Cairo Co. uses the allowance method of accounting for uncollectible accounts. Cairo

Co. accepted a $5,000, 12%, 3-month note dated May 16, from Alexandria Co. in

exchange for its past-due account receivable.

Required:

Part a. Prepare the journal entry for the receipt of the note on May 16.

Part b. Prepare the journal entries for (1) the receipt of interest and (2) the receipt of the

principal balance at maturity on August 14.

Part c. Assume that Alexandria made the interest payment but not the principal payment

on August 14. On November 30, Cairo writes off the note when it becomes clear that

Alexandria will never pay. Prepare the journal entry to write-off the note receivable.

Match the term and its definition. There are more definitions than terms.

Terms

____ 1> Net Sales Revenue

____ 2> Allowance Method

____ 3> Notes Receivable

____ 4> Accounts Receivable

____ 5> Average Net Receivables

____ 6> Subsidiary Account

____ 7> Historical Percentage of Bad Debt Losses

____ 8> Annual Interest Rate

Definitions

A. The amount of interest a lender receives during a year.

B. A system used by companies to allocate their budgets over the different operating

expenses.

C. The numerator of the receivables turnover ratio.

D. A separate record for each accounts receivable customer.

E. Used by the percentage of credit sales method to estimate bad debts.

F. Another name for a company’s total revenue, which is calculated by multiplying the

quantity sold by the average price.

G. The costs of maintaining accounts with customers who have not made recent

purchases.

H. The interest that a company receives during the year divided by the principal of the

loan.

I. The rate at which a company pays off its liabilities or debts.

J. The total amount of money loaned through notes that the lender has not yet collected.

K. The denominator of the receivables turnover ratio.

L. The average level of net sales revenue the firm earns each month.

M. An accounting method which involves estimating bad debts.

N. The portion of past credit sales that have not yet been collected.

Which of the following statements about the end of an asset’s life is not correct?

A) At the end of an asset’s life, its book value should equal its residual value.

B) At the end of an asset’s life, the Accumulated Depreciation should equal the

depreciable cost.

C) At the end of an assets life, the book value would equal zero if there is no residual

value.

D) Assets are not to be depreciated below residual value unless the double-declining

balance method is used.

Goods placed in inventory are initially recorded at:

A) market value.

B) the amount paid to acquire the asset.

C) the amount paid to prepare the asset for sale to customers.

D) the amount paid to acquire the asset and prepare it for sale.

Eaton Electronics uses a periodic inventory system. On March 31, Eaton has two

plasma TVs on hand at a cost of $1,500 each (serial numbers 11534892 and 11534894).

In April, the company purchases four more identical TVs from Toshiba for $1,450 each

(serial numbers 11542631 through 11542634). In May, the company purchases five

more identical TVs for $1,600 each (serial numbers 11550964 through 11550968). In

June, Eaton sells two of these TVs (serial numbers 11534894 and 11542631). There

were no additional purchases or sales during the remainder of the year.

Use the information above to answer the following question. Eaton Electronics uses the

specific identification method. What is its cost of goods sold?

A) $3,000

B) $2,950

C) $3,200

D) $3,033

The normal balance of any account is the:

A) left side.

B) right side.

C) side which increases that account.

D) side which decreases that account.

Which of the following statements about financial accounting is correct?

A) Financial accounting reports are used primarily by employees to make business

decisions related to production.

B) Financial accounting reports are used primarily by management to understand

whether a product line should be discontinued.

C) Financial accounting reports are primarily prepared to provide information for

external decision makers.

D) Financial accounting reports primarily contain detailed internal records of the

company.

The annual interest payment on bonds:

A) increases over the life of the bonds when bonds are issued at a discount.

B) decreases over the life of the bonds when bonds are issued at a discount.

C) stays constant over the life of the bonds, regardless of whether bonds are issued at

par, a discount, or a premium.

D) increases over the life of the bonds under the effective-interest method, but stays

constant under the straight-line method of amortization.

Which of the following analysis techniques does notpertain to changes over time?

A) Trend analysis

B) Horizontal analysis

C) Time-series analysis

D) Vertical analysis

Which of the following statements about Retained Earnings is correct?

A) Retained Earnings represents cash available to pay dividends to stockholders.

B) Retained Earnings cannot be restricted by loan covenants.

C) Retained Earnings generally consists of cumulative net income less any net losses

and dividends since inception.

D) Retained Earnings is reduced by the par value of the common stock that is issued.

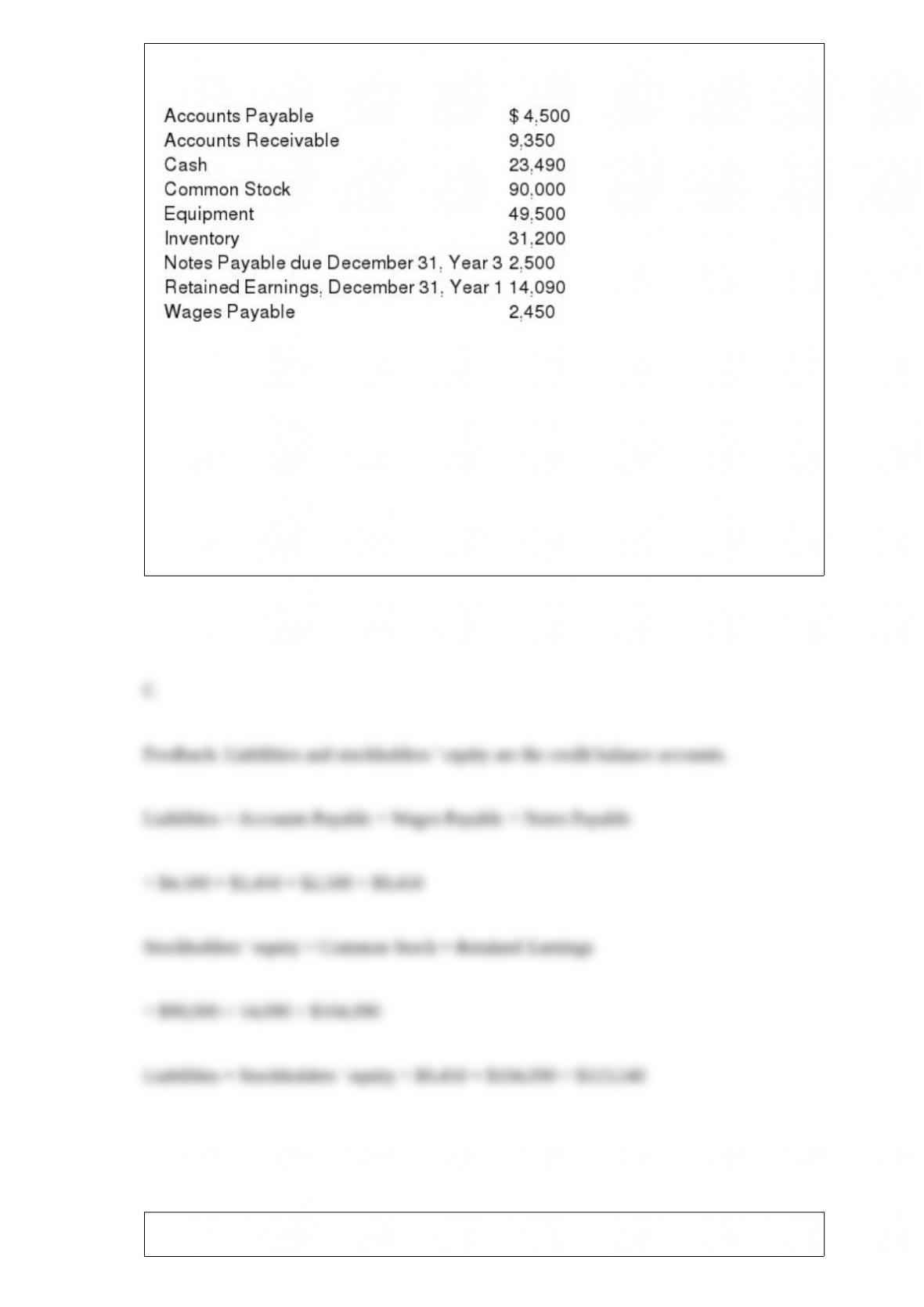

A company reported the following information at December 31, Year 1:

Use the information above to answer the following question. What is the total of the

credit balance accounts?

A) $111,040.

B) $104,090.

C) $113,540.

D) $108,590.

Which of the following is not an accounting transaction?

A) Issued shares of stock to investors in exchange for cash contributions of $4,000.

B) Ordered inventory from suppliers for $3,000.

C) Sold equipment to another company for $3,000 and accepted a note from the

company promising payment in 6 months.

D) Borrowed money from the bank by signing a promissory note for $2,000.

Inventory shipped FOB destination and in transit on the last day of the year should be

included in:

A) the inventory balance of the seller.

B) the inventory balance of the buyer.

C) neither the inventory balance of the buyer or the seller.

D) both the inventory balance of the buyer and the seller.

Which of the following types of items would you be most likely to see below the

income tax expense line on an income statement?

A) Gain on Sale of Discontinued Operations, Net of Tax

B) Gross Profit

C) Cumulative Effect of Accounting Change

D) Salaries Expense

Thompson Company had beginning inventory of $6,000, cost of goods sold of $14,000,

and ending inventory of $8,000. Purchases were:

A) $12,000.

B) $10,000.

C) $9,000.

D) $16,000.

Which of the following statements about inventory costing methods is correct?

A) A change in inventory method is allowed only if it improves the accuracy of the

company ‘s financial results.

B) During a period of rising prices, LIFO results in a higher income tax expense than

does FIFO.

C) International Financial Reporting Standards (IFRS) allow the use of LIFO but not

FIFO.

D) In the U.S., if a company uses LIFO on the income tax return, it may use a different

method for financial reporting.

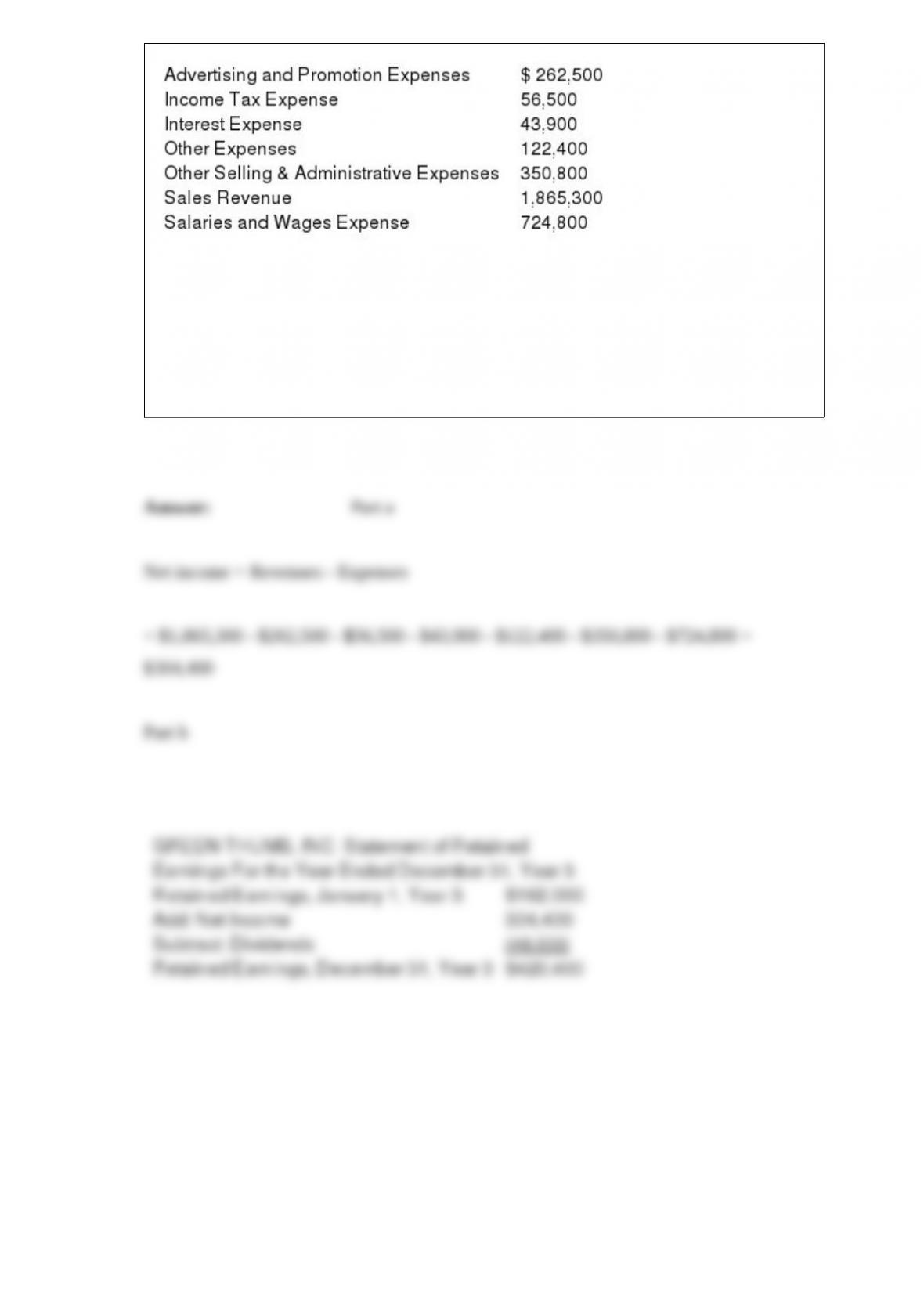

A list of Year 3 revenues and expenses for Green Thumb, Inc. is provided below.

Required:

Part a. Calculate the net income for the Green Thumb, Inc. for Year 3.

Part b. Prepare a statement of retained earnings for Green Thumb, Inc. for Year 3.

Assume the company had retained earnings of $162,000 as of January 1, Year 3, and

paid out $46,000 in dividends during Year 3.