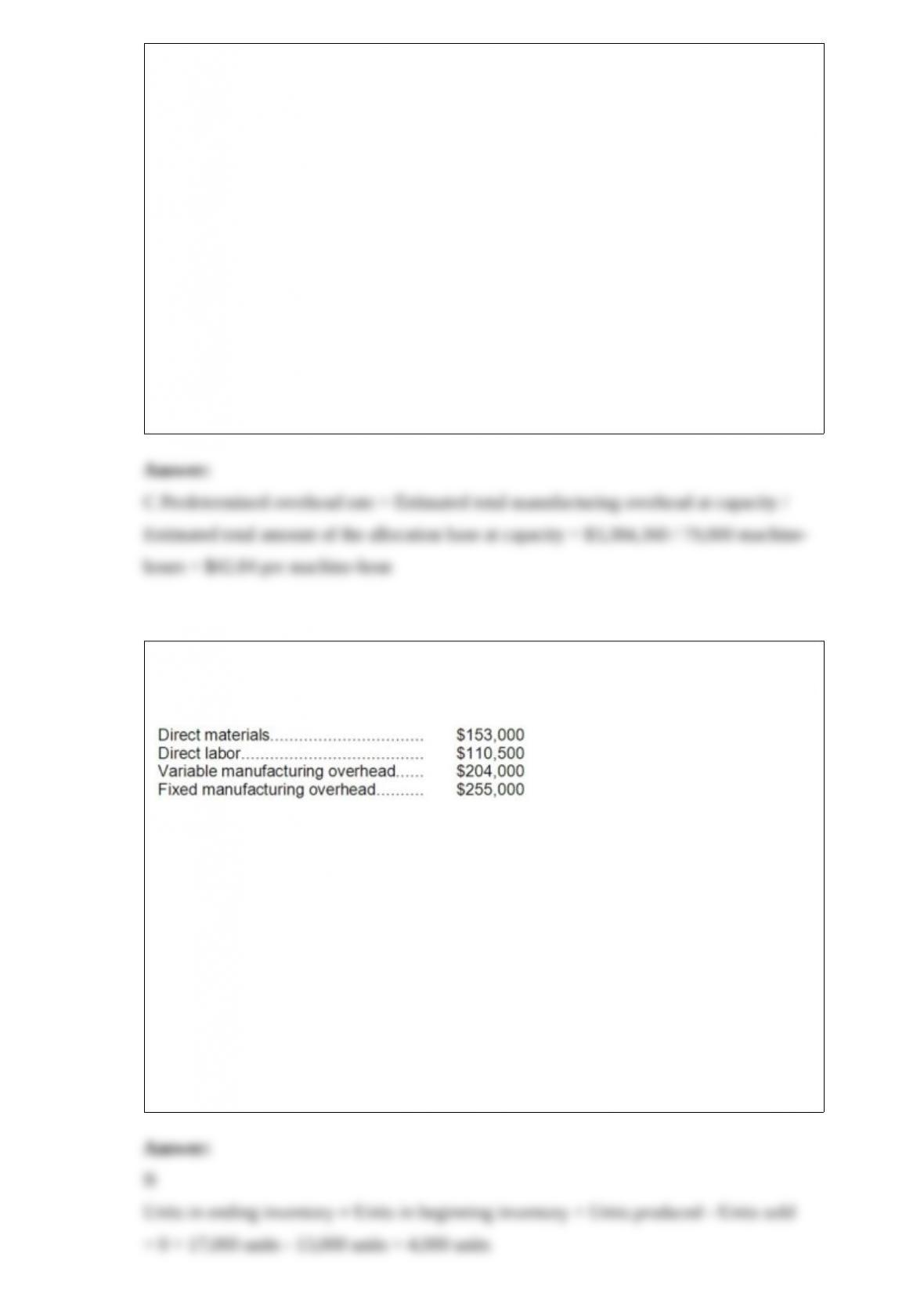

2) Harris Corporation produces a single product. Last year, Harris manufactured 17,000

units and sold 13,000 units. Production costs for the year were as follows:

Sales were $780,000 for the year, variable selling and administrative expenses were

$88,400, and fixed selling and administrative expenses were $170,000. There was no

beginning inventory. Assume that direct labor is a variable cost.

Under absorption costing, the ending inventory for the year would be valued at:

A.$190,800

B.$170,000

C.$230,800

D.$0

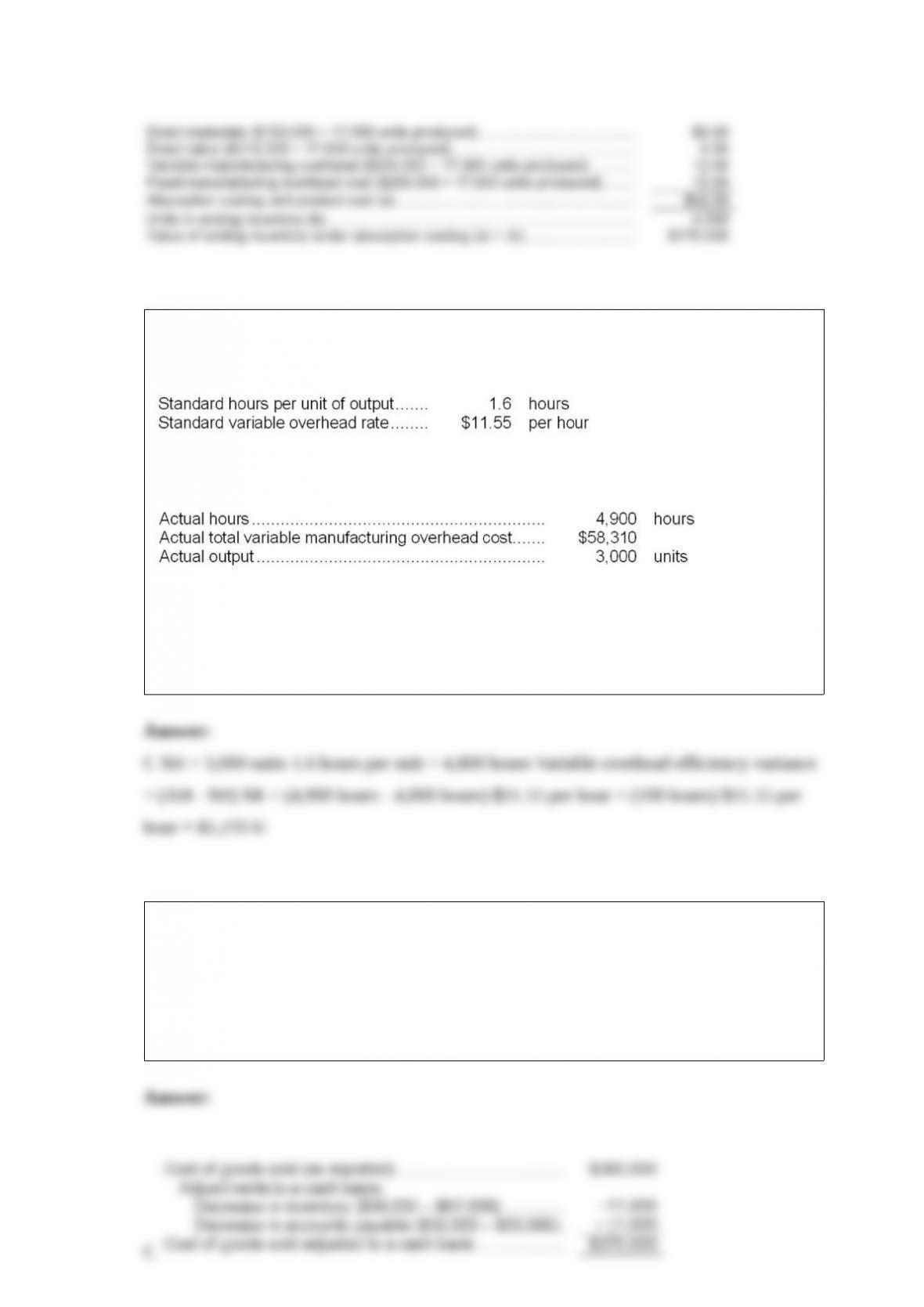

3) The following standards for variable manufacturing overhead have been established

for a company that makes only one product:

The following data pertain to operations for the last month:

What is the variable overhead efficiency variance for the month?

A.$1,680 F

B.$1,190 U

C.$1,155 U

D.$1,190 F

4) On the statement of cash flows, the cost of goods sold adjusted to a cash basis would

be:

A.$360,000

B.$350,000

C.$370,000

D.$381,000

5) Assume that dropping Product G would result in a $40,000 increase in the

contribution margin of other product lines. If Bailey chooses to drop Product G, then

the change in net operating income next year due to this action will be a:

A) $95,000 increase

B) $95,000 decrease

C) $25,000 decrease

D) $25,000 increase

6) In a statement of cash flows, which of the following would be classified as an

investing activity?

A.The sale of the company’s own common stock for cash.

B.The sale of equipment.

C.Interest paid to a lender.

D.The issuance of bonds payable.

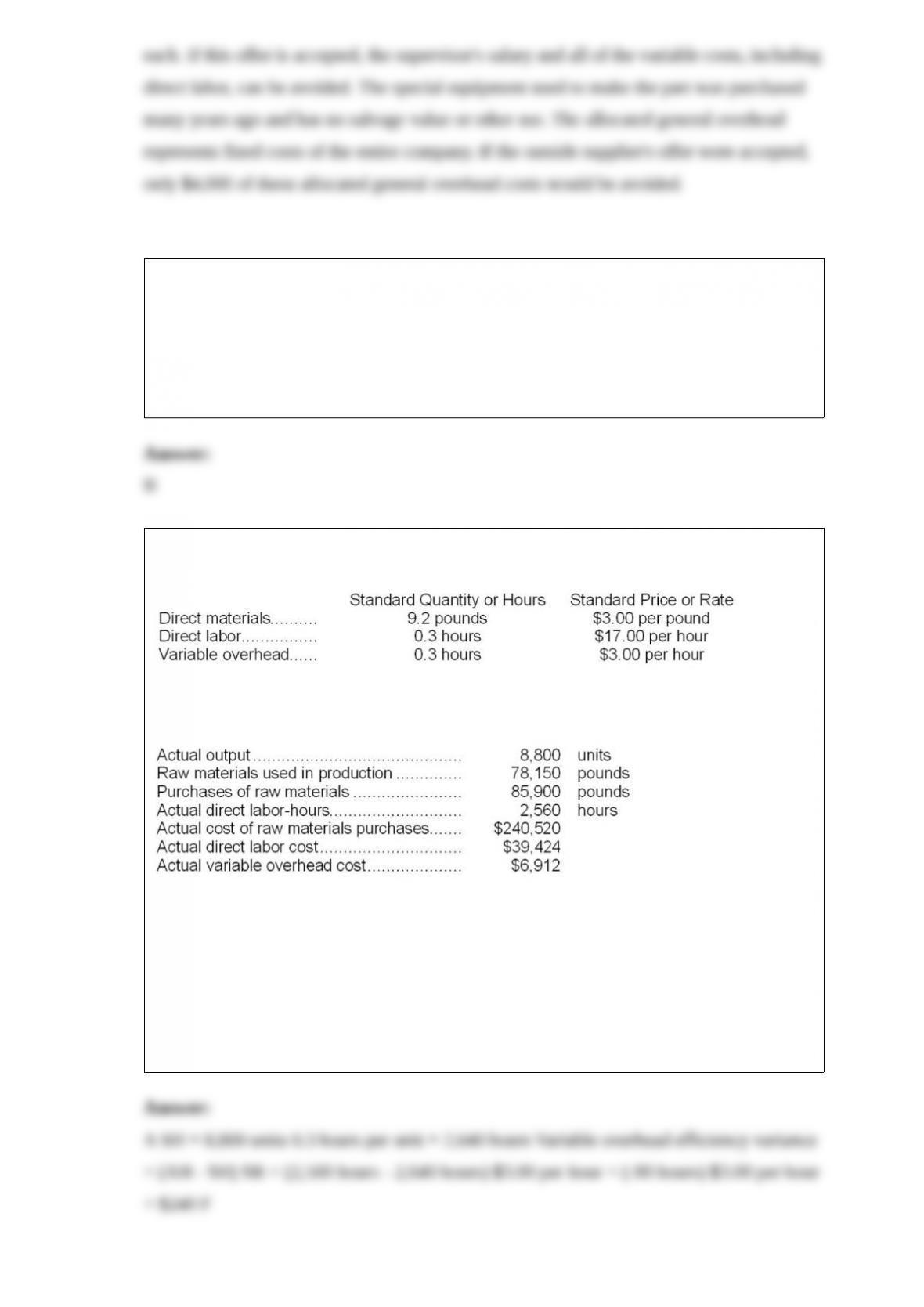

7) Berends Corporation makes a product with the following standard costs:

The company reported the following results concerning this product in April.

The company applies variable overhead on the basis of direct labor-hours. The direct

materials purchases variance is computed when the materials are purchased.

The variable overhead efficiency variance for April is:

A.$240 F

B.$216 U

C.$216 F

D.$240 U

8) On the statement of cash flows, the selling and administrative expense adjusted to a

cash basis would be:

A.$201,000

B.$166,000

C.$254,000

D.$210,000

9) The unit target selling price using the absorption costing approach is closest to:

A.$105.75

B.$83.33

C.$121.50

D.$86.00

10) Soledad Corporation had $36,000 of raw materials on hand on December 1. During

the month, the Corporation purchased an additional $71,000 of raw materials. The

journal entry to record the purchase of raw materials would include a:

A.credit to Raw Materials of $71,000

B.debit to Raw Materials of $71,000

C.credit to Raw Materials of $107,000

D.debit to Raw Materials of $107,000

11) The company’s equity multiplier at the end of Year 2 is closest to:

A.0.28

B.1.28

C.3.53

D.0.78

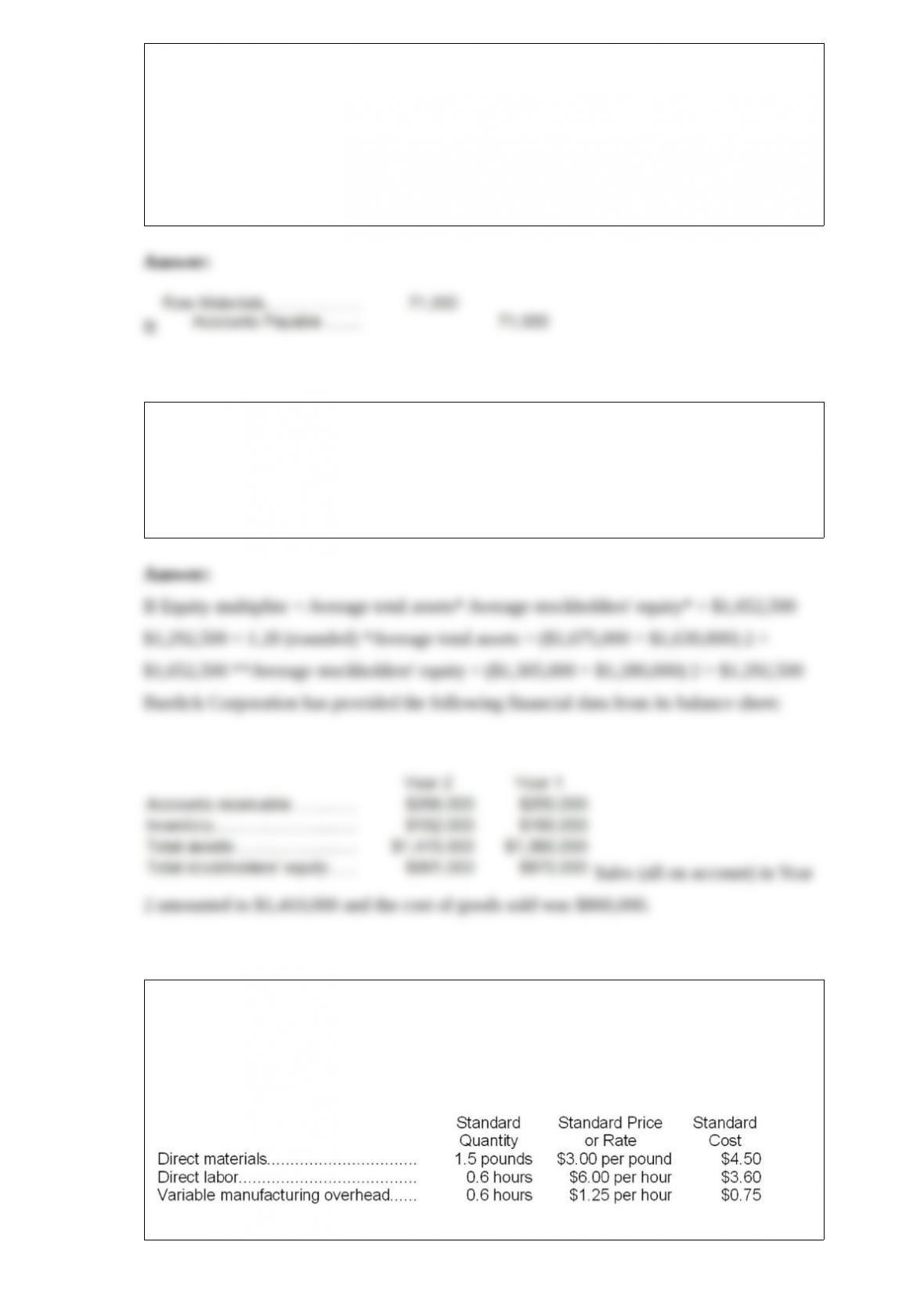

12) Pardoe, Inc., manufactures a single product in which variable manufacturing

overhead is assigned on the basis of standard direct labor-hours. The company uses a

standard cost system and has established the following standards for one unit of

product:

During March, the following activity was recorded by the company:

The company produced 3,000 units during the month.

A total of 8,000 pounds of material were purchased at a cost of $23,000.

There was no beginning inventory of materials on hand to start the month; at the end of

the month, 2,000 pounds of material remained in the warehouse.

During March, 1,600 direct labor-hours were worked at a rate of $6.50 per hour.

Variable manufacturing overhead costs during March totaled $1,800.

The direct materials purchases variance is computed when the materials are purchased.

The materials quantity variance for March is:

A.$4,500 F

B.$10,500 F

C.$10,500 U

D.$4,500 U

13) What would be the average fixed cost per unit at an activity level of 5,600 units?

Assume that this level of activity is within the relevant range.

A) $32.27

B) $15.68

C) $65.74

D) $15.40

14) The total cash flow net of income taxes in year 2 is:

A.$140,000

B.$200,000

C.$151,000

D.$73,000

15) The net present value of this investment is:

A.$40,000

B.$3,625

C.$57,831

D.$95,800