The balance in the Prepaid Rent account before adjustment at the end of the year is

$21,000, which represents three months’ rent paid on December 1. The adjusting entry

required on December 31 is to

a. debit Rent Expense, $7,000; credit Prepaid Rent, $7,000.

b. debit Rent Expense, $14,000; credit Prepaid Rent $14,000.

c. debit Prepaid Rent, $7,000; credit Rent Expense, $7,000.

d. debit Prepaid Rent, $14,000; credit Rent Expense, $14,000.

Answer:

Current liabilities

a. are obligations that the company is to pay within the forthcoming year.

b. are listed in the balance sheet in order of their expected maturity.

c. are listed in the balance sheet, starting with accounts payable.

d. should not include long-term debt that is expected to be paid within the next year.

Answer:

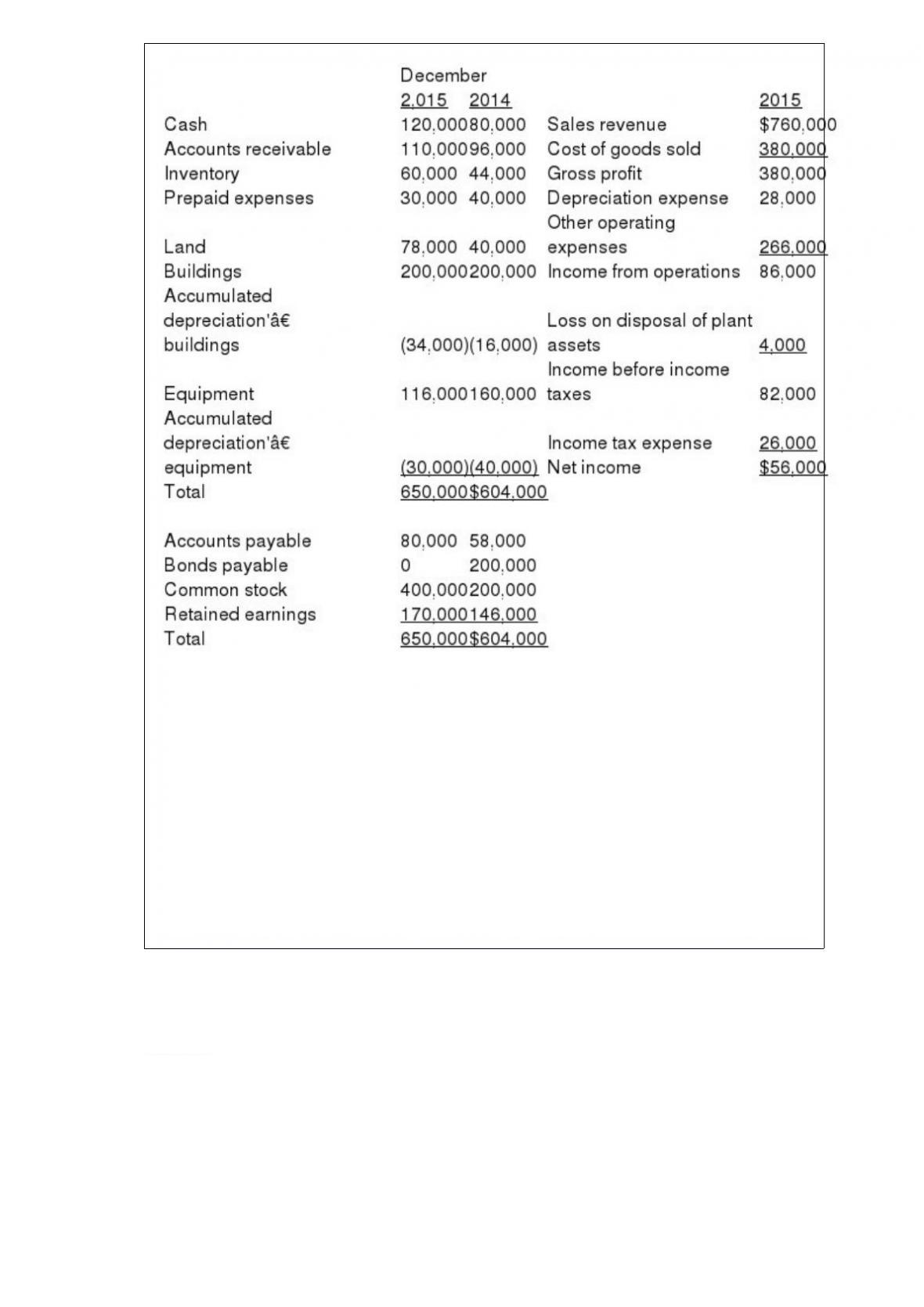

Presented below is information related to the operations of Simpson Corporation.

Additional information:

(a) In 2015, Simpson declared and paid a cash dividend.

(b) The company converted $200,000 of bonds into common stock.

(c) Equipment with a cost of $44,000 and a book value of $24,000 was sold for

$20,000. Land was acquired for cash.

Instructions:

Prepare a statement of cash flows in proper form for 2015, using the indirect method.

Answer:

Depletion expense is computed by multiplying the depletion cost per unit by the

a. total estimated units.

b. total actual units.

c. number of units extracted.

d. number of units sold.

Answer:

Treasury stock is

a. stock issued by the U.S. Treasury Department.

b. stock purchased by a corporation and held as an investment in its treasury.

c. corporate stock issued by the treasurer of a company.

d. a corporation’s own stock which has been reacquired but not retired.

Answer:

The use of reversing entries

a. is a required step in the accounting cycle.

b. changes the amounts reported in the financial statements.

c. simplifies the recording of subsequent transactions.

d. is required for all adjusting entries.

Answer:

When an investor owns between 20% and 50% of the common stock of a corporation, it

is generally presumed that the investor

a. has insignificant influence on the investee and that the cost method should be used to

account for the investment.

b. should apply the cost method in accounting for the investment.

c. will prepare consolidated financial statements.

d. has significant influence on the investee and that the equity method should be used to

account for the investment.

Answer:

A sales discount does not

a. provide the purchaser with a cash saving.

b. reduce the amount of cash received from a credit sale.

c. increase a contra-revenue account.

d. increase an operating expense account.

Answer:

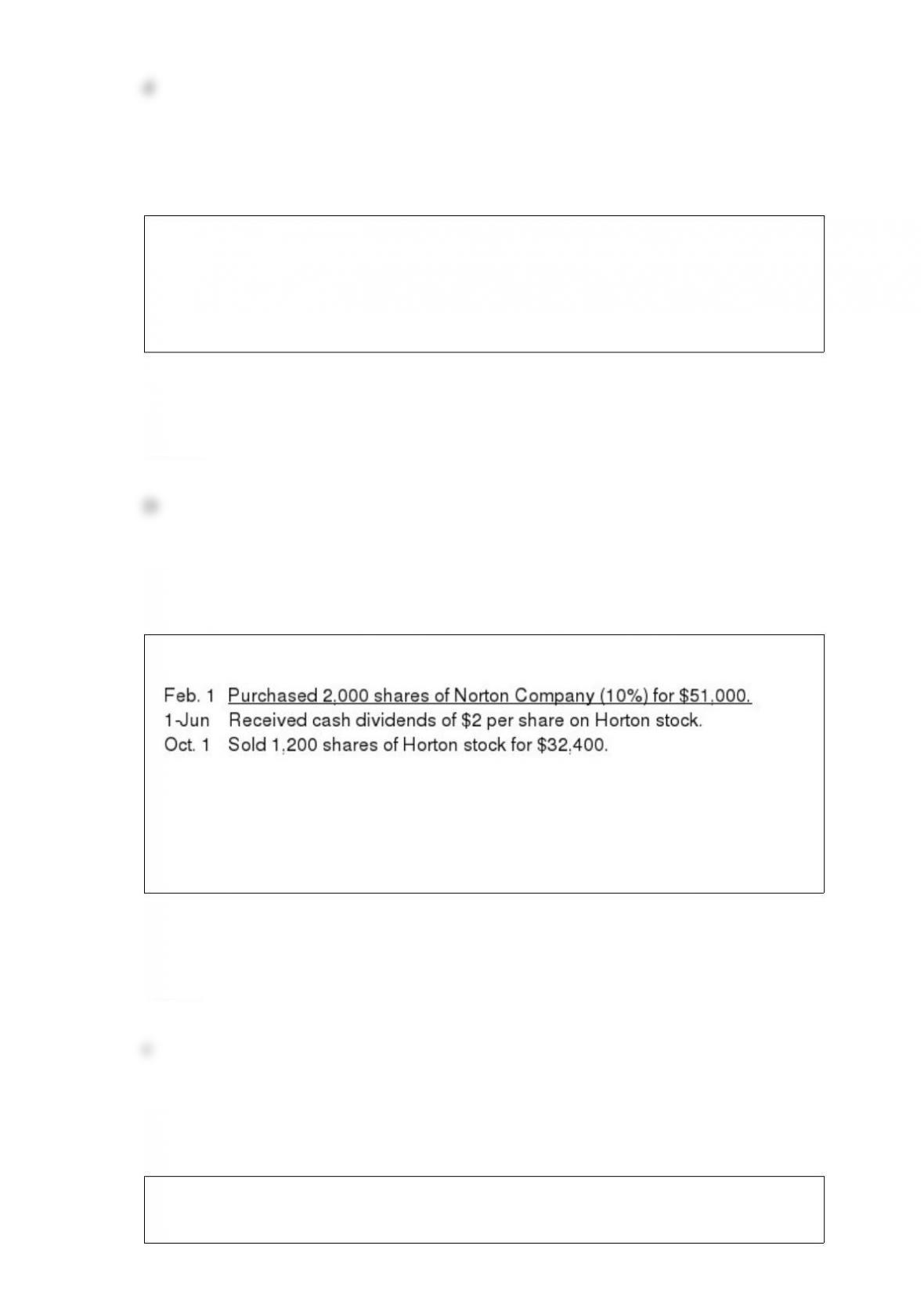

Blaine Company had these transactions pertaining to stock investments:

The entry to record the purchase of the Horton stock would include a

a. debit to Stock Investments for $45,900.

b. credit to Cash for $45,900.

c. debit to Stock Investments for $51,000.

d. debit to Investment Expense for $5,100.

Answer:

The formula for horizontal analysis of changes since the base period is the current year

amount

a. divided by the base year amount.

b. minus the base year amount divided by the base year amount.

c. minus the base year amount divided by the current year amount.

d. plus the base year amount divided by the base year amount.

Answer:

Match the following terms and definitions.

a. Accounts receivable

b. Creditor

c. Accounts payable

d. Note payable

_______ (1) Amounts due from customers

_______ (2) Amounts owed to suppliers for goods and services purchased

_______ (3) Amounts owed to bank

_______ (4) Party to whom money is owed

Answer:

With an interest-bearing note, the amount of assets received upon issuance of the note is

generally

a. equal to the note’s face value.

b. greater than the note’s face value.

c. less than the note’s face value.

d. equal to the note’s maturity value.

Answer:

All of the following are property, plant, and equipment except

a. supplies.

b. machinery.

c. land.

d. buildings.

Answer:

In converting net income to net cash provided by operating activities, under the indirect

method:

a. decreases in accounts receivable and increases in prepaid expenses are added.

b. decreases in inventory and increases in accrued liabilities are added.

c. decreases in accounts payable and decreases in inventory are deducted.

d. increases in accounts receivable and increases in accrued liabilities are deducted.

Answer:

Which statement is false regarding the lower-of-cost-or-market (LCM) method of

inventory?

a. Market is defined as current replacement cost, not selling price.

b. LCM is an example of the accounting concept of conservatism.

c. LCM is applied to individual items listed on the inventory summary sheets.

d. All of these answer choices are correct.

Answer:

Abaco Enterprises had beginning inventory of $45,000 at March 1, 2015. During the

month, the company made purchases of $360,000. The inventory at the end of the

month is $51,000. What is cost of goods available for sale for the month of March?

a. $45,000

b. $51,000

c. $354,000

d. $405,000

Answer:

Revenues would not result from

a. sale of merchandise.

b. issuance of common stock.

c. performance of services.

d. rental of property.

Answer:

The final closing entry to be journalized is typically the entry that closes the

a. revenue accounts.

b. dividends account.

c. retained earnings account.

d. expense accounts.

Answer:

The statement of cash flows will not report the

a. amount of checks outstanding at the end of the period.

b. sources of cash in the current period.

c. uses of cash in the current period.

d. change in the cash balance for the current period.

Answer:

Lyleen Boat Company’s bank statement for the month of September showed a balance

per bank of $7,000. The company’s Cash account in the general ledger had a balance of

$5,459 at September 30. Other information is as follows:

(1) Cash receipts for September 30 recorded on the company’s books were $5,700 but

this amount does not appear on the bank statement.

(2) The bank statement shows a debit memorandum for $40 for check printing charges.

(3) Check No. 119 payable to Mann Company was recorded in the cash payments

journal and cleared the bank for $248. A review of the accounts payable subsidiary

ledger shows a $36 credit balance in the account of Mann Company and that the

payment to them should have been for $284.

(4) The total amount of checks still outstanding at September 30 amounted to $5,000.

(5) Check No. 138 was correctly written and paid by the bank for $409. The cash

payment journal reflects an entry for Check No. 138 as a debit to Accounts Payable and

a credit to Cash in Bank for $490.

(6) The bank returned an NSF check from a customer for $360.

(7) The bank included a credit memorandum for $2,560 which represents collection of a

customer’s note by the bank for the company; principal amount of the note was $2,500

and interest was $60. Interest has not been accrued.

Instructions

(a) Prepare a bank reconciliation for Lyleen Boat Company at September 30.

(b) Prepare any adjusting entries necessary as a result of the bank reconciliation.

Answer:

Match the items below by entering the appropriate code letter in the space provided.

____ 1> A contractual arrangement that gives the lessee temporary use of property.

____ 2> The cash paid by the employer to the pension plan is defined.

____ 3> A contractual arrangement which is in effect a purchase of property.

____ 4> A pension plan where employee receipts after retirement are defined.

____ 5> A potential liability that may become an actual liability in the future.

Answer:

When the physical count of Rosanna Company inventory had a cost of $4,350 at year

end and the unadjusted balance in Inventory was $4,500, Rosanna will have to make the

following entry:

Answer:

Under the double-declining-balance method, the depreciation rate used each year

remains constant.

Answer:

Stockholders elect the _______________, who in turn hire the ______________ of the

company who have day to day responsibility for running the corporation.

Answer:

______________, _______________, and _______________ have debit normal

account balances whereas _______________, ________________, and

________________ have credit normal account balances.

Answer:

Journalizing and posting closing entries is a required step in the accounting cycle.

Discuss why it is necessary to close the books at the end of an accounting period. If

closing entries were not made, how would the preparation of financial statements be

affected?

Answer: